- How to start a venture capital firm

- What is venture capital?

- What is a venture capital firm?

- VC firm vs. VC fund

- How to start a venture capital firm

- What problem are you trying to solve?

- Building the founding team

- Building your track record

- How to develop your investment thesis

- How to structure your firm and fund

- How to raise your first fund

- How to recruit LPs to your first fund

- How to build your operational foundation

- Fund administration

- Banking, legal, tax, and audit partners

- How to manage the fund lifecycle

- Capital calls and closings

- Financial reporting and LP communication

- Tax and audit readiness

- How VC economics work

- Management fees

- Carried interest

- Frequently asked questions about starting a venture capital firm

- Download the First Time Fund Manager Checklist

If you’re considering starting and raising your own venture capital fund, you might already work at a venture capital firm or be an angel investor. Or maybe you work at a tech company, or a nonprofit organization completely outside the startup network. Regardless of where you’re starting, it’s crucial to understand the ecosystem you’re stepping into.

What is venture capital?

Venture capital (VC) is an investment strategy in which investors provide early-stage startups or private companies with cash in exchange for equity ownership in the company. The investors’ hope is that the startups will become more valuable over time so that when there is a liquidity event or other opportunity to sell off equity in the company, the investors might make a profitable return on their investment. To pursue these strategies, the VC investors pool their own capital with outside money from others to invest in startups. The VCs set up asset management firms to manage all of the funds they launch.

What is a venture capital firm?

