Companies on Carta made more than 60,000 new hires during the first four months of 2024. Over that same span, more than 60,000 employees on Carta left their positions.

That’s a lot of activity: A lot of dream jobs earned, a lot of new opportunities begun—and, unfortunately, a lot of opportunities ended.

As these tens of thousands of individual lives have changed, the broader landscape of startup compensation has changed, too. Layoffs have become less common. The average salary has increased for some job functions, such as design, and declined for others, such as customer support. And the geography of startup compensation is shifting: The average size of pay packages is on the rise for employees in metro areas like Atlanta, Cincinnati, Pittsburgh, and Sacramento.

The startup ecosystem looks a little different today than it did two or three years ago. It only makes sense that the way startups compensate their employees has shifted, too.

At Carta, we believe it’s our responsibility to share the insights that come from an unmatched amount of data about the private market. The data below comes from thousands of CTC customers with over 500,000 data points used by Carta Total Compensation. Other metrics in the report, such as those that describe employee movement, derive from the aggregate pool of more than 1 million employees currently working for the 45,000 startups that use Carta to manage their cap tables.

Download the equity compensation addendum hereH1 2024 key takeaways

Salary and equity held steady: The average amounts of both salary and fully diluted equity issued to new employees have been largely unchanged since last September. The market seems to have landed on a new normal for equity packages, which had previously declined sharply in late 2022 and 2023.

Hiring hasn’t picked back up: There were fewer new hires this January than in any of the previous four Januaries. The same was true for this February, this March, and this April. In part due to lower hiring, total net headcount on Carta has remained flat.

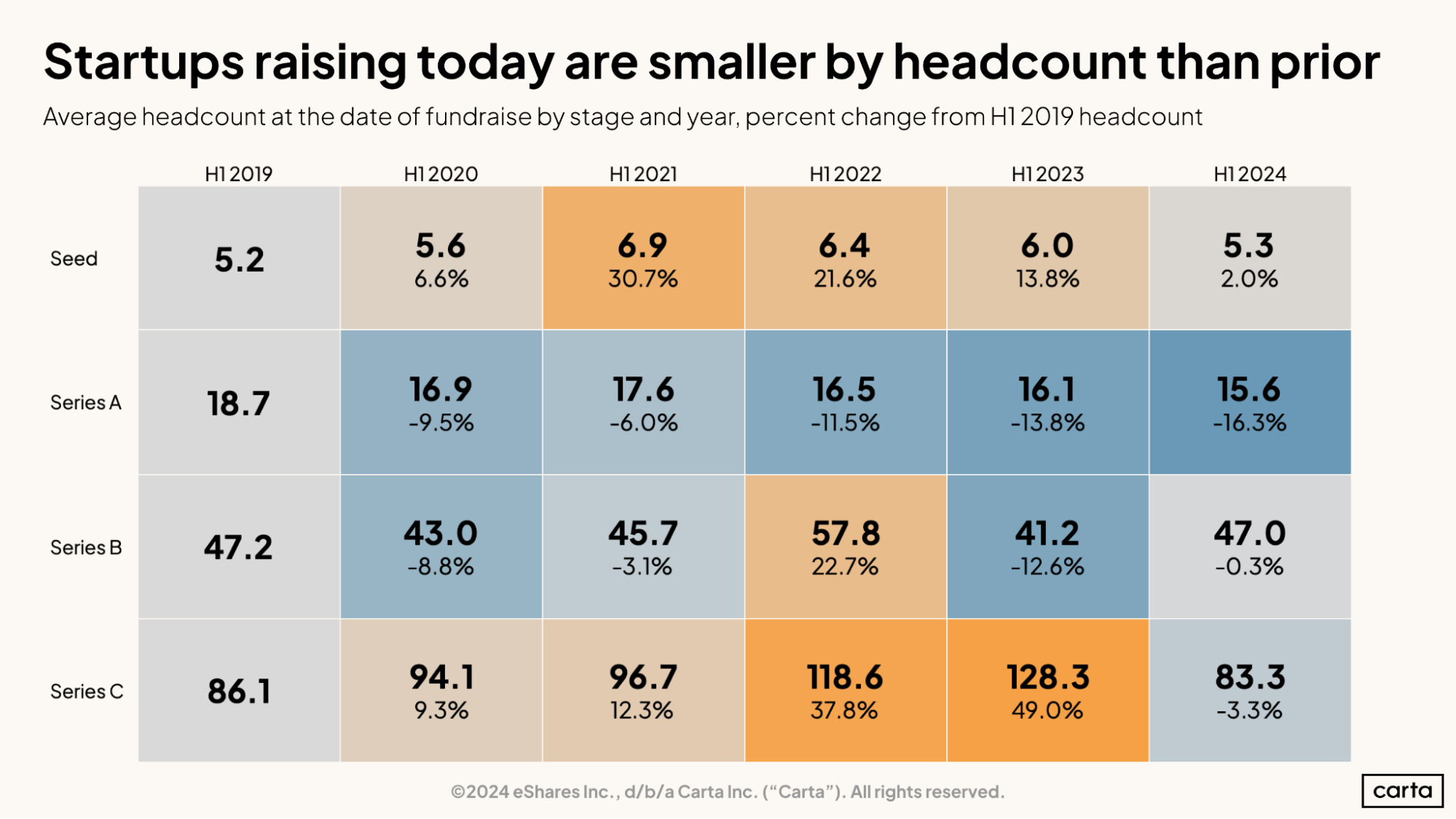

Companies raising cash are leaner: Startups that closed seed funding in H1 had an average of 5.3 employees, down from 6.9 in H1 2021. Series A startups have averaged 15.6 employees so far this year, compared to 17.6 in H1 2021. At most stages, successful fundraising teams have been smaller.

Hiring & headcount

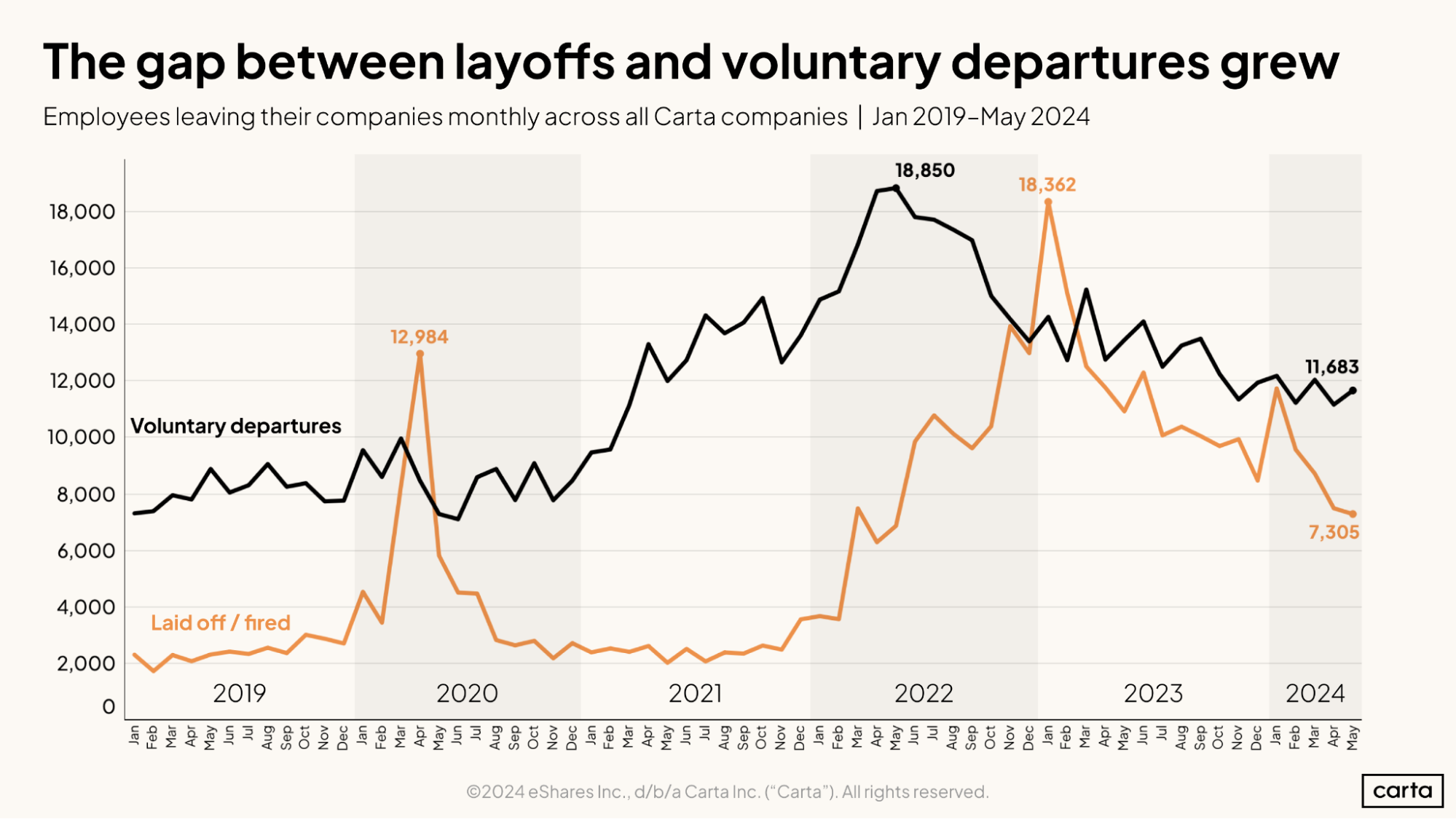

The number of monthly job departures from companies on Carta has been declining steadily so far in 2024, with most of that reduction coming from a dip in layoffs and firings. There were 7,305 of these involuntary departures in May, down 38% since January 2024 and 62% from the recent peak of layoffs and firings, which occurred in January 2023.

Voluntary job departures have also been on the wane over the past two years, if to a less dramatic degree than involuntary moves. There were 11,683 voluntary job departures on Carta in May, 4% lower from this January’s total and down 51% from May 2022, the recent high point.

As this year has progressed, layoffs and firings have begun to make up a smaller portion of all job departures. Overall, there were 18,988 departures tracked on Carta in May. Less than 40% of those departures were involuntary, the smallest proportion since September 2022.

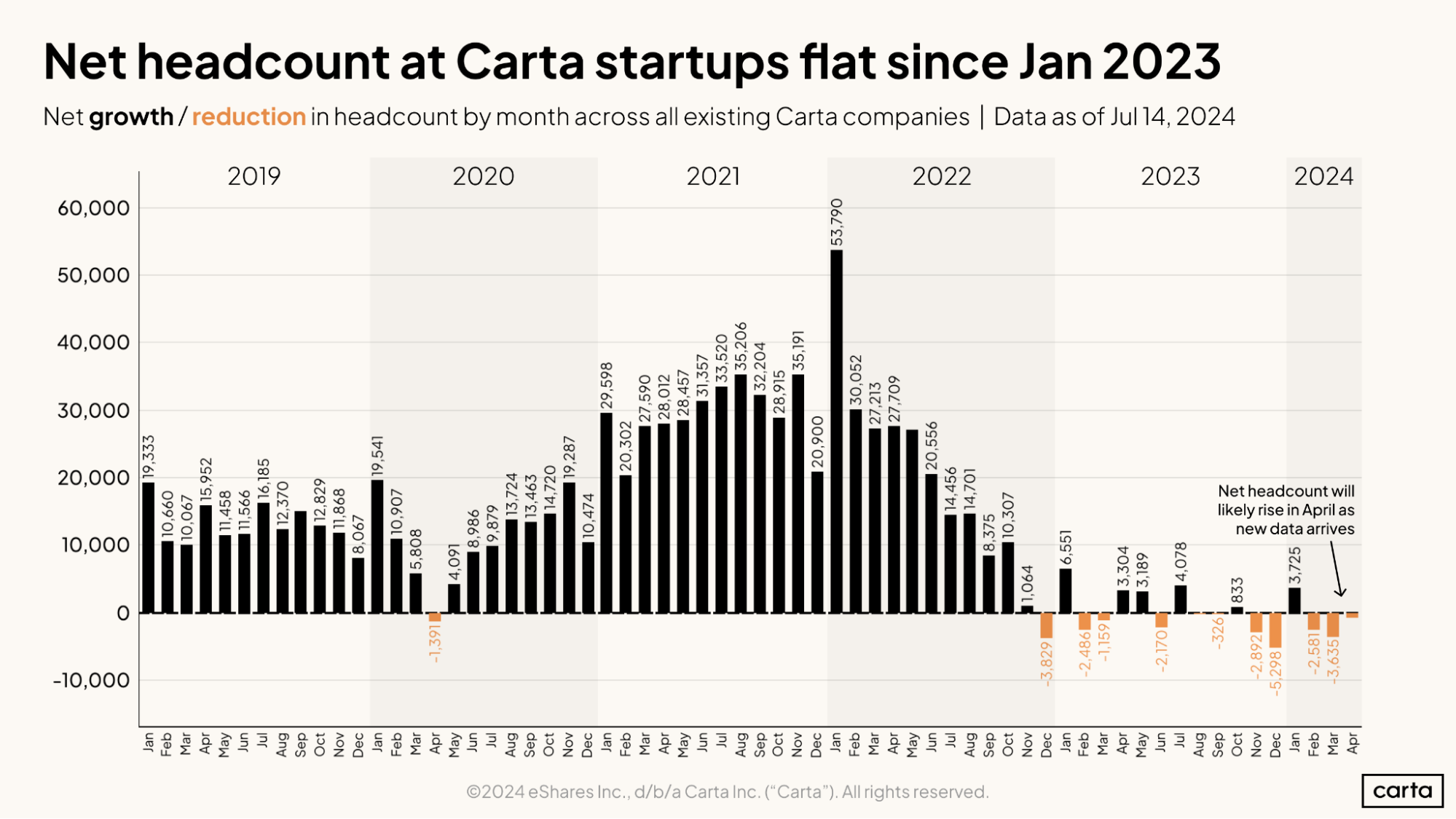

Ever since late 2022, the total number of employees on Carta has essentially been in a state of stasis. Headcount would grow by a few thousand one month, then decline by a few thousand the next. This stands in sharp contrast to the preceding four years, when net headcount on Carta typically grew by at least 10,000 people per month.

