Every quarter, Carta releases information on the startup ecosystem in our State of Private Markets report. It can take a few weeks for rounds to be recorded on our platform, so we produce a full analysis after we get the final numbers.

However, we publish a “first cut” of data as close to the end of the quarter as possible. This initial work focuses on startup valuations and cash raised across venture stages.

Here’s how Q3 is shaping up for U.S. startups:

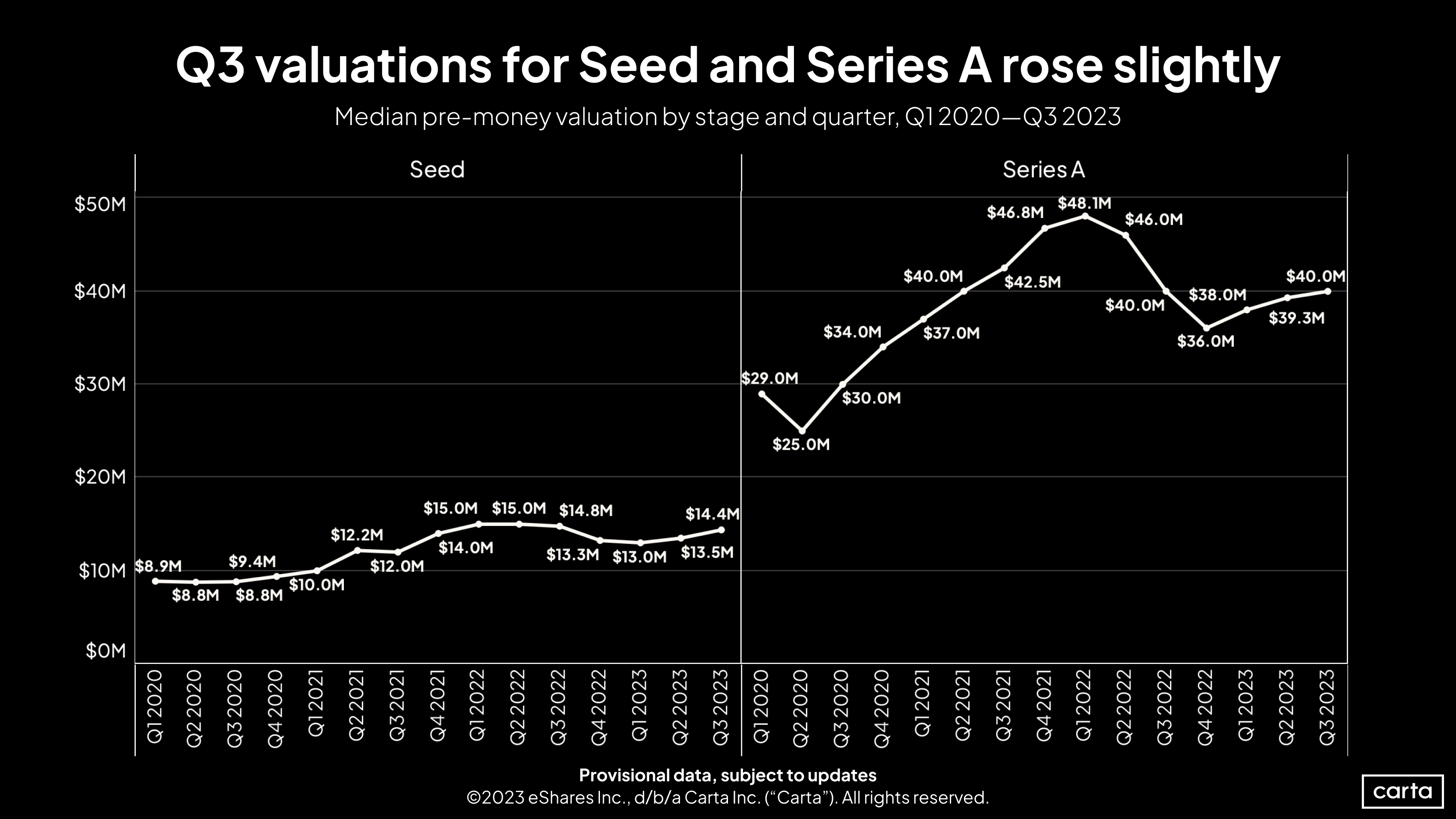

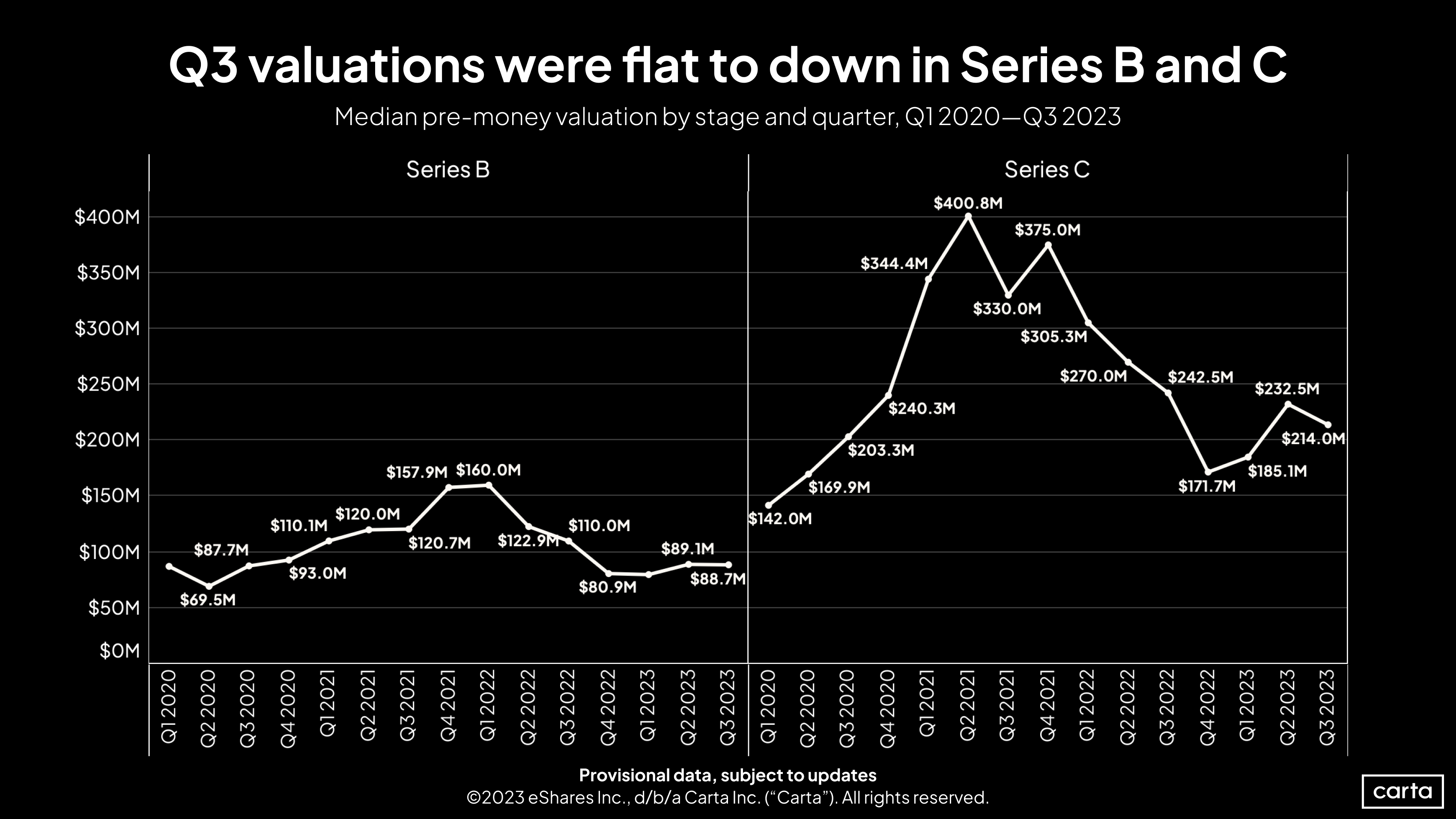

