Private companies frequently offer equity compensation as a tool to attract employees. Depending on the type of company, they can deploy their equity in different ways.

The cadence of when equity grants vest is one key difference—and that can depend on how the company is structured. Private equity firms typically invest in companies that are structured as corporations, or as limited liability companies or LLCs. (In venture capital, a subset of private equity in which firms typically take a minority interest rather than a majority stake, the firms usually invest in corporations.)

At PE-backed corporations, for instance, monthly vesting schedules are most common, once the employee has reached certain time-based conditions. This means that employees receive a new portion of vested options each month, providing a consistent stream of financial enticement.

At PE-backed LLCs, on the other hand, annual vesting schedules are the norm. In these instances, employees receive a new portion of equity awards once a year, which can place a particular emphasis among employees on reaching each new annual milestone.

Is your company structured as a corporation, or as an LLC? Is it backed by venture capital investors, or by private equity? Are you part of a management team, or a rank-and-file employee? If your company offers equity compensation, the answers to all of these questions might impact the vesting schedules of any equity grants you receive.

>> See the 2025 PE Executive Equity Report

How vesting schedules differ

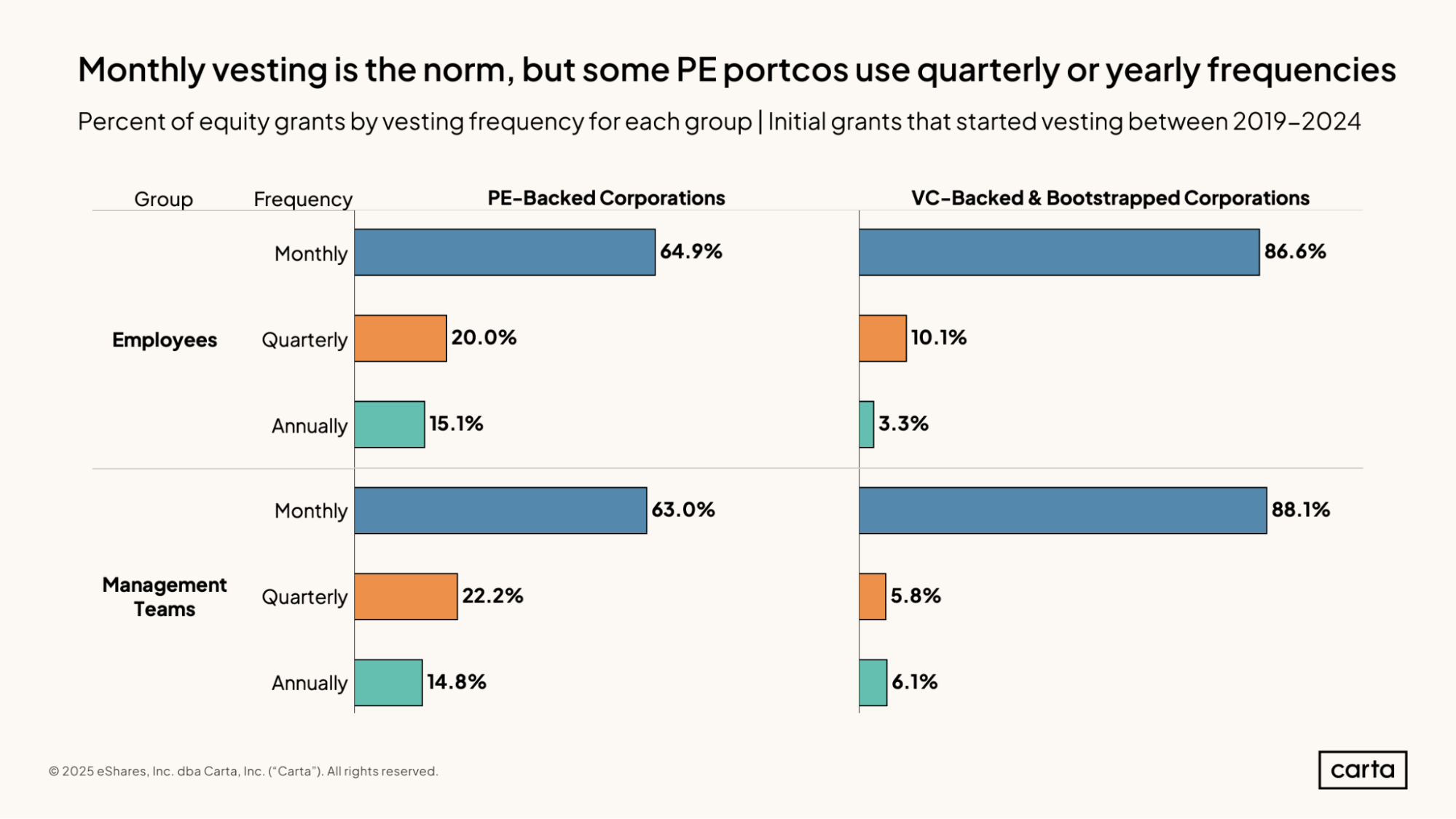

Among both management teams and standard employees, a little less than two-thirds of equity grants issued at private equity-backed corporations are on monthly vesting schedules. About one in five grants issued by PE-backed corporations vest on a quarterly basis, while a slightly smaller portion of grants vest annually.

This is directionally similar to the breakdown of vesting schedules at corporations that are either bootstrapped or backed by VC investors. But this universe of VC-backed companies is significantly more reliant on monthly vesting schedules. Among management teams at VC-backed and bootstrapped corporations, about 88% of equity grants vest monthly, versus just 6% each for quarterly and annual vesting.

Compared to PE-backed corporations, these VC-backed and bootstrapped corporations are more likely to be young startups that are trying to rapidly gain traction and drive early-stage growth. VC-backed corporations may also be more likely to be found in buzzy industries where the battle for top performers is particularly fierce, such as AI. These condensed timelines and the need to compete for talent may be two reasons why VC-backed corporations show such a clear preference for monthly vesting.

