A global pandemic. A bull market for the ages. The first extended venture slowdown in more than a decade. For startups and the venture capitalists who fund them, the past three years have been an era of upheaval.

These macro twists and turns have contributed to a cascade of smaller changes in the venture market. Some of these changes are related to geography: Thanks in no small part to the proliferation of remote work and the growing acceptance of pitching your startup over Zoom, the venture capital industry has grown more geographically diverse in recent years.

This trend is particularly significant at the seed stage. As today’s seed startups continue to grow and raise new rounds of funding, they will become tomorrow’s Series A, Series B, and Series C companies. At any given moment, the current seed crop is a preview of what the broader venture market may look like in years to come.

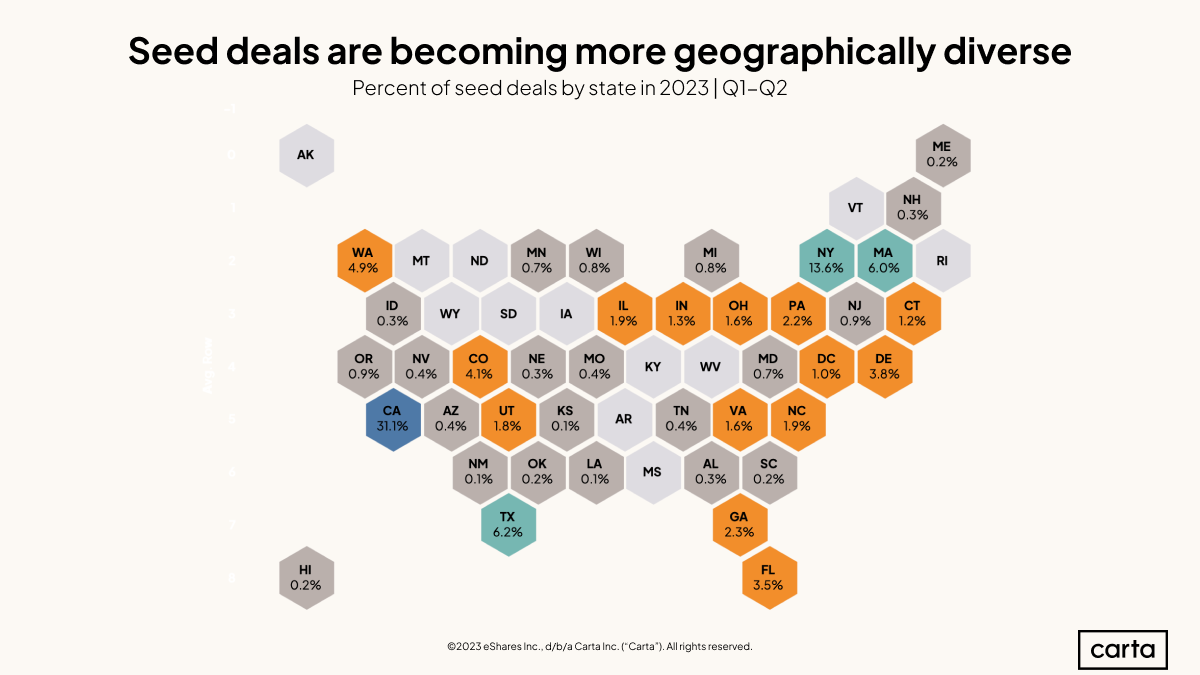

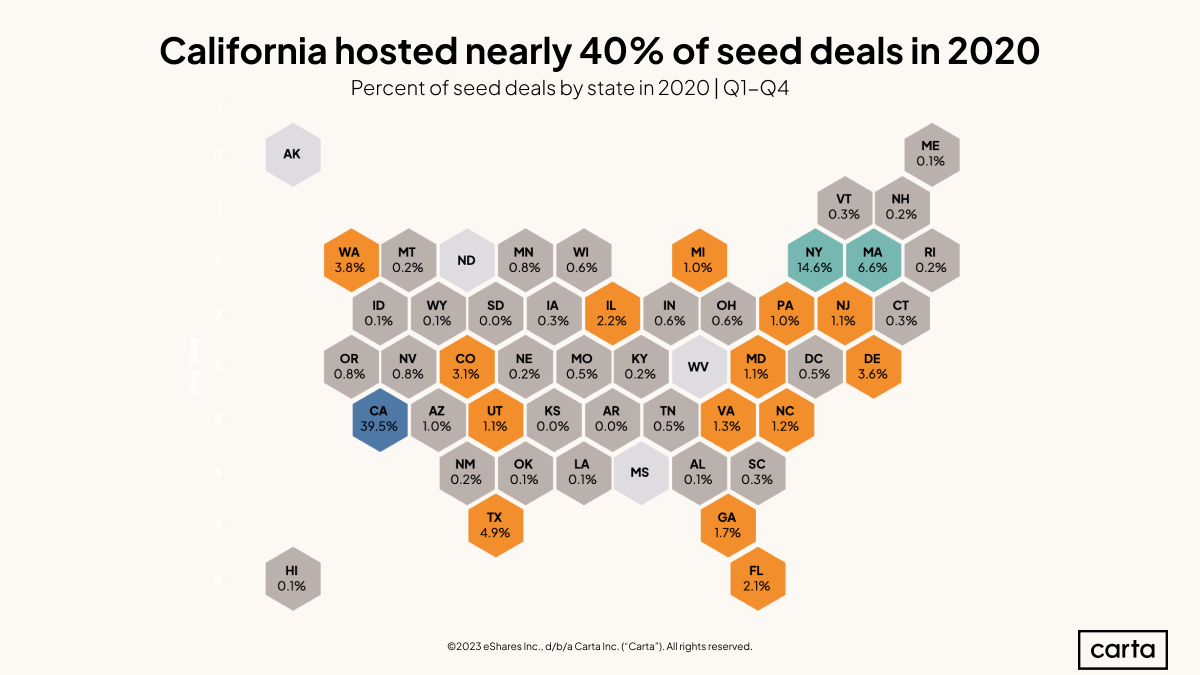

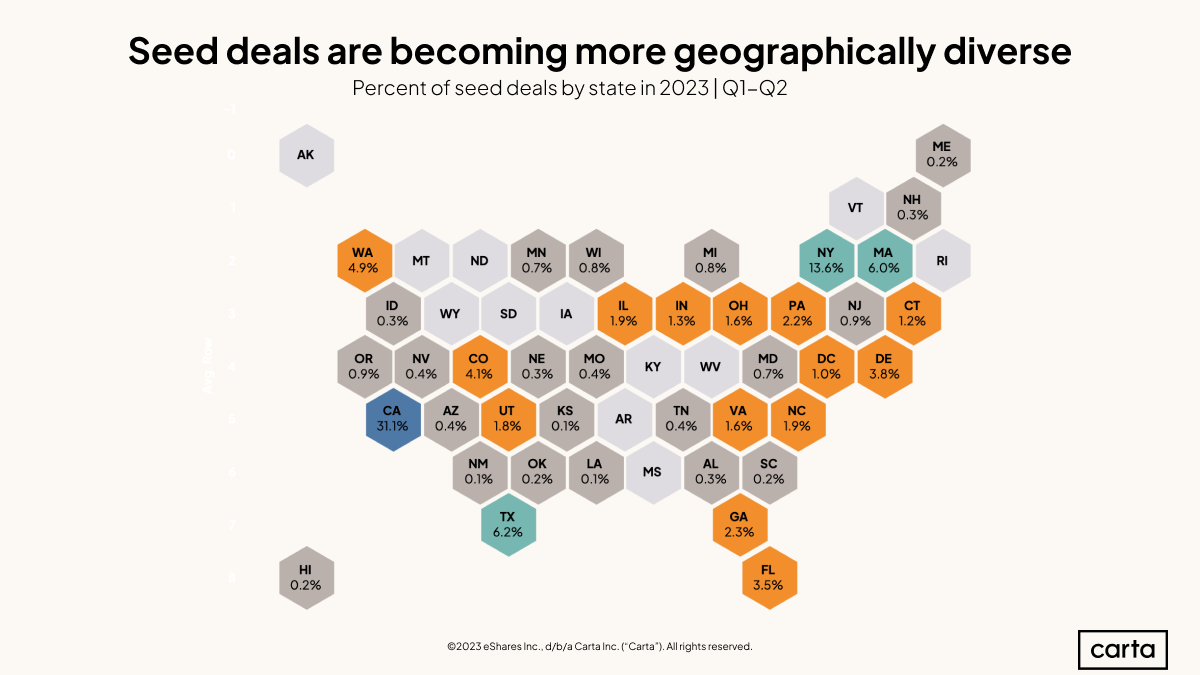

To quantify these recent geographic shifts—and to glean some insights on how the VC industry may continue to change—we compared a map of how seed deals on Carta were distributed throughout the U.S. in 2020 to the same map for the first six months of 2023.

