Nearly all of the venture capital funds that formed between 2017 and 2024 are still actively managing their portfolio companies, and most are still seeking their first successful exit. It’s still far too early to draw confident conclusions about what the final performance of these various fund vintages will look

But with data from more than 2,500 venture funds that currently use Carta Fund Administration, we can examine a current snapshot of fund performance for these latest VC vintages for signs of where they might be headed.

Across funds in the 2017 vintage, for instance, the median IRR was 11.5% at the end of Q1 2025. The median TVPI—a metric that tracks the total growth of a fund’s value—was 1.72x. And the median DPI—which tracks returns distributed back to LPs—was 0.27x.

But within this cohort of funds, there is substantial variation. At the 25th percentile of performance, median IRR for the 2017 vintage is just 5%. At the 75th percentile, it’s 18.7%. Up at the 90th percentile, where the best performing funds reside, the median IRR for 2017 funds is 28.3%.

Some of these recent vintages are at very different points in their fund lifecycles than others and have had the opportunity to invest in very different market climates. This report aims to explore the impact these variables have had so far on each vintage’s performance metrics.

Only U.S. funds are included in this analysis, and all included funds are direct venture investors, as opposed to funds of funds. Funds must be in vintage years 2017 through 2024. More detail on our methodology can be found at the end of this report.

Highlights

For recent funds, DPI is hard to find: Just 37% of funds in the 2019 vintage and 30% of funds from 2020 had generated any amount of distributions for their LPs by the end of Q1 2025.

