After the pandemic bull market came to an end in 2022, the leverage of the venture capital market tilted in favor of investors.

Along with a reset in valuations, it became more common for new VC funding rounds to include deal terms that help protect investors from downside risk or extract more upside; these include liquidation preferences, participating preferred shares, and cumulative dividends.

Read Carta's latest State of Private Markets report

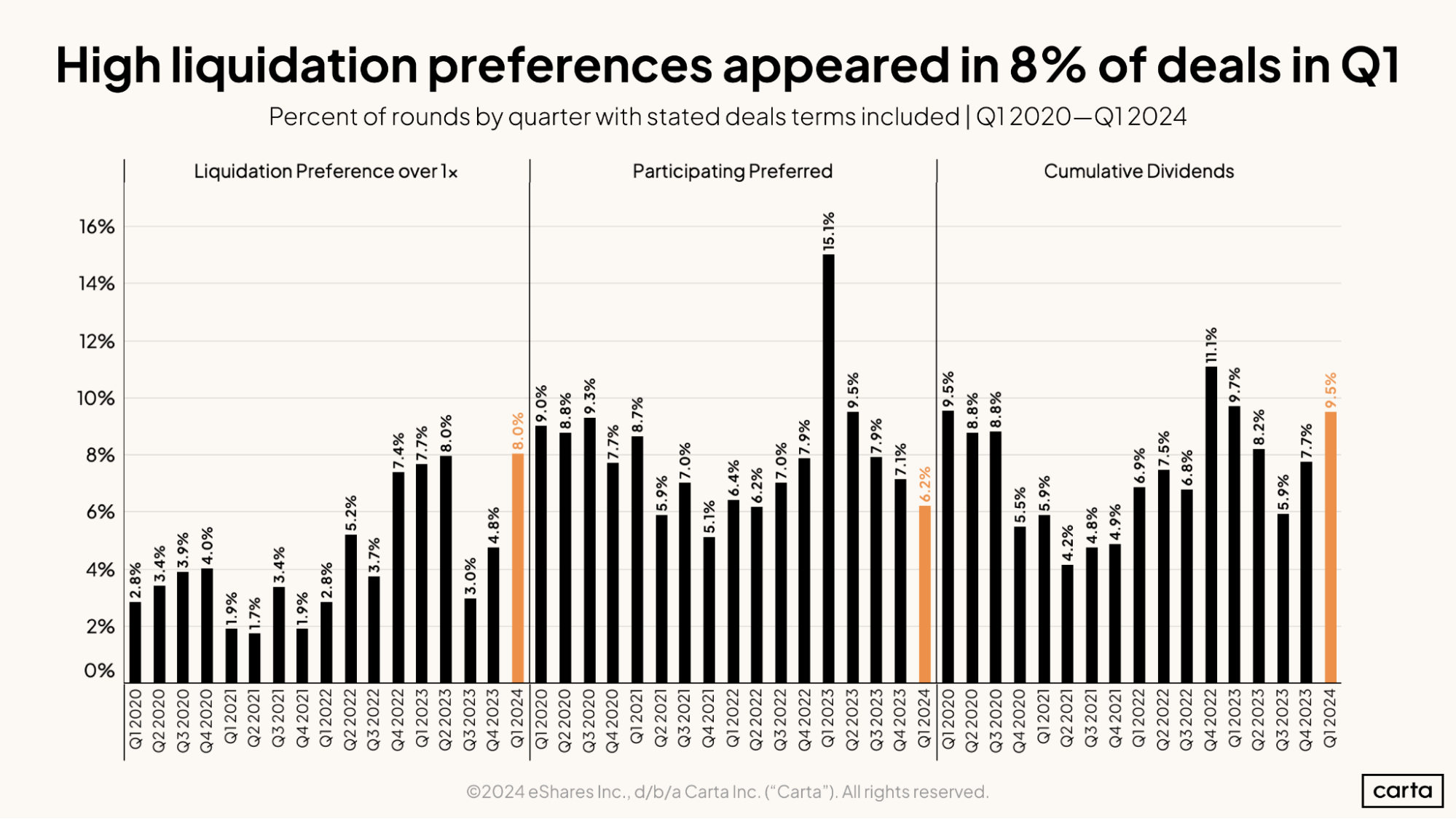

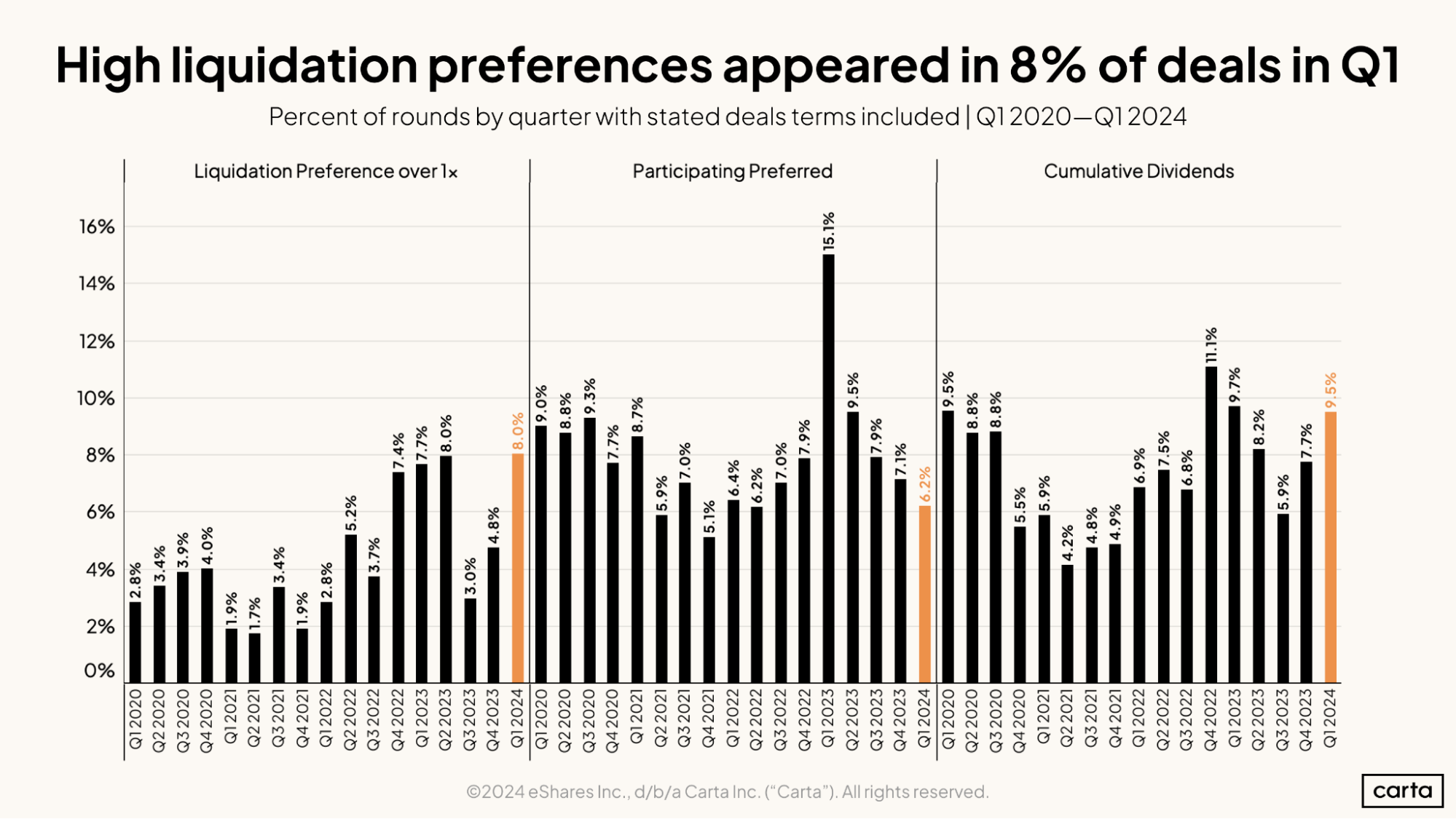

This trend continued in Q1 2024, with liquidation preferences of 1x or higher appearing in 8% of all new funding rounds on Carta—tied for the highest percentage in any quarter this decade.

The vast majority of new funding rounds still don’t include these types of structure. But for some startups—particularly those that are struggling to raise capital amid a venture downturn—they’ve become a persistent factor in deal negotiations.

In his work as a partner at the law firm Crowell & Moring, Jon O’Connell has worked on many fundraising processes in recent months.

