Since the Traitorous Eight left Shockley Labs to start Fairchild Semiconductor in 1957, the concept of equity—of owning a piece of the company where you work—has become ubiquitous.

Today, startups don’t even question whether they should give their employees options.

That doesn’t mean there isn’t work to be done improving how those options work. As Hunter Walk recently pointed out, the most talented hires generally deserve to get more equity.

Then there’s accessibility. Robert Noyce called owning shares a “great revelation and a great motivation,” but harnessing that power relies on employees having the ability to actually exercise their options. In too many cases, they don’t.

Fortunately, that’s changing.

According to our data:

More companies are adopting longer PTE windows, letting their employees exercise outside the traditional 90-day post-termination windows.

Employees are exercising more when they can exercise early, increasing their potential upside while avoiding a potentially punitive tax bill at the end of it.

Employees are exercising more of their vested shares, with changes to the Alternative Minimum Tax (AMT) a crucial financial factor.

Stock options are getting more employee-friendly

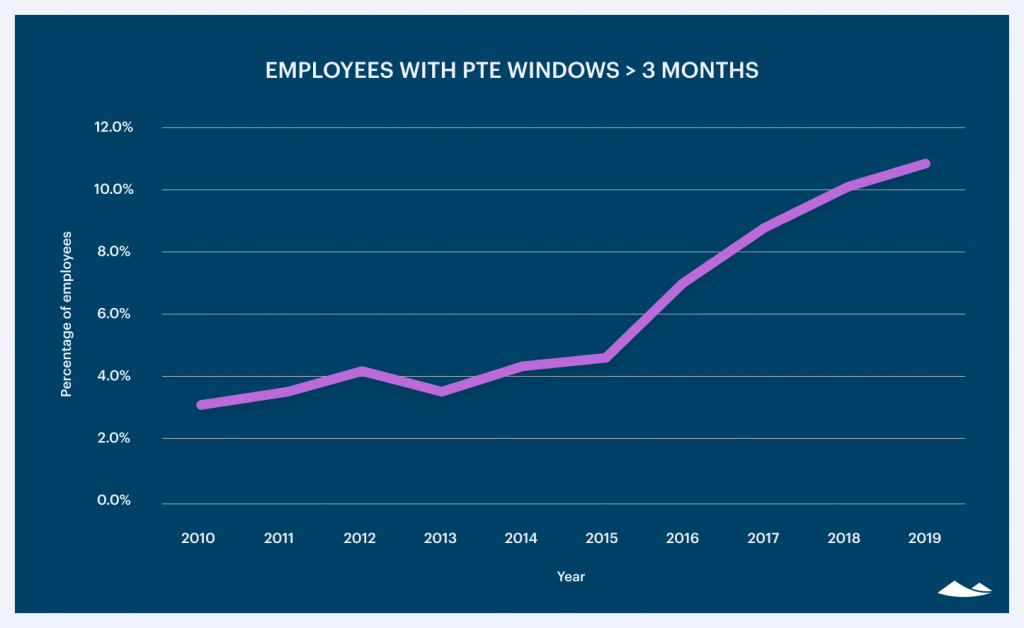

The traditional PTE window has been painfully short for many employees. While a 90-day PTE window is standard, some companies give their employees just 30 days to exercise their options after leaving.

The problem with short PTE windows is that employees who leave before their company gets sold or goes public—no matter how long they were at the company—suddenly have just 30 or 90 days to come up with the thousands of dollars they need to cover the price of exercising their options (and to address tax impact for that year).

What we’ve seen over the last decade, however, is amore than 3x jump in the percentage of employees receiving PTE windows longer than 90 days.*

With more startups staying private longer, it’s safe to say the “golden handcuff” problem isn’t going anywhere.

Companies have been pushing back against punitively short PTE windows for some time. Buffer, Carta, Coinbase, Mixpanel, and Pinterest are just some of the companies that have extended their PTE windows, making it easier for all of their employees to exercise their options—not just those who can most easily afford to do so.