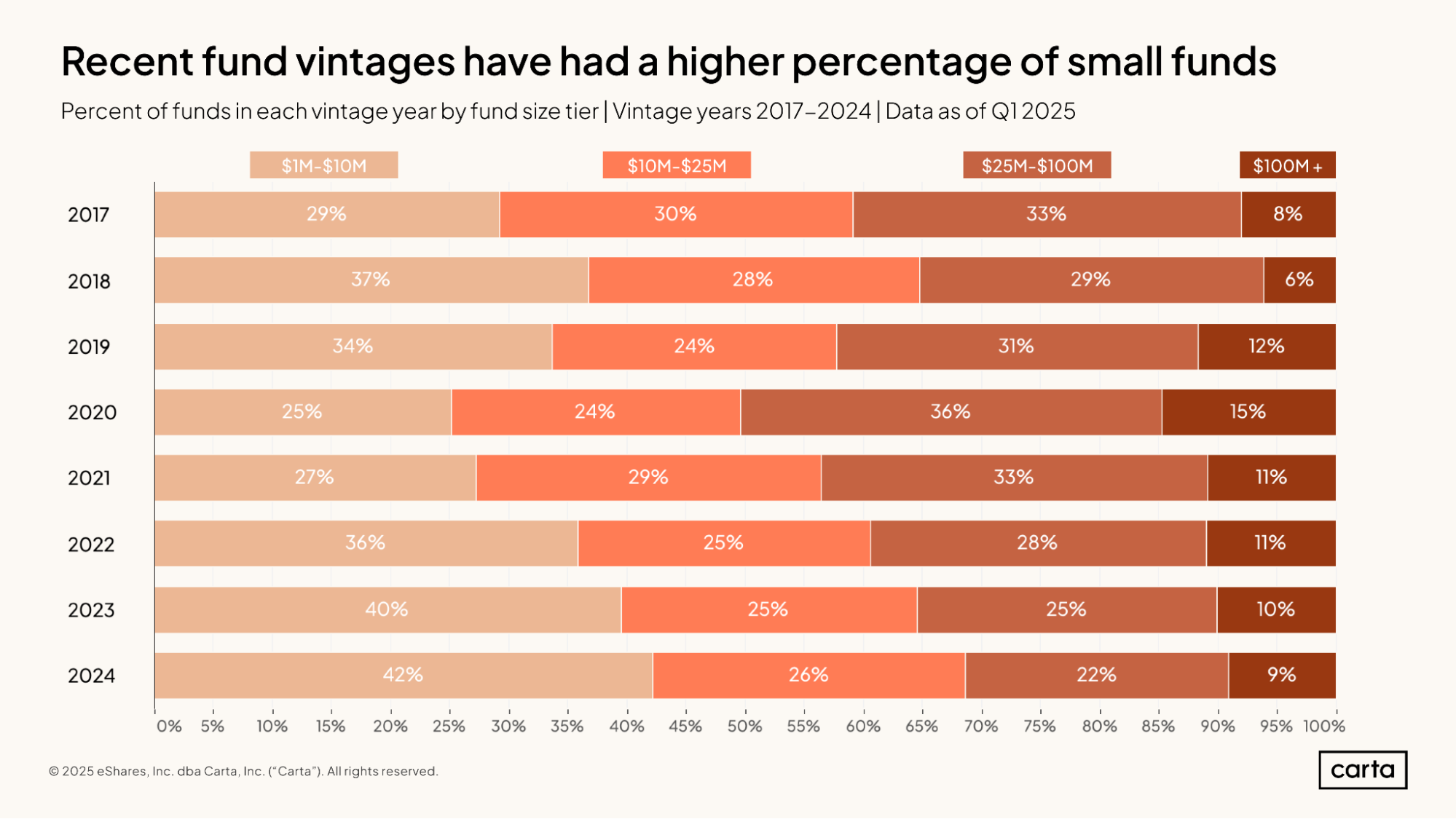

Smaller funds have grown more common: Back in the 2020 vintage, 25% of closed venture funds in this sample were between $1 million and $10 million in size, and 36% were between $25 million and $100 million. In the 2024 vintage, the scales flipped: 42% of funds were between $1 million and $10 million, and 22% were between $25 million and $100 million.

TVPI figures show slight positive momentum: The median TVPI increased in Q1 for each of the 2017, 2018, and 2020 vintages. Before this, the TVPIs for these vintages had been steadily trending down. Median TVPI for the 2018 vintage, for instance, had declined in each of the past five quarters.

