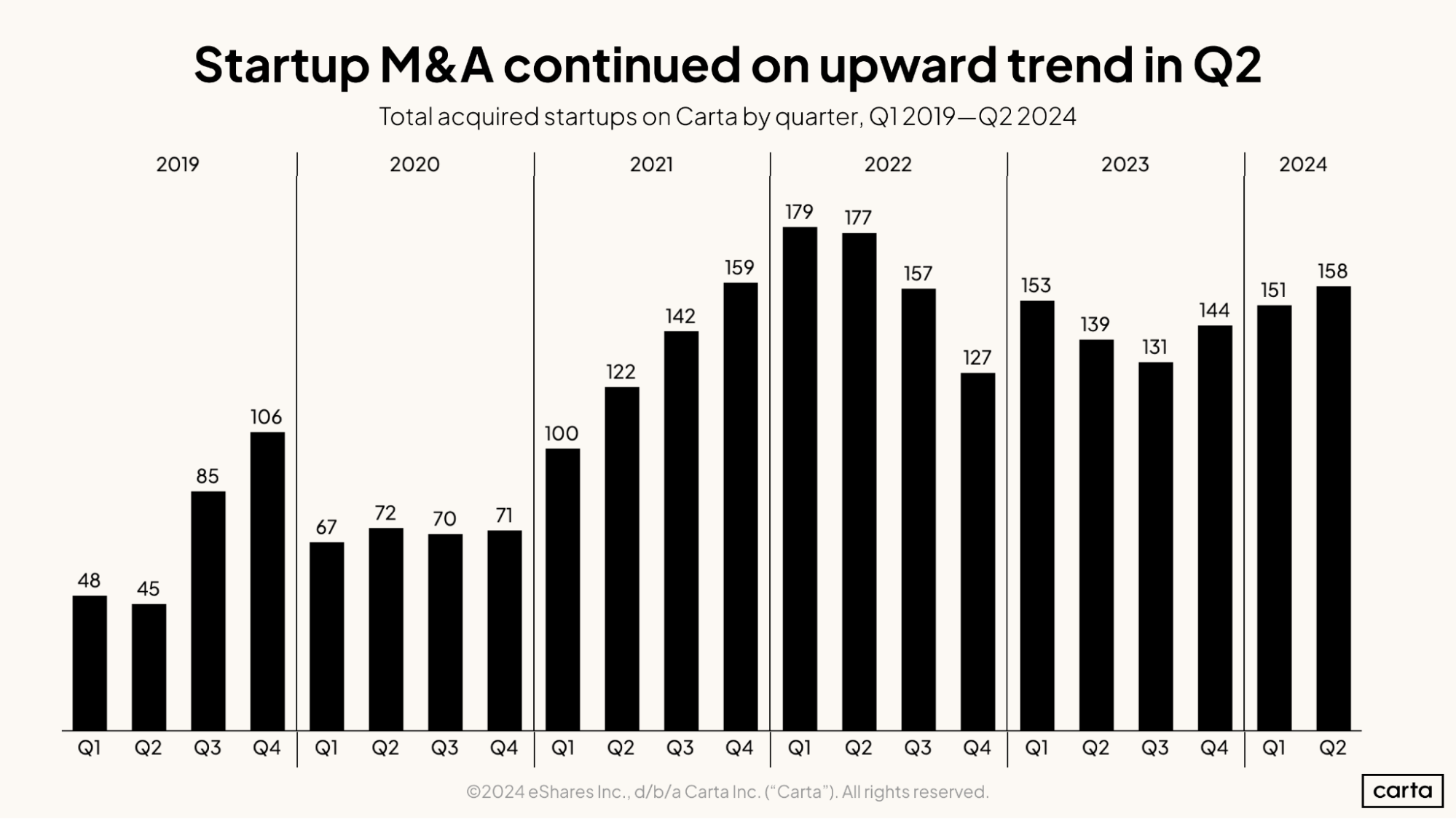

For the past two years, the rate of mergers and acquisitions targeting startups on Carta has mostly held steady. In each of the past eight quarters, total M&A deal count has landed somewhere between 127 and 158.

Within the past year, the overall trend has been a slight rise: M&A deal activity on Carta increased by 10% in Q4 2023 compared to the prior quarter, by another 5% in Q1 2024, and then by another 4% in Q2, which saw 158 M&A transactions—the fourth-highest quarterly count since the start of 2019.

