It can require a lot of capital to operate a late-stage startup—often tens or even hundreds of millions of dollars each year.

So far in 2024, raising that capital from VCs has been a challenging proposition.

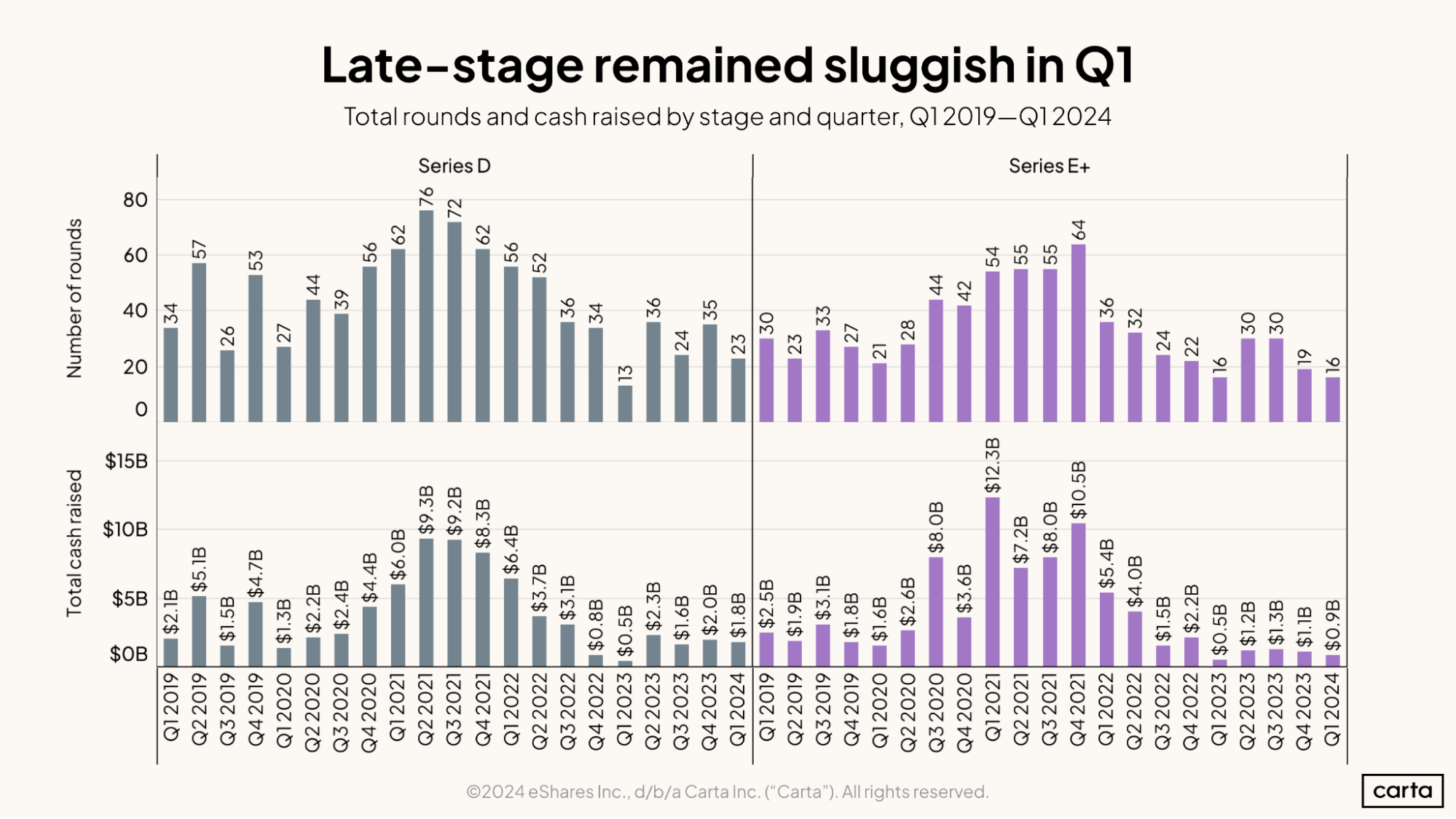

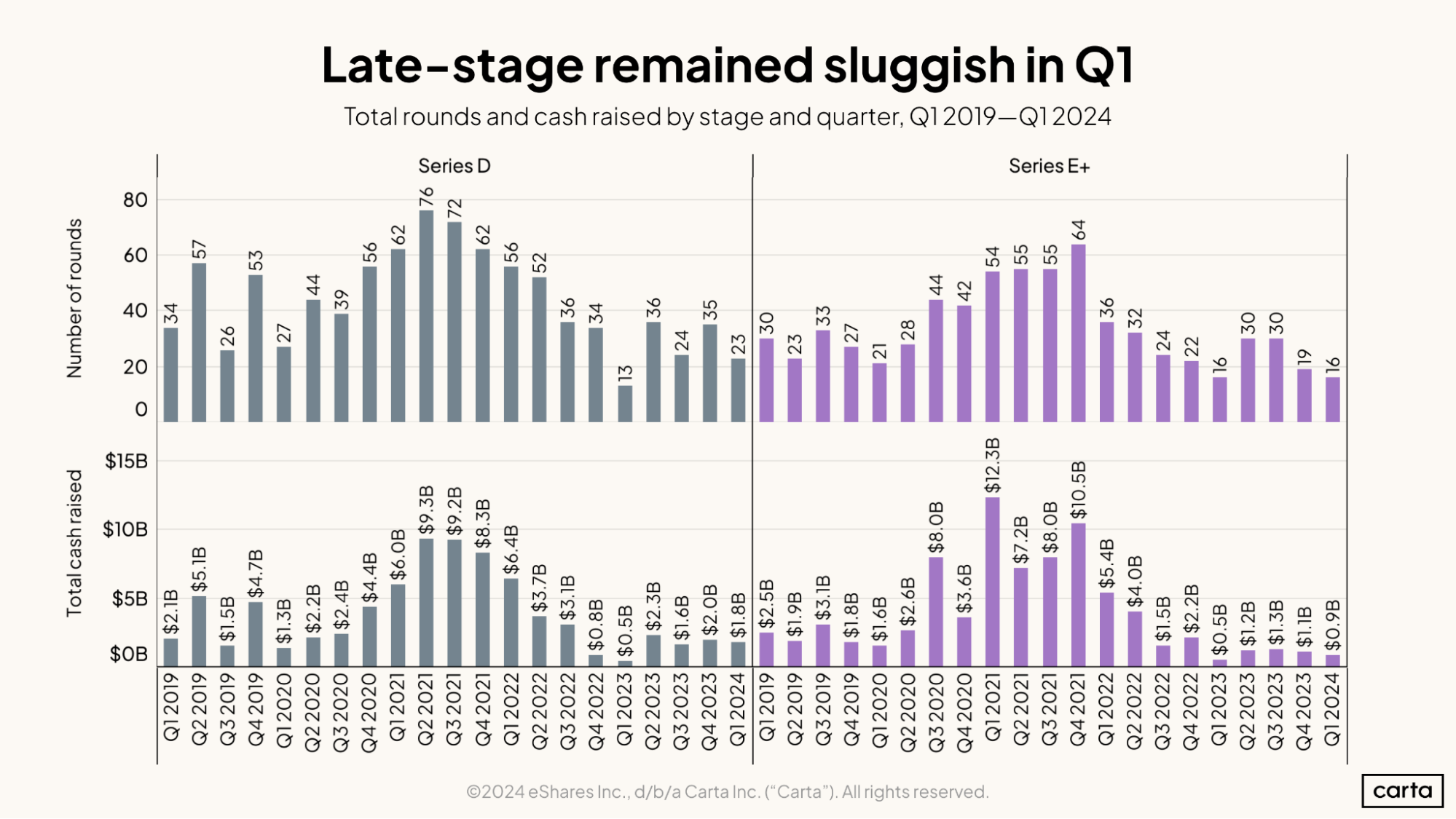

Get the latest dataIn Q1, companies on Carta closed just 23 Series D rounds, plus another 16 rounds at Series E or later. This combined 39 venture fundings at Series D and beyond is the second-lowest quarterly total since the start of 2019, ahead of only Q1 2023.