Fund details

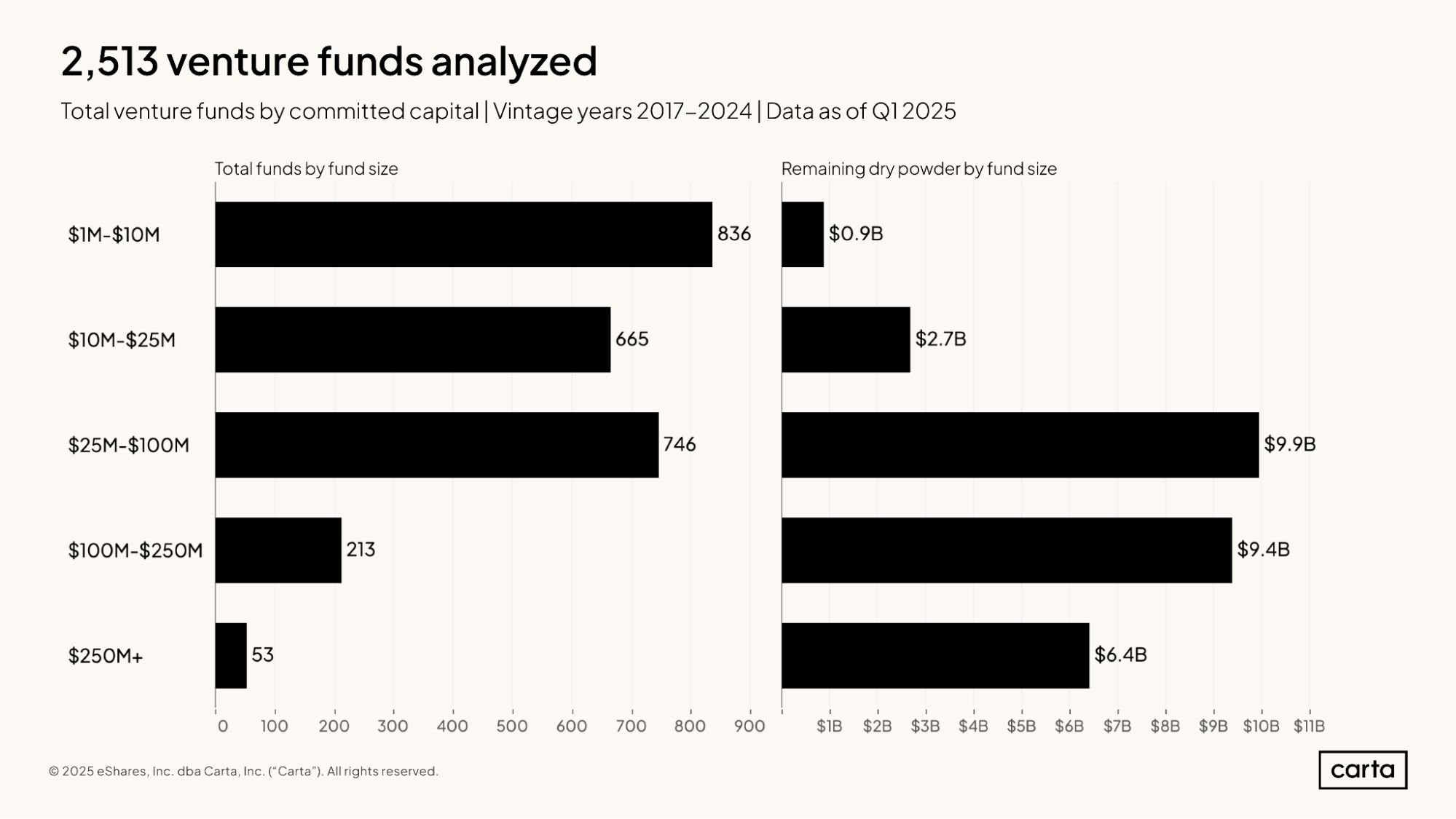

This analysis includes data from 2,513 venture funds with vintage years ranging from 2017 through 2024. A large majority of these funds—about 89%—have less than $100 million in committed capital, while about 11% are larger than $100 million.

This 11% of $100 million-plus funds, however, combine to account for 54% of all dry powder currently committed to funds in this sample. In venture capital, as in much of the private markets, a relatively small minority of funds typically maintains an outsized portion of the buying power.

Throughout the 2020s, the percentage of venture funds that have less than $10 million in committed capital has been steadily increasing with each new vintage. In the 2024 vintage, 42% of all funds were between $1 million and $10 million in size, compared to 25% of funds at the start of this decade.

The percentage of funds larger than $100 million declined some over this span, falling from 15% in 2020 to 9% in 2024. But the larger change has come in the cohort of funds that are between $25 million and $100 million in size. These accounted for 22% of the 2024 fund vintage, down from 36% in 2020.

To at least some degree, this tilt of the market toward smaller funds is likely symptomatic of some LPs cutting their contributions to the venture capital asset class. In a less frothy venture ecosystem, smaller funds may become more common.

