Healthcare startups on Carta combined to raise $23 billion in new venture funding across 1,387 individual rounds in 2024. Both of those figures are roughly in line with annual totals from 2023. After the ups and downs of the decade’s earlier years, the market for VC fundraising in healthcare seems in some ways to have settled into a new normal.

In other ways, however, the healthcare landscape continues to transform.

One of the biggest changes, investors say, is that companies are doing more with less. The rapid acceleration of the AI market in recent years has created new technological capabilities in healthcare, and after the market reset in 2022, many investors are prioritizing early-stage profitability rather than growth at all costs. This combination is causing many startups in healthcare—including the healthtech, biotech & pharmaceuticals, and medical devices sectors—to assume leaner business models.

“Founders are using AI internally to build faster and more efficiently,” says Katie Reiner Peykar, a partner at Torch Capital who focuses on the healthcare space. “We’re not seeing the same amount of engineering talent or full-time hires at the seed stage that you needed back in 2020 and 2021. Companies are executing a lot more efficiently with fewer dollars.”

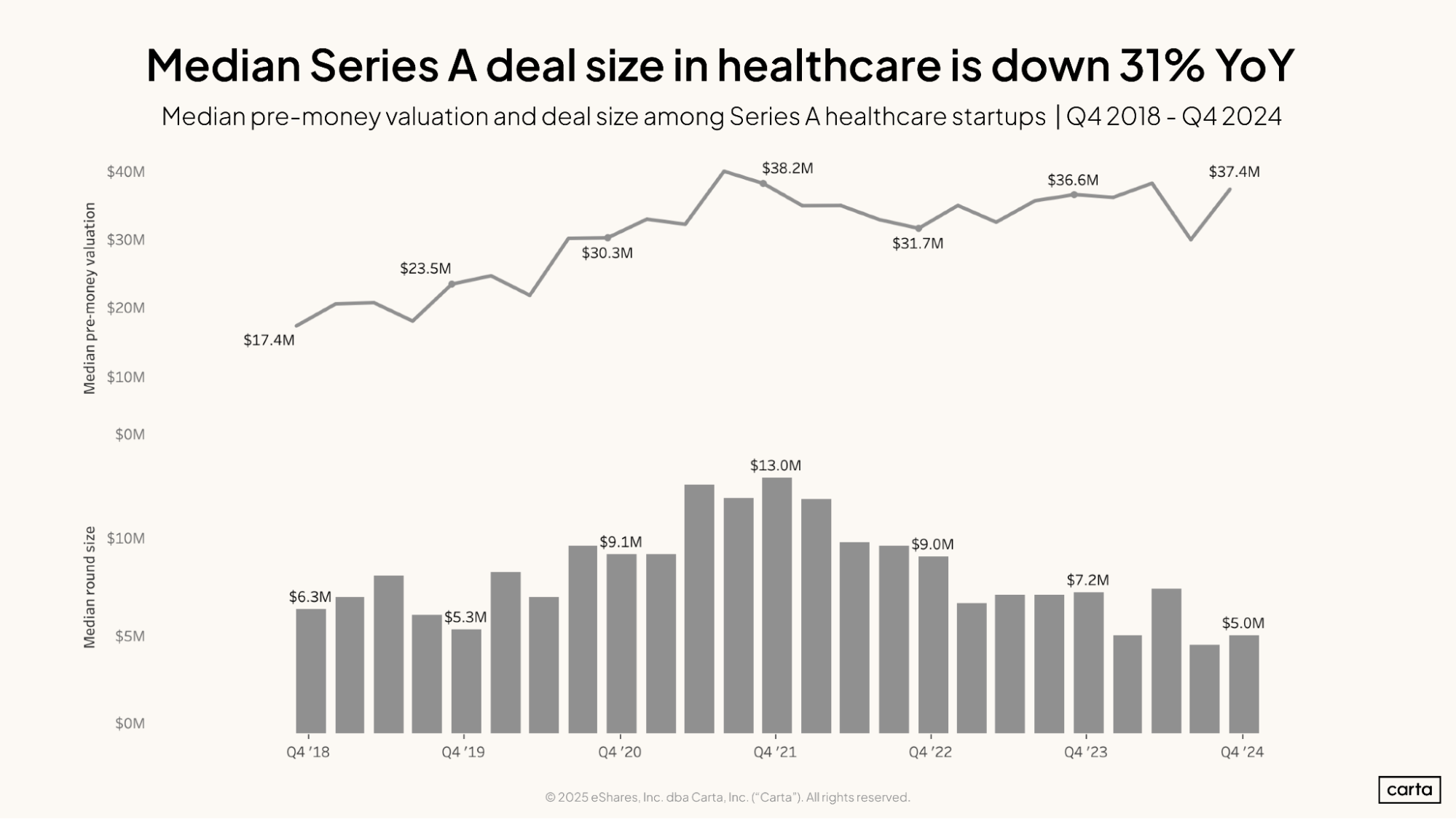

These new attitudes and strategies have manifested in smaller round sizes: In Q4 2024, the median healthcare round on Carta was 30% smaller than a year prior at the seed stage and 31% smaller at Series A. Healthcare startups are still raising plenty of venture capital. But the shape of the fundraising market continues to shift.