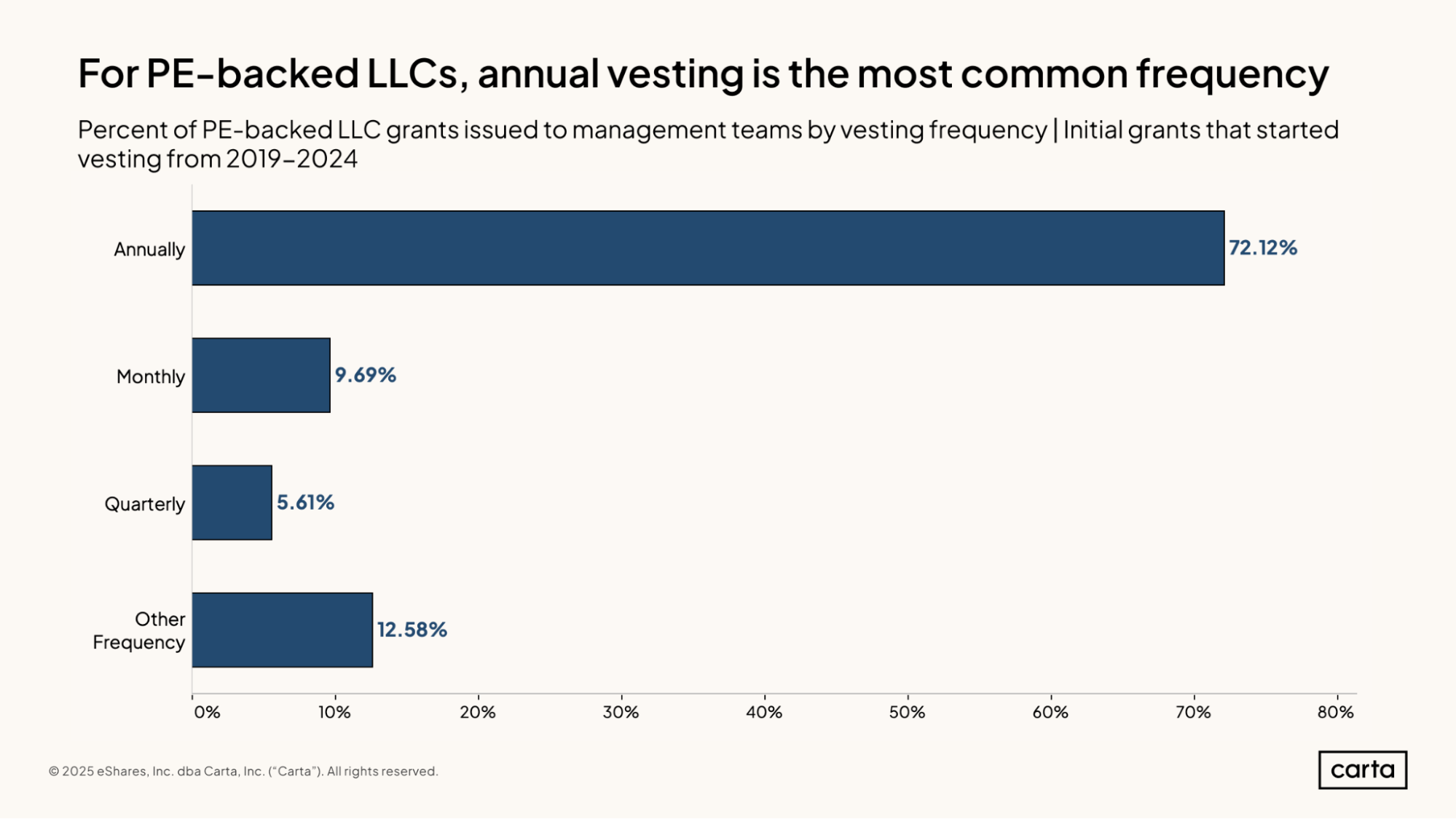

At PE-backed LLCs, meanwhile, monthly vesting schedules are far less common than they are at corporations. Instead, among this population of companies, annual vesting is the norm. About 72% of LLC grants issued to management teams from 2019 through 2024 had annual vesting schedules, compared to less than 10% with monthly vesting.

Part of the reason for this difference in vesting schedules is the structural differences between corporations and LLCs. While most corporations issue equity grants in the form of stock options or stock units, LLCs are instead more likely to issue profit interest units. These are more likely to be linked to a company’s annual financial results, which can make them better-suited for annual vesting.

Annual vesting schedules are also typically easier to manage for company finance teams and back offices, including simpler tracking for tax purposes. And, in general, it’s common for LLCs to have fewer administrative resources than corporations. For a smaller company, annual vesting is sometimes the simpler option.

How vesting cliffs differ

For the first year of employment, it often doesn’t matter whether equity vests monthly, quarterly, or annually. Before an employee begins to receive any equity at all, it’s common that they must first clear an initial cliff.