Late-stage deal activity slumped significantly during 2022, serving as a leading indicator that the bull market of 2021 was coming to an end and an industry-wide venture slowdown had begun. It briefly looked like a late-stage recovery might be underway in mid-2023, when deal count at Series E and beyond hit 30 for two consecutive quarters. Instead, the slump has continued.

“Late-stage rounds are pretty big,” says Jon O’Connell, a partner at the law firm Crowell & Moring who specializes in VC fundraisings. “They require a significant amount of capital. And that’s a lot harder to obtain for companies that have been affected by a slowdown.”

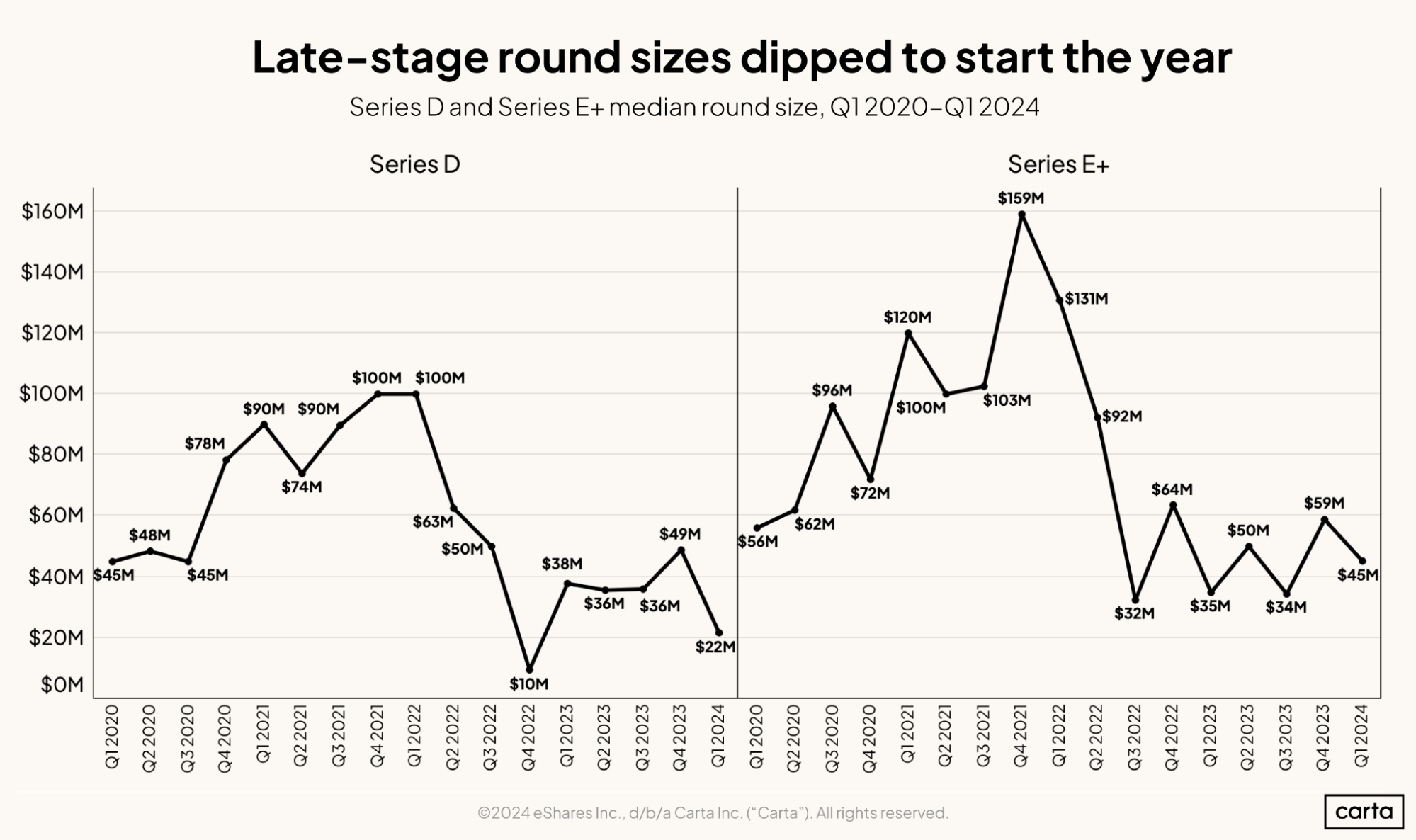

A decline in deal size

Late-stage funding rounds certainly do require “a significant amount of capital.” But not quite as significant an amount as they used to.

The median Series D round size in Q1 fell to $22 million, a big drop from a median of $49 million in Q4 2023. At Series E+, meanwhile, the median round size was $45 million in Q1, compared to $59 million the prior quarter.

These are still larger round sizes than you’ll find at any other stage. But they’ve fallen off sharply in the past couple of years. Compared to Q4 2021—perhaps the peak of the late-stage market’s recent boom—median Series D round size has declined by 78%, and median Series E+ round size has fallen by 72%.

The role of IPOs

One reason that the late-stage market has slowed down: The IPO market has slowed down, too.

When fundraising activity surged at Series D and Series E+ in late 2020 and throughout 2021, it happened alongside a concurrent increase in IPOs. Late-stage private companies were flocking to the public markets and generating attractive returns for their investors—in some cases, only a few months after the initial investment. Other investors took note and pumped more capital into other late-stage companies in hopes of creating similarly swift returns themselves.

Lately, however, turning a quick profit through an IPO has proven more rare, because IPOs have become fewer and farther between. In 2023, just 108 companies raised $50 million or more in IPOs on U.S. exchanges, compared to 397 companies in 2021.

The lack of IPOs can make late-stage investing less appealing. It also means that some late-stage investors are squeezed for cash. If a VC’s existing investments aren’t returning capital, then they have less money to deploy in new deals.

“A lot of late-stage investing is based on the idea of a relatively short timeline to liquidity,” says Adam Nash, a longtime angel investor and tech executive who’s now the CEO at Daffy, a fintech startup focused on charitable giving. “Normally, if a late-stage firm assumes an investment might be liquid in three years, it actually makes a big difference in the numbers if that turns out to be five years instead of three.”