Several significant changes stood out. Some of these shifts are probably due in part to the continued growth of Carta’s database. But they also signal that the future of venture capital funding in the U.S. could look different from its past.

2020

2023

1. California is still king

Startups based in California have raised 31.1% of all seed rounds in the U.S. so far this year, more than twice as many deals as any other state. But the gap between California and the rest of the country is shrinking. Between 2017 and 2020, California was home to at least 37% of all seed deals on Carta. That figure fell to 33.8% in 2021 and 31.4% in 2022 before dipping again this year.

There’s no doubt that California remains a venture capital powerhouse, thanks to the presence of Silicon Valley and other hubs like Los Angeles and San Diego. (It’s also the most populous state in the Union.) But as the venture industry continues to grow and mature in the 2020s, other states are gaining ground.

2. Florida’s climb continues

Florida startups raised 2.1% of seed rounds in the U.S. in 2020. So far this year, that rate has risen to 3.5%, resulting in a 1.7x increase in Florida’s share of seed activity in the nation over the past three years. Only Indiana (2.17x), Pennsylvania (2.2x), and Ohio (2.67x) had larger increases over that span.

Go back a little further, and the trend is even more pronounced. Back in 2018, Florida logged less than 1% of all seed investments in the U.S. Since then, its share of the market has been on a steady upward trajectory.

3. Texas cracks the top three

Texas has been home to 6.2% of seed fundings so far this year. That’s up from 4.9% in 2020, and it’s the Lone Star State’s largest share dating back to at least 2017. It’s also the third-highest percentage of any state in 2023—the first time on record that Texas has ranked so highly.

In recent years, Massachusetts has had a stranglehold on the No. 3 spot, trailing California and New York. But seed funding in the traditional healthcare hotspot has declined relative to the rest of the country—Massachusetts has a 6% share of all U.S. seed activity so far this year, down from 6.6% in 2020. That’s still fourth-highest of any state, but it’s no longer enough to hold off Texas.

4. An increase in seed deserts

In 2020, only four states—Alaska, Mississippi, North Dakota, and West Virginia—played host to zero seed investments on Carta. So far this year, the count of seed-free states is up to 12—nearly 25% of all states in the country.

To be clear, this is only through six months, and it’s likely that some of those 12 states will see at least one seed investment before the year is up. But this statistic suggests a possible counterpoint to the assertion that the venture environment is growing more geographically diverse. While the diversification argument certainly holds true in some ways, there are plenty of states where startup deals are still few and far between.

5. The South takes a leap

Texas and Florida are leading the way. But an upswing in seed funding is underway across much of the South. The 16 states (plus Washington D.C.) that comprise the South census region combined for 17.7% of all seed investments on Carta in 2020. So far this year, that share of deal count is sitting at 22.2%, with Virginia, North Carolina, and Georgia among the other states that have seen their share of seed activity increase.

That 22.2% figure from the first half of 2023 is well above the 18.4% share of venture capital activity across all stages that the South claimed in 2022. A higher rate of seed activity in the South could signal that later stages of the startup lifecycle are also poised for more growth there in the years to come.

6. Colorado hits new heights

In the West census region, Colorado is another state with a growing presence on the VC scene. Startups in Colorado have raised 4.1% of all seed rounds in 2023, its highest rate since at least 2017.

This is a notable increase since 2020, when Colorado claimed 3.1% of seed activity. On a shorter timeline, it’s even more significant. Seed funding in Colorado had fallen off in both 2021 and 2022, with its share of seed deals dipping to 2.9% and 2.5%, respectively. So far this year, that trend has reversed course.

And it isn’t only seed startups: Colorado companies across all stages have been drawing increased investor interest in 2023.

Get weekly insights in your inbox

The Data Minute is Carta’s weekly newsletter for data insights into trends in venture capital. Sign up here:

DISCLOSURE: This communication is on behalf of eShares Inc., d/b/a Carta Inc. (“Carta”). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. ©2023 eShares Inc., d/b/a Carta Inc. (“Carta”). All rights reserved. Reproduction prohibited.