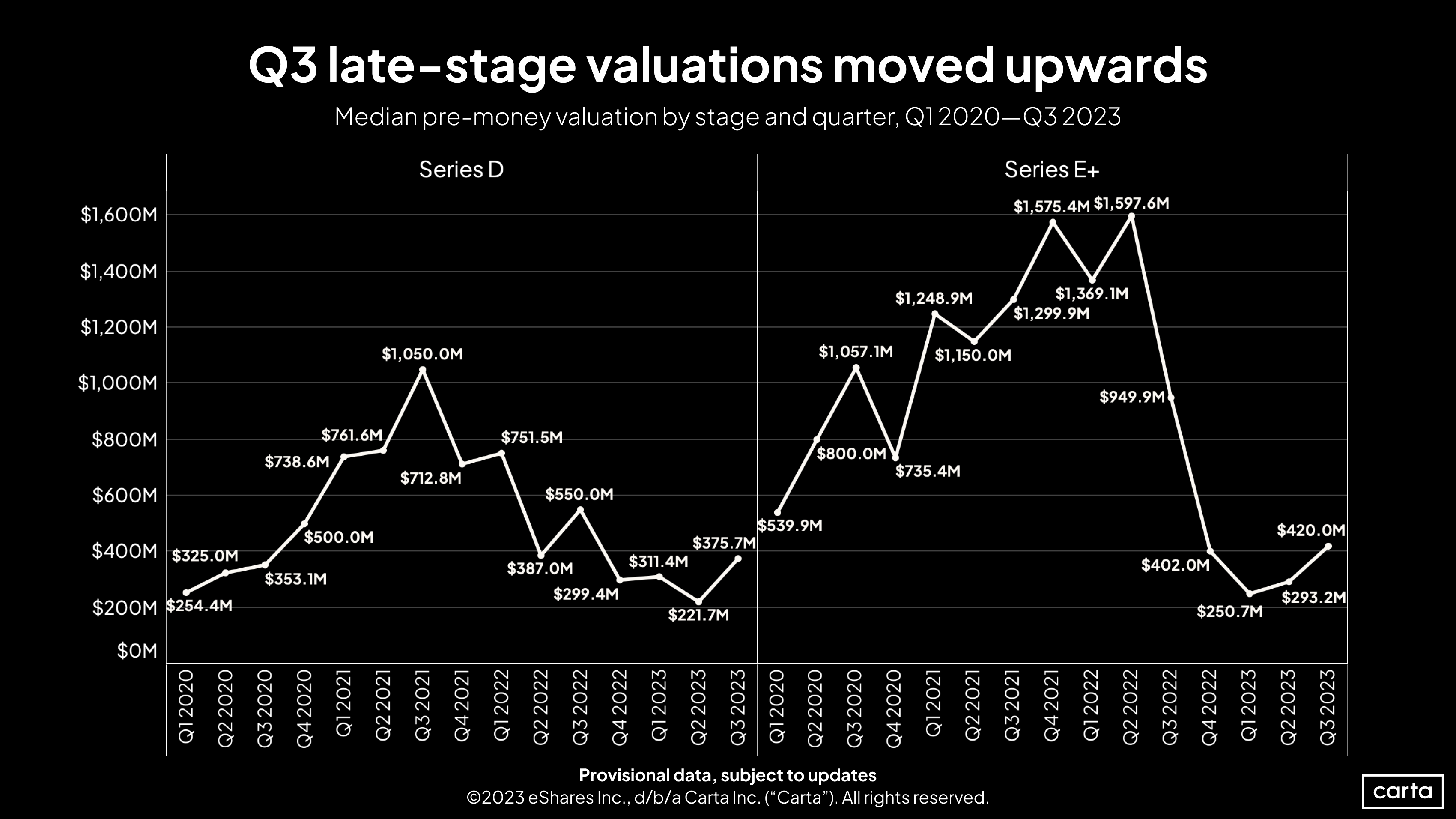

Valuations see slight increase: Median pre-money valuations ticked upward or remained flat for most venture stages from Q2 to Q3. The change was most positive for Series D and E+ rounds, though valuations at those late stages remain well off their 2021 highs.