The role of lower valuations

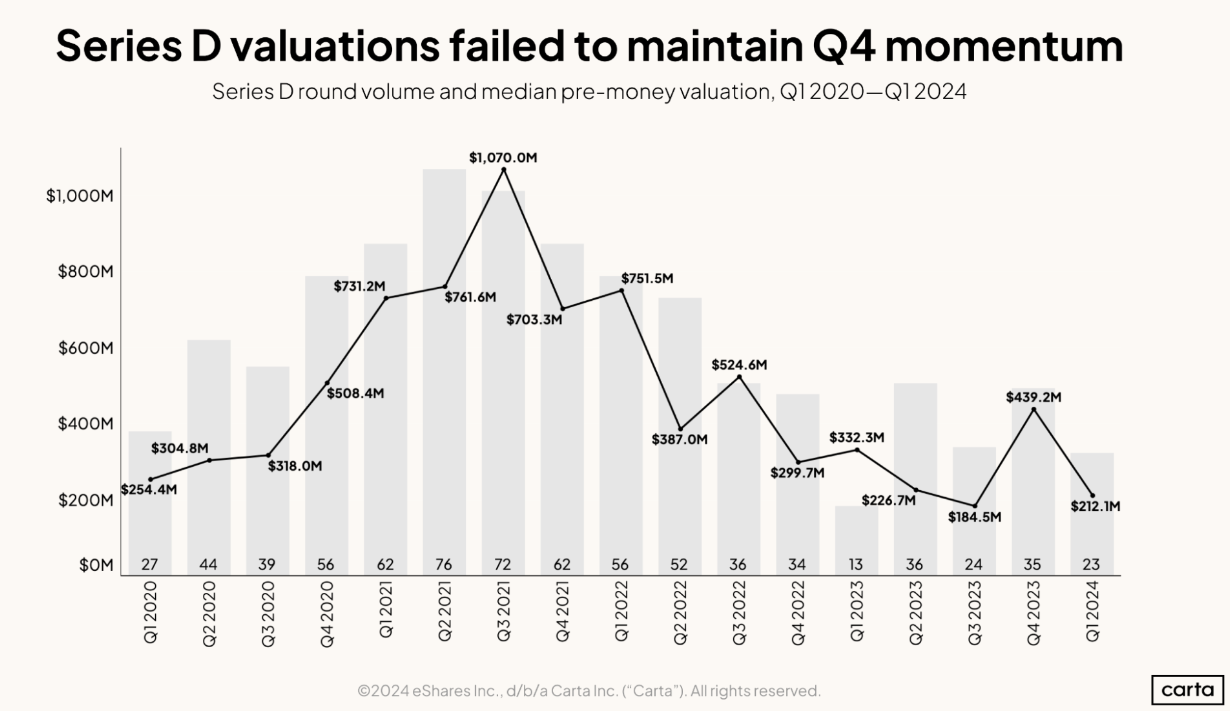

As with late-stage deal counts, late-stage valuations have fallen off since the 2021 bull market. At Series D, the median valuation on Carta sank to $212.1 million in Q1 2024, down from a high of $1.07 billion in Q3 2021.