“I’m definitely seeing more participating preferred, usually with a cap from 1.5x to 3x,” O’Connell says. “I’m seeing different types of more investor-friendly anti-dilution protection, like full ratchet. And I’m occasionally seeing some redemption rights.”

What structured deal terms mean for founders

There are many types of deal terms that an investor might demand to reduce the risk that they lose money on a VC investment, or to enhance their upside. Some of the most common examples include:

Participating preferred shares are a type of company stock that allow an investor to recoup their investment in multiple ways. If the company has an exit or other liquidation event, an investor with participating preferred shares is first in line to get their investment back. They also then get a cut of the remaining proceeds, in proportion to their ownership stake. Participating preferred shares don’t guarantee a profit: if a startup exits at a value that’s below the last post-money valuation, an investor might still net zero.

Liquidation preferences put an investor in front of the line to be paid out in the event of an exit, similar to participating preferred shares. They often guarantee that the investor will be paid out at a certain multiple on their investment. For instance, in the event of an exit, a shareholder with a 2x liquidation preference would receive twice their initial investment before common shareholders and other investors junior in liquidation preference receive any proceeds at all.

Cumulative dividends are guaranteed annual dividends that ensure a shareholder receives at least some minimum return on their investment, regardless of whether the company is profitable or is paying out a wider dividend to all shareholders. Most cumulative dividends are paid on a per-share basis.

Full ratchet is a provision that protects an investor from being diluted in the event that the company raises a subsequent down round.

Redemption rights give an investor the right to sell back their shares to the company in the future at a preset price, giving them a way to exit their investment even if the company does not achieve an exit itself. The higher the redemption price, the less risk an investor takes on.

The state of negotiations

Frances Mosley is a counsel at the law firm WilmerHale who works with startups and VCs on fundraising and a range of other corporate issues. Like O’Connell, she says the balance of power has clearly shifted in fundraising negotiations in 2023 and 2024.

“I’m seeing a lot more investor-favorable types of terms, as well as investor-favorable valuations,” she says.