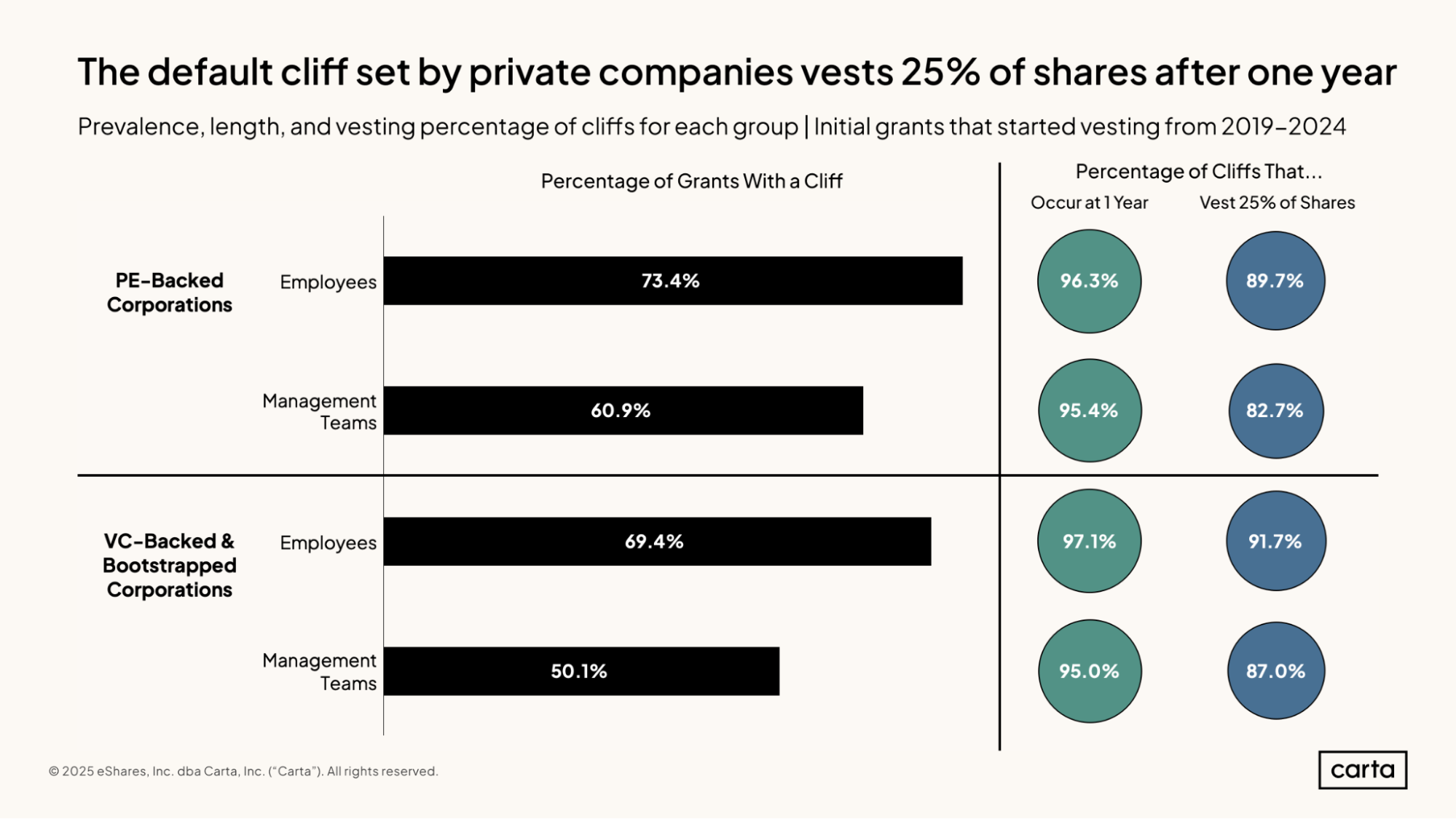

At PE-backed corporations, 73.4% of all grants issued to employees and 60.9% of grants issued to members of management teams have a cliff. At VC-backed and bootstrapped corporations, 69.4% of employee grants and 50.1% of management grants have a cliff.

For both types of companies, the vast majority of cliffs that exist—at least 95%—occur at the one-year mark.

The basic purpose of a cliff is to incentivize a long-term commitment (or at least a medium-term one) from employees. From the employee perspective, a one-year cliff can be a motivation to ride out any initial turbulence while acclimating to a new position. From the company perspective, a one-year cliff can function as a sort of probationary period, giving managers the option to assess performance over an extended stretch of time before employees gain a place on the cap table.