In the broader M&A landscape stretching far beyond the world of venture-backed startups, the state of dealmaking remains uncertain. Global M&A activity was down about 13% year over year during H1 2024, according to S&P Global’s latest industry report. The value of all deals, meanwhile, increased by about 12% in H1.

The upshot: Even if a handful of mega-deals are driving up dollar amounts, lower transaction counts indicate the broader market is still operating with caution after the economic roadbumps of the past two years, including higher interest rates, a widespread reset in valuations, and unexpected geopolitical upheaval.

“While the overall number of transactions remains lackluster, the bigger deals are helping bring some growth to the overall value of transactions," writes Joe Mantone, lead author of S&P Global’s report.

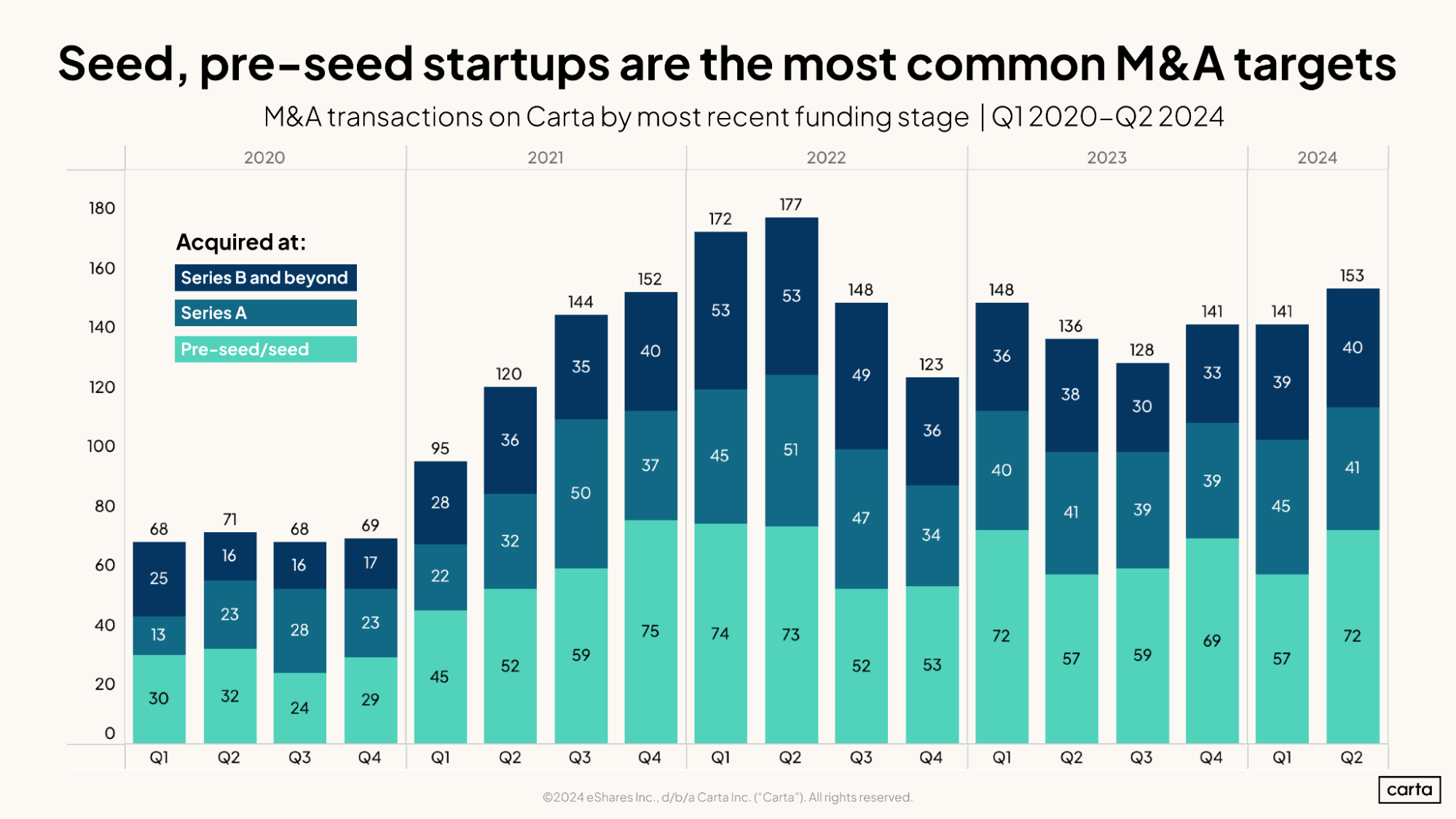

What types of startups are M&A targets?