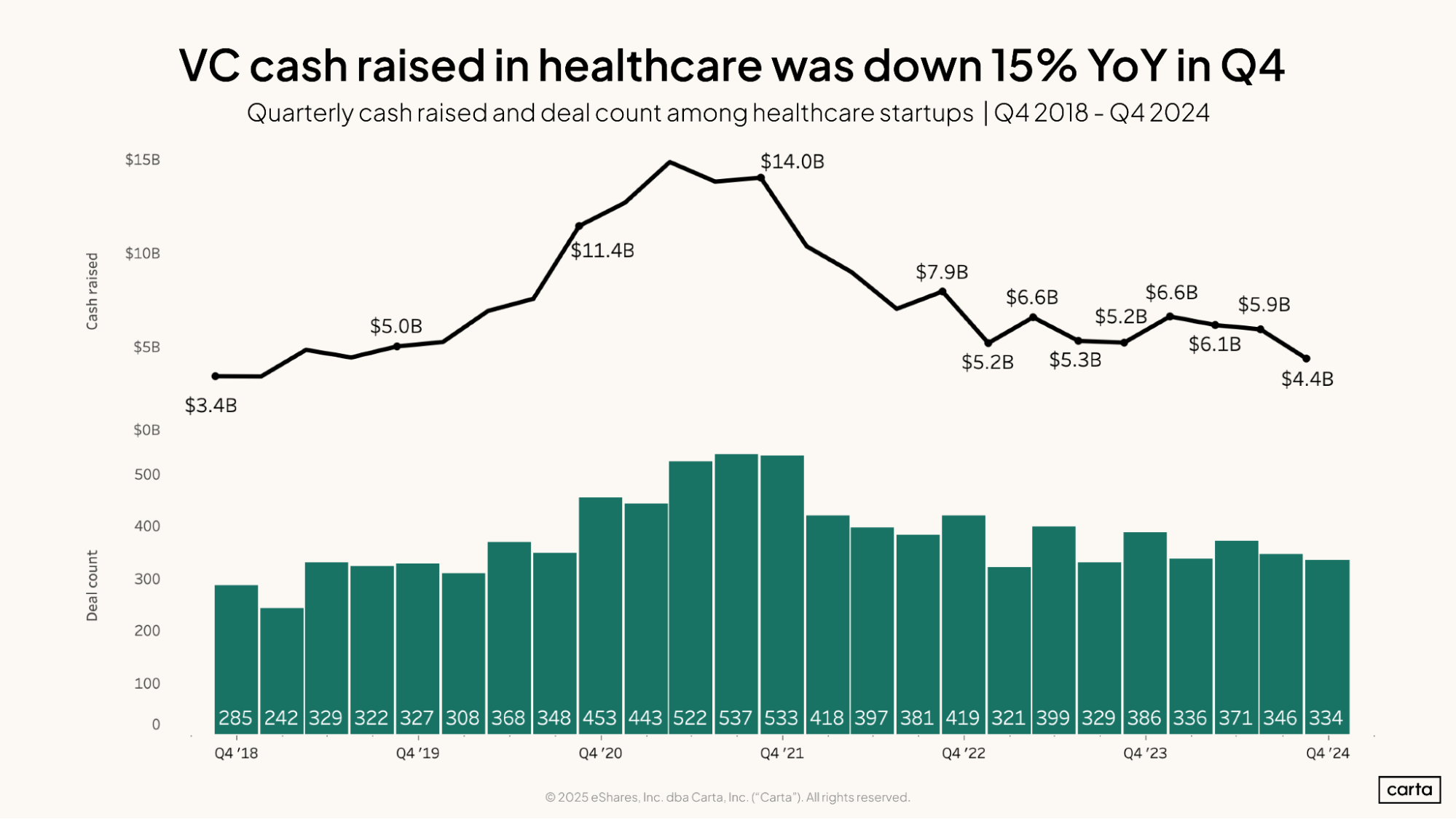

Investment in healthcare dropped in Q4: While annual fundraising totals from 2024 were in line with those from 2023, the pace of capital deployment slowed as last year progressed. Healthcare startups on Carta raised $4.4 billion in Q4 2024, compared to $6.6 billion in Q1.

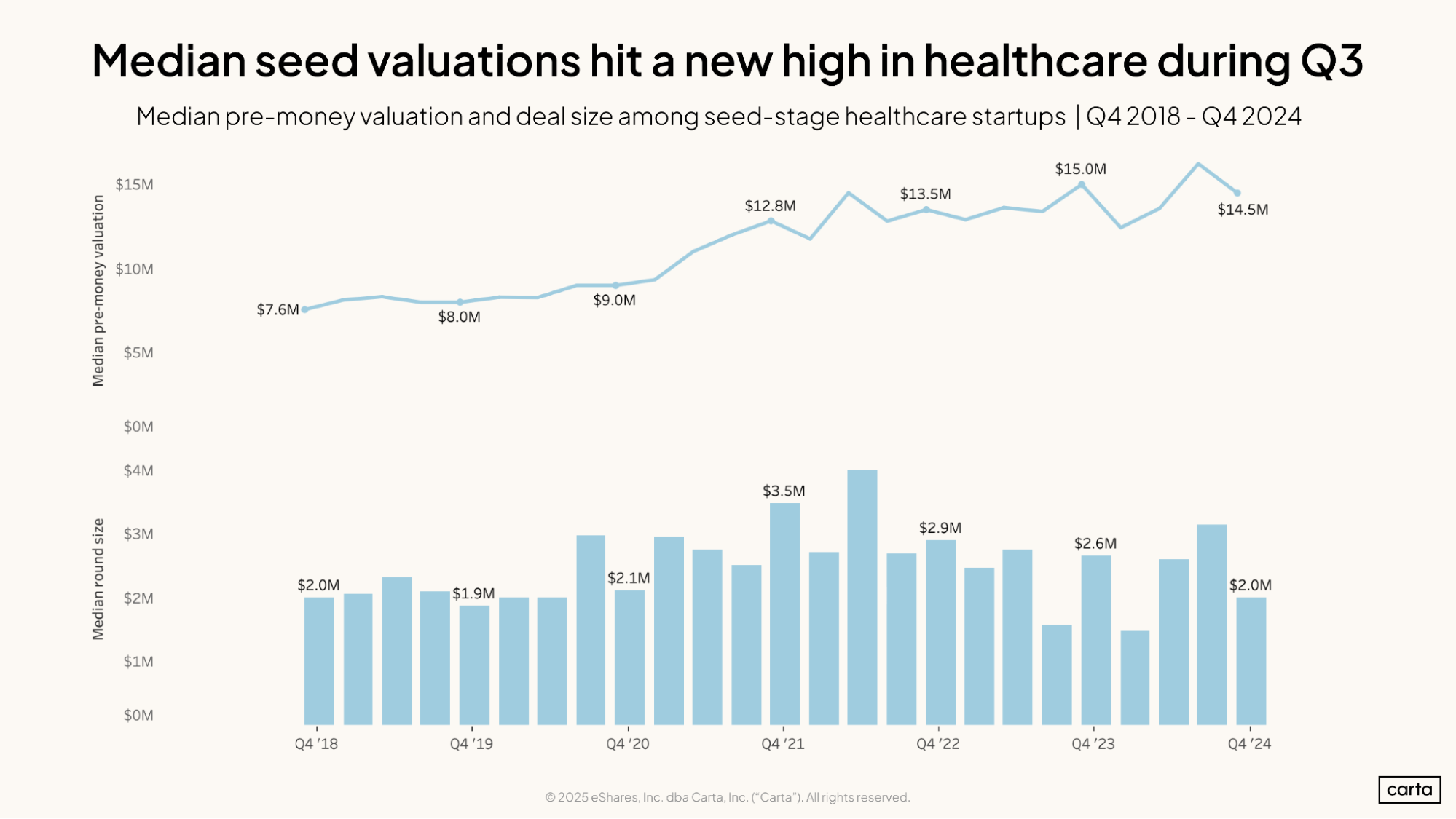

Valuations are holding steady: At both seed and Series A, valuations in healthcare ended 2024 near recent highs. The median healthcare valuation in Q4 was $14.5 million at the seed stage and $37.4 million at Series A.

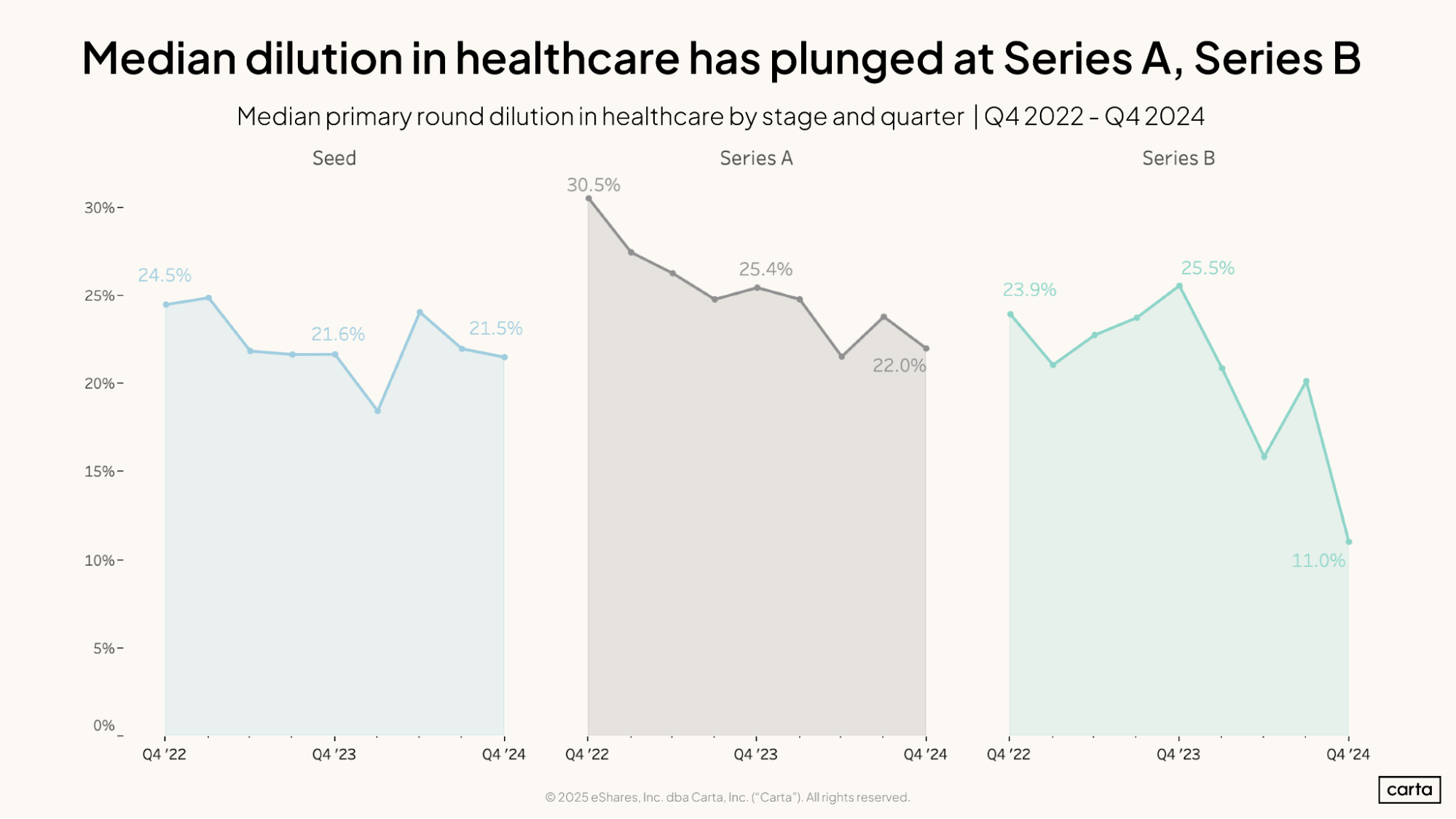

Dilution is declining sharply: Median dilution on Series A healthcare deals was 22% in Q4 2024, down from 25.4% a year prior. At Series B, median dilution fell from 25.5% to 11% over the same period.

>> Download more industry-specific data from the State of Private Markets 2024 report .

Across all stages, healthcare startups on Carta combined to raise $4.4 billion in funding across 334 new investments in Q4. The total for cash raised represents a 15% decline year over year, while deal count is down 13%. After reaching $6.6 billion in Q1, quarterly dollar count has now declined in three straight quarters

On an annual basis, there wasn’t much movement between 2023 and 2024. Total cash raised by healthcare startups rose by 3%, while the number of VC funding events fell by 3%.

Look back a little longer, however, and the difference is stark. Compared to 2021, annual deal count in healthcare was down 32% in 2024, while cash raised had fallen by 58%.

“I think there’s been a paradigm shift in early-stage investing within healthcare,” Reiner Peykar says. “In 2020 and 2021, you saw a surge of capital flowing into anything healthcare, often without a deep understanding of competitive moats and long-term scalability. Now, as we are in another potential bubble, with this AI bubble, I’m seeing both investors and founders be more discerning. We’re seeing a lot more diligence on both sides.”

