- Rule 506(b) vs. Rule 506(c)

- What is Rule 506(b)?

- Who can invest in 506(b) securities offerings?

- 506(b) benefits

- 506(b) limitations

- What is Rule 506(c)?

- Who can invest in 506(c) securities?

- How 506(c) investors can verify LP accreditation

- 506(c) benefits:

- 506(c) limitations:

- What is the future of Rule 506?

- Download the VC regulatory playbook

Rules 506(b) and 506(c) of Regulation D give private funds two ways to raise investment capital without registering the offering with the Securities and Exchange Commission (SEC). These exemptions allow issuers of private securities—including the general partners (GP) of private funds—to avoid regulations the SEC mandates for registered securities offerings.

Choosing between the 506(b) and 506(c) exemptions is an important decision GPs have to make when they set up a fund. Each affects fundraising differently, and you’ll want to choose the exemption that best suits your fundraising needs.

What is Rule 506(b)?

Rule 506(b) is part of Section 4(a)(2) in the Securities Act of 1933, which outlines rules companies or investors must follow to sell securities in a private offering.

506(b)’s defining feature: A GP can raise an unlimited amount of money as long as they do not publicly advertise or solicit investments for the fund.

Who can invest in 506(b) securities offerings?

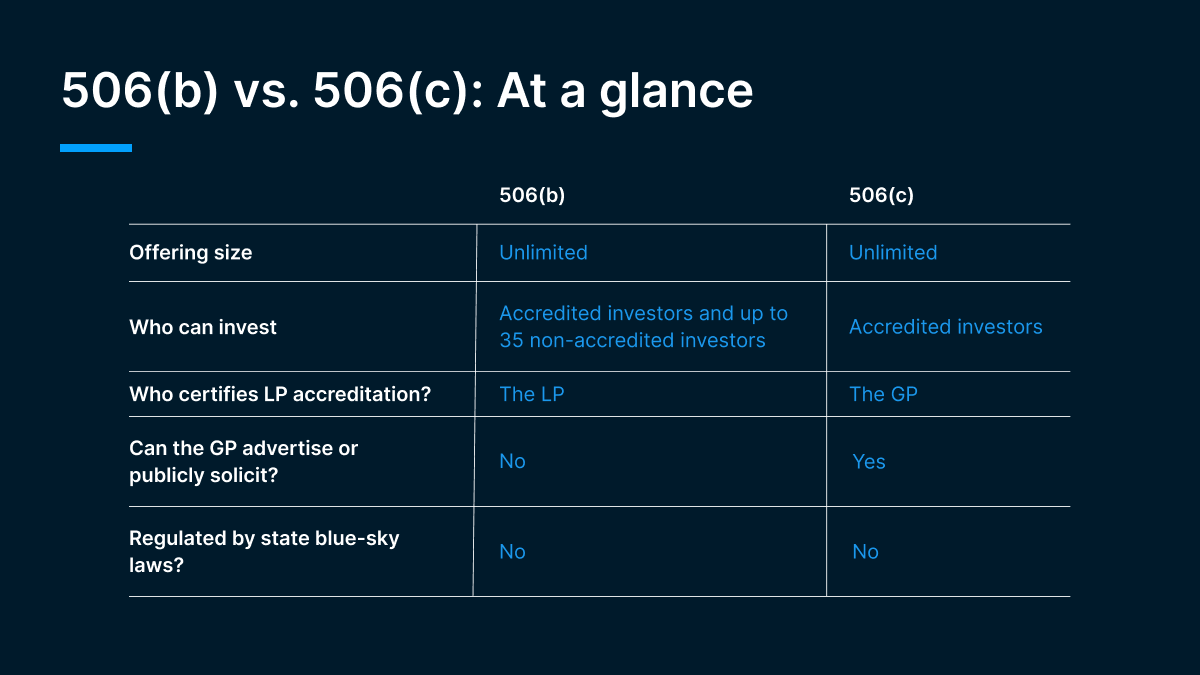

Rule 506(b) permits GPs to raise money from an unlimited number of accredited investors and as many as 35 non-accredited investors. Non-accredited investors in the offering must be sophisticated investors, and they must be given additional disclosure documents similar to those typically provided in Regulation A offerings. Issuers cannot publicly market a 506(b) offering; this means that GPs raising a VC fund under the 506(b) exemption can’t advertise the fund or generally solicit investors.

506(b) benefits

Rule 506(b) offerings are not regulated by state blue-sky laws.

Purchasers can self-verify their accreditation status; GPs aren’t responsible for verifying accreditation.

If a GP only takes on accredited investors, they can avoid filing burdensome disclosure documents with the SEC that would need to be provided to non-accredited investors.