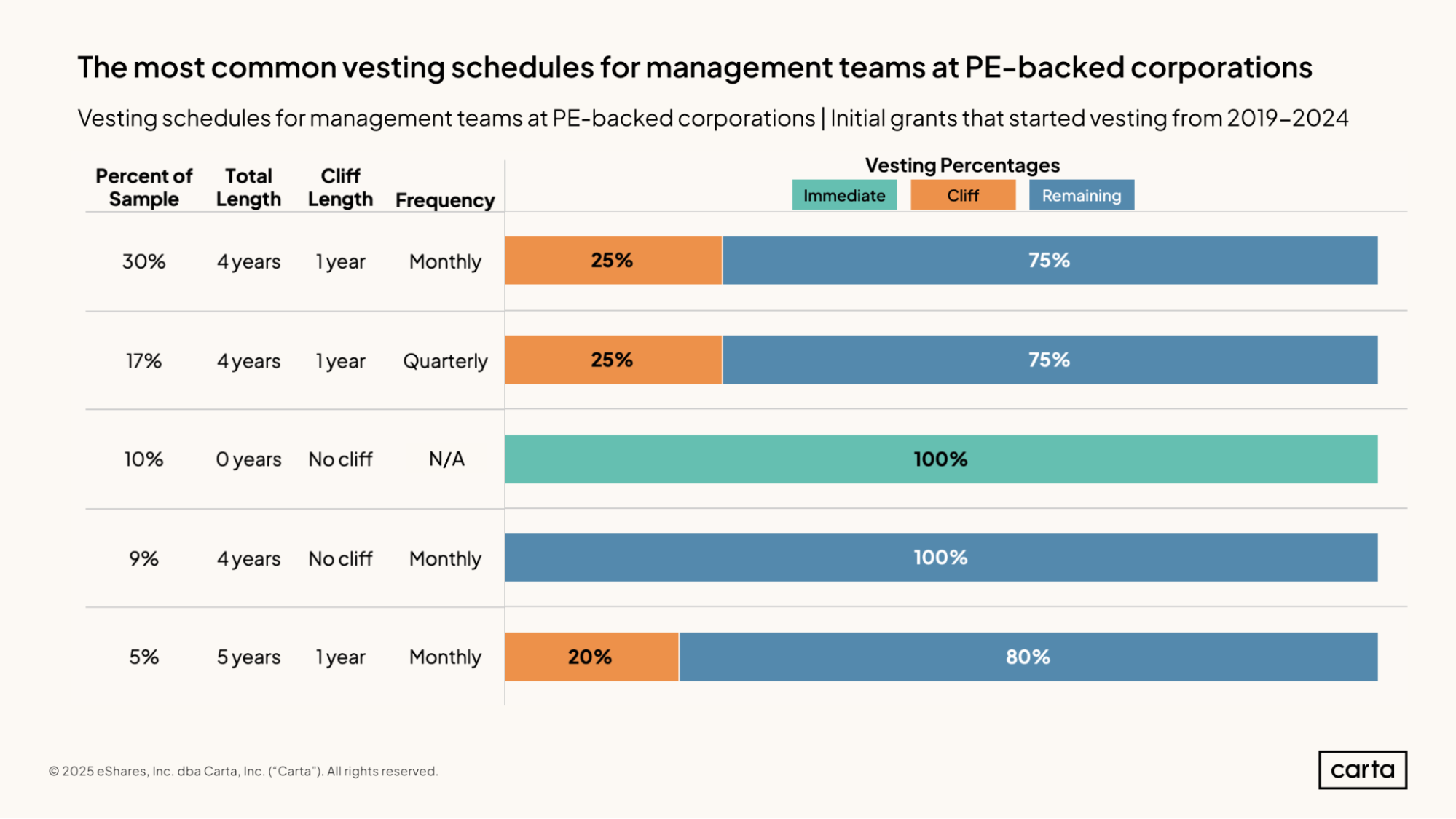

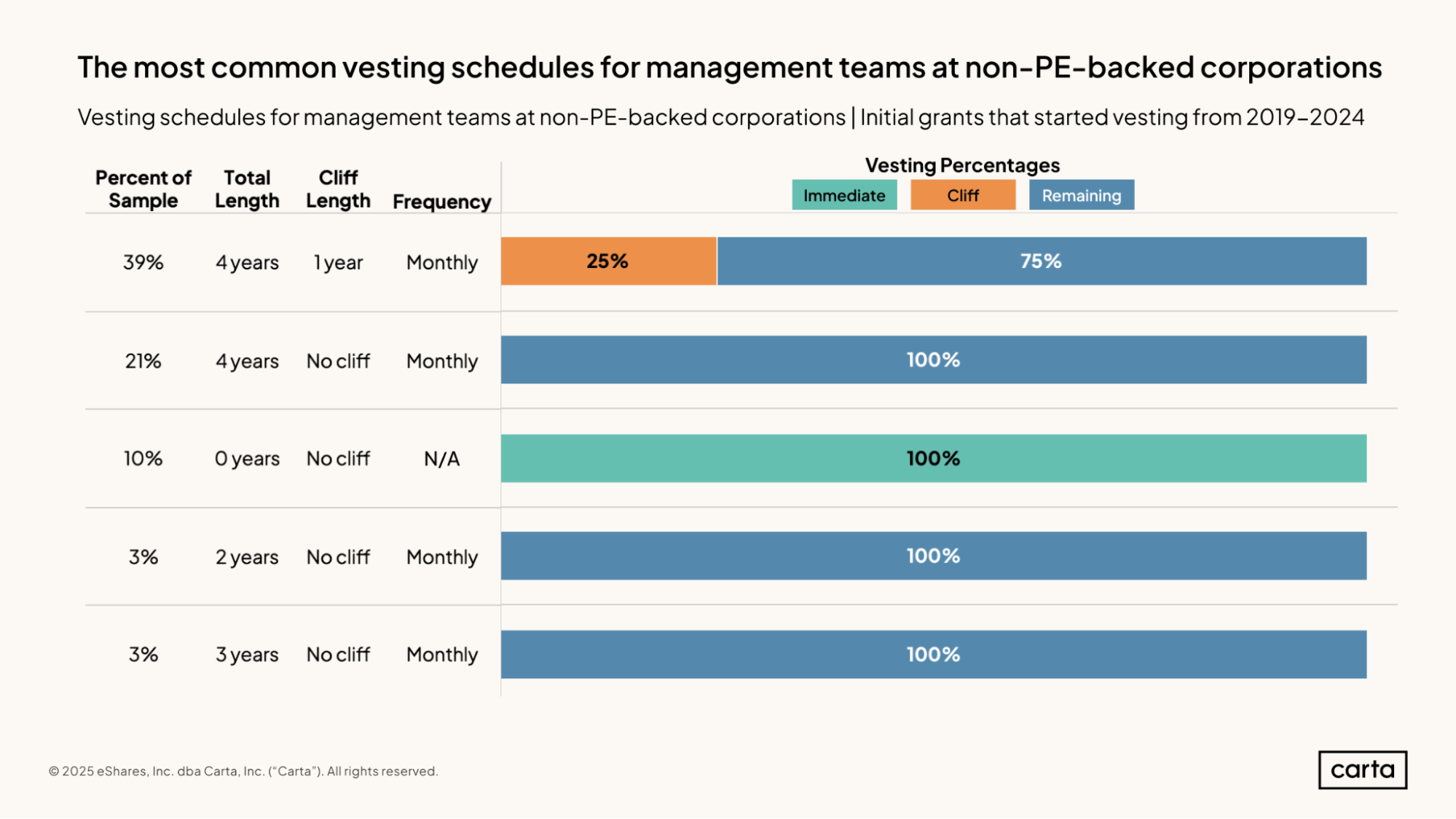

The most common vesting schedules

If we combine some of the key variables around equity vesting—the total length of the grant, the length of the initial cliff, and the frequency of vesting—we can arrive at several different “recipes” for how companies tend to structure their equity grants.

At PE-backed corporations, for instance, the most common recipe is a four-year grant with a one-year cliff and a monthly vesting schedule. About 30% of grants issued by companies in this category meet this description. The second most common recipe, at 17%, is a four-year grant with a one-year cliff that vests quarterly.

At corporations that are not backed by PE, the most common recipe is the same: A four-year grant, a one-year cliff, and monthly vesting.

One main difference in vesting between PE-backed corporations and non-PE-backed corporations is that quarterly vesting schedules are far less common in the latter group. None of the top five equity recipes among non-PE-backed corporations involves quarterly vesting.

Another point of divergence is related to cliffs. At corporations without PE backing, four of the five most common equity recipes involve no cliff at all. Some of the most common recipes among non-PE-backed companies also involve shorter grant timelines, either two years or three years. Shorter equity grants can be used to incentive performance over a tighter time window, such as if an employee is in the final stages of preparing for an IPO.

Sign up for the Data Minute newsletter:

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. ©2026 Carta. All rights reserved. Reproduction prohibited.