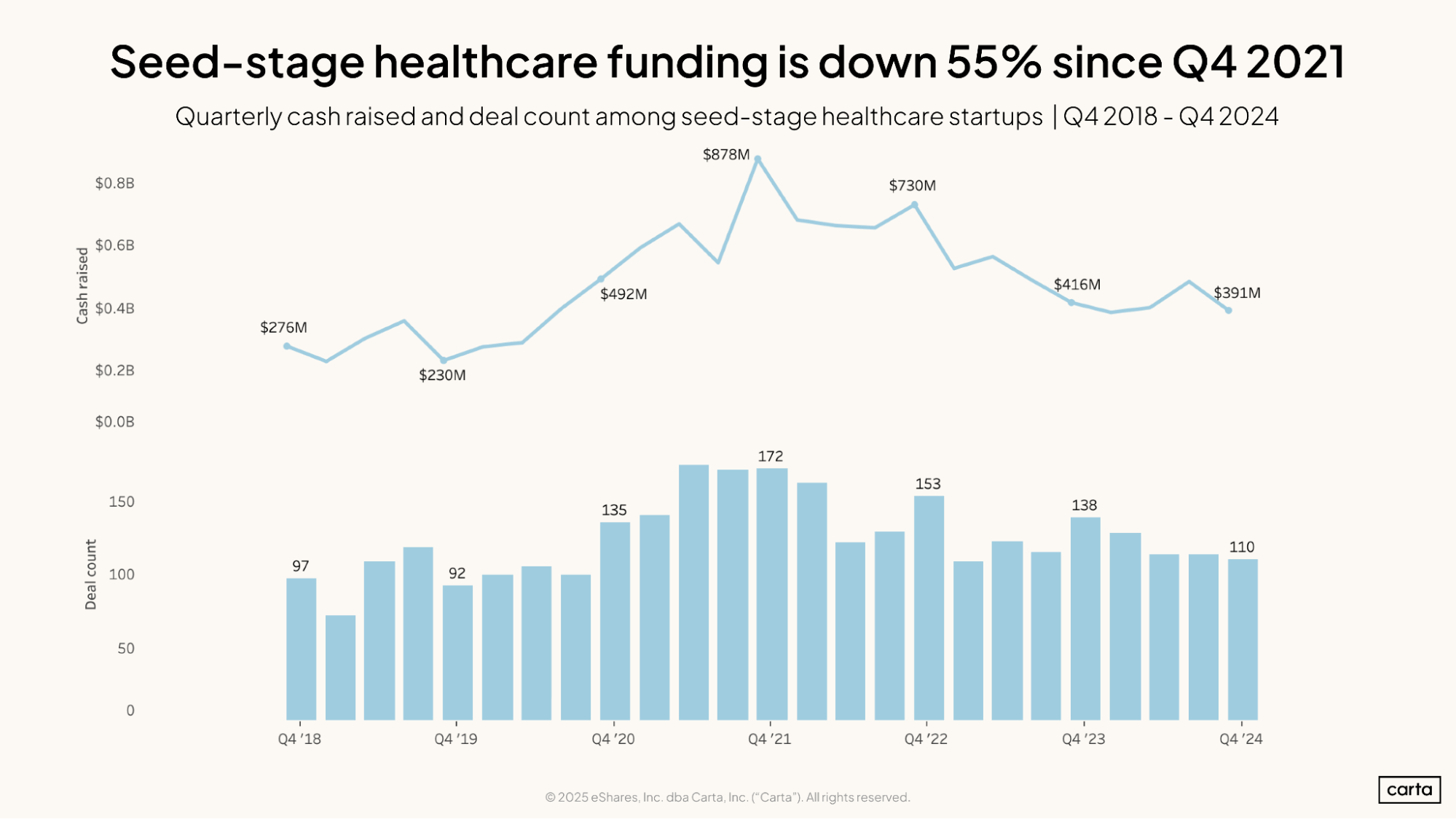

At the seed stage, both deal counts and total cash raised by healthcare startups have been trending down for the past three years. In Q4, cash raised fell to $391 million, the second-lowest figure so far in the 2020s. Compared to the recent peak of the market in Q4 2021, cash raised by seed-stage healthcare startups is down 55%.

Quarterly deal count, meanwhile, ebbed to 110, the lowest point since Q1 2023. When it comes to deciding which early-stage companies are worthy of backing, seed-stage healthcare investors were as discerning last year as at any point in recent history.

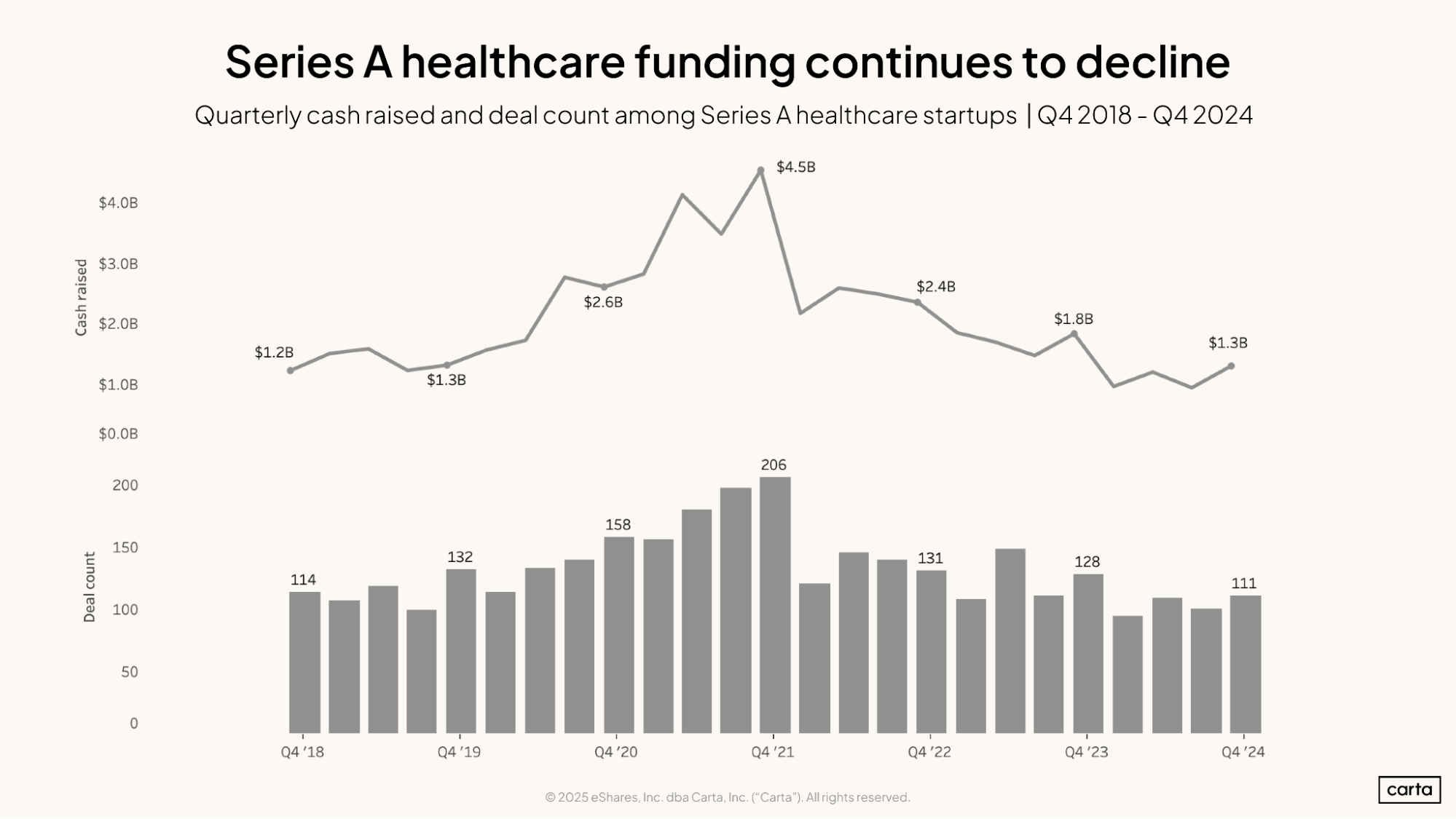

Similar trends are underway at the next stage of the traditional fundraising cycle. Total cash raised by Series A healthcare startups slipped to $1.3 billion in Q4, down 28% year over year, while quarterly deal count dropped to 111, a 13% decline.

Part of the reason for these recent declines in deal count at both seed and Series A may be that some early-stage investors are directing their attention elsewhere, according to Jack Januszewski, a vice president and healthcare investor at West Harlem Innovation Network, the social impact arm of Spring Mountain Capital. After the recent market reset, some VCs are spending more time managing their existing investments and less time pursuing new ones.

“The past few years, people are still keeping their cards pretty close to the vest,” Januszewski says. “A lot of funds are focused on portfolio management versus doing new deals.”

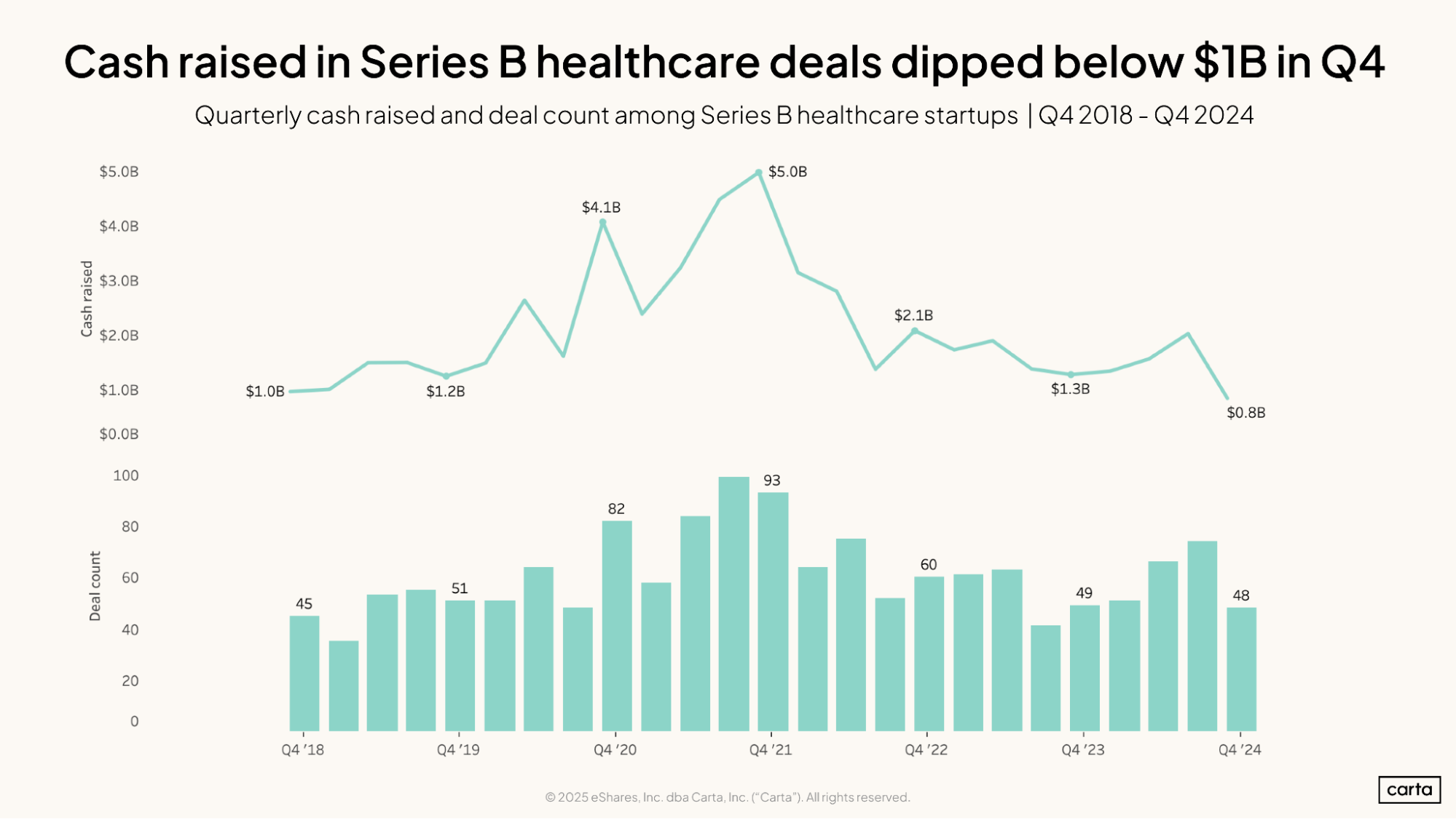

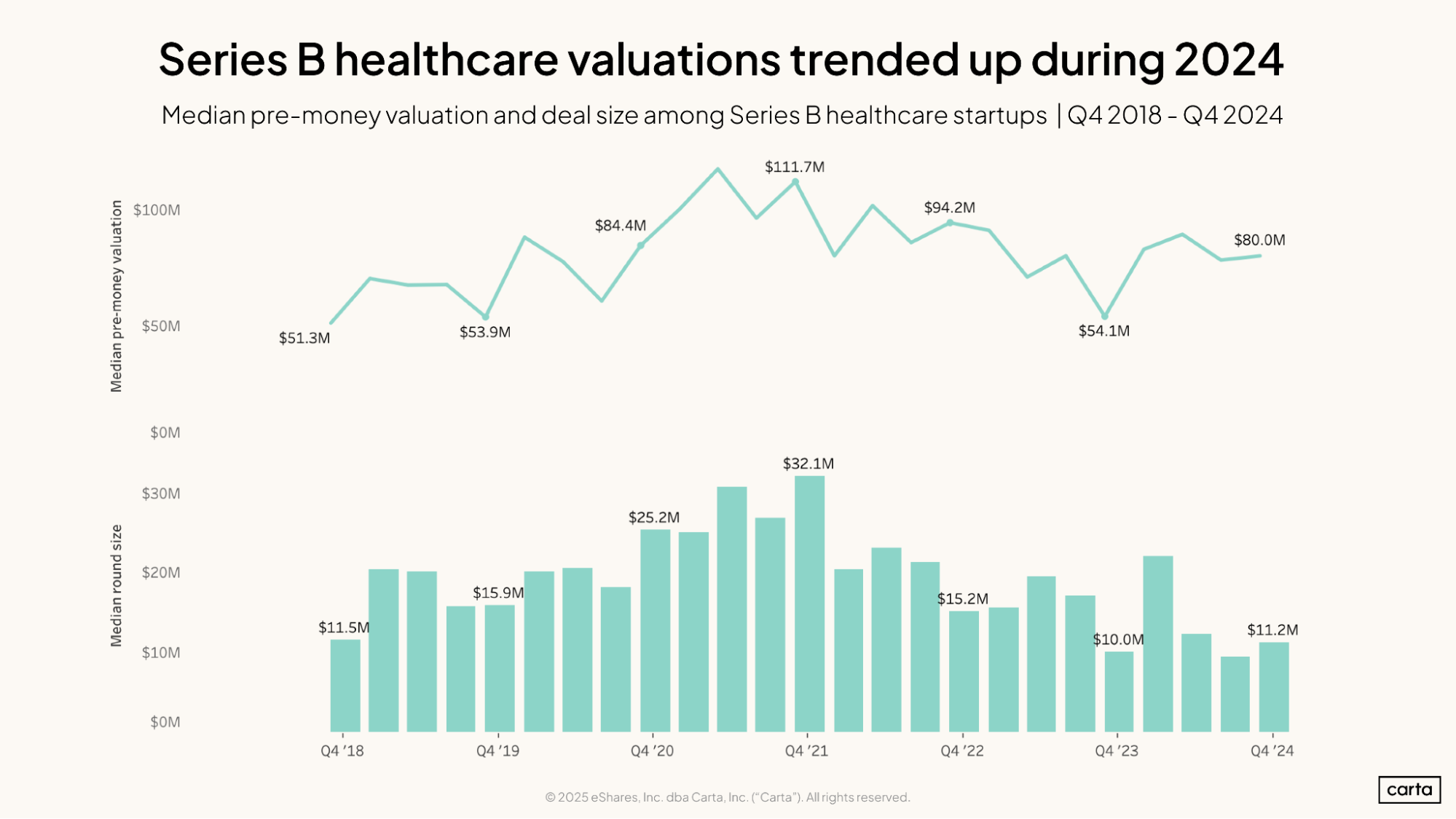

There are fewer new healthcare investments each quarter at Series B than at seed and Series A, which leaves the data at this stage more prone to quarterly swings. On an annual basis, however, last year was a mixed bag: Series B healthcare deal count was up 12% in 2024, while cash raised at the stage was down 8%.

In terms of capital raised, the Series B market has seen steeper declines from the recent heights of the market than those found at seed or Series A. Total investment in Series B healthcare was 84% lower in Q4 2024 than it was three years ago, in Q4 2021. Over that same span, seed funding has fallen by 49% and Series A funding by 68%.

Recent decreases in cash raised in healthcare are present at the company level, too. The median healthcare seed round fell to $2 million in Q4 2024, a 30% dip from the same period in 2023.

Even as round sizes, total cash raised, and the number of new deals all decline, seed valuations in healthcare remain strong. The median seed valuation did dip slightly in Q4, dipping to $14.5 million, but it still remains near recent highs.

Because seed-stage startups often lack established financials or any reliable business track record, deciding on valuations for these companies is often more art than science. This can be particularly true in healthcare, where early-stage startups may still be a long way from conducting clinical trials, navigating regulatory requirements, or going through other phases of development that may prove critical to their ultimate success or failure.

“It’s hard to arrive at intrinsic value at the earliest stages,” Januszewski says. “It’s always more of a negotiation, what feels right to you as an early-stage investor or founder knowing that you are setting up for a long-term relationship.”