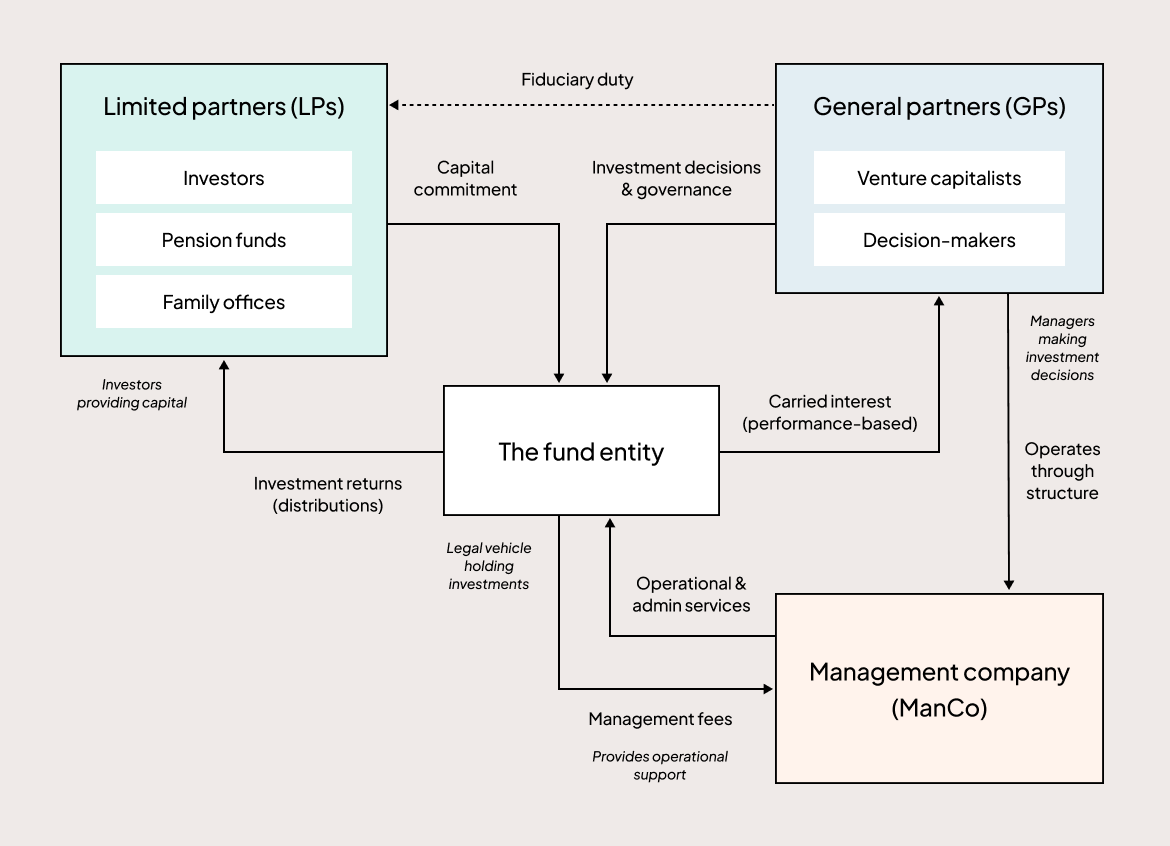

A VC firm is a management company (manco) that raises and manages investment funds, acting as the hidden hand behind many of the most innovative early-stage companies. The firm itself is the ongoing business, while a VC fund is the specific investment vehicle that uses a private markets exemption to avoid the registration requirements of the Securities Act. The people who manage the firm and make investment decisions are called general partners (GPs), while the investors who provide the money for the fund are called limited partners (LPs); these roles are central to common fund structures.

The firm, run by the GPs, earns revenue by charging the fund management fees and a share of the profits, known as carried interest. This structure allows the GPs to build an enduring business that can raise and manage multiple funds over time.

VC firm vs. VC fund

VC firms are different from VC funds.

The VC firm is the business that oversees the investment strategies of the VCs. It’s the entity you’re thinking of when you hear the brand name of a VC. It is the manco that rents office space, employs investment analysts, and subscribes to financial publications. Successful venture firms often operate several VC funds at one time—Fund I, Fund II, and so on.

The VC fund is the legal entity that pools money to invest in assets like startups and pursues its own particular investment strategy. The fund then owns those assets until it sells them.

→ Learn more about VC fund structures

How to start a venture capital firm

In the steps below, we’ll outline the steps to setting up a new VC firm before raising your first fund. We've also summarized the information in our first-time fund manager checklist.

What problem are you trying to solve?

Before you can raise a new fund, you need to clarify the problem you’re trying to solve. Be as specific as possible about your intentions. Once you know the problem you want to solve—say, lack of capital for female founders at the seed stage, a lack of support for early-stage founders in the Midwest, or the development of innovative climate resiliency technologies—you can do some further research and refining.

Consider the following factors before you raise a fund:

Your own expertise: What kind of experience and expertise do you have? Is your knowledge, skill set, or network an asset? What tools do you have at your disposal? Where will you need help?

Your target demographics: Who are the founders and companies you want to help? What are their struggles and goals? What are their specialties? Where do they live and operate? Who are their target customers? How much capital have they historically raised and when? What kind of LPs will be interested in investing in these founders?

The market landscape: Do institutional investors want access to your target demographic? Why or why not? What other companies and VC firms are trying to solve the problem you want to solve? Where are they succeeding and falling short?

The answers to these questions will either serve as the foundation to your fund strategy or guide you in another direction.

Building the founding team

Because a VC firm is a business, it needs a strong leadership team to succeed. The classic image of a startup launched by a team of co-founders with complementary skills holds true, especially for companies that successfully raise venture capital. An ideal team might include a partner with deep investment experience, another who is a former startup founder with operational expertise, and another with a strong professional network for finding deals and raising money.

Having someone else who can complement your own skills can be beneficial for your first time. For example, if you have a strong operational background as a former COO, you might want to partner with someone with a background in finance or with technical expertise. From there, you can figure out the basics, such as how you’ll pay yourselves, where your office will be, what equipment you’ll need, and who you need to hire next.

It is possible to start a firm as a solo GP. However, this path places a much heavier operational burden on one person. A solo GP must handle all aspects of the business, from VC investing to fund administration, which makes strong external partners and a robust technology platform essential for managing the back office.

The founding GP role

As a fund manager, you’ll be both an entrepreneur of your own firm and a fiduciary of outside capital. You’re responsible for attracting the attention of companies and founders, corresponding with LPs, constructing a portfolio, executing deals, and handling fund administration.