In Q2, about 47% of startups on Carta that were acquired through M&A were at the seed or pre-seed stage. By and large, this is in line with the past few years. Companies at seed or pre-seed have accounted for somewhere between 40% and 50% of all M&A targets in 16 of the past 18 quarters.

As the wider venture capital market has slowed down over the past two years, M&A activity has shifted slightly earlier in the company lifecycle. During late 2021 and 2022, for instance, more M&A targets were at Series B and beyond than were at Series A in five straight quarters. Since then, however, that has reversed: As of today, the number of M&A targets at Series A has outstripped the number of targets at Series B and beyond for six straight quarters.

SaaS is the most populated industry segment in Carta’s database, so it makes sense that SaaS startups are also the most common acquisition targets. About 40% of all M&A targets so far in 2024 operate in the SaaS sector.

Tracking dealmaker sentiment

Earlier this year, Boston Consulting Group released its M&A Sentiment Index, a new tool that combines the latest market data with BCG’s own analysis to measure the current mood among M&A dealmakers. At its June 2024 launch, the index sits at 78, well below its average of 100, which “suggests that decision makers expect below-average activity over the next approximately six months.”

Danny Friedman, managing director and senior partner at BCG, points to several factors that have played a role in quieting M&A. Chief among them, he believes, is higher interest rates.

“Until interest rates and inflation pressures really come fully down, I don’t think we’re going to be all the way there, as far as deal activity,” Friedman says. “I think that should get better in the next six to 12 months.”

The role of regulation

But time might not heal all that’s ailing the M&A market. Friedman noted that regulators in recent years have been increasingly eager to put M&A deals under their microscopes. This can hinder those deals that are subject to regulatory challenge; it can also create a chilling effect among potential buyers and sellers who decide they don’t want to risk the trouble.

“The regulatory environment is still a headwind,” Friedman says. “Both the FTC in the U.S. and also internationally, I think the regulatory agencies are much more aggressive. And that’s a headwind that I don’t think is going to go away.”

The forecast for tech

The mood among dealmakers isn’t the same in every industry. The energy and industrials sector scores a 105 in BCG’s M&A Sentiment Index, highest of any sector the tool tracks. The tech sector checks in at a 92, second-highest among major industries.

Much of this activity, Friedman says, has been driven by companies looking to automate or digitize some aspect of their operations, including the addition of new tools and talent focused on AI.

“The technology and software sectors are pretty hot sectors, in terms of companies either buying new technologies or new capabilities,” Friedman says. “Some of the areas where we’ve seen higher levels of activity are technology, energy, healthcare, and consumer.”

A dearth of exits

Startups looking to achieve an exit and return capital to their shareholders typically have two primary options: An M&A deal or an IPO. And at the moment, the IPO market is looking even chillier than the market for M&A.

Through August 22, just 85 companies valued at $50 million or more had gone public in the U.S., combining to raise $23.3 billion in IPO proceeds. Extrapolate those totals out to the full year, and you’d get 132 public offerings and $36.1 billion in proceeds.

Both of those totals would surpass 2023’s counts of 108 IPOs and $19.4 billion in capital raised. But they would also be a far cry from the levels of activity that were common in venture capital through much of the 2010s and early 2020s. In 2015, for instance, 275 companies valued at $50 million or more conducted IPOs, and they combined to bring in $85.3 billion as a result.

If and when the IPO market picks back up in the coming months, it could provide a boon to the startup M&A market, too. When it comes to investors being eager to invest their capital in young tech companies, a rising tide tends to lift all boats.

“When IPOs are going up, it means there’s more confidence in the market. Investors are buying into new technologies and smaller companies,” Friedman says. “And when there’s great enthusiasm for investing in new technologies and new capabilities, that can help drive M&A activity, too.”

Get the latest data

Sign up for the Carta Data Minute newsletter to receive the latest data on VC financings, valuations, compensation, and more:

DISCLOSURE: This communication is on behalf of eShares, Inc.,dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. All product names, logos, and brands are property of their respective owners in the U.S. and other countries, and are used for identification purposes only. Use of these names, logos, and brands does not imply affiliation or endorsement. ©2024 eShares, Inc. dba Carta, Inc. ("Carta"). All rights reserved. Reproduction prohibited.