Valuations also remain elevated at Series A: The median was $37.4 million in Q4 2024, up 2% year over year. Even compared to the bull-market frenzy of 2021, investors are still willing to pay high prices for some early-stage healthcare opportunities.

But as valuations inch up or hold steady, Series A round sizes in healthcare continue to decline. Reiner Peykar says that this combination—strong valuations plus smaller rounds—means that the decreases in round size aren’t proof of investor pessimism. Instead, they’re a sign of investors pushing founders to be more efficient in their early-stage spending.

“Investors are definitely more diligent about not over-capitalizing founders at the earliest stages,” she says. “They’re focused on giving founders the money they need to prove out early indicators and milestones before raising the next round.”

Between Q4 2021 and Q4 2023, the Series B healthcare market experienced a serious shakeup. Median round size declined by 69% over that span, dropping to just $10 million, while median pre-money valuation fell by 52%, to $54.1 million.

Since then, both figures have trended back up, signaling that the Series B healthcare market may have at least reached its nadir, if not begun a true resurgence. Median valuation is up a healthy 48% year over year, while median round size rose by 12%.

To calculate the dilution in a venture investment, we divide the round size by the valuation. So, an algebra question: What happens when valuations hold steady (or get bigger) while round sizes get smaller? The answer: Dilution declines—in some cases, precipitously.

Median dilution in Series A healthcare deals was 22% in Q4 2024, compared to 25.4% in Q4 2023 and 30.5% the year before that. At Series B, median dilution was just 11% in Q4 2024, a huge fall-off from 25.5% the year prior.

Reiner Peykar believes that this shift is to some degree a knock-on effect from the way healthcare startups have shifted their business models. If a company reaches profitability earlier on its journey, it can operate from a position of strength in future fundraising negotiations, which may give it the leverage to limit dilution.

“Companies are now building from the get-go with a profitability mindset, and they’re not needing the same resources to scale,” she says. “A lot of these businesses have extended runway and have passed into profitability, so they don’t need to raise a massive round like they would have, where there might have been more dilution.”

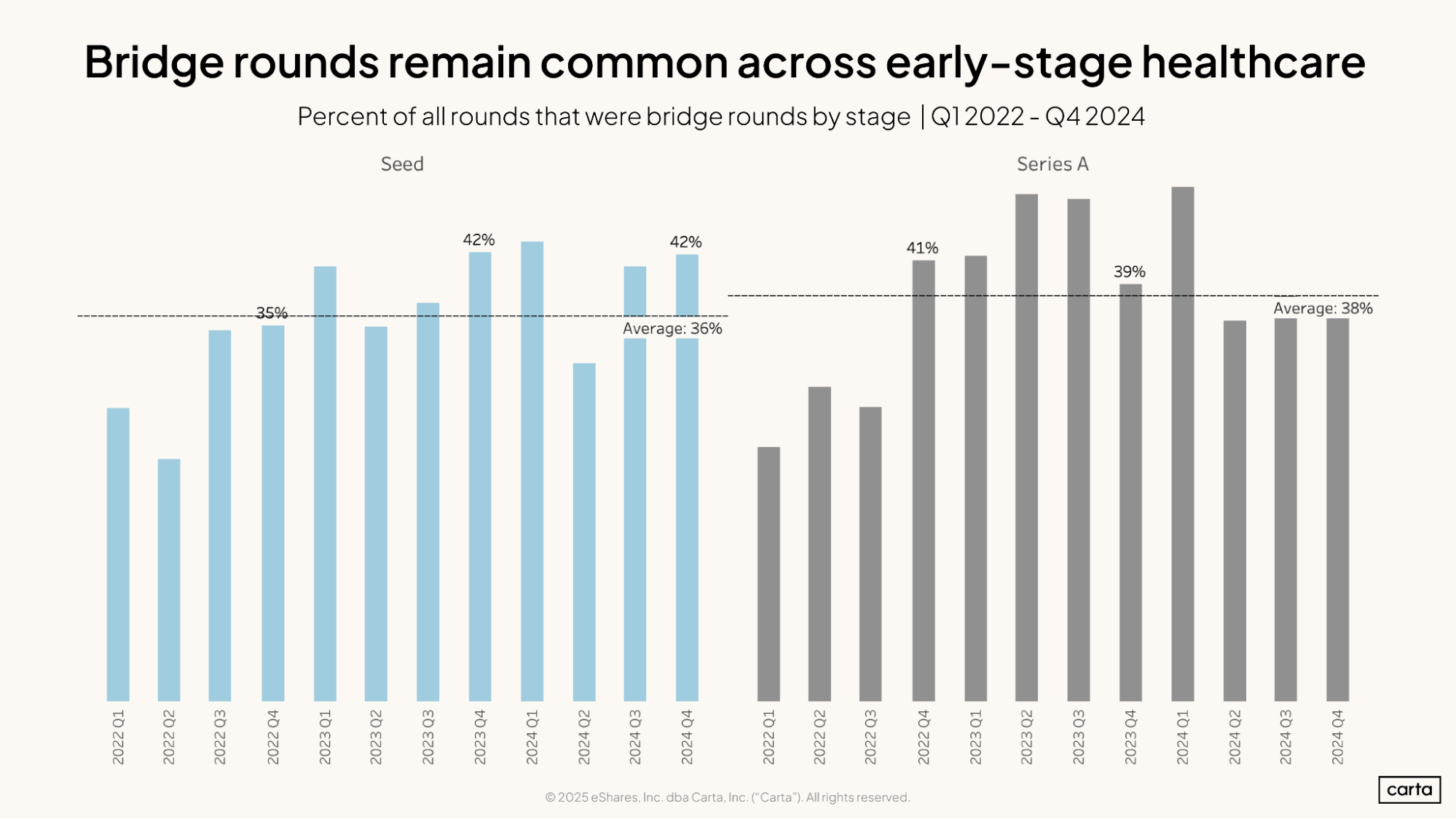

A substantial portion of new funding events across the healthcare landscape are bridge rounds. In Q4 2023, the bridge-round rate reached 42% at the seed stage and 36% at Series A.

These numbers are slightly lower than the rates of bridge rounds across VC as a whole, but not by much. Regardless of sector, about 43% of new funding events at the seed stage were bridge rounds in Q4 2024, plus another 37% at Series A.

As these types of fundings have grown more common in recent years, Januszewski says that any stigma that may have existed around bridge rounds in earlier eras has begun to fade. Instead of being seen as an inferior second choice for startups unable to raise new primary funding, bridge rounds are increasingly seen as just another strategic option that startups have at their disposal.

“At the end of the day, I think bridge rounds can make sense depending on the company,” Januszewski says. “If you’re in healthcare, particularly life sciences, and you just need a little more time to get to that inflection point of value, then a bridge round can not only be prudent, it can also be an incredibly good opportunity as an investor to grab more value.”