This new emphasis on financial austerity means that, in terms of employees, the startup industry is no longer growing like it used to.

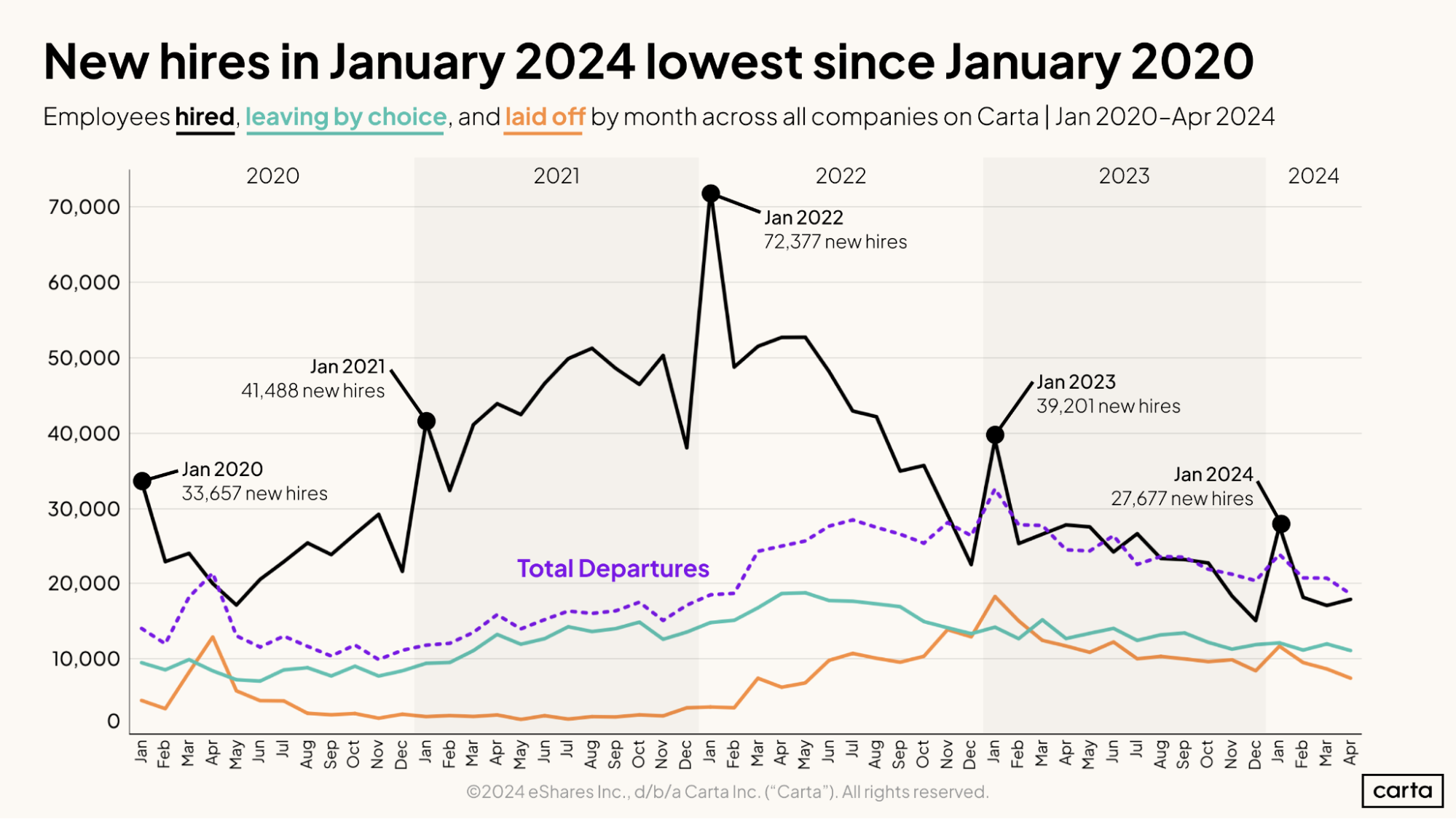

Hiring data bears out the low-growth hypothesis. January is typically an active time for adding talent. In three of the past four full years, it’s been the busiest hiring month of the year. Once again, January 2024 saw a spike in new hires relative to other recent months.

Relative to past Januaries, however, it was a slow start to the year. The 27,677 new hires that occurred on Carta in January 2024 is down 29% from the previous January. It’s also the fewest new hires that have taken place in any January so far this decade.

The ensuing three months did little to dispel the notion that this may be a quiet year on the hiring front. Just like in January, there were fewer new hires in each of February, March, and April in 2024 than in any prior year in the 2020s.

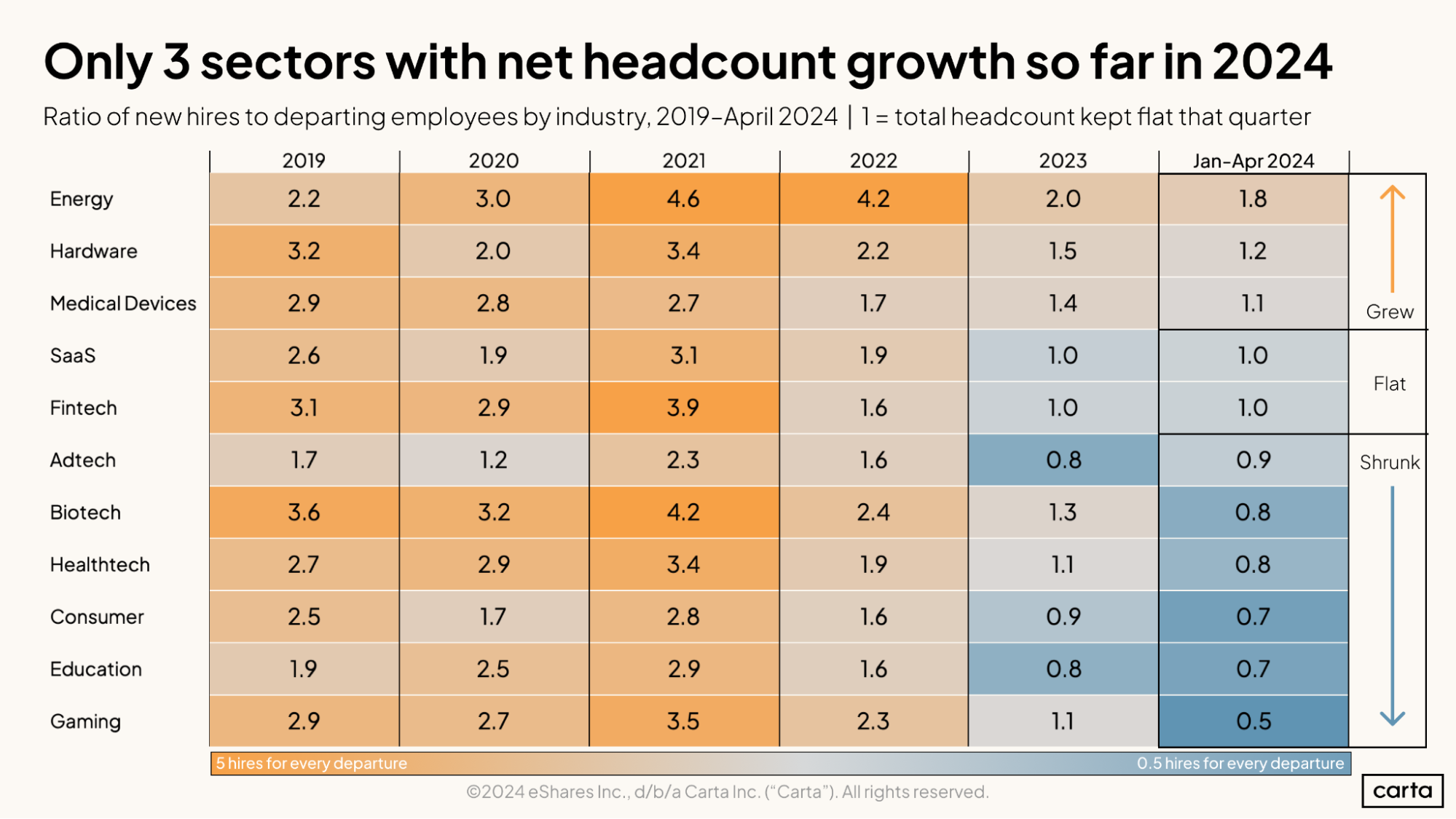

In the first four months of the year, total net headcount on Carta declined for six of the 11 primary industries we track. It stayed flat for two more. That leaves just three industries where total headcount has grown: medical devices, hardware, and energy. The most growth took place in energy, where hires outpaced departures by 1.8x during the first four months of the year.

If those rankings hold throughout the rest of 2024, it would be the third straight year in which energy had a higher rate of headcount growth than any other major industry. Many of these startups are working on ways to discover and implement new energy technologies and processes—the type of long-term, research-intensive work that might be less responsive to short-term shifts in the tech market.

Company composition

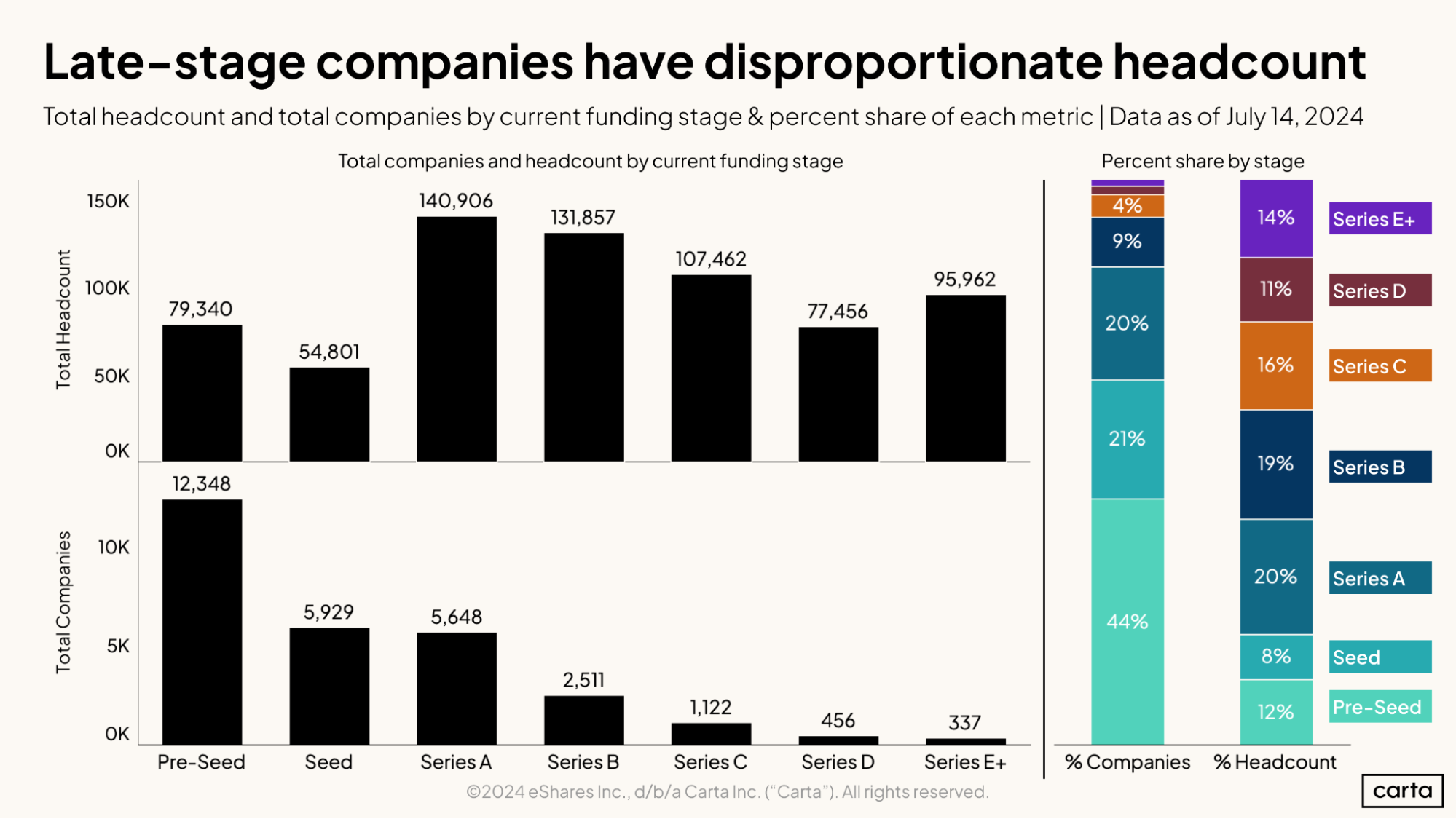

Less than 3% of all venture-backed companies on Carta are currently at Series D or later. But these late-stage companies account for about 25% of all headcount on Carta, a testament to just how much larger these advanced startups are than their early-stage peers. The average company at Series E+ has nearly 285 employees on its payroll, while the average pre-seed company has just six or seven employees.