That’s why it’s helpful to start with the following (although not an exhaustive list):

A compelling investment thesis

Good relationships with founders

Business or industry expertise

A competitive drive to win deals

A smart portfolio construction strategy

Great networking skills

Patience

The ability to articulate why your fund is different

The willingness to contribute financially

Building your track record

Before you can convince LPs to invest in your fund, you need to prove you can make successful investments. A track record is the most important evidence you can offer to show LPs that you know how to pick successful startups, and industry benchmarks provide a detailed snapshot of the latest data for fund returns.

Your track record is your past performance as an investor that details the types of investments you’ve made, why you made them, and what kinds of returns you’ve been able to secure. Prospective LPs have many firms and funds to choose from. To gauge your potential for success, they'll consider fund performance metrics like total value paid-in (TVPI), multiple on invested capital (MOIC), and internal rate of return (IRR).

LPs are more focused than ever on a fund’s ability to generate real returns, especially since while the number of completed exits has been steady at around 1,300 annually, truly return-generating exits like IPOs have been rare. According to a recent survey of LPs, distributions to paid-in capital (DPI) is the metric that rules them all. After all, LPs invest in venture funds because of the promise of future returns; without those returns, they won’t have capital to reinvest in the next generation of funds.

If you’re starting your first firm or fund, you won’t be able to point to previous fund metrics. To prove to LPs that you have what it takes to be successful, first-time fund managers can establish a track record in a few different ways:

Angel investing: You can use your own money for angel investing in early-stage startups, allowing you to assemble a portfolio that resembles a personal venture fund. Angel investments can be any size, but usually they’re under $100,000. This demonstrates your personal conviction and ability to identify promising companies early.

Syndicates: You can pool capital with other investors in an angel syndicate to participate in larger deals. This shows you can collaborate and attract other investors to the deals you find.

Special purpose vehicles (SPVs): Aspiring fund managers can create a single-deal entity, called an SPV, to invest in one specific company, often at the pre-seed, seed, or Series A stage. This is an effective way to show LPs you can execute a fund-like process from start to finish.

Warehousing investments: Warehoused investments are investments in portfolio companies that a VC makes while fundraising but before the fund entity is legally formed. The investments are reserved as to be transferred to the fund once it is closed.

How to develop your investment thesis

Your investment thesis is the strategic blueprint for your fund. It defines your firm’s unique point of view and guides every investment decision you make. A strong thesis provides clear answers to what you invest in, why you are positioned to win those deals, and how you will execute deal sourcing.

A well-defined thesis is also critical for your firm's operations. The types of companies you target and the size of your investments are key elements of portfolio construction that will determine your target fund size. This, in turn, dictates the management fee budget you will have to run the firm and pay for essential services. As Allison Barmen Gates, GP at Sempervirens, explained during Carta’s Building an Investment Track Record webinar, a structured due diligence process is key. She uses a framework called the “five Ts” to evaluate investment opportunities, which helps maintain strategic focus.

Team: Is the founding team prepared and committed to building a large business?

Technology: What is the quality of the technology and how can it adapt over time?

Total addressable market: Is the total addressable market (TAM) large enough for the company to grow to the size needed for a venture-scale return? This type of return is what allows top-tier VC funds to deliver for their own investors. For instance, the top decile TVPI—or total value to paid-in capital—for small funds ($1-10 million) from the 2017 vintage was 5.33x, meaning the fund’s total value was projected to be more than five times the capital invested by its partners.

Terms: Are the investment term sheets structured in a way that allows you to generate a return for your investors?

Tailwinds: Are there broad market trends, like the rise of AI or fintech, that will help this company succeed?

How to structure your firm and fund

Limited partnerships and limited liability companies (LLCs) are used to facilitate relationships between VCs and third-party investors, as well as operate the activities of the VC firm itself.

The process of fund formation is the most critical step in building a compliant and scalable VC business. This process involves creating the legal and financial architecture for both your manco and your investment fund. Mistakes made at this stage can create significant legal and operational problems down the road.

This is often the most complex part of starting a firm, and many emerging managers seek expert guidance. The founders of Emmeline Ventures partnered with Carta to navigate this process for their debut fund. As co-founder La Keisha Landrum Pierre noted, “It really matters who you partner with to get it right out of the gate. We’re really happy that we went with Carta.”