506(b) limitations

GPs are prohibited from talking about the fund publicly while fundraising, and from running a crowdfunding campaign to bring in capital.

GPs can’t take on non-accredited investors without offering the same disclosure documents typically required under Regulation A of U.S. securities laws.

An overwhelming majority of private fund GPs raise funds under the 506(b) offering rules. These include private equity, venture capital, and real estate funds, among others.

For an established firm, raising capital under 506(b) is often a no-brainer. It allows them to draw on their network of limited partners (LP) and avoid going through the time and expense of actively verifying each LP’s accreditation status.

To state that they are raising capital in a 506(b) offering, a firm simply checks the 506(b) option when they complete their Form D notice, the filing that confirms which exemption the fund is claiming. The SEC requires Form D to be filed within 15 days of the first close.

What is Rule 506(c)?

In 2012, Congress passed the Jumpstart Our Business Startups (JOBS) Act to help the U.S. economy recover from the Great Recession. As part of the JOBS Act, Congress lifted the ban on publicizing securities offerings for issuers who raise exclusively from accredited investors. The SEC created Rule 506(c) to outline the requirements investors must meet to participate in those offerings.

506(c)’s defining feature: A GP can perform general solicitation and advertising without any limitation on how much capital they can raise.

Who can invest in 506(c) securities?

Accredited investors are eligible to invest in 506(c) offerings, but unlike with the 506(b) exemption, the fund’s GP must take “reasonable steps to verify” that the purchasers are accredited or hire a third party to perform the verification.

How 506(c) investors can verify LP accreditation

What exactly does “reasonable steps to verify” mean? That depends on how the LP claims eligibility.

If an LP is claiming accreditation based on income, the GP may need to obtain the LP’s tax forms for the previous two years. GPs also would have to obtain confirmation that the LP’s income will continue to meet the minimum threshold for accredited investors (which is $200,000 annually for an individual and $300,000 for a married couple) in the current year.

If the LP claims accreditation based on net worth, GPs can review the LP’s assets by collecting proof of the purchaser’s assets and liabilities (for example, bank statements and brokerage reports) within the past three months. GPs must also obtain confirmation from the LP that all liabilities that could impact net worth have been disclosed. To be an accredited investor, an individual must have a net worth of more than $1 million, excluding their primary residence.

If the LP claims accreditation based on one of the SEC’s recognized professional certifications, the GP would need to obtain a copy of that certification.

GPs may also get written confirmation from the investor’s attorney, broker dealer, registered investment adviser, or CPA confirming they took reasonable steps to verify the investor’s accreditation status in the past three months.

Once the fund manager verifies an investor’s accredited status, the investor can self-certify as an accredited investor with that GP for a period up to five years, assuming the GP doesn’t become aware of information to the contrary within that timespan.

506(c) benefits:

Rule 506(c) offerings are not subject to state blue-sky laws.

GPs can publicly market their capital-raising offer to a larger investor base, beyond just one-on-one conversations and emails within their personal and professional networks.

506(c) limitations:

Verifying accredited investors takes up time and money.

Many investors are reluctant to give sensitive information to GPs they don’t have a personal relationship with.

Given the potential liability third parties take on when they certify investor accreditation, accountants and lawyers are unlikely to make these certifications except perhaps for very large, lucrative clients.

Due to these limitations, GPs with robust networks of accredited investors often seek to avoid compliance costs and regulatory risks by raising money under Rule 506(b). On the flip side, emerging GPs without an established network of accredited investors could benefit from raising as a 506(c) because it allows them to solicit investors via social media, print advertising, or marketing.

Under the current rules, GPs that file a fundraise as a 506(b) offering are allowed to change the offering’s exemption status to 506(c) if they want to advertise their fund. But GPs who originally filed under 506(c) can’t reverse course and retroactively become a 506(b) if they’ve already advertised.

What is the future of Rule 506?

The SEC recently approved other accreditation methods in addition to the income verification requirement, and modestly expanded the accredited investor base; this boost to the number of eligible investors could be helpful to GPs raising serial 506(c) offerings. However, because these changes don’t address the initial income verification burdens, they may not be enough to encourage more 506(c) fundraising.

In fact, the SEC may propose changes to make 506(c) less attractive to GPs: The agency’s regulatory agenda includes plans to amend Regulation D and Form D to improve investor protections. The SEC is likely to revisit a 2013 proposal that would introduce stricter filing requirements and hand out harsher penalties for failing to meet them, including a possible one-year ban from using the exemption.

Download the VC regulatory playbook

Need to know more about how private funds are regulated?

Fill out the form below to download the Carta VC regulatory playbook, an end-to-end resource for understanding the basics in venture capital regulation.

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. ©2026 Carta. All rights reserved. Reproduction prohibited.