Despite this huge disparity in average company size, total headcount across all employees on Carta is dispersed relatively evenly across the venture lifecycle. No stage comprises more than 20% of all employees on Carta (Series A), and no stage comprises less than 8% (seed).

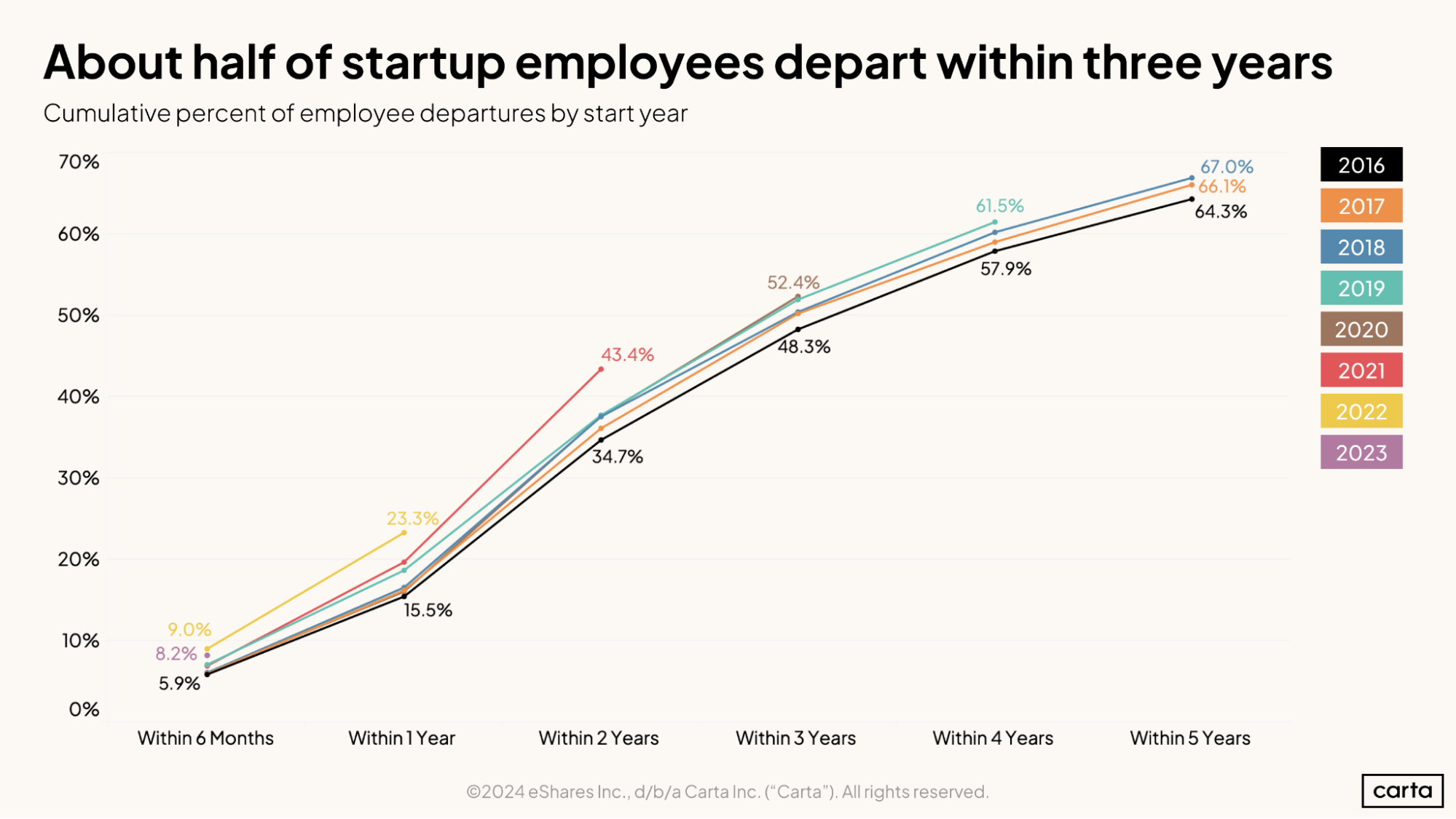

In recent years, the time between when an employee is hired and when they leave their job keeps getting shorter. Since the pandemic in particular, it appears that workers as a whole are less inclined to stick with jobs for longer periods of time.

One example: 43.4% of all employees on Carta who were hired in 2021 had left within two years. That proportion never reached 40% among workers hired in any year from 2016 to 2020. Another example: 23.3% of all employees hired in 2022 had left within one year. Again, that’s significantly higher than any of the previous six annual cohorts.

However, this trend may already be coming to an end. The cohort hired in 2023 saw 8.2% of employees leave within six months; while that’s higher than most recent years, it’s lower than the 9.0% rate for employees hired in 2022.

Companies that closed Series A rounds in the first half of 2024 had an average of 15.6 employees. That’s 16.3% lower than the average headcount for Series A companies five years ago, in 2019. The average employee count has also declined over that span at Series B and Series C.

The average size of seed-stage companies ticked up slightly between H1 2019 and H1 2024. On a shorter timeline, however, seed-stage companies are shrinking, too. The average seed startup was 23% smaller in H1 2024 than it was in H1 2021.

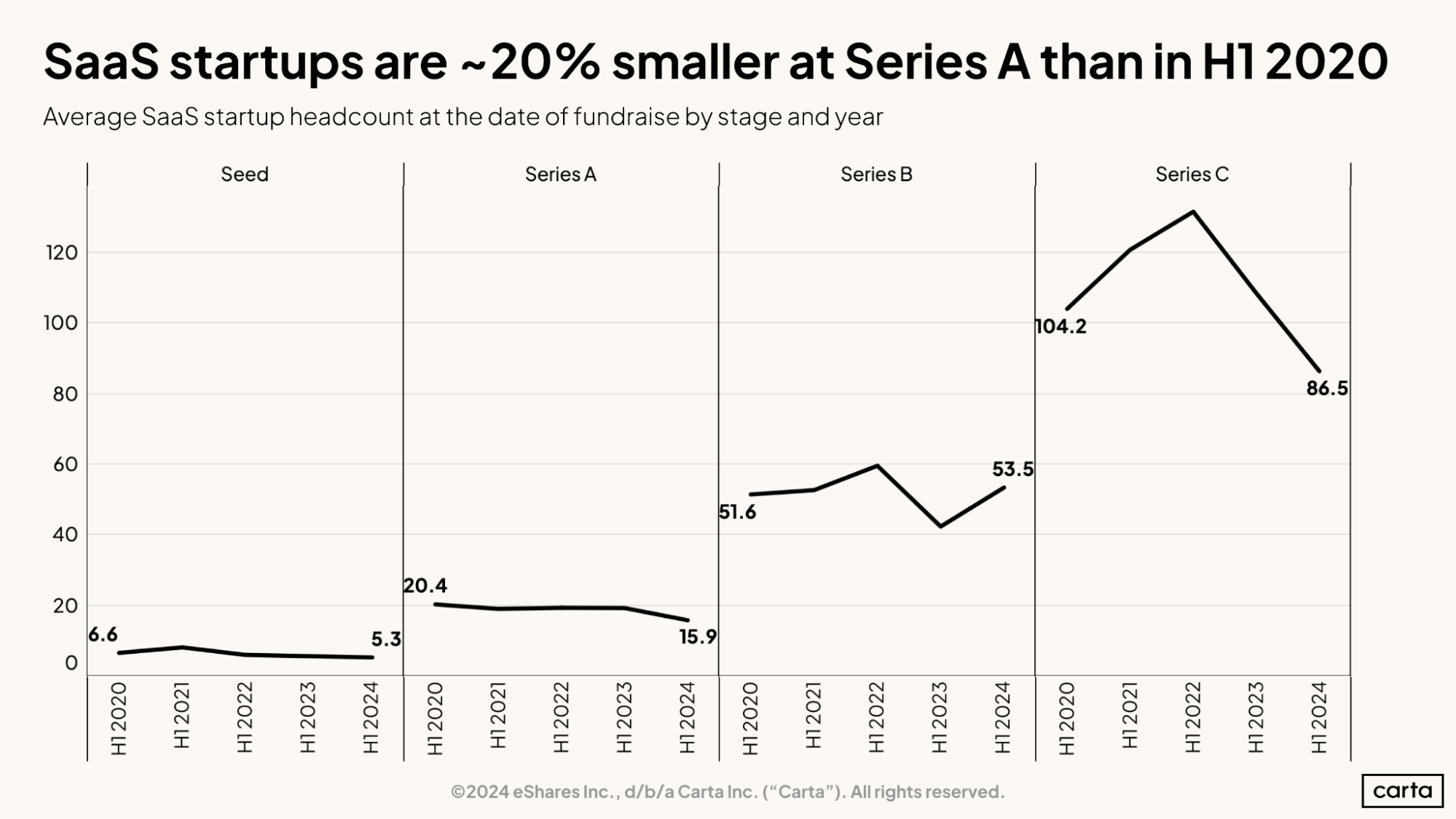

Similar trends in company size can be found within the SaaS sector, the most common industry designation for startups on Carta. Average headcount has declined over the past few years at seed, Series A, and Series C, and it’s increased only slightly at Series B.

The biggest recent shift has occurred at Series C, where median headcount for SaaS companies has fallen from 131.7 in H1 2022 to 86.5 in H1 2024, a 34.5% decline in the span of two years. This reduction in the typical size of Series C companies began at the same time as the recent slowdown in the broader venture market.

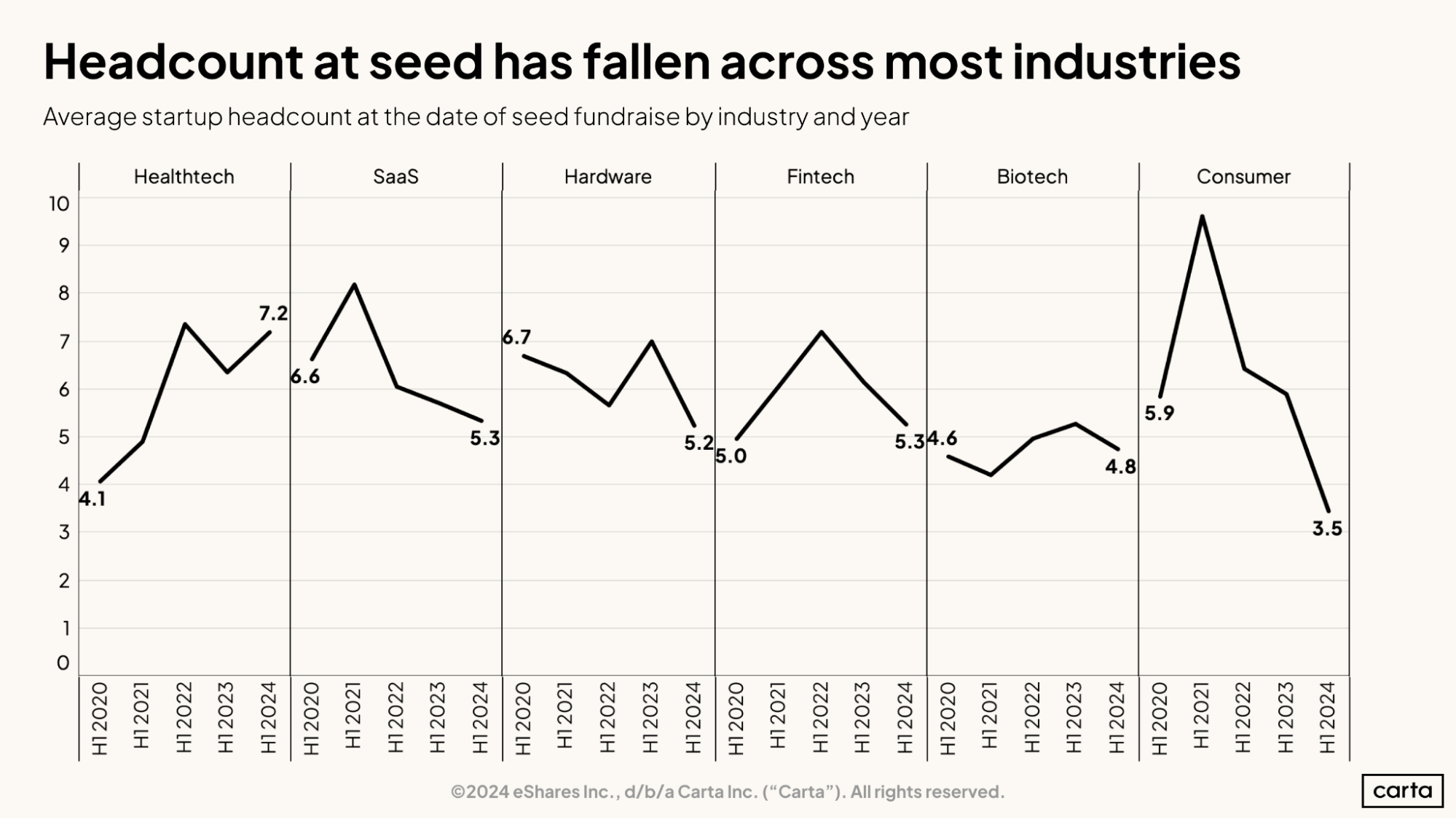

In some sectors, the typical size of companies that have raised seed funding has changed significantly in recent years. Average headcount at seed-stage healthtech startups rose by 76% from H1 2020 to H1 2024. On the other end of the spectrum, average headcount for seed-stage consumer startups declined by 41% over that same span.

In other sectors, little has changed in terms of company size over the past several years. Average seed-stage headcount has ticked up by the smallest of margins in both fintech and biotech.

A full table displaying average headcounts by industry across various fundraising stages can be found in this addendum.

Salary trends

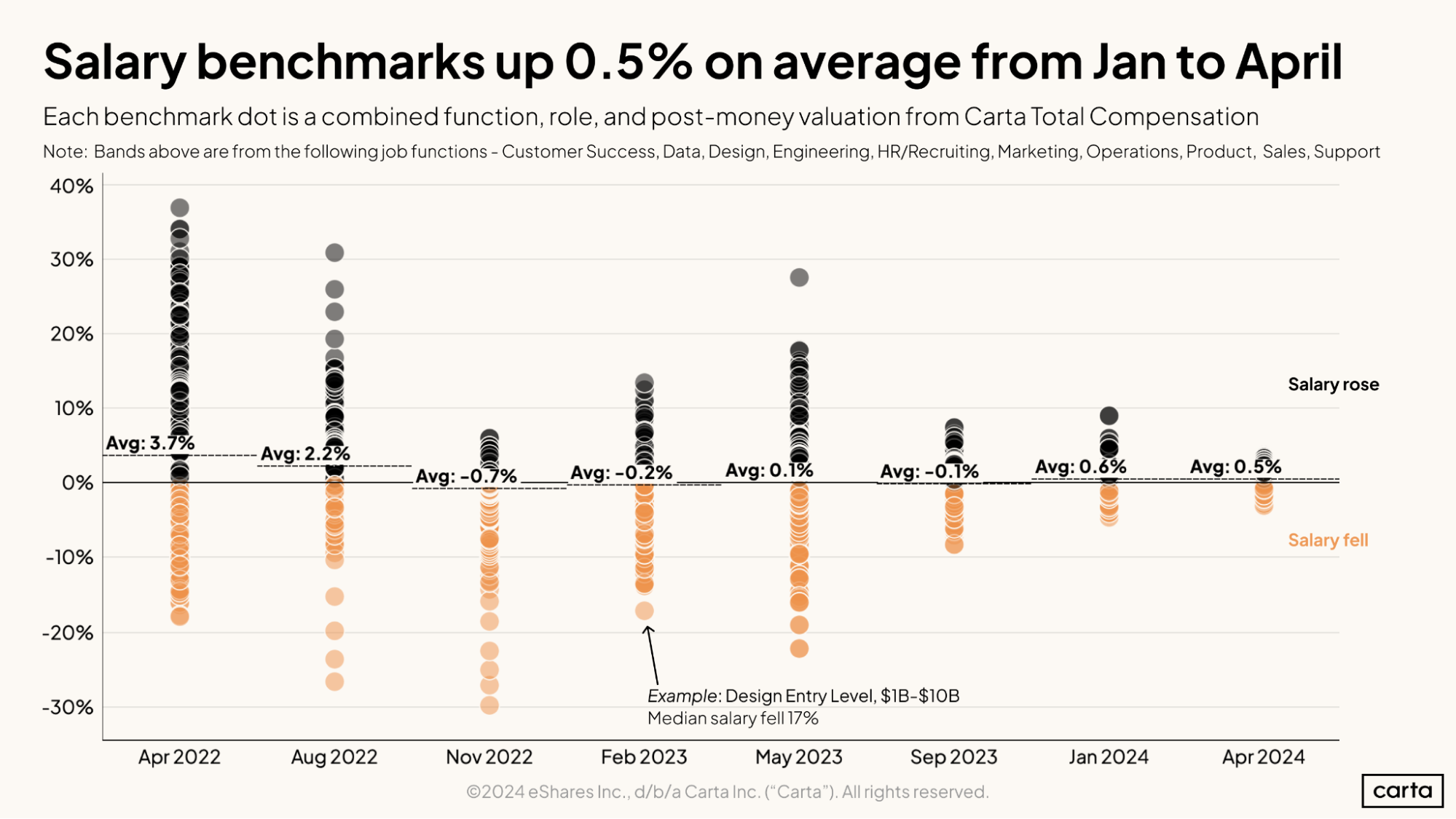

The average salary benchmark across a wide range of job functions increased by 0.5% between January and April, continuing a stretch of modest salary gains in recent months. The average salary benchmark previously rose by 0.6% between September 2023 and January 2024.

Over this same recent span, the distribution of salary benchmark movement has grown much more compact—fewer job functions are seeing salaries rise significantly, and fewer are seeing salaries fall significantly. In fact, no salary benchmark rose or fell by more than 5% between January and April.

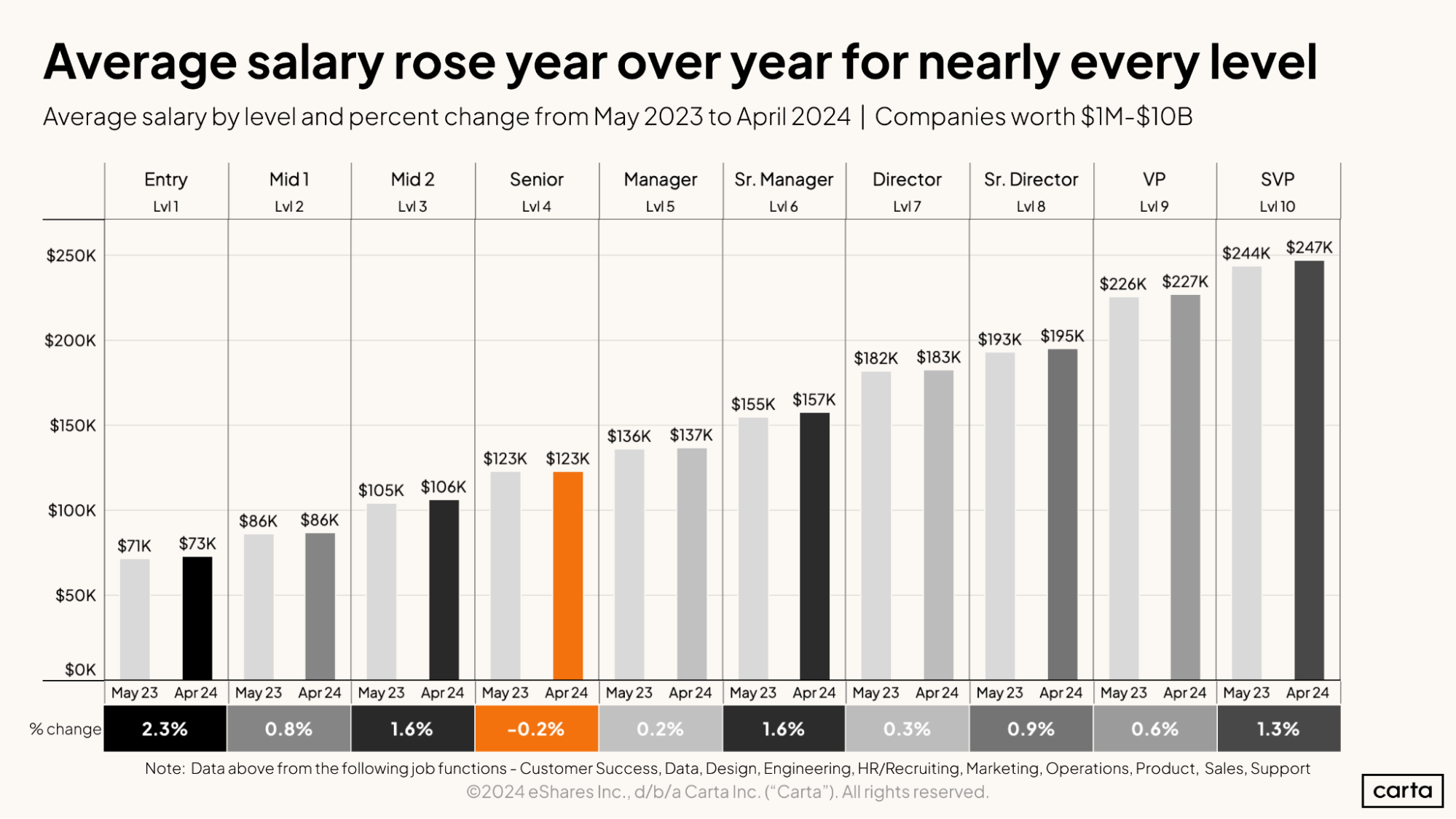

Employee paychecks got bigger in the past year. The average salary on Carta increased from May 2023 and April 2024 for nearly every job level, with senior individual contributors the lone exception. In terms of percentage gains, the largest increases occurred for entry-level employees, who saw their average salary rise by 2.3%.

For every job level, however, the average increase in salary over this span did not keep pace with inflation. The annual inflation rate in the U.S. was 3.4% for the 12 months ending in April 2024.