The limited partnership fund structure

In the United States, the standard legal structure for a VC fund is a limited partnership. This is a legal entity composed of an entity acting as the GP, which manages the fund, and the LPs, who invest in it. This structure is standard because it provides liability protection for the LPs, meaning they are generally not responsible for the fund's debts beyond their invested capital. LPs cannot be involved in the active management of the partnership.

The foundational legal document for the fund is the limited partnership agreement (LPA). The LPA is the rulebook that governs the relationship between the GP and LPs. It outlines all of the fund's terms, including its lifecycle, fees, and the scope of the GP's authority.

The management company and GP entity

A typical VC firm uses a multi-entity structure that separates the firm’s business operations from the investment fund itself. This separation is crucial for liability protection, and operational clarity.

The management company (manco): This is the operating business that employs the partners and staff. It is usually structured as an LLC and uses management fees from the fund(s) to pay for all firm expenses, including salaries, rent, and service providers.

The GP entity: This is a separate entity, also typically an LLC, that serves as the legal GP of the fund. Its primary purpose is to hold the carried interest, or the share of profits, earned from the fund's successful investments. Typically, there is one GP entity per fund, but usually one manco across all funds.

Mancos structured as an LLC may provide each member with the benefits of both limited liability and pass-through taxation. This separation by legal entities limits liability to the individual entities, rather than exposing the various types of VC cashflows and other assets to liability from any one of the funds. This means if one of a firm’s funds gets saddled with liabilities, it generally won’t impact its other funds.

Mancos are indeed typically structured as LLCs, and their internal organization can vary depending on the VC firm’s operating preferences, like team, overhead, and platform activities. Because the same employees within a manco may perform services for multiple funds, the manco will sit across multiple funds.

Bring the resources back in

As the GP of the fund, the LLC you created to act as the fund’s GP has the legal authority to manage the fund’s affairs—which includes the ability to hire service providers. At firms with multiple funds, the VC firm usually acts as the manco for all of its funds. In other words, the fund’s GP hires the VC firm to perform management functions for the fund, like hiring and paying investment staff, securing office space and computers, and so on.

This way, the VC firm is still able to share its resources for the benefit of all of the funds it oversees, while shielding itself from liability from all of those funds.

How to raise your first fund

Once your fund is legally set up, the next step is raising capital. This involves pitching your investment thesis to potential LPs and securing their capital commitments, often from institutional investors, family offices, or high-net-worth individuals. The fundraising process comes with a significant administrative burden that can distract you from building investor relationships. Even for a smaller fund with less than $25 million in commitments, you could be managing dozens of LPs; the median fund had 27 LPs between 2017 and 2022, with some funds managing as many as 51.

Your fund’s LPs will remain passive investors, while you as the fund manager will make the day-to-day investment decisions. LPs officially become investors in your fund when they sign subscription documents and you countersign them as GP.

GPs need to manage a data room with sensitive documents, securely distribute subscription documents to dozens of potential LPs, and track signature progress. You also have to collect LP information to run compliance checks, like know your customer (KYC) and anti-money laundering (AML), on every investor.

Even if you’re a seasoned investor, raising a VC fund requires a completely different set of skills than making individual investments or working within an existing VC organization. Many first-time fund managers organize their fund strategies around their personal experience and networks of experience because these connections can offer privileged access to deal flow, talent pools, and industry expertise.

How to recruit LPs to your first fund

Building a convincing fund thesis and conveying it in a professional pitch deck is challenging work. But it’s only half the battle. Finding LPs whose investment interests align with your fund thesis, and persuading them to invest capital in your fund, is your next challenge.

Most VC funds raise under regulatory exemptions that prohibit them from advertising or making public solicitations for capital contributions. That means you can only fundraise from your existing personal and professional networks. The number of potential LPs in your networks may depend on your background, your work experience, and where you live. These will mostly be investors who meet the definition of an accredited investor.

As an emerging fund manager, you’ll need to canvass your network, ask for introductions to new LPs who have an interest in your investment areas, and start taking meetings. Start by making a list of people in your networks who may qualify as accredited, and pitch them on your investment thesis.