In the future, expect to see more companies following suit.

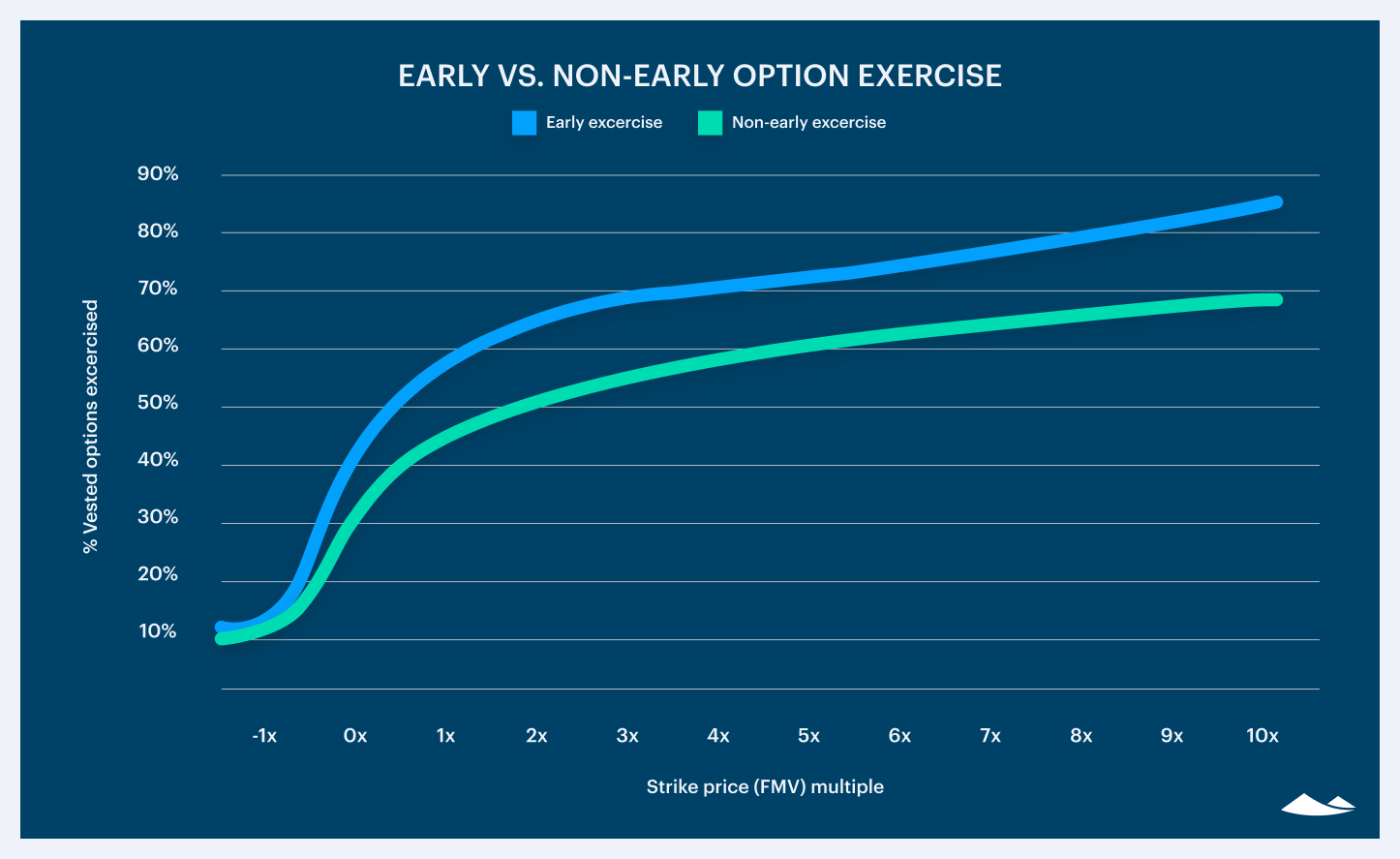

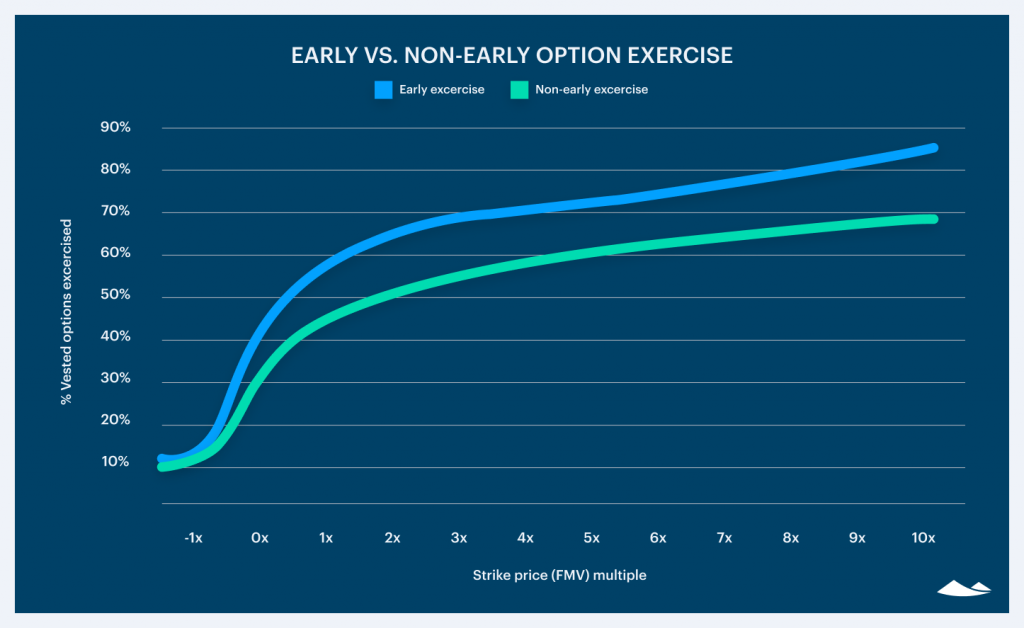

Employees are exercising even more when they can exercise early

While grants with extended PTE have gone up, the proportion of early exercise has stayed consistent over the last few years. The percentage of options on Carta that can be early exercised has remained unchanged at about 15% since 2010.

Early exercise offers employees the ability to own their vested shares sooner than they otherwise would, giving them more flexibility in their careers. With early exercise, employees can avoid more punitive aspects of the tax code (like AMT) and start the clock on long-term capital gain tax treatment earlier.

Early exercise has risks. But if an employee believes strongly that their options will be worthwhile and they have the financial ability to pay for those shares, early exercise can be a powerful mechanism to reduce AMT and take advantage of qualified exemptions.

Unsurprisingly, our data shows that employees tend to exercise more of their options when they’re given the option to exercise early.

Employee exercises are up

Unless an employer offers longer PTE, or the employee took advantage of early exercising, leaving a startup, especially a successful one, can be costly.

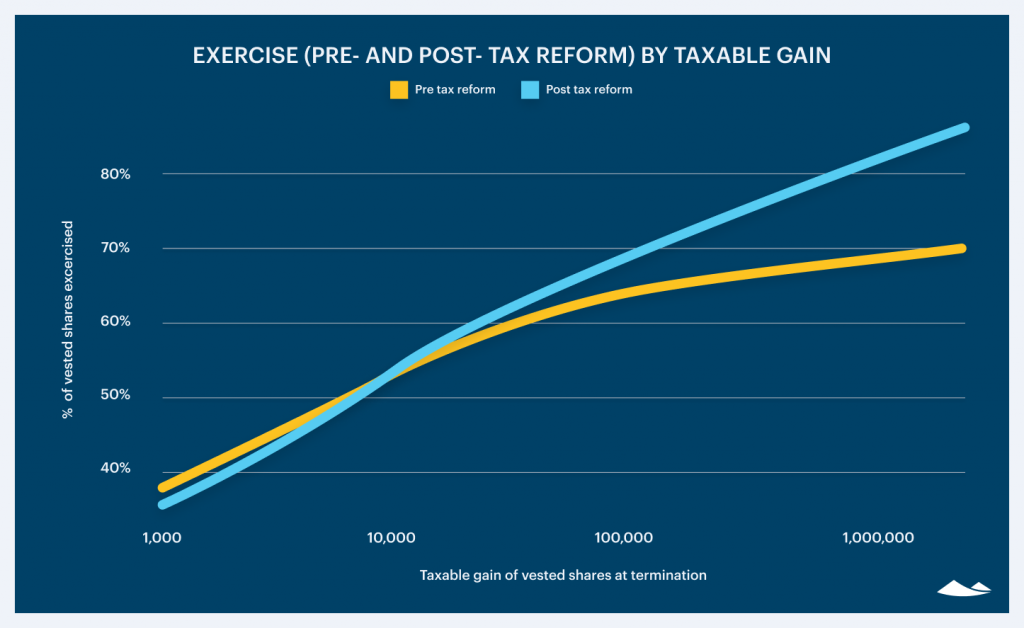

AMT has disproportionately affected startup employees because there isn’t a liquid market for private market stock. Depending on the taxable income of an employee, the spread between the strike price and FMV at exercise could be taxed between 26-28%—leaving that employee with a hefty tax bill whether or not they have any way of cashing in on their options.

In 2017, Congress passed the Tax Cuts and Jobs Act which increased the total exemption and the phaseout threshold for AMT. In short, employees could exercise more options and avoid a large AMT bill.

Our data on employee exercising post-termination and those with higher-valued options has taught us that*:

Employees with options worth about $100,000 are exercising 67% of vested shares compared to 62% pre-tax reforms.

Employees with options worth $1M are exercising 79% of vested shares compared to 67% pre-tax reforms.

This chart shows the exercise percentage of vested options by taxable gain upon termination.*

It’s hard to say for certain how much the AMT change directly affected exercise behavior. There are lots of macro factors that could play a role, including a stronger economy in general encouraging more people to exercise their options.

Still, the data we have suggests there are several ways founders and companies could help more employees exercise and keep money from being left on the table, including things like longer PTE windows, offering the ability to exercise and sell to cover, tender offers, and making early exercise available to all.

The future of employee options

The data we’ve looked at on employee exercise behavior is encouraging, but shows that there’s still considerable work to be done.

We believe employees should see the upside of the companies they work for. Longer PTE windows mean that people stay with companies because they want to, not because they have to.

We believe private companies should give their employees a share in what they’re building. Companies should make it easier for employees to exercise their options, not exclude them by making it more difficult.

We believe that equity is one of the most effective vehicles for startup founders to create and sustain inclusive cultures of equality, fairness, and transparency.

Although there is still clearly a long way to go in making equity more equitable, important, necessary conversations about employee equity are taking place and attitudes are changing––albeit slowly. We see a rising tide where founders are becoming more sensitive to the need to not just offer competitive options grants, but equity plans that make exercising more convenient, fair, and rewarding.

* This study uses a sample of Carta’s founder and employee cap table data, aggregated and anonymized. Companies who have contractually requested that we not use their data in anonymized and aggregated studies are not included in this analysis.

DISCLOSURE: This communication is being sent on behalf of eShares, Inc. dba Carta, Inc. (“Carta”). This communication is not to be construed as legal, financial or tax advice and is for informational purposes only. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. This post contains links to articles or other information that may be contained on third-party websites. The inclusion of any hyperlink is not and does not imply any endorsement, approval, investigation, or verification by Carta, and Carta does not endorse or accept responsibility for the content, or the use, of such third-party websites. Carta assumes no liability for any inaccuracies, errors or omissions in or from any data or other information provided on such third-party websites. All product names, logos, and brands are property of their respective owners in the U.S. and other countries, and are used for identification purposes only. Use of these names, logos, and brands does not imply affiliation or endorsement.