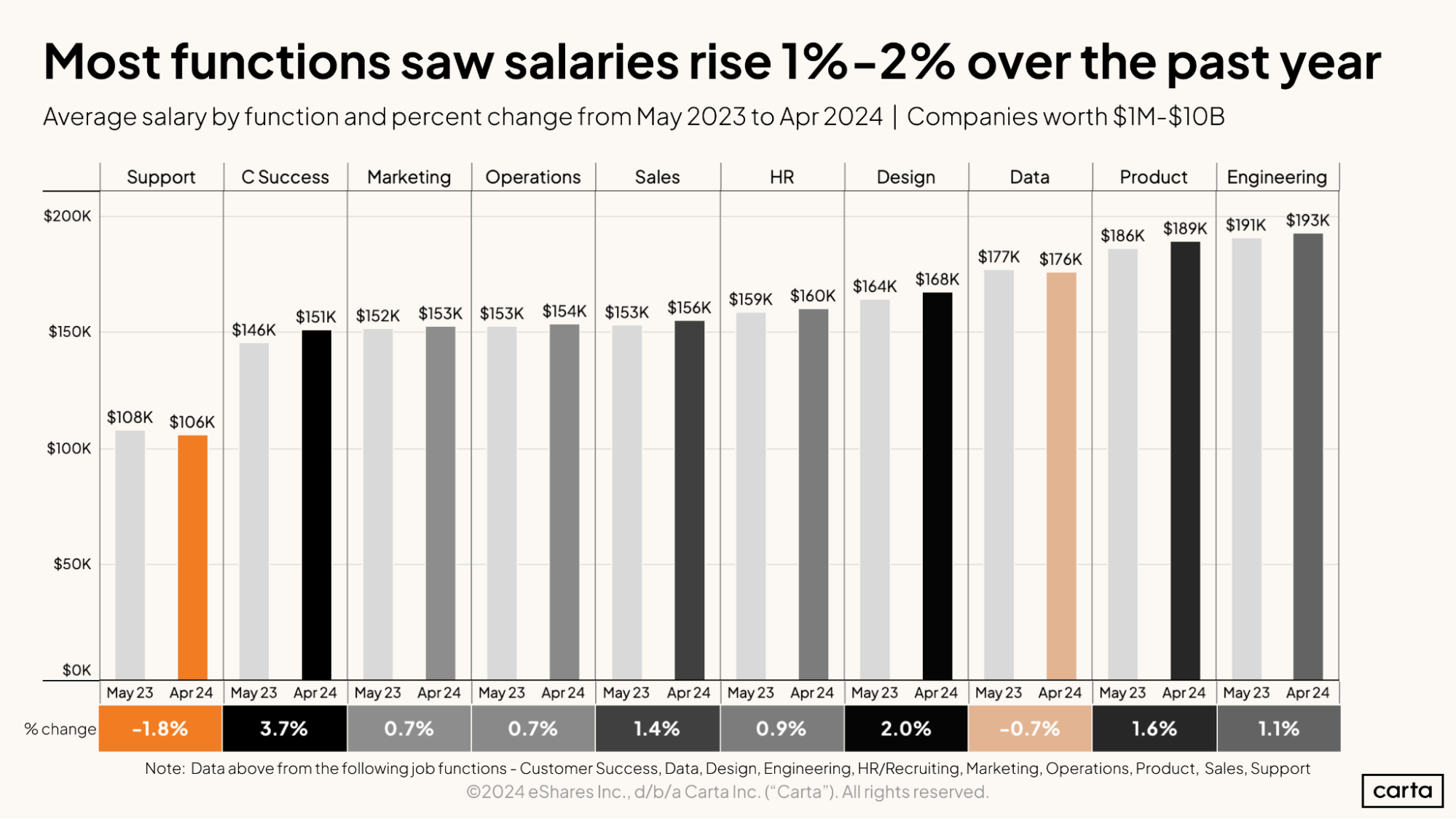

Average salaries stayed mostly steady from May 2023 to April 2024 across different job functions, as was the case for different job levels. But there’s a bit more variation among functions, at both ends of the financial spectrum. The average salary for customer success employees increased by 3.7% during this span—outpacing inflation—while the average salary for support employees declined by 1.8%.

As of April, average salaries were quite similar across customer success, marketing, operations, and sales, with all of those functions landing somewhere between $150,000 and $160,000. Product and engineering are clearly the two highest-paying functions, with average salaries around $190,000.

Equity trends

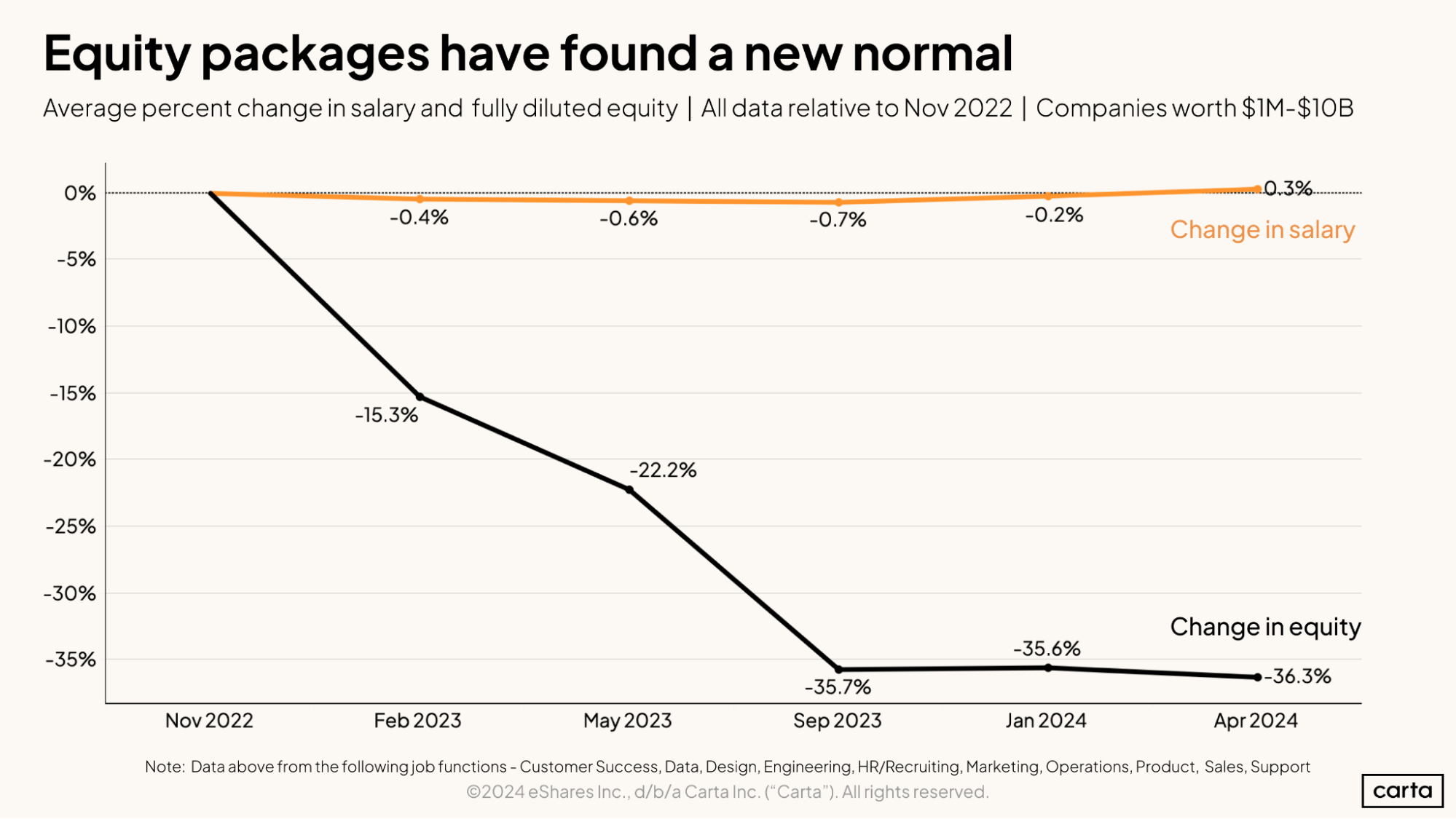

The average size of equity packages issued to new hires (measured on a fully diluted basis) has declined substantially since November 2022. Since September 2023, however, it has barely budged. The startup world as a whole seems to have settled on a new normal for the amount of equity compensation that new hires can expect—at least for now.

Average salaries, meanwhile, have moved only marginally over the past 18 months. But the recent trend is up: The average salary has now risen above what it was in November 2022 for the first time.

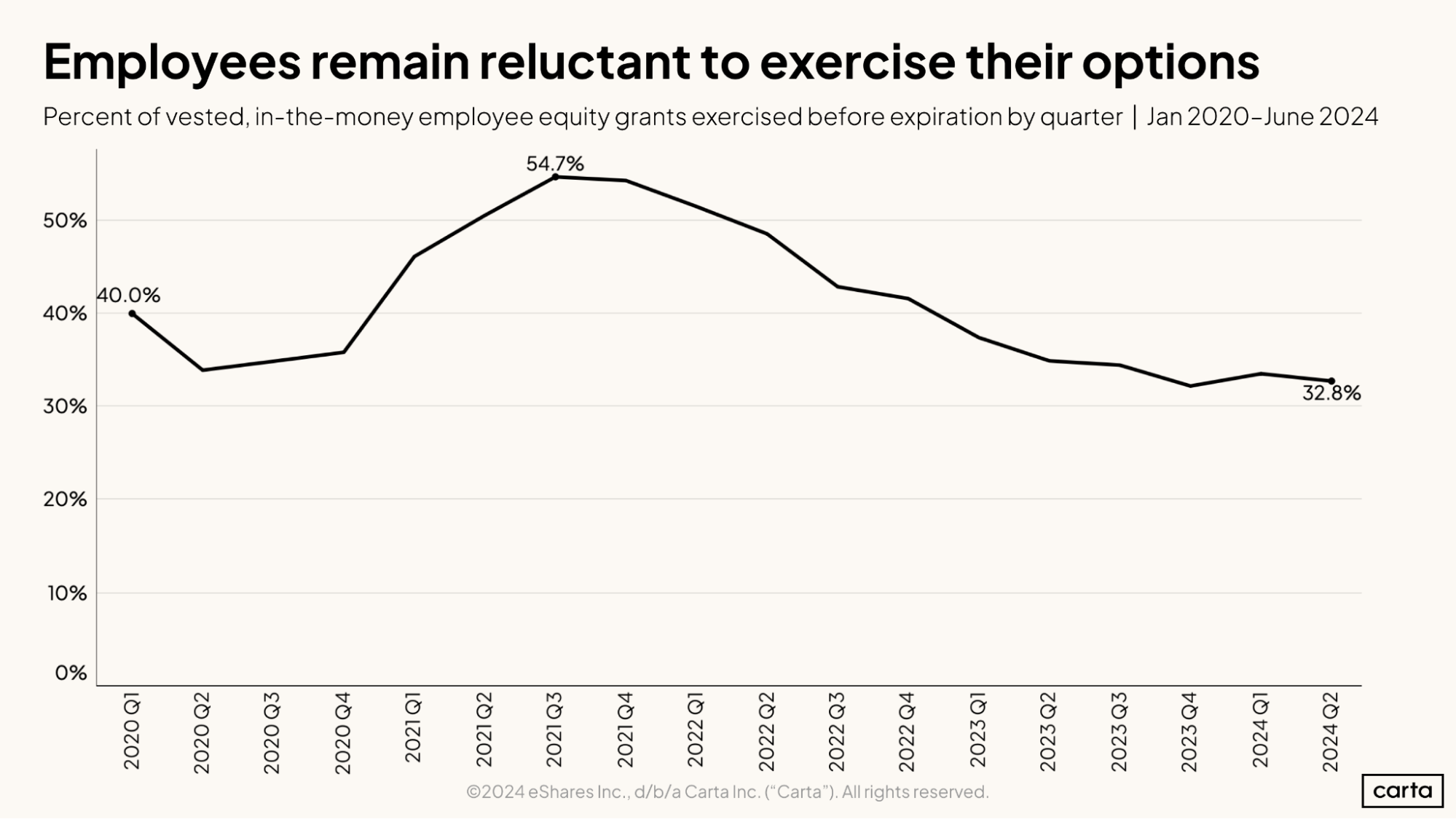

The percentage of vested, in-the-money stock options that employees choose to exercise before they expire has been in a state of steady decline over the past few years. There was a brief pause to this trend in Q1 2024, when the exercise rate ticked up slightly. But it resumed again in Q2, as the exercise rate fell once again, dipping to 32.8%.

In general, option exercise rates tend to correlate with venture-backed valuations and with employee confidence: Employees are more likely to exercise options when valuations are high, because they believe doing so will be financially worthwhile. The recent decline in the overall exercise rate has tracked closely with the recent timeline of declines in valuations.