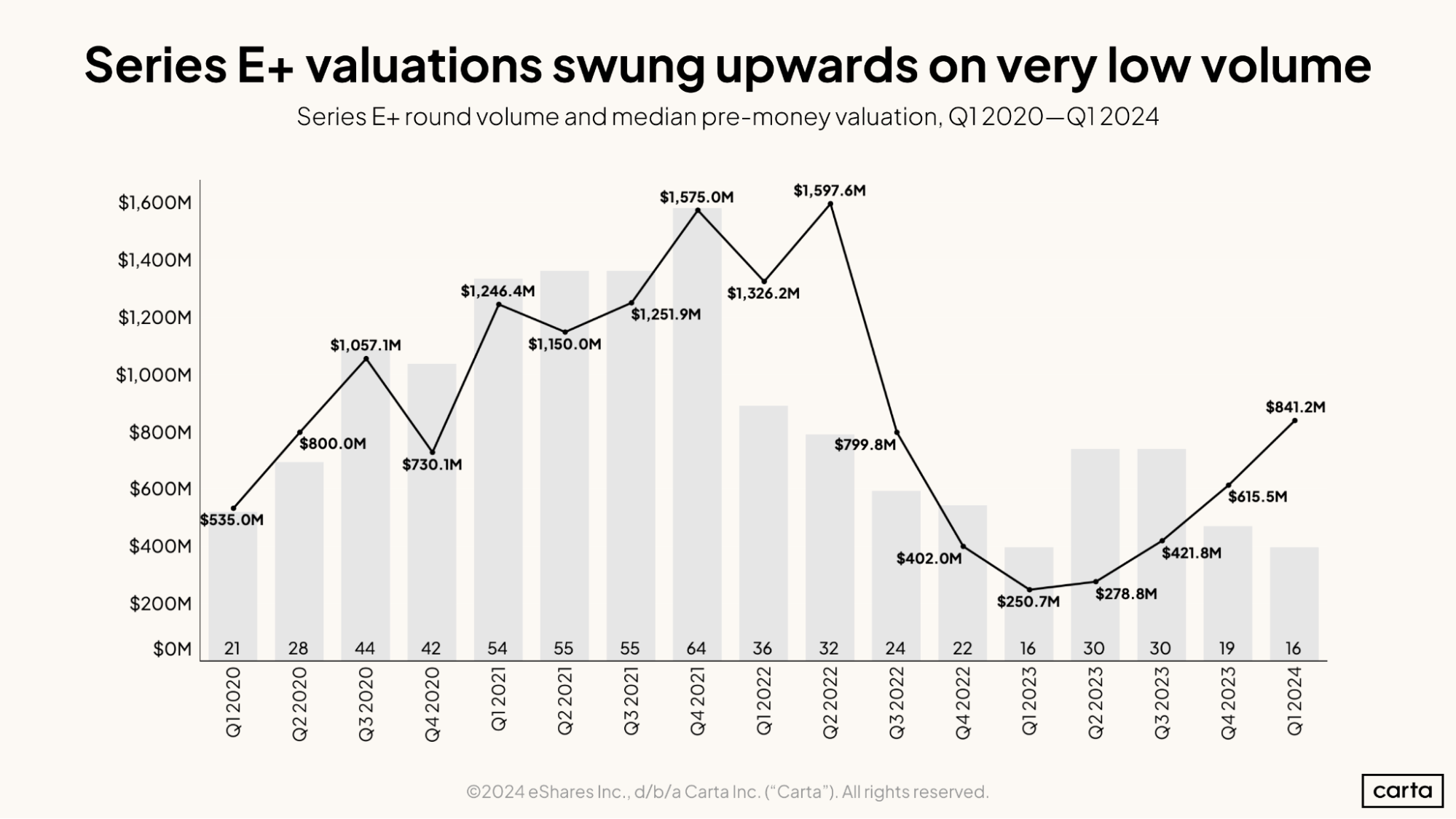

Later stages are faring a little better. The median valuation in rounds at Series E+ rose to $841.2 million in Q1. That’s good for a 236% year-over-year increase, but it’s still well off the recent high of nearly $1.6 billion in Q2 2022.

In some ways, this reduction in late-stage valuations over the past two years is complementary to the reduction in late-stage deal count. Both trends are signs that VCs have grown less bullish about the market. When investors grow more selective, their universe of investment-grade companies shrinks, leading to fewer deals. And when competition for deals is less intense, VCs have more leverage in negotiations, which can drive down valuations.

But there can also be a cyclical effect, with lower valuations further driving down deal count. Some companies are wary about raising a new primary round in this environment because they’re concerned about the potential long-term impacts of a down round. If a company’s coffers are well stocked, leadership might choose to wait on raising new capital and use up some of its runway instead.

Other companies are opting to raise bridge rounds or other types of extensions to stay afloat without a new priced round. In Q1, about 26% of all new rounds raised by Series D companies on Carta were bridge rounds, up from 20% the previous quarter. That aligns with what O’Connell has seen in his work with companies on the fundraising trail.

“I’m seeing a lot more bridge rounds and other bridge-type deals going on that are insider-led transactions,” O’Connell says. Still, bridge rounds at the latest stages have spiked less than they have in the early-stage market.

New market realities

This current cocktail of fewer deals, smaller deal sizes, and lower valuations might be hard to swallow for companies currently trying to raise a late-stage round.

The VC landscape looks very different from the last time many of these companies were on the fundraising trail.

“In that long, pre-pandemic bull market, there were high late-stage valuations, low sensitivity to core economics, and an almost perverse attraction to businesses that required a lot of capital,” Nash says. “The companies that were built on an assumption that they could snap their figures and raise the next round within six to 12 months—that is a big problem.”

Get the latest data

For weekly insights into Carta's unparalleled data on the private markets, sign up for Carta’s Data Minute weekly newsletter: