Over the past five years, a subtle but unmistakable shift has emerged in the makeup of startup term sheets.

At every stage of startup life, the median level of dilution in new funding rounds is declining. Put in plain terms, this means that companies raising new funding have been selling off a smaller portion of their stock to venture capital investors, which can improve a startup’s financial upside and operational flexibility moving forward.

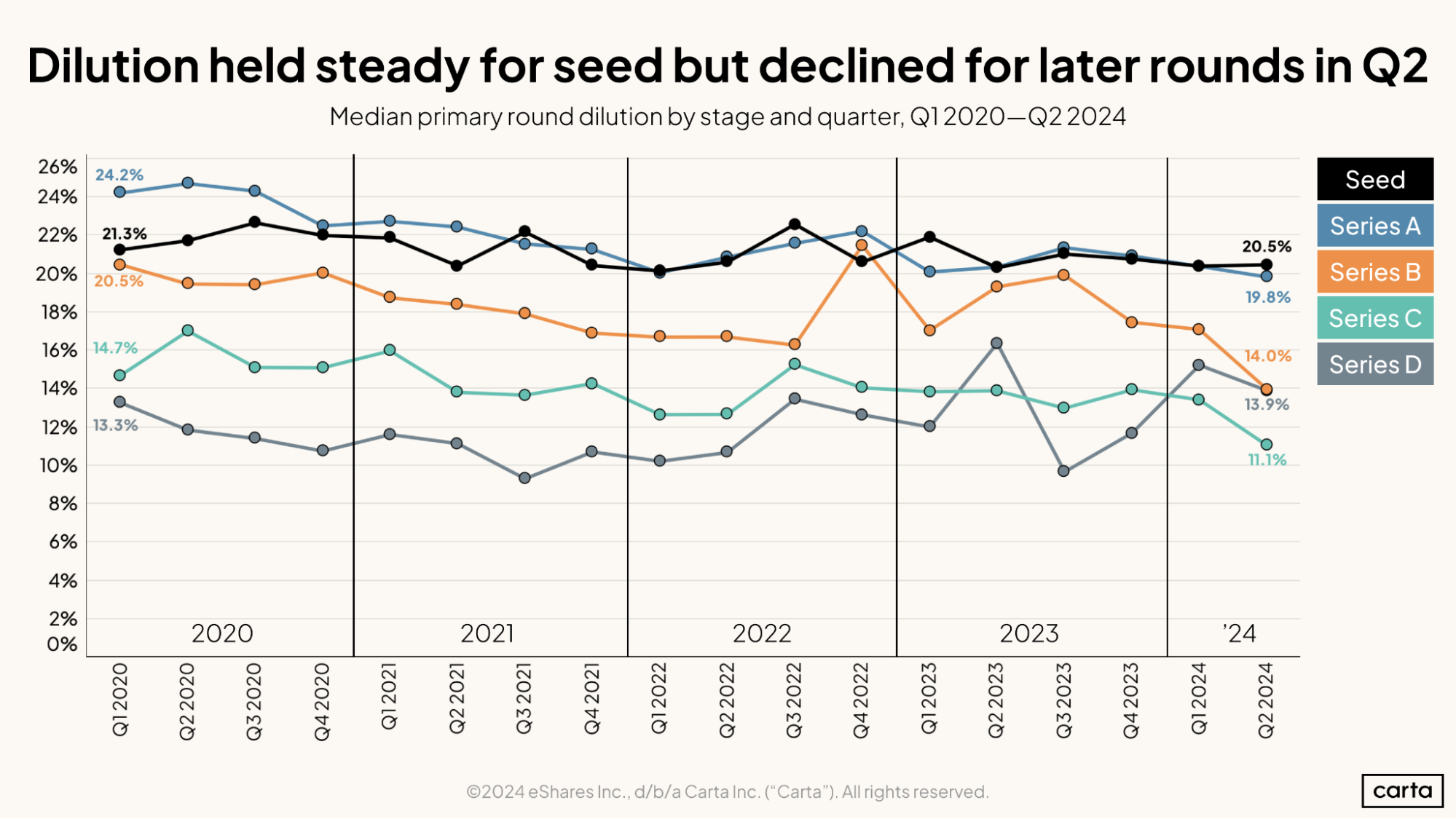

Here’s the latest data on how median dilution—defined as the round size in a primary funding event divided by the pre-money valuation—has evolved at every stage from seed to Series D:

As you can see, from one quarter to the next, median dilution might go up or down at any one stage. But across the past four and a half years, and across all stages, the long-term trend is unmistakable.

This shift in dilution is also the sort of trend that can only emerge in the big picture. Alex Civetta, an associate at Mintz who frequently works on venture financings, says he hasn’t noticed a material change in dilution in his own work. But he knows that, when it comes to analyzing a global market, personal experience has its limits.

“I’m not sure any individual practitioner has a high enough volume across enough industries to be able to say, ‘Yeah, I’ve noticed a subtle decline in the way dilution works,’” Civetta says. “But that doesn’t mean it’s not there.”

Why is dilution changing?

Many long-term statistical trends in VC funding have clear explanations. This one does not.

Lower dilution levels are traditionally seen as a sign of an company-friendly fundraising environment; when the market’s hot, the thinking goes, companies can use their leverage to raise capital at higher valuations, driving down dilution. But this trend in declining dilution has persisted through a roller-coaster ride of VC market conditions, from the steady growth of the late 2010s through the bull-market years of the early 2020s all the way to the ongoing venture slowdown that began in 2022.

What other variables are at play? VC dealmakers point to several factors that may be helping drive funding dilution levels to new depths.

1. Smaller checks, smaller numerators

Because dilution is measured by dividing one number over another, there are two ways for dilution levels to decline. One is for the valuation—the denominator in the equation—to get bigger. The other is for the round size—the numerator—to shrink.

During the early 2020s, both round sizes and valuations were generally increasing, but valuations were increasing at a faster rate. Thus, dilution levels decreased. Since the venture market turned in mid-2022, both round sizes and valuations have generally decreased, but round sizes decreased at a faster rate. The mathematical outcome is the same.

“Companies are raising smaller rounds, and that will result in less dilution,” says Kamran Ansari, a venture partner at Headline Ventures.

In some cases, these recent decreases in round size are the result of investor pessimism. With valuations trending down, investors aren’t as eager to put capital to work as they used to be. In other cases, raising smaller rounds is a strategic choice: Many companies have prioritized efficiency over growth in the current environment, which can reduce their need for capital.

In still other cases, investors are putting capital to work at earlier points in a company’s development. And these younger companies sometimes require smaller investments. Abby Miller Levy, managing partner and co-founder at Primetime Partners, says that many of the startups raising seed or Series A rounds today have less revenue than companies raising rounds at those stages in the past.

“Investors are ready to put money to work, and they’re doing that at less traction than they were a decade ago,” Miller Levy says.

2. A different kind of dilution

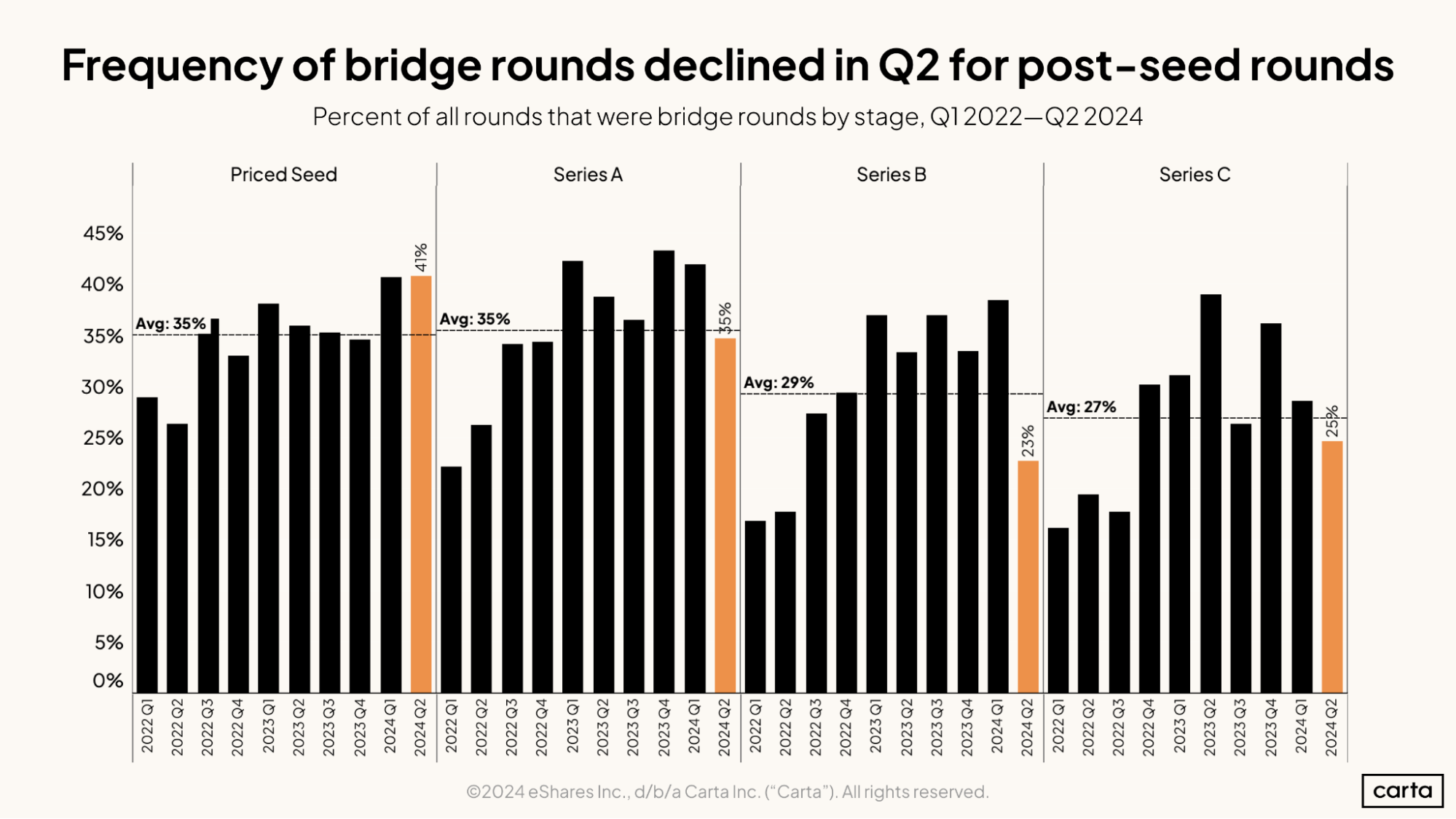

While some startups are raising smaller primary rounds, others are forgoing primary rounds entirely and raising bridge rounds, instead. This shift in the type of rounds startups are raising could be another reason why dilution is declining.

Bridge rounds can come in many different forms. Ansari says he’s seen a particular rise in the frequency of convertible notes, a type of debt instrument issued to investors that can convert into equity at a later date.

“You’re seeing a lot of convertible notes at Series A, B, and C, which was not really that common three or four years ago,” Ansari says.

At every stage from seed to Series C, the percentage of all new rounds taking place that are bridge rounds has climbed to historically high levels in recent years. In Q2, however, the rate of bridge rounds (as compared to new primary rounds) dipped significantly at three of those four stages.

In a roundabout way, the recent uptick of bridge rounds could be contributing to a decline in dilution levels among the population of companies raising primary rounds.

Those startups that are most attractive to venture capitalists will be able to raise funding in any environment, and at attractive terms. When the funding market tightens, as it has in the past two years, companies that are for whatever reason less appealing to VCs are more likely to feel the squeeze.

In the recent past, this might mean that these sort of mid-tier startups had to accept higher dilution in order to raise capital. In more recent quarters, many of these startups were unable to raise primary rounds on any terms and shifted to bridge rounds, instead.

This changes the nature of the data. When these aforementioned mid-tier startups move from raising primary rounds to bridge rounds, it removes some of the highest-dilution rounds from the dataset of primary rounds. And when that happens, median dilution levels will by definition decline.

While these bridge rounds don’t factor into our dataset on dilution in primary fundings, they are still dilutive events. Convertible notes, for instance, can cause dilution down the line when they eventually convert into equity.

“At some point, you have to pay the piper,” Ansari says. “If you have convertible notes stacking up, then those are going to convert into equity at some point. And if that next equity round isn’t at a significant valuation increase, there’s a dilution tsunami coming.”

3. Imbalanced incentives

Dilution is a consideration for parties on both sides of the table when negotiating a new venture fundraising. But in Civetta’s experience, it’s typically a bigger priority for founders than it is for VCs.

Most VCs invest in tens or even hundreds of startups. But founders only have one company. In many cases, it’s a company they’ve dedicated years of their lives to building. It makes sense that many founders are willing to scratch and claw to retain as much of their company as they can.

“From my perspective, the dilution metric is a more personal and immediate concern to founders than it is to an investor,” he says.

Civetta also notes that the growing availability of fundraising data makes it easier for founders to decide what terms to ask for. Instead of relying on the standard industry benchmark of somewhere around 20% dilution per round, founders are now able to see much more clearly what their peers in the market are doing.

A founder who’s concerned with controlling dilution might try to limit the dilution in their own fundraising round to below the industry average. When enough of these founders succeed, average dilution will decline.

“The availability of the data can start to affect the data itself over the course of time,” Civetta says. “It’s kind of cool now to have access to all this information and be able to look back.”

Get the latest data

Sign up for the Carta Data Minute newsletter to receive the latest data on VC financings, valuations, compensation, and more:

DISCLOSURE: This communication is on behalf of eShares Inc., d/b/a Carta Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. ©2024 eShares, Inc. dba Carta, Inc. ("Carta"). All rights reserved. Reproduction prohibited.