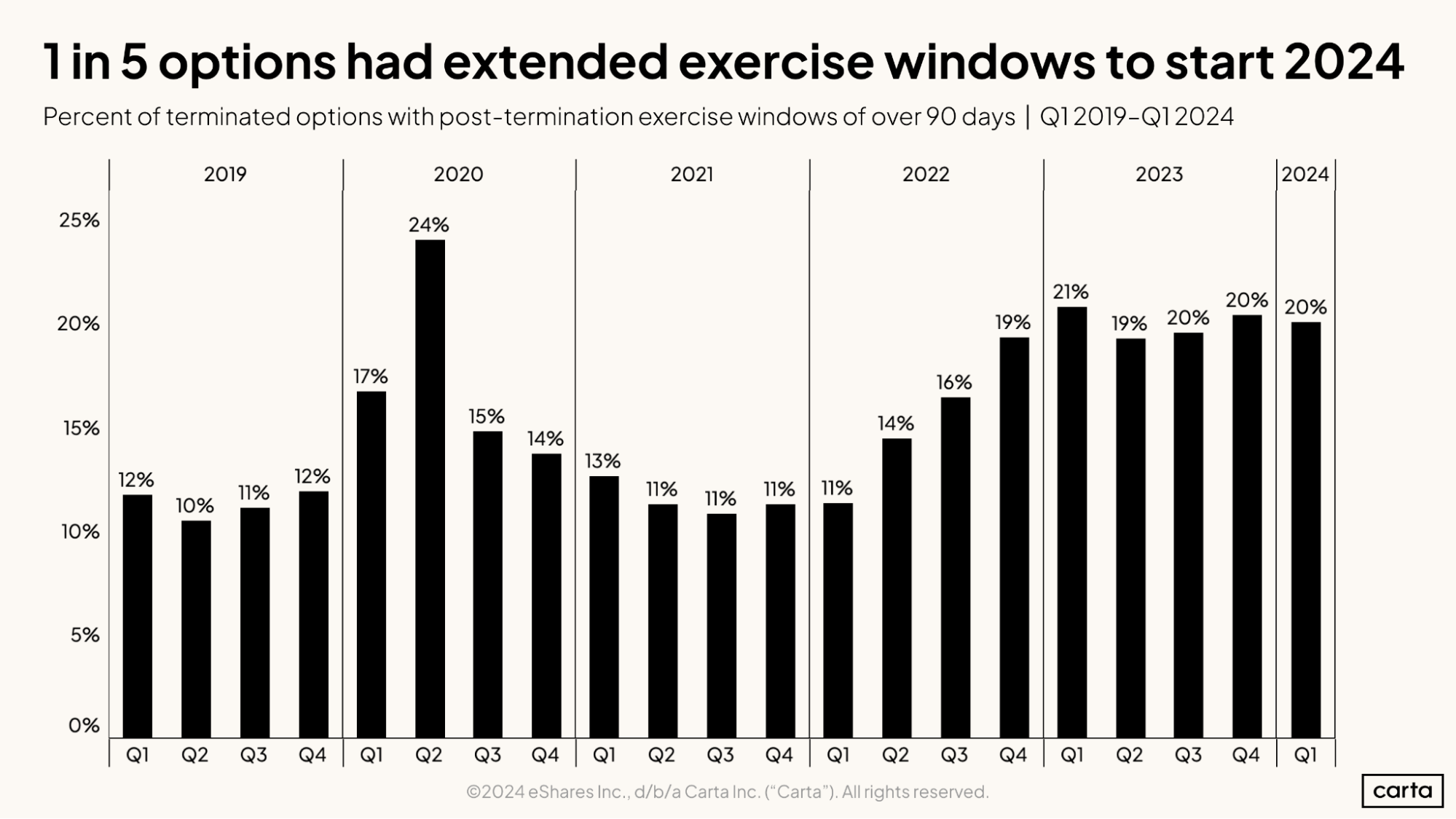

Most of the time, when a company parts ways with an employee, the former employee has 90 days to decide whether to exercise any vested stock options. Over the past several quarters, however, the frequency with which companies offer an extended post-termination exercise period (PTEP) longer than 90 days has gone up—and now seems to have settled on a new normal.

In each of the past six quarters, the rate of extended PTEP for terminated options has landed somewhere between 19% and 21%. In each of the past three quarters, it’s landed at an even 20%. To some degree, this increase in extended PTEP may be a response to higher layoff rates in recent quarters. It may also be part of a long-term shift in how companies treat terminated options.

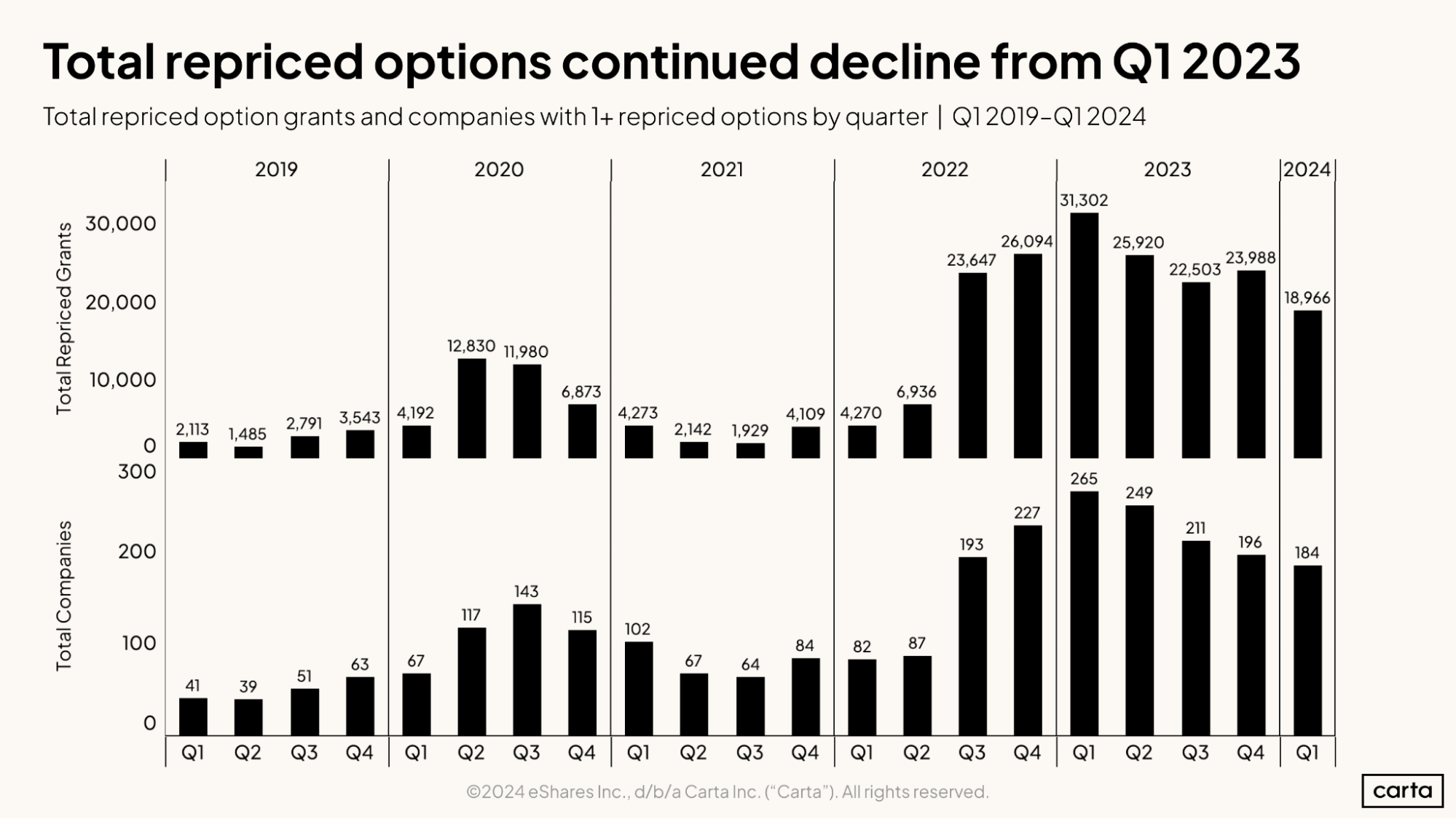

In Q1, 184 companies on Carta combined to reprice 18,966 individual stock option grants. Both of these numbers are lower than the repricing figures for any quarter in 2023. But they’re also significantly higher than the repricing levels seen in 2019, 2020, and 2021.

Option repricings tend to be more common in times when venture-backed valuations are either flat or declining. In that sort of environment, repricing previously issued options is a way for companies to make those options more attractive currency to their employees and other shareholders. The rise in options repricings aligns neatly with the slowdown in venture activity that began in 2022.

Compensation geography

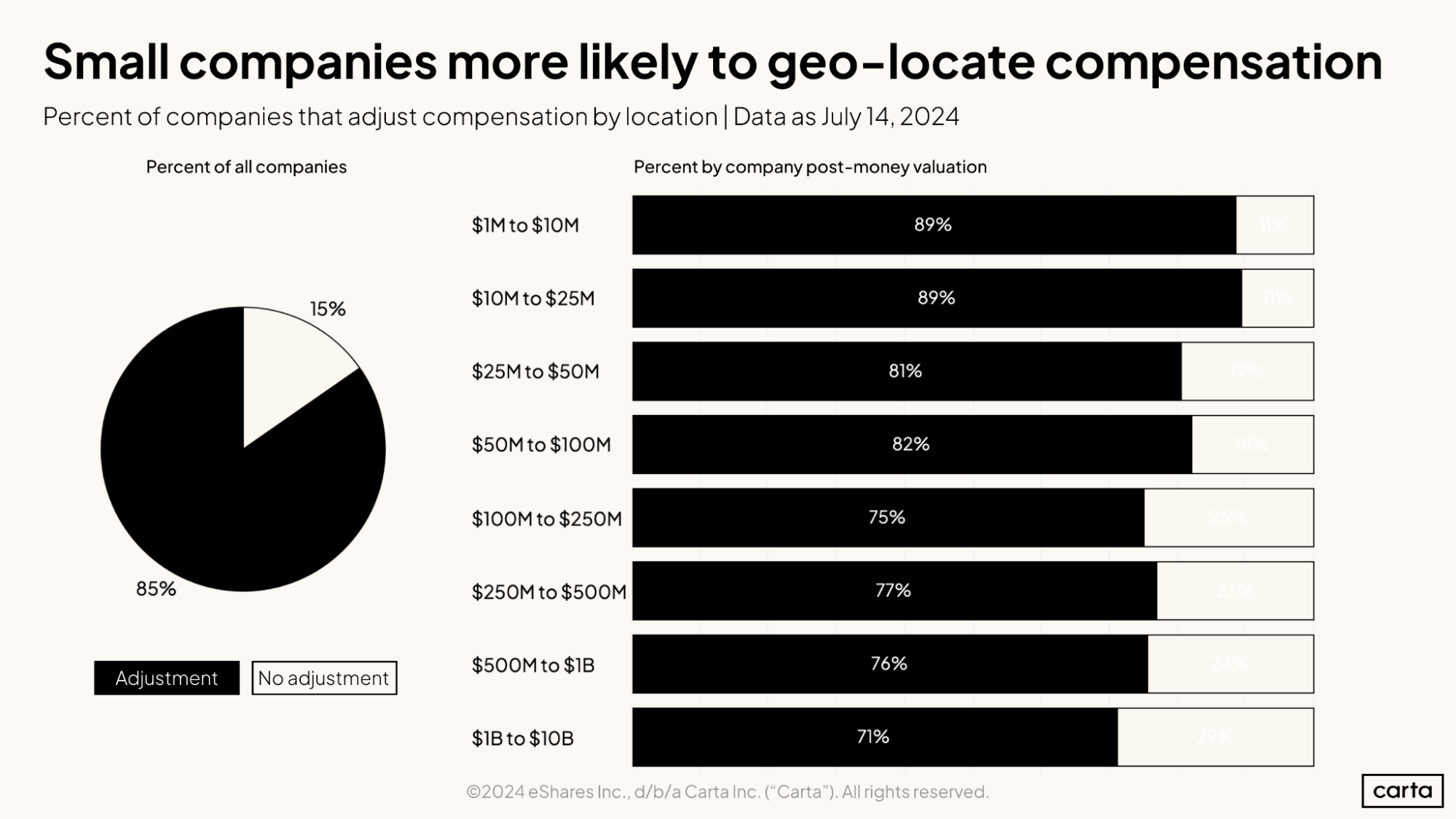

No matter their size, the majority of venture-backed startups adjust their compensation based on an employee’s location. But smaller companies are a bit more likely to offer geographic adjustments than larger companies. Nearly 90% of all startups valued at less than $25 million factor in an employee’s location when determining compensation, compared to just 71% of all companies valued at $1 billion or more.

Exceptions abound, but in general, startups on the lower end of the valuation spectrum tend to be younger, while more valuable startups tend to be more mature. Less-valuable startups are more likely to geo-locate compensation; this could be due in part to a shift in market sensibilities, with companies formed in the last few years more likely to offer location-based adjustments than older companies that came of age prior to the pandemic.

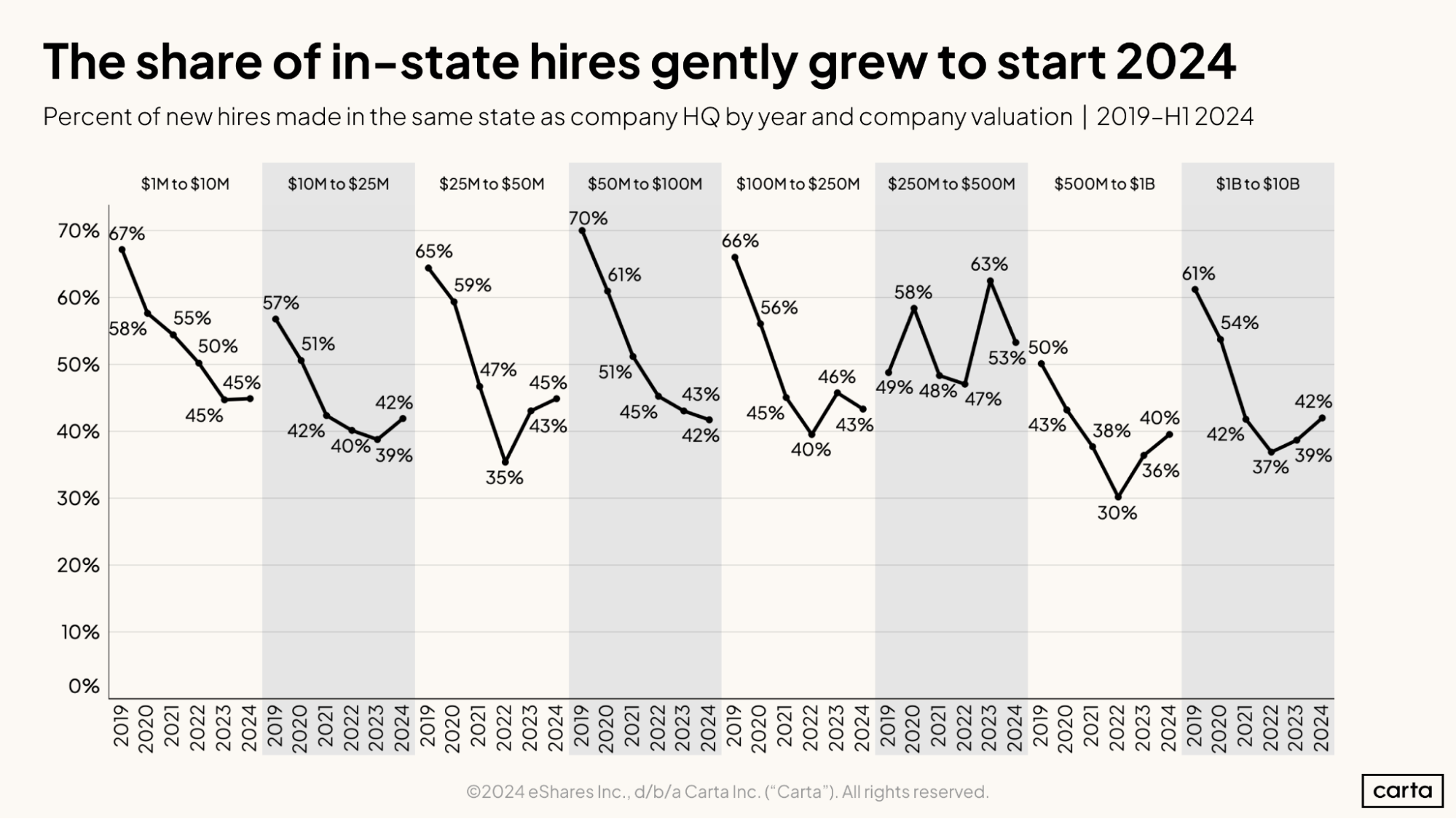

Over the past few years, startups have grown less likely to make hires in their home state and more likely to add talent in other markets. In some cases, there’s been a significant shift. For instance, back in 2019, startups valued between $1 million and $10 million made 67% of their hires in their home state. By 2023, that rate had fallen to 45%.

But that trend has not necessarily continued into 2024. The frequency of home-state hires has ticked up so far this year for companies valued between $1 million and $10 million. It’s also increased for startups valued between $10 million and $50 million, and for much larger companies valued at $500 million or more. For startups in that middle ground—valued between $50 million and $500 million—in-state hires continued to decline in frequency in 2024.

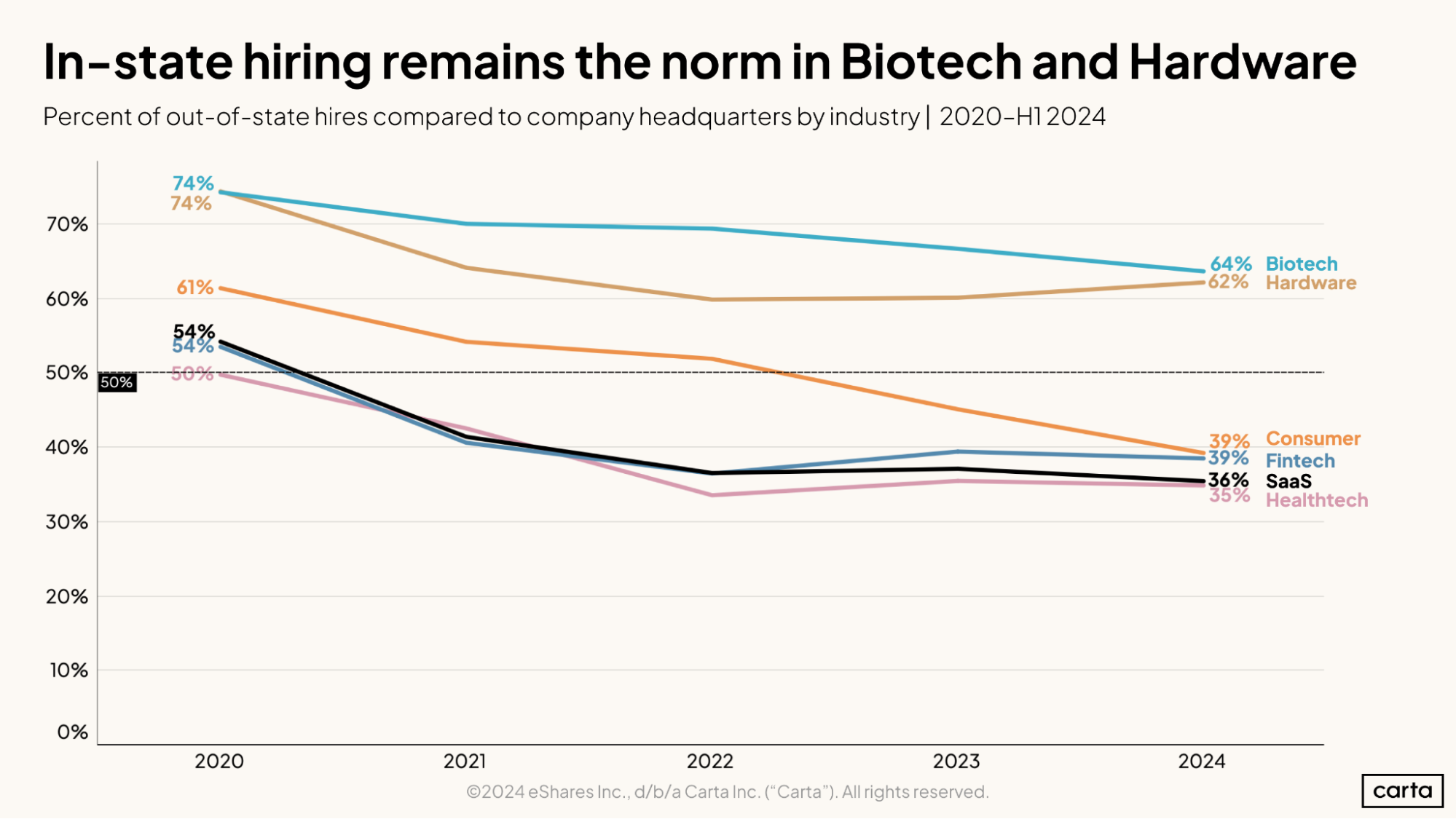

The markets where startups look to hire can also depend on their industry, as well as their valuation. Companies in research-intensive industries such as biotech and hardware, for instance, still make a majority of their hires in the same state where they’re based. Companies that are more reliant on software—such as those in fintech and consumer—are much more likely to make out-of-state hires.

The geographic complexion of startup hiring is undergoing a clear shift in the 2020s. One of the biggest changes has come in SaaS. Back in 2020, about 54% of all new hires at SaaS startups worked in the same state that their company was located. So far this year, that rate has fallen by a third, dropping to 36%.

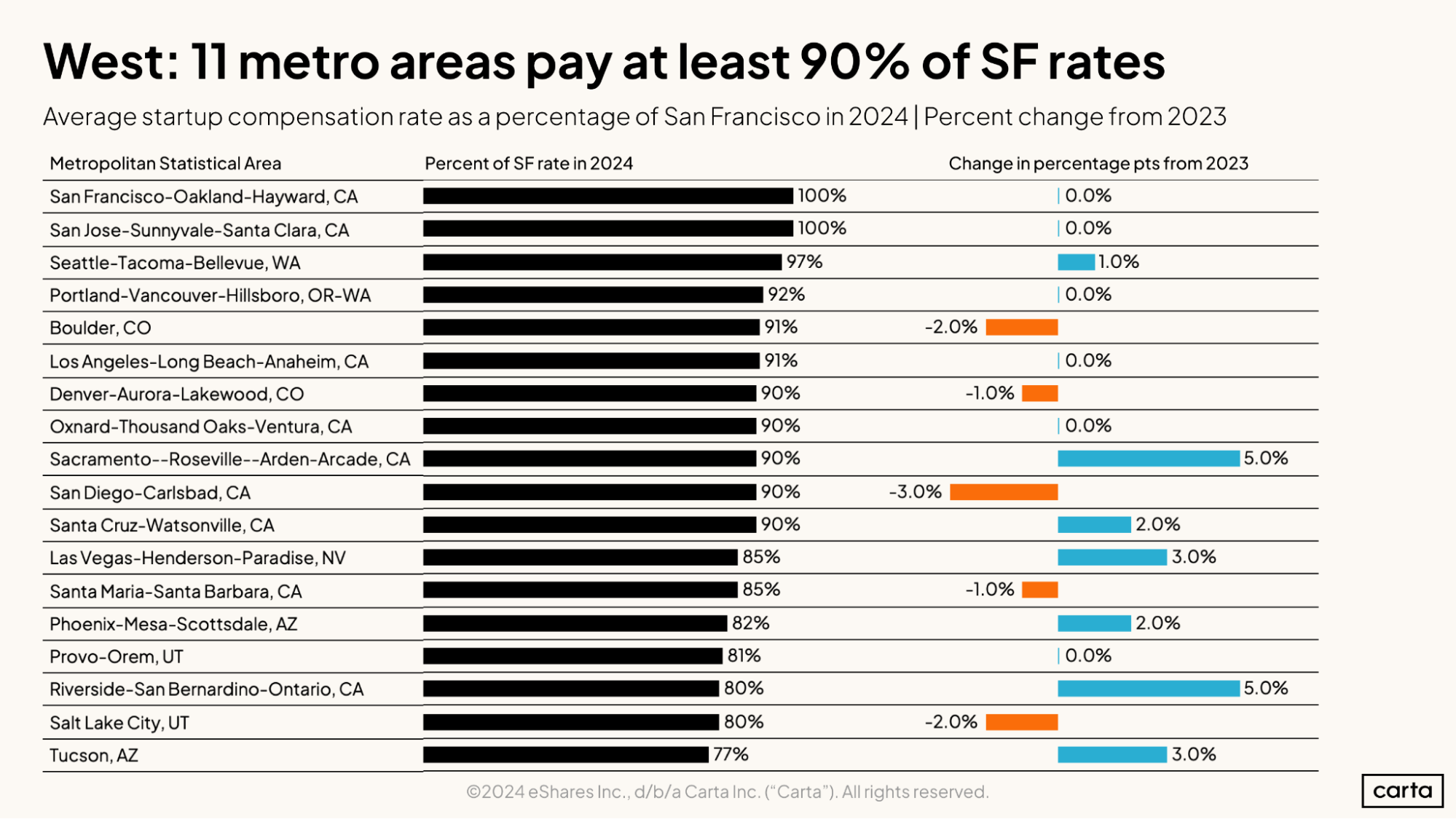

In terms of geography, compensation is typically higher for startup employees who work in the Bay Area than any other market in the West census region. But plenty of other metros aren’t too far behind. Employees in the Seattle area have been paid at about 97% the level of San Francisco and San Jose so far in 2024, while eight other metro areas are at 90% or higher of San Francisco levels.

Some of the biggest gainers so far this year have been in California: Workers in the larger Sacramento region and the Riverside metro have both seen their average compensation increase by 5% in 2024 relative to average compensation in San Francisco. San Diego, Boulder, and Salt Lake City, meanwhile, have all seen compensation levels dip relative to San Francisco.

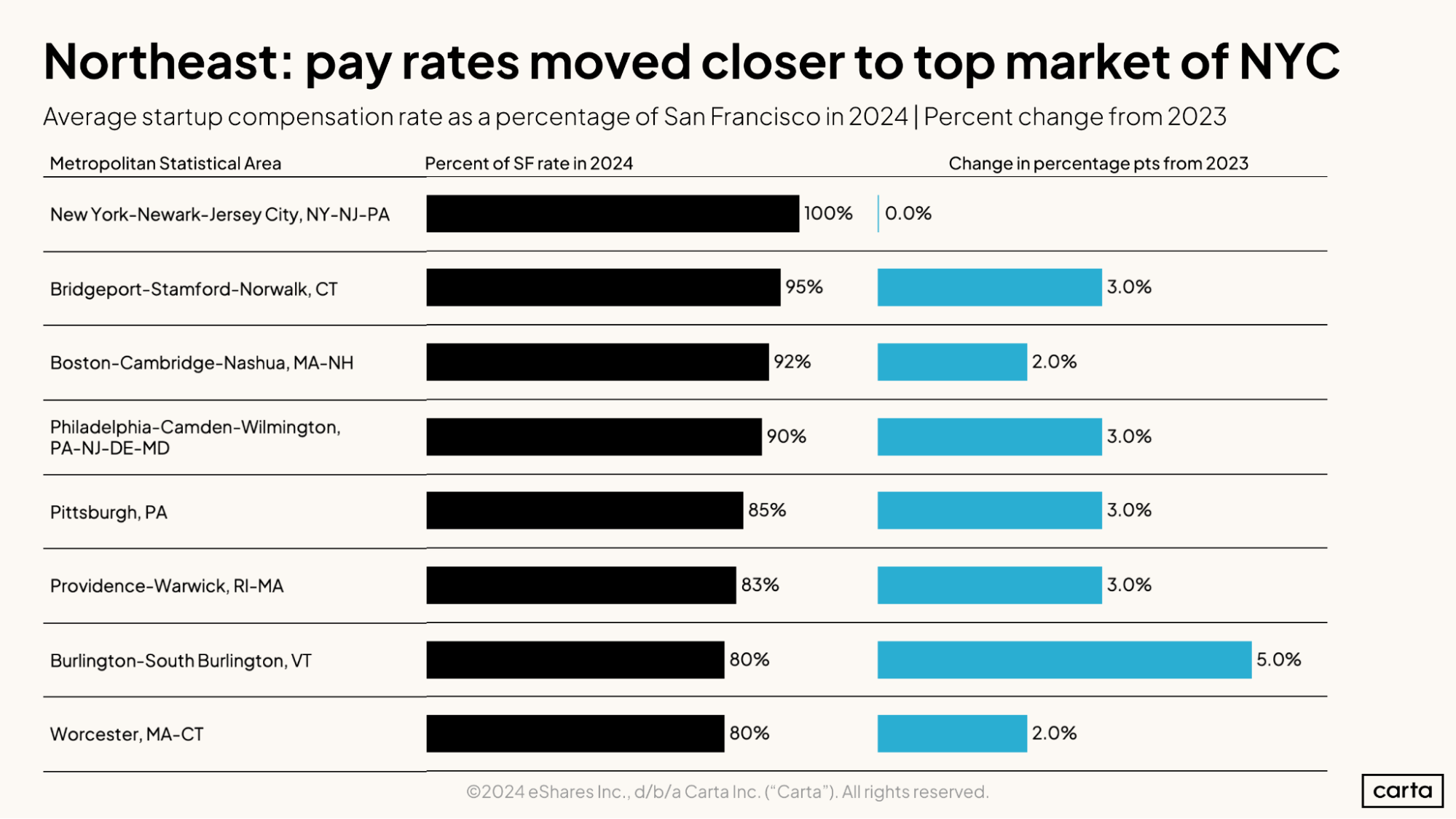

New York City is the only metro area where average compensation can equal that of the Bay Area. Thus, it remains the standard for compensation in the Northeast census region. But several other markets are gaining ground.

Average compensation in Boston is at 92% of average compensation in New York so far this year, up two percentage points. Workers in Burlington, Vt., have gained five percentage points on their peers in New York. Philadelphia, Pittsburgh, and Bridgeport, Conn., are among the other regions where pay has increased in 2024 relative to the top of the market.

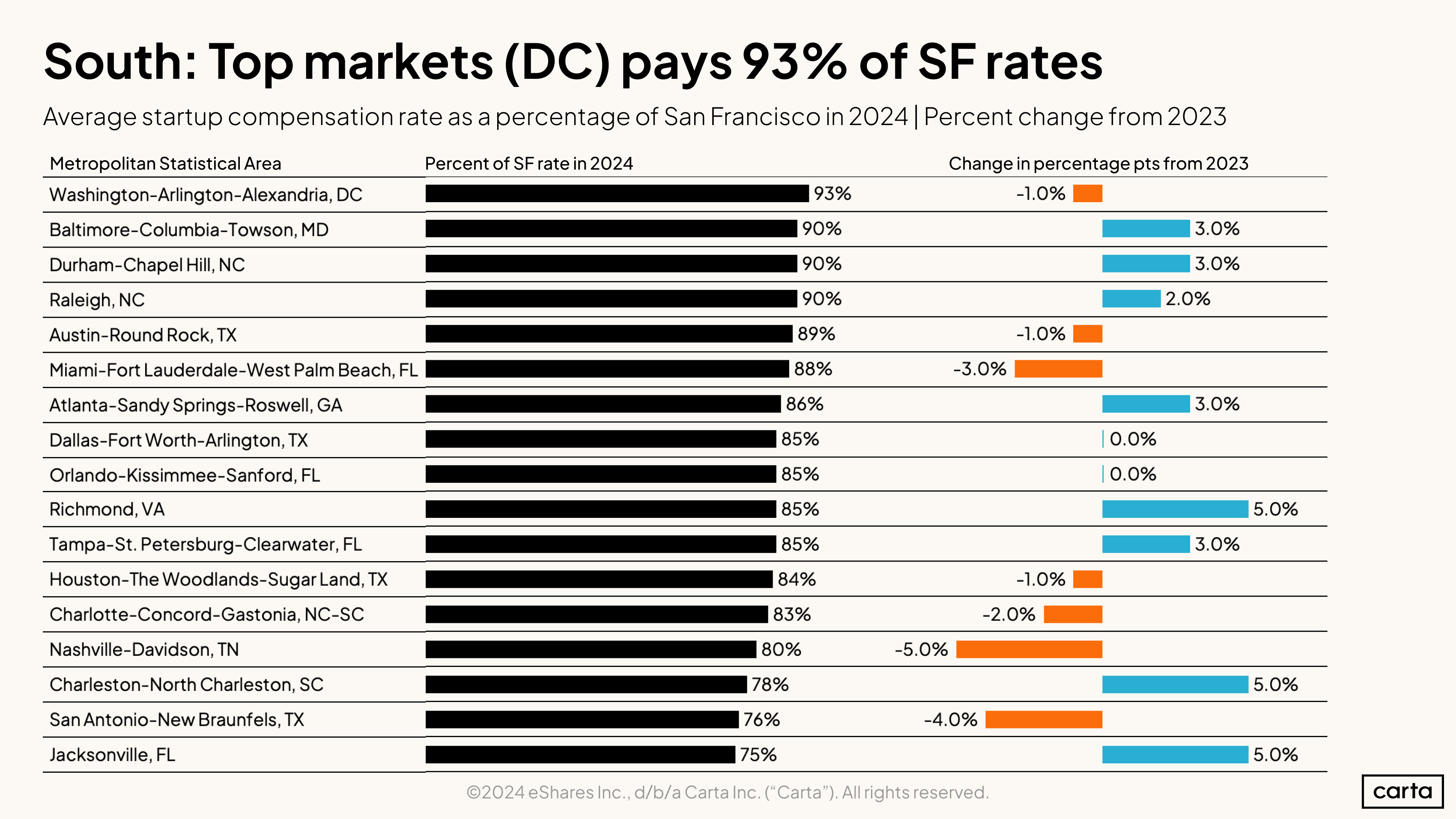

The South census region is full of metro areas where average compensation levels are somewhere between 80% and 90% of what they are in San Francisco. And several of those metros have experienced notable changes so far in 2024.

Average compensation is up this year in Baltimore and the North Carolina Research Triangle. It’s risen even higher in Richmond, Va., and Charlotte, N.C., both of which have seen gains of five percentage points. Conversely, in Miami, average compensation has declined by three percentage points so far this year relative to San Francisco. Nashville and San Antonio have also seen relative compensation levels decline.

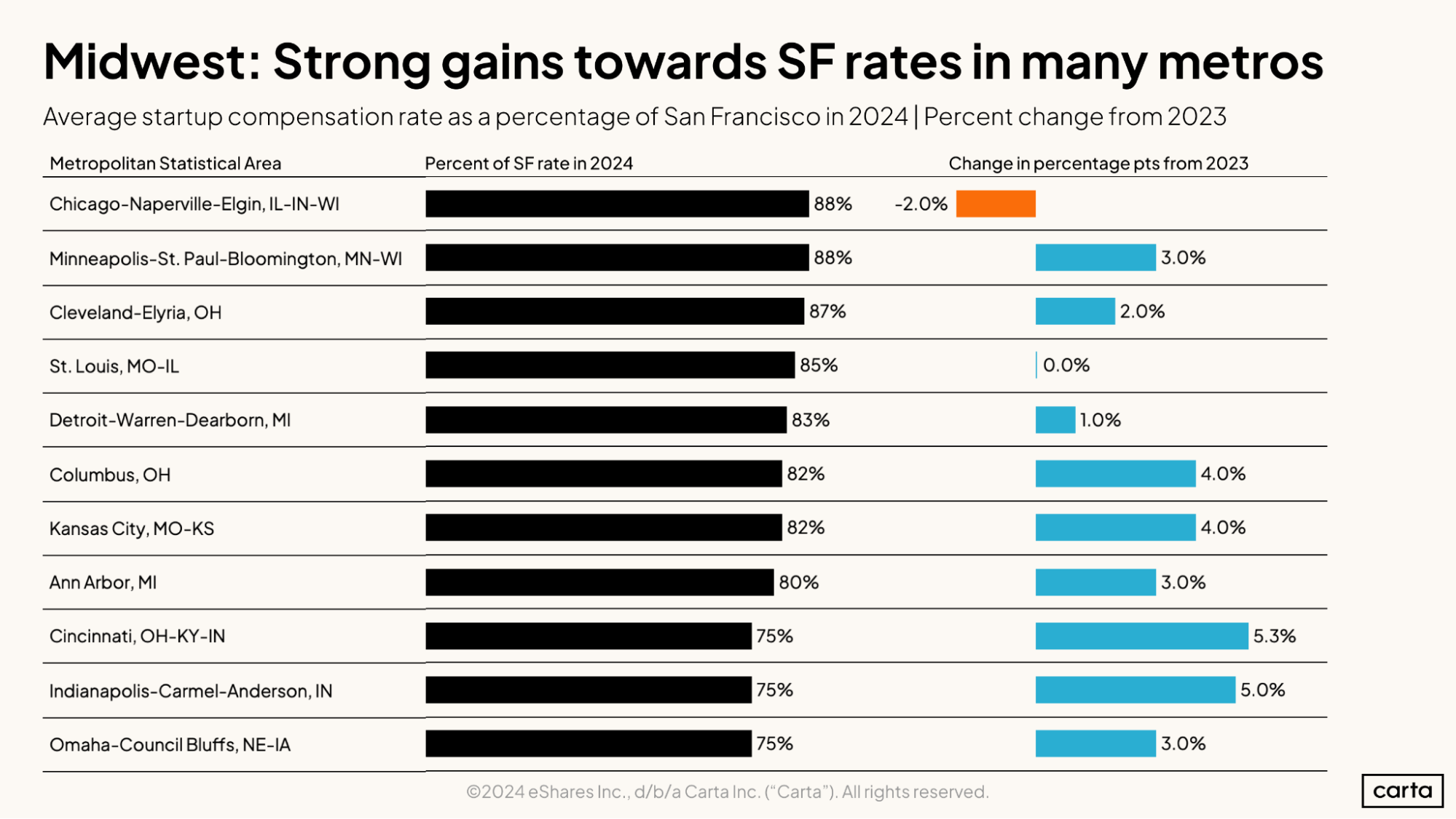

In terms of compensation, it’s been a promising start to the year for most of the major metro areas in the Midwest census region. Average compensation in Chicago is down two percentage points relative to San Francisco, and it’s flat in St. Louis. But average compensation has ticked up in nine of the region’s other notable metros, including gains of more than 5% in Cincinnati and Indianapolis.

Chicago is the traditional standard-bearer for the Midwest venture market. But in terms of compensation, at least, the gap between the Windy City and its peers is shrinking—or, in one case, has vanished entirely. Average compensation in the Twin Cities is now equal to average compensation in Chicago, and Cleveland and St. Louis are not far behind.

Additional equity compensation data

Download the equity addendum below to see:

Employee option pool sizes by valuation

Median advisor equity for pre-seed, seed, and Series A companies

Median equity grants for a startup’s first 10 employees

Median equity grants for startup board members at the early stages

Average headcount by stage and industry over time

Methodology

Overall dataset

This report comes from thousands of CTC customers with over 500,000 data points used by Carta Total Compensation. Other metrics in the report, such as those that describe employee movement, derive from the aggregate pool of more than 1 million employees currently working for the 45,000 startups that use Carta to manage their cap tables.

The data presented above represents an aggregated, anonymized view into the compensation practices of these startups. Companies that have contractually requested that we not use their data in anonymized and aggregated studies are not included in this analysis.

This report represents a snapshot as of July 14, 2024. Historical data may change in future studies. New companies signing up for Carta’s services will increase the amount of data available for the report.

Salary & equity

All salaries presented in this report are expressed in U.S. dollars. Except where indicated, total payroll numbers do not include any variable compensation, such as bonuses or commissions, that may be given to employees.

All equity values presented in this report are expressed as a percentage of fully diluted company shares.

In the sections on salary and equity trends, changes over time reflect updates to Carta Total Compensation bands. These benchmarks are updated once per quarter to incorporate newly hired employee data as well as any adjustments to current employee compensation.

DISCLOSURE: This communication is on behalf of eShares Inc., d/b/a Carta Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. ©2024 eShares, Inc. dba Carta, Inc. ("Carta"). All rights reserved. Reproduction prohibited.