How to build your operational foundation

A modern VC firm should run on integrated VC solutions, not a patchwork of spreadsheets and disconnected service providers. Building a scalable business requires a solid operational foundation from day one. This means choosing partners and systems that can grow with you.

This might include:

A fund administrator to help manage all of the back office needs for your fund

A bank where you can open bank accounts for your fund

An audit firm if your fund needs to be audited

A tax provider to help prepare tax filings

A lawyer to help you draft the LPA and other fund documents and negotiate with LPs

Many emerging managers find that partnering with a comprehensive service provider is the most efficient way to establish their back office. This trend is reflected in the growing presence of smaller funds on integrated platforms. Among funds closed on Carta, those with $1 million to $10 million in committed capital—a group largely composed of emerging managers—accounted for at least 40% of all new funds in 2024 and the first half of 2025. That figure is up from just 25% in 2020.

Fund administration

Fund administration is the operational engine of your firm. It includes the critical back-office functions of accounting, financial reporting, and treasury management. Traditionally, firms outsourced these tasks to administrators who provided stale, quarterly reports. But LPs are no longer content to wait, creating a new urgency for fund managers to provide liquidity. In response, modern funds are accelerating their timelines; for example, 15% of venture funds from the 2023 vintage began returning capital to LPs within just six quarters—a higher rate than any other recent vintage at that same threshold.

A modern approach combines expert service with fund administration software. This gives GPs real-time visibility and control over their fund’s financials. This shift from a simple service provider to a true operational partner is a key advantage for new firms.

Banking, legal, tax, and audit partners

While a fund administrator can act as the central operational hub, you will also need to select other specialized partners. These include a bank, a law firm, a tax preparer who understands VC tax treatment, and an auditor for the fund's required annual audit.

When choosing these partners, it is best to select providers who have deep experience in the venture ecosystem. Their familiarity with industry norms and regulations will be invaluable. It is also important that their workflows can integrate with your core technology platform to avoid manual data transfer and reconciliation.

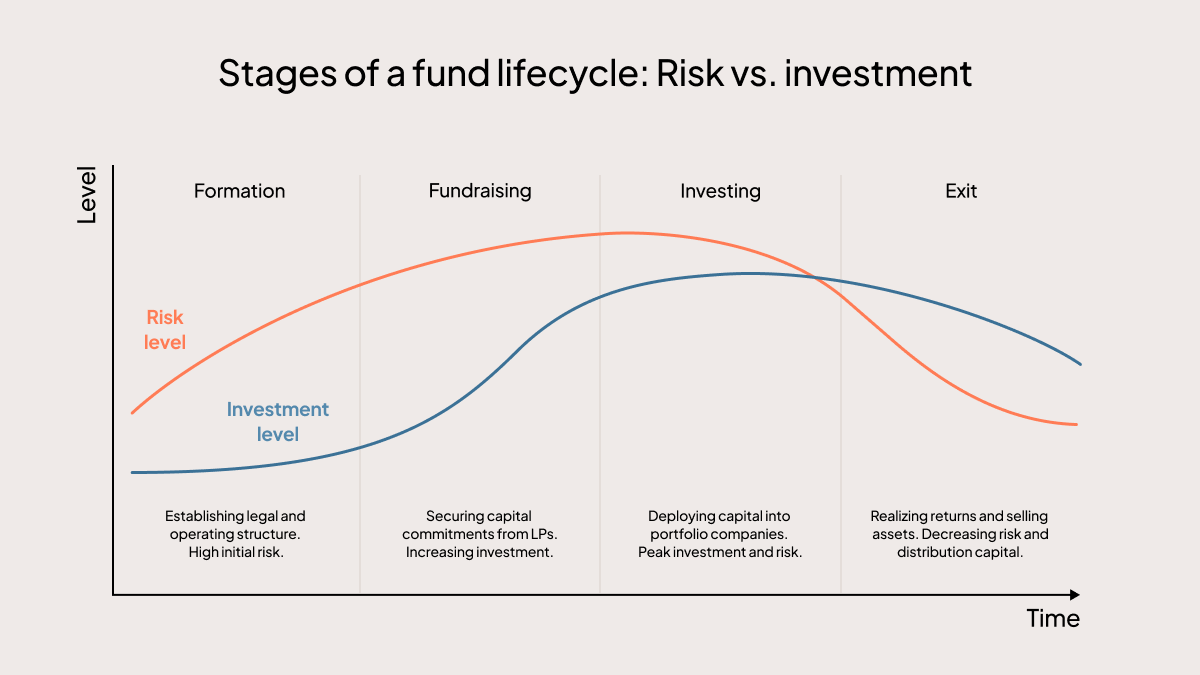

How to manage the fund lifecycle

Once your fund is raised and your operational foundation is in place, the ongoing work of fund management begins. The fund lifecycle covers every event from your first investment to your final distribution to LPs. A centralized record for all fund activity is essential for maintaining accuracy and compliance.

A unified platform connects every stage of the fund lifecycle. This ensures that data flows seamlessly from one activity to the next, creating an auditable record of every transaction and decision.

Capital calls and closings

A capital call is the process of formally requesting committed capital from your LPs. You will call capital to fund new investments and to pay the fund's management fees, and may use a capital call line of credit to bridge timing gaps.

Using a platform-based workflow automates the creation and delivery of capital call notices. It also tracks the receipt of funds and updates the fund's general ledger in real time. This automation eliminates many of the manual, error-prone processes that can slow down a fund's operations.

Financial reporting and LP communication

As a fund manager, you have a fiduciary duty to keep your LPs informed. This includes providing critical reporting documents that detail fund performance metrics, such as the schedule of investments (SOI) and partner capital account statements (PCAPs).

A dedicated LP portal provides your investors with a secure, on-demand view of their commitments, fund performance, and all essential documents. This level of transparency is what modern LPs expect. It is also a key tool for building trust and maintaining strong investor relationships over the long term.

Tax and audit readiness

The annual fund audit and tax season can be stressful. Traditionally, these processes involve manually gathering documents and reconciling data between your fund administrator, tax preparer, and auditor. This can be a time-consuming and frustrating exercise for everyone involved.

Modern fund administration platforms streamline these high-stakes compliance tasks. A dedicated auditor portal allows your auditor to securely access the necessary information directly. Having all fund data and documents in one centralized, audit-grade system transforms the experience from a painful exercise into a collaborative and efficient review.

How VC economics work

To manage your firm effectively, you need to understand its business model. A VC firm has two primary income streams: management fees and carried interest. These are often referred to as the industry's standard fee structure.

Fees | Purpose |

Management fee | The income used to pay for all firm operating expenses, including salaries, rent, software, and service providers like fund administration |

Carried interest | The GP's share of the fund's investment profits, earned only after LPs have received their entire invested capital back |

Management fees

The management fee is the predictable income stream that keeps the lights on at your firm. It is typically calculated as a small percentage of the fund's committed capital and is paid annually.

This fee is drawn down from LP commitments via capital calls throughout the fund's investment period. These funds are paid to the manco entity to cover all of the firm's operating expenses.

Carried interest

Carried interest, or carry, is the performance-based compensation for the GP. It represents a share of the fund's profits and is the primary incentive for generating strong returns.

It is important to understand that carry is only earned after the LPs have been repaid their initial investment, called the hurdle rate. This profit distribution is determined by a complex calculation known as a distribution waterfall. Automating this calculation on a fund administration platform is essential to ensure accuracy and fairness for all parties.

Starting a VC firm is a complex but rewarding journey. Building a strong operational foundation from day one is critical for long-term success and allows you to focus on what matters most: finding and funding the next generation of great companies.

If you're ready to turn your investment thesis into a reality, speak to an expert about launching your fund.

Frequently asked questions about starting a venture capital firm

What is a venture capitalist?

A venture capitalist is an investor who provides funding to early-stage or growth companies in exchange for equity, aiming for high returns as the company grows.

What’s the best way to launch a new venture capital fund?

The best way to launch a new VC fund is to use Carta Fund Formations, which streamlines fund setup, handles legal and compliance, and simplifies fund administration—all in one platform.