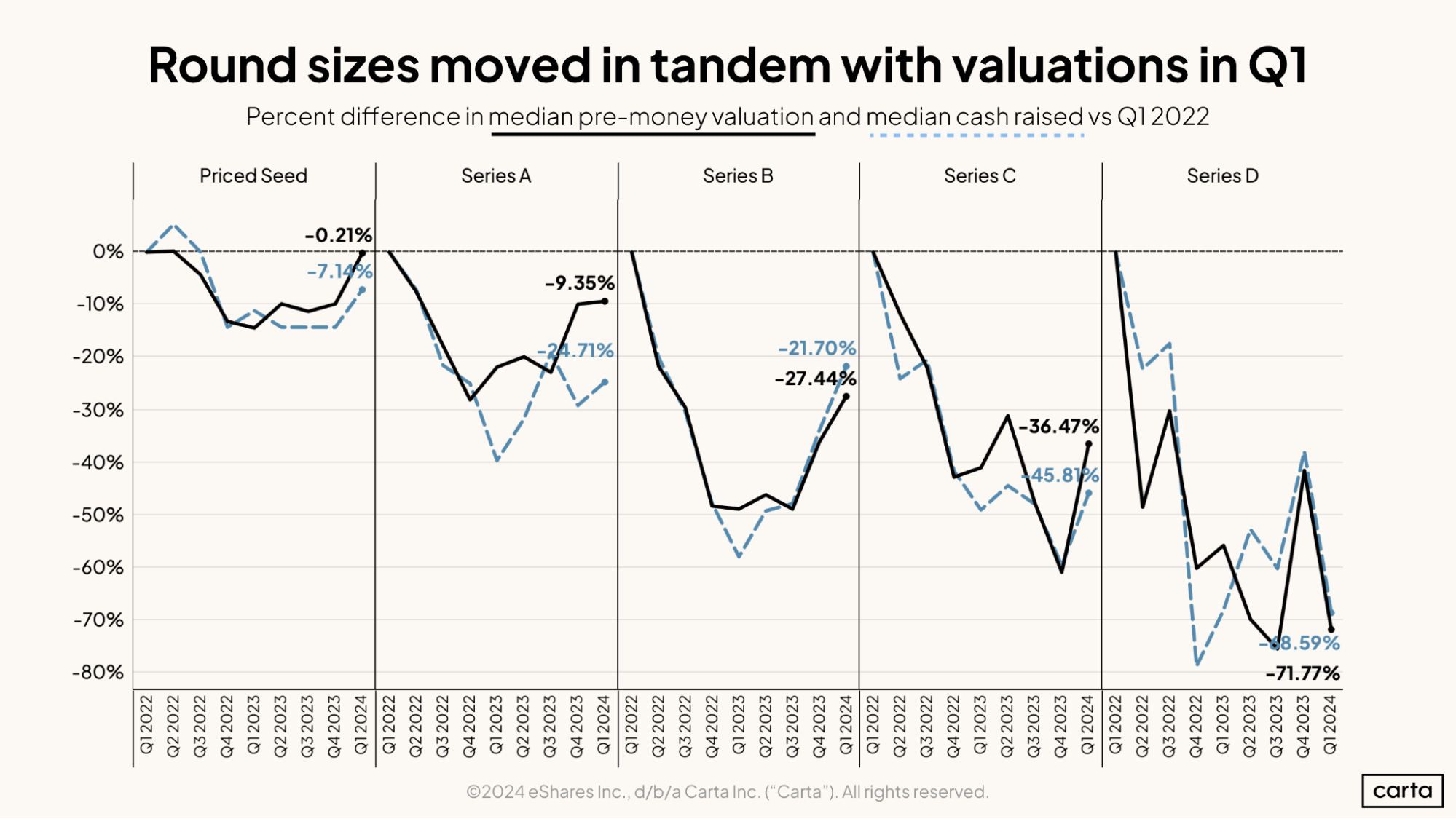

In most new funding rounds, the main ways that VCs are taking advantage of the more investor-friendly environment are by investing in companies at lower valuations and writing smaller checks. The median valuation and median deal size have both declined at every stage of the venture lifecycle since the start of 2022.

These trends are ubiquitous in the current VC landscape. But that’s not the case for other types of investor-friendly deal terms.

The deals O’Connell has seen that involve structure like participating preferred shares or redemption rights have typically fit a certain profile: Mature companies in need of new capital that are struggling to raise a new round unless they give investors a bit of extra enticement.

“Where the structure comes in is more at the later stage, maybe Series B, Series C and beyond,” O’Connell says. “And it’s kind of imposed—it is what it is if you want to raise a round. That’s different from early-stage, where you’re not really seeing that type of structure in seed and Series A deals.”

Investors are showing restraint

Even as she’s seen the market shift, Mosley says that none of the companies she works with have raised rounds this year that include participating preferred shares or liquidation preferences higher than 1x. That’s a testament to the fact that, even though these types of terms have grown more common, they’re still quite rare.

But the possibility of a VC seeking such friendly terms is always in the back of her mind.

“Every time I get a term sheet, I’m waiting for it,” Mosley says. “Are they going to ask for 2x, or for participating preferred?”

If VCs have the leverage in fundraising negotiations in 2024, why aren’t more of them asking for structure? For Mosley, there’s a clear answer: Investors and their companies are on the same team.

If a VC gets participating preferred shares or a big liquidation preference, it could hamstring the company down the line, complicating the cap table and making it more difficult to bring on investors. These types of terms can also limit the returns to common shareholders, such as employees, which can make equity-based compensation less attractive.

Most investors want to avoid such problems. They want their portfolio companies to be as healthy and well-positioned as possible to grow fast and go after the big exit that all VCs desire.

These types of structure in a funding deal might protect investors against downside risk. But they can also limit upside potential.

“I get the impression that investors understand the ball’s in their court at this moment,” Mosley says. “And a lot of them are looking long term, and they’re thinking, ‘What’s good for the company is good for us.’ So I think they’re trying to balance that out and make sure they’re not gouging companies on terms.”

Get the latest data

For the latest data on venture capital fundraising, startup hiring, compensation benchmarks, and more, sign up the Carta Data Minute:

DISCLOSURE: This communication is on behalf of eShares Inc., d/b/a Carta Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. All product names, logos, and brands are property of their respective owners in the U.S. and other countries, and are used for identification purposes only. Use of these names, logos, and brands does not imply affiliation or endorsement.©2024 eShares, Inc. dba Carta, Inc. ("Carta"). All rights reserved. Reproduction prohibited.