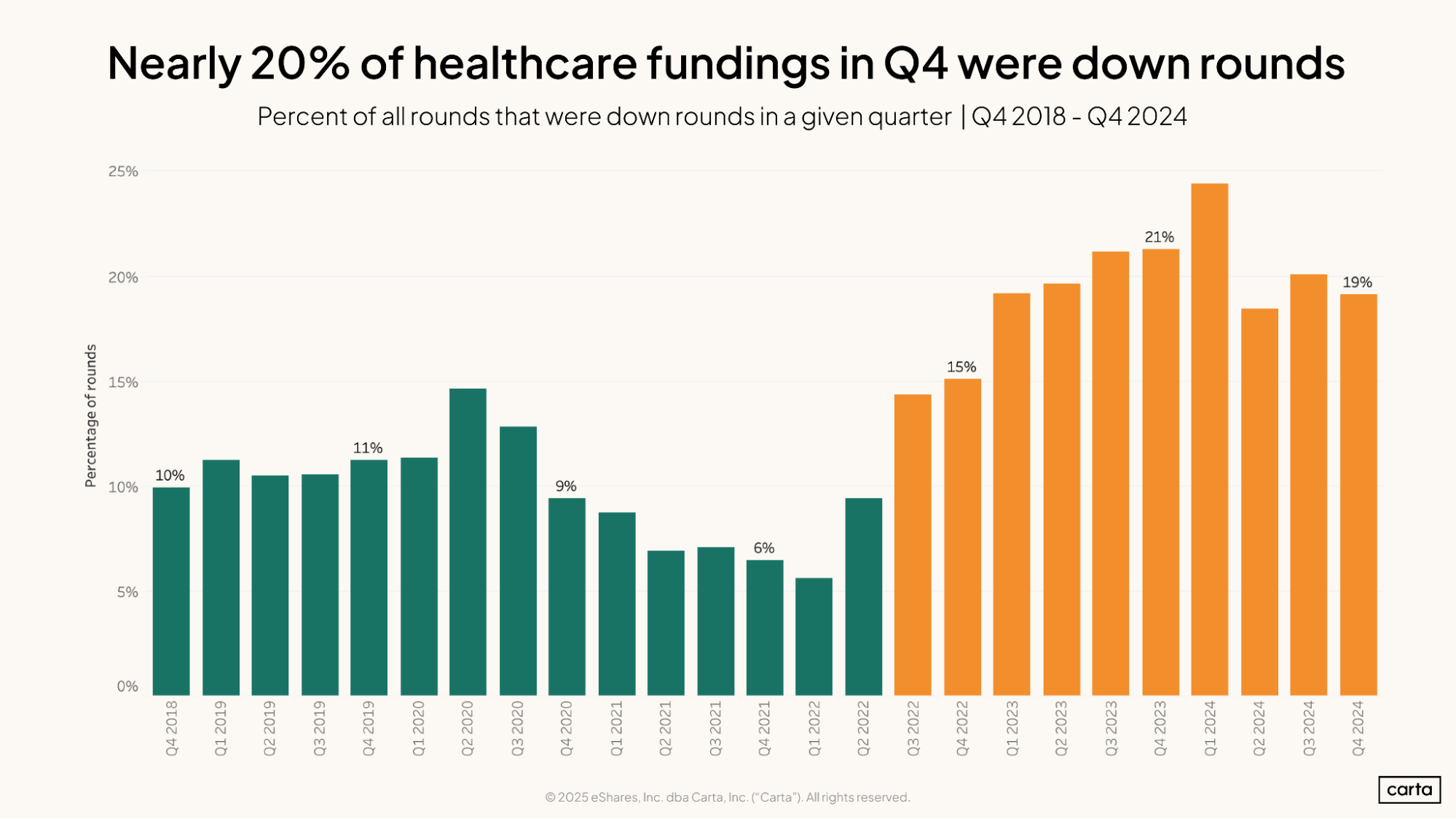

The rate of all new healthcare investments in which valuations were lower than that of the previous round declined slightly over the course of 2024, settling at 19% in the final quarter of the year. Still, down rounds remain a persistent aspect of the healthcare fundraising landscape.

Multiple years have passed since the venture market underwent a valuation reset, but it’s still the case that many startups raising new primary rounds in 2024 were doing so for the first time since the market turned. Some startups that last raised capital in a friendlier valuation environment are finding down rounds difficult to avoid.

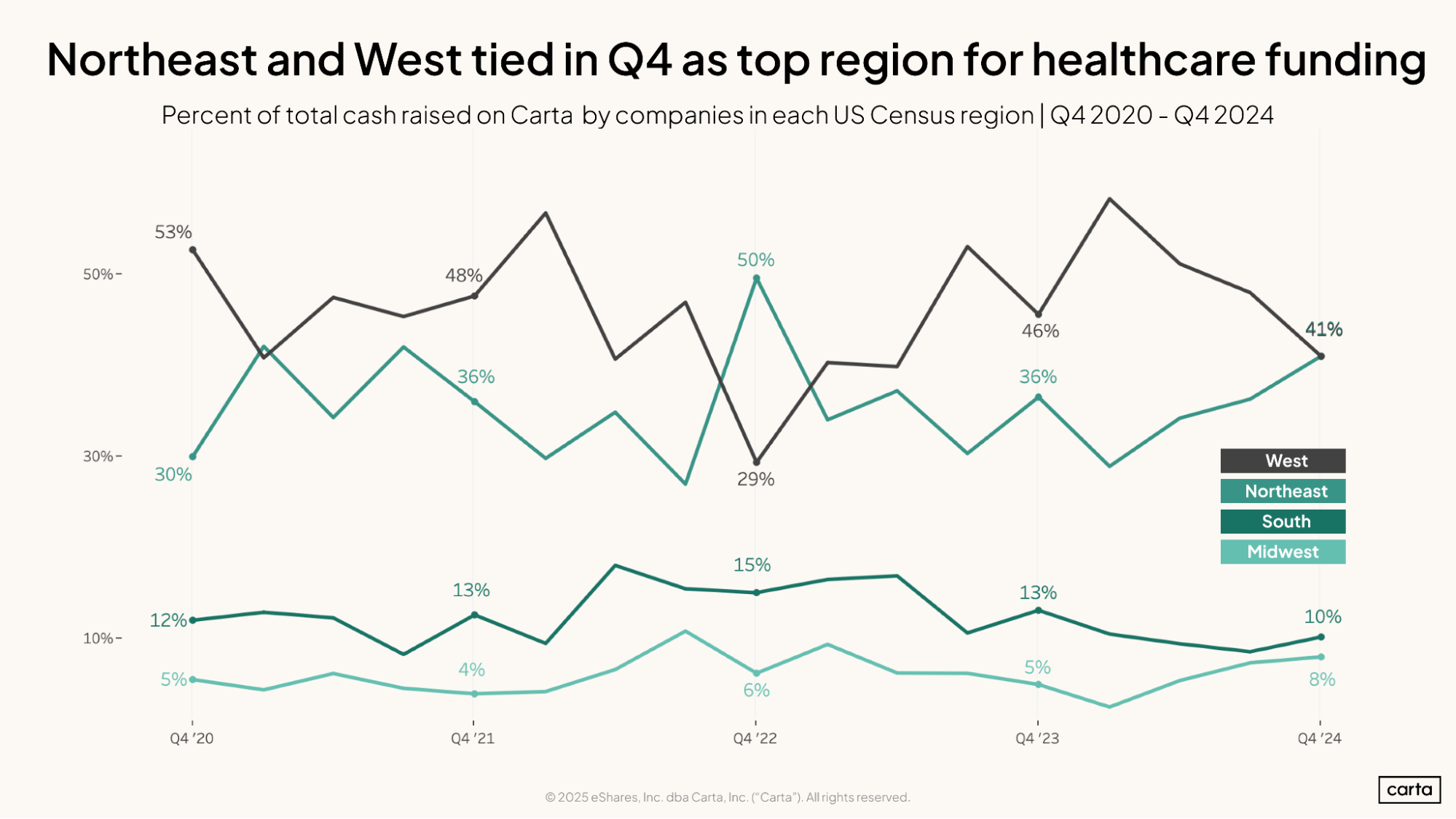

The West and Northeast each claimed 41% of all venture dollars raised by healthcare startups during Q4, tying for the top spot on the regional leaderboard. This is a shift from a recent trend of Western dominance: Previously, startups from the West census region had raised the lion’s share of all healthcare funding in 13 of the past 14 quarters.

Even with this push late in the calendar, however, the Northeast still lagged well behind the West in annual fundraising. Startups in the West raised 50% of all healthcare funding on Carta over the full course of 2024, compared to 34% for the Northeast.

Sign up for the Data Minute newsletter:

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. ©2026 Carta. All rights reserved. Reproduction prohibited.