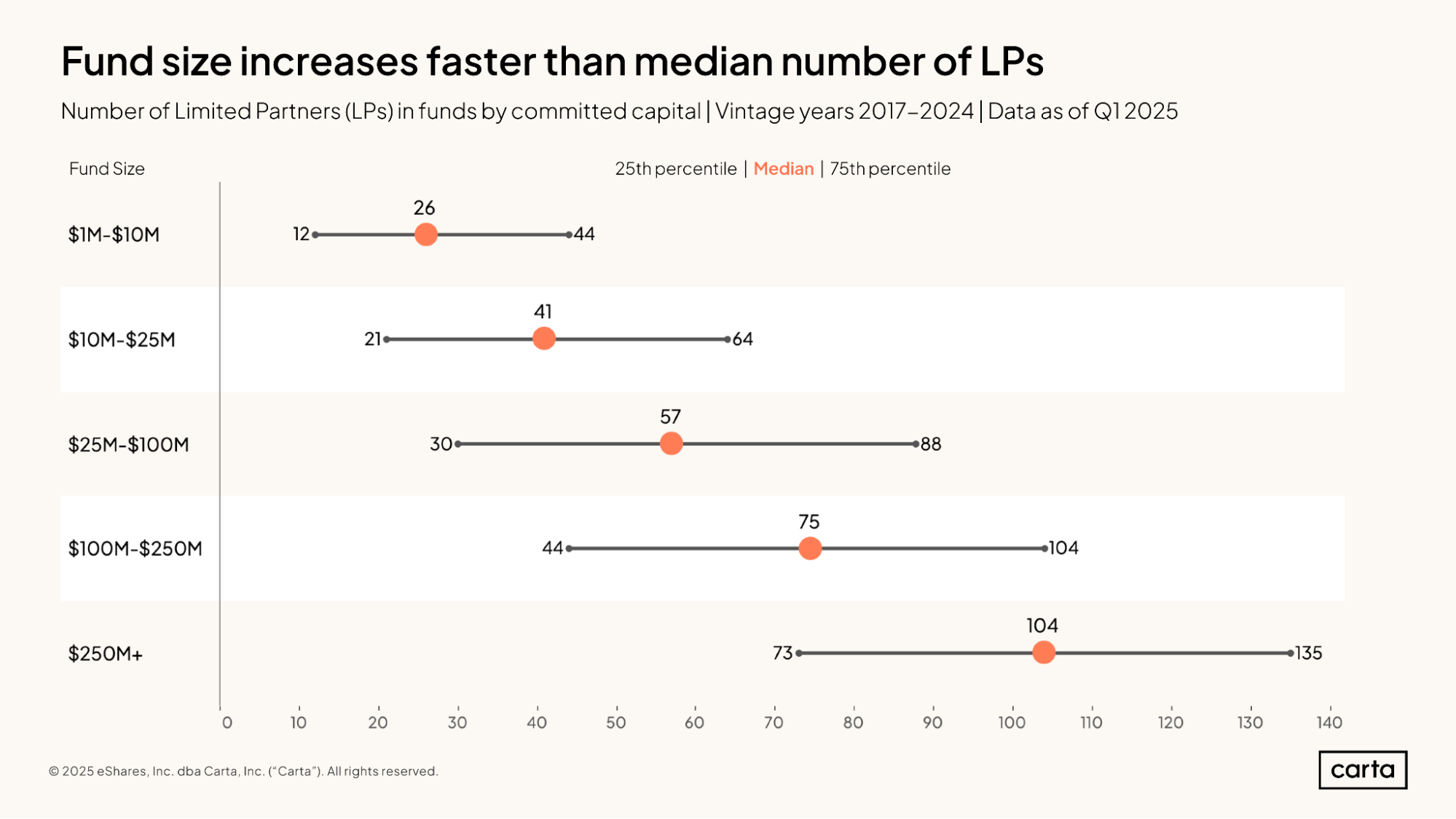

With more capital comes more LPs. Among funds between $1 million and $10 million in size, the median new fund raised between 2017 and 2024 had 26 different LPs. For funds larger than $250 million raised over that span, the median LP count was four times higher, at 104.

Funds of similar sizes can structure their LP bases in very different ways, however. The range between the 25th percentile and 75th percentile for the number of LPs can give a better idea for the norms within a cohort. For instance, half of all funds in the $1 million to $10 million cohort have somewhere between 12 and 44 LPs.

Full report available: Start reading now for free

See our complete VC Fund Performance report, including 20 additional charts and best-in-class data on fund performance.

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. ©2026 Carta. All rights reserved. Reproduction prohibited.