How much money do you need to start a venture capital firm?

You typically need at least $1–2 million to cover initial fund setup, legal, and operating costs, though this can vary based on fund size and use of streamlined platforms like Carta Fund Formations. You need cash for two main purposes: the GP commitment, which is your personal investment into the fund, and working capital to cover fund expenses before management fees are called. GP commitment is typically expected by LPs to show that GPs have “skin in the game.”

How much of my own money do I need to invest in the fund?

Typically, you should contribute 1–2% of the fund’s total capital (GP commit) to align interests with LPs, though exact amounts can vary based on fund size and investor expectations. Recent SPV data shows the median contribution from a GP is typically between 0.3% and 1.2% of the overall SPV size.

How much capital should I aim to raise for my first fund?

For a first fund, most solo or emerging managers typically aim to raise between $10 million and $25 million, balancing manageable portfolio size, investor expectation, and the amount of management fee that the GP takes on as salary.

Can you start a venture capital firm by yourself?

Yes, it is possible to be a solo GP, but it is an operationally demanding path. A strong, technology-driven fund administration partner is essential for a solo GP to manage the back office effectively and succeed.

How can solo GPs start a venture fund with minimal cost?

Solo GPs can start a venture fund with minimal cost by using platforms like Carta Fund Formations, which offer affordable, streamlined fund setup and administration, reducing the need for expensive legal and back-office services.

What team members are essential for a new VC firm?

Essential team members for a new VC firm include the GP(s) to lead investments, legal and compliance support, and fund administration or operations personnel, which can be in-house or outsourced.

What is “2 and 20” in venture capital?

“Two and 20” refers to the standard fee structure in the VC industry, which consists of a 2% management fee and 20% carried interest. This model is also common in private equity.

What are the key regulatory and compliance requirements I need to consider when starting a venture capital fund or firm?

Key regulatory and compliance issues for starting a VC fund include fund registration or exemptions with the SEC, adhering to state “blue sky” laws, investor accreditation requirements, anti-money laundering rules, and proper fund documentation and reporting.

How do I find and attract limited partners (LPs)?

Find and attract LPs by leveraging your personal network, building relationships with angel investors, family offices, and institutional investors, and clearly communicating your fund’s unique value and track record.

How should I source and evaluate deals as a new VC?

As a new VC, source deals by networking with founders, attending industry events, leveraging referrals, and building an online presence through a website and social media channels. Evaluate deals by assessing the team, market opportunity, traction, and alignment with your investment thesis.

What track record do LPs expect from first-time fund managers?

LPs expect first-time fund managers to show a track record of successful angel investments, relevant industry experience, or proven ability to source and support promising startups, even if not from managing a prior fund.

What are the best ways to differentiate my fund in a competitive market?

Differentiate your fund by developing a clear, focused investment thesis, leveraging unique industry expertise or networks, showcasing a strong track record, and providing exceptional value and support to portfolio companies.

How do I structure follow-on investments and reserves?

Allocate a portion of your fund (often 50-70%) as reserves specifically for follow-on investments in your most promising portfolio companies, based on performance milestones and future funding needs.

How do I measure and report fund performance to LPs?

Measure and report fund performance to LPs using key metrics like IRR, TVPI, and DPI, and provide regular updates on portfolio company progress and financials through transparent, periodic reports.

What are the key milestones to track during the fundraise and investment periods?

Key milestones include first close, final close, amount committed, capital called, number of investments made, portfolio company performance updates, follow-on rounds, and eventual exits or returns.

Download the First Time Fund Manager Checklist

Our free checklist breaks down the key steps you need to follow to launch your first VC fund.

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. This post contains links to articles or other information that may be contained on third-party websites. The inclusion of any hyperlink is not and does not imply any endorsement, approval, investigation, or verification by Carta, and Carta does not endorse or accept responsibility for the content, or the use, of such third-party websites. Carta assumes no liability for any inaccuracies, errors or omissions in or from any data or other information provided on such third-party websites. © 2026 eShares, Inc. dba Carta, Inc. All rights reserved. Reproduction prohibited.