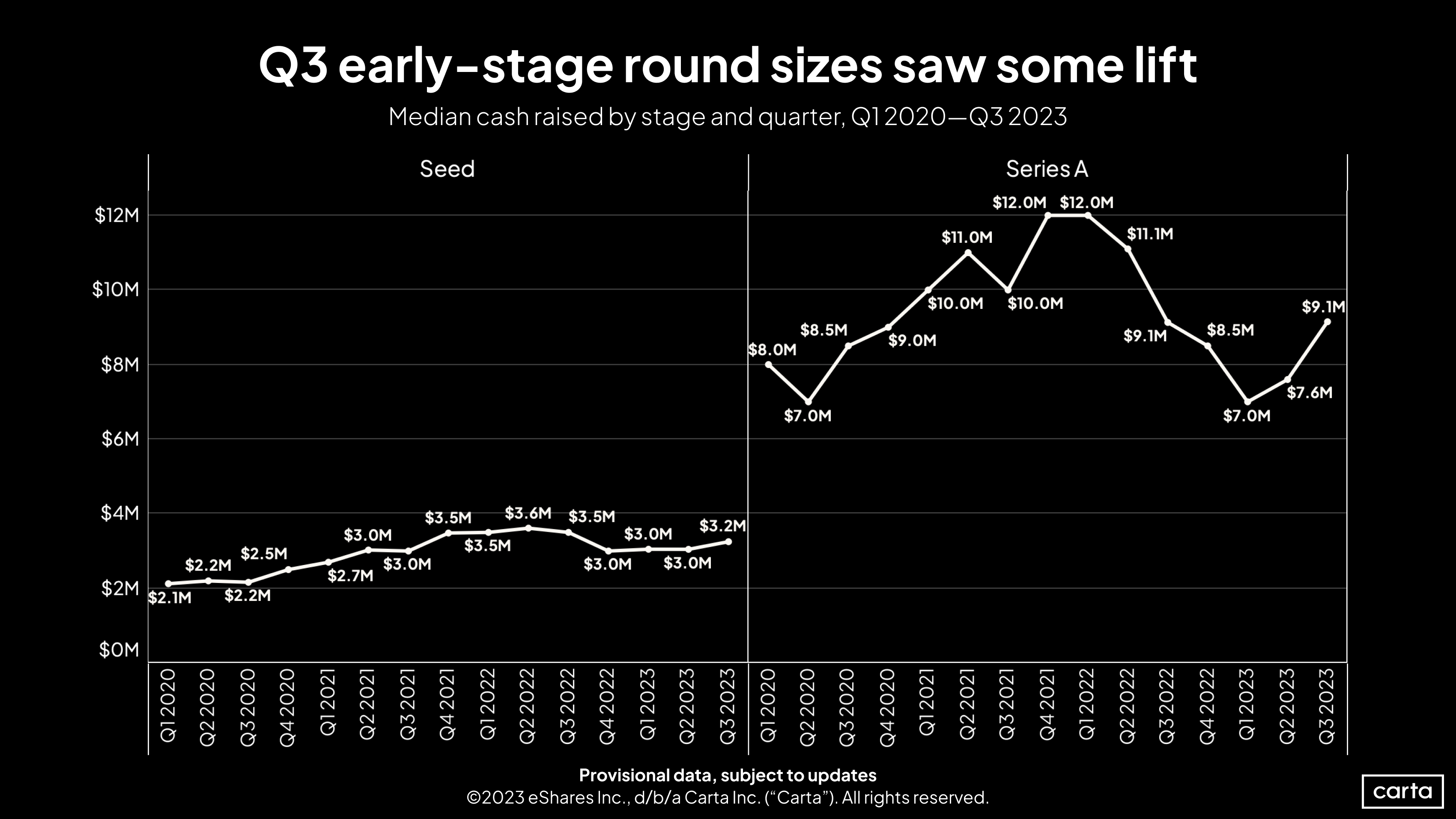

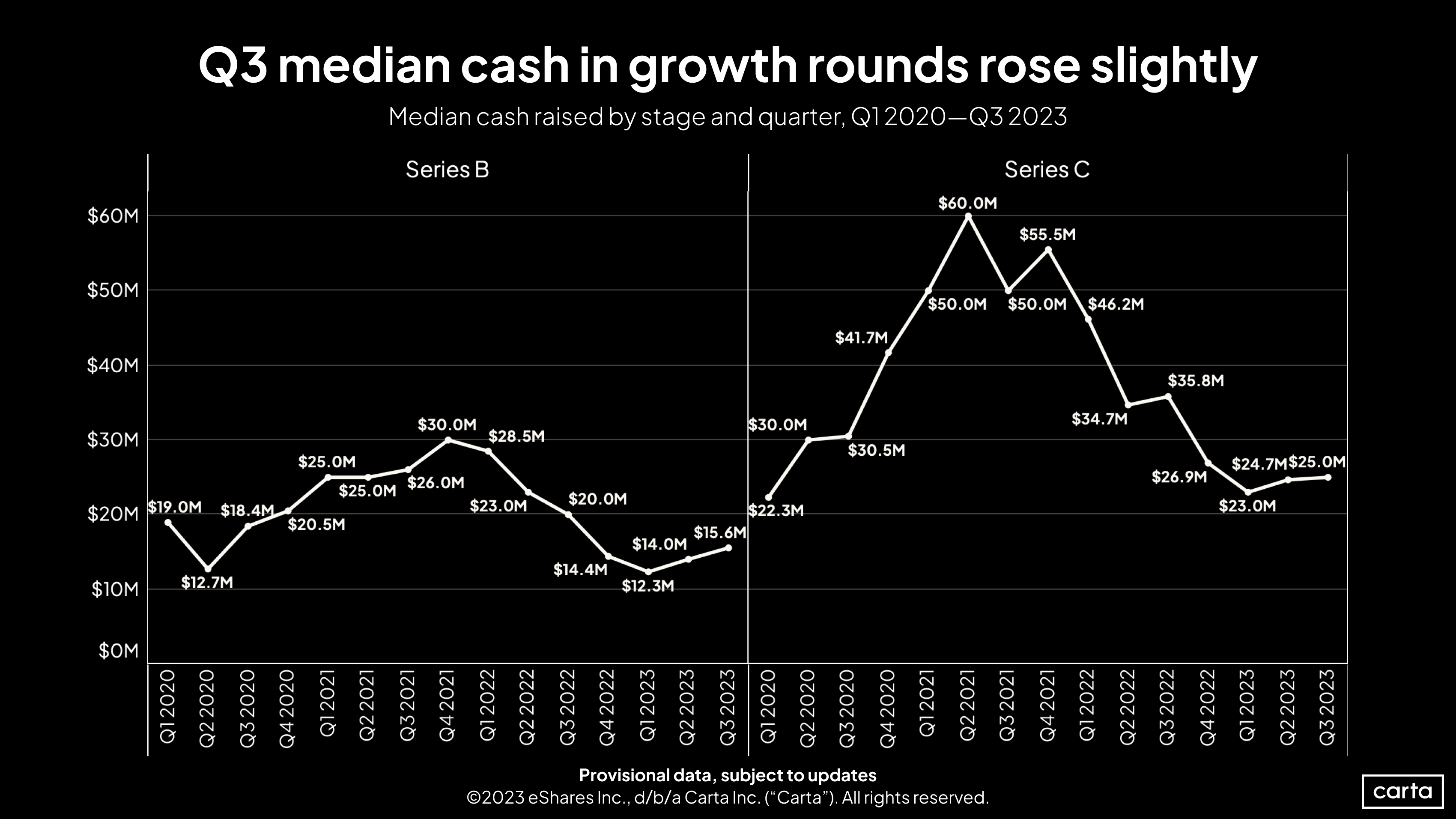

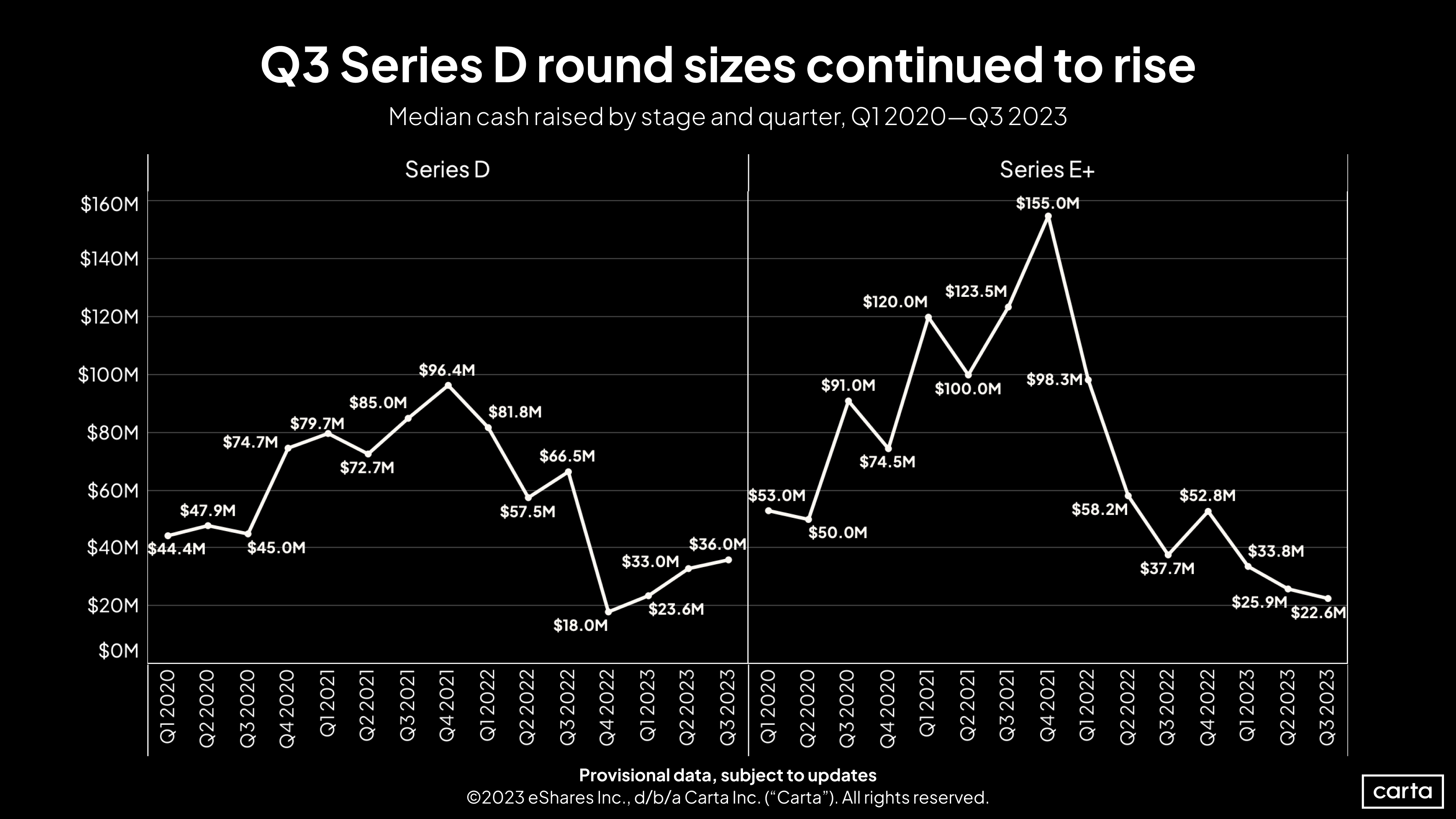

Round sizes holding steady: Median round sizes saw little change from Q2 save for some substantial growth at Series A.

Although the final numbers on total rounds and capital raised are not yet available for Q3, it may prove to be a slightly weaker quarter than Q2 for overall venture activity.

We’ll publish our full set of quarterly data in the coming weeks. To receive the full report direct to your inbox, sign up for our Data Minute newsletter.

To see the valuations and round size data below split into primary and bridge round figures, download the addendum below.

Seed & Series A

Series B & Series C

Series D & Series E+

Download the addendum

To see the valuations and round size data below split into primary and bridge round figures, you can download this addendum now:

DISCLOSURE: This communication is on behalf of eShares Inc., d/b/a Carta Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. ©2023 eShares Inc., d/b/a Carta Inc. ("Carta"). All rights reserved. Reproduction prohibited.