For the third year in a row, the venture capital industry got a little less crowded in 2024.

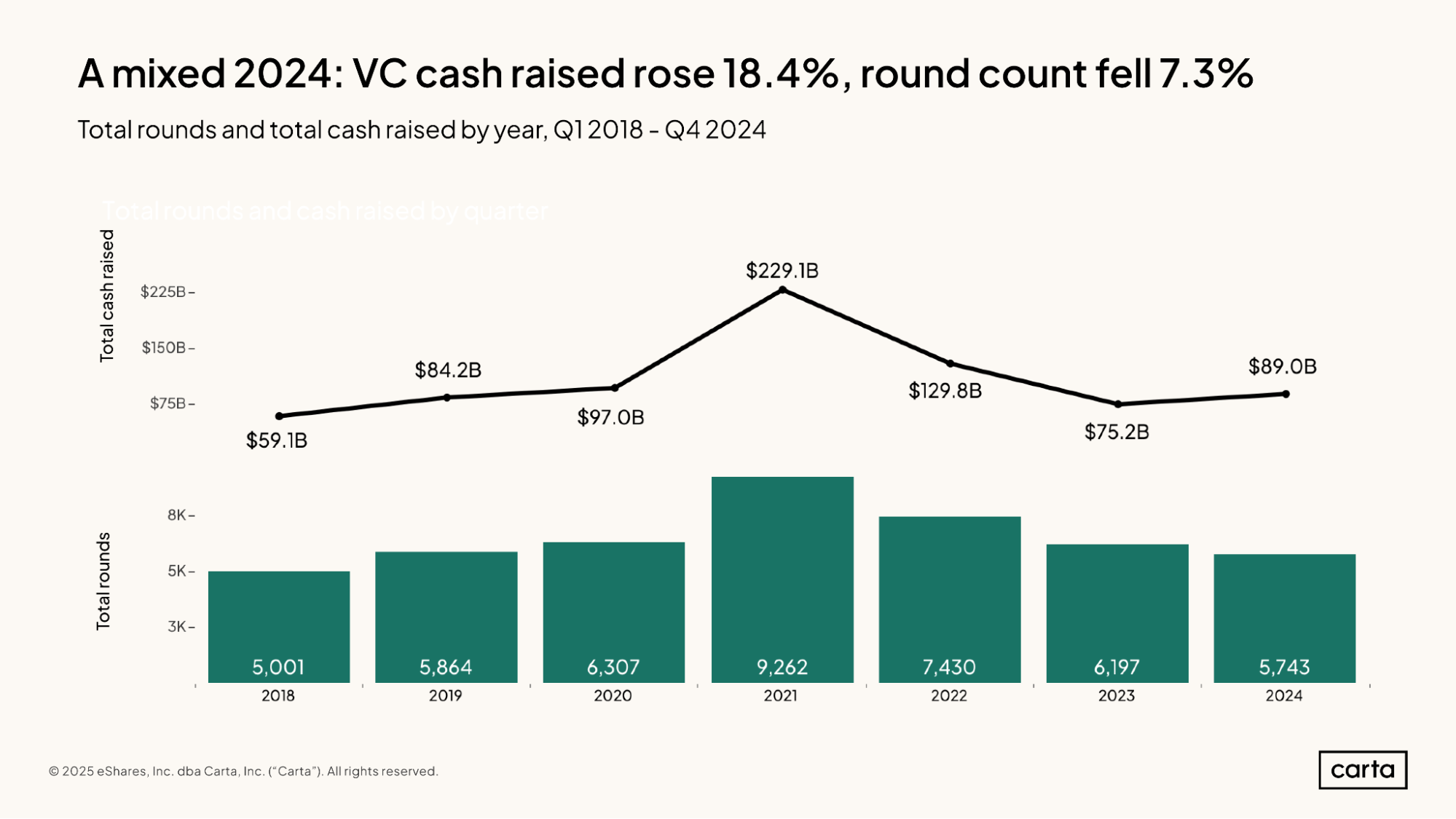

Startups on Carta closed 5,743 new investments during 2024, marking a 7% decline from the year before. It was the lowest annual total of new VC fundings since 2018.

On the other side of the table, there was a 46% annual decline last year in the number of new venture funds raised in the U.S. From 2021 to 2024, the number of new funds fell by 68%. As fewer new funds close, fewer firms are writing checks. Over the past three years, the annual count of investors who made at least one new investment in a U.S.-based startup declined by 26%.

Venture investors and venture-backed founders are two distinct groups, but they’re facing a similar conundrum: Raising capital isn’t as simple as it used to be.

“We’ve been very fortunate that we are still deploying capital, and still have capital to deploy over the next year before we raise our next fund,” says Rachel Springate, founding partner at Muse Capital, an early-stage fund that invests in women's health, gaming, and a range of other consumer tech solutions. “But there is less money, fewer people writing checks—certainly in our space, where there’s a lack of funding anyway.”

Capital grows more concentrated

For VC investors like Springate, the change has been stark: Total cash raised from LPs by U.S. venture funds fell 22% in 2024 and is down nearly 60% from two years ago.

For startups, however, cash remains relatively plentiful. In fact, as the number of VC deals on Carta declined year over year in 2024, total cash raised leaped by more than 18%.

Instead of a lack of cash, for companies, it’s a question of concentration. Available capital is being divided up among fewer and fewer hands. At the startup level, this is demonstrated by an increase in check sizes: Across all stages, the average venture round size was $15.5 million in 2024, up 28% from a $12.1 million average in 2023.

At the same time, the balance of deal activity shifted toward later stages. While the number of new investments declined in 2024 at both the seed stage and Series A, deal counts ticked up at Series B, Series C, and Series D. These numbers seem to indicate that investors grew a bit less likely last year to make new bets on emerging startups and more likely to do deals involving larger, more mature companies.

The same trend can be found at the investor level. The average venture fund size got much bigger in 2024, climbing 44% higher than it was in 2023. Meanwhile, the number of first-time venture funds sunk to its lowest point in the past decade, falling by 57% year over year.

Instead of investing in these emerging managers, LPs were much more likely to back established brands: In 2024, a group of just nine firms was responsible for nearly 50% of all capital raised by U.S. funds.

Among both startups and investors, capital became more concentrated in 2024 among the industry’s biggest names.

Investors reconsider their VC approach

This growing concentration among both startups and VC investors has been apparent over the past year to Divya Viveka, venture partner at Blue 9 Capital, a family office that pursues investments in early-stage companies and emerging fund managers across several tech sub-sectors.

One of the primary reasons for the change, she believes, is a shift in performance. Throughout the late 2010s and early 2020s, both the GPs who invest in startups and the LPs who invest in venture funds grew accustomed to a certain standard of returns. For much of this extended bull run, investors were confident that a wide swathe of potential investments across the venture asset class would be able to produce attractive results.

But this confidence has been shaken by a lack of recent exits and a reset in venture-backed valuations. And in times of upheaval, investors tend to seek havens of certainty. In many cases, this has created a reluctance to invest in emerging firms and startups without proven track records.

In other cases, it’s created a reluctance about the venture industry as a whole.

"Many private investors have recently pulled back from venture capital, particularly at the later stages," says Viveka. "The market has been marked by uncertainty over the past four to five years, with contracting DPI and growing concerns about whether venture capital remains a viable investment strategy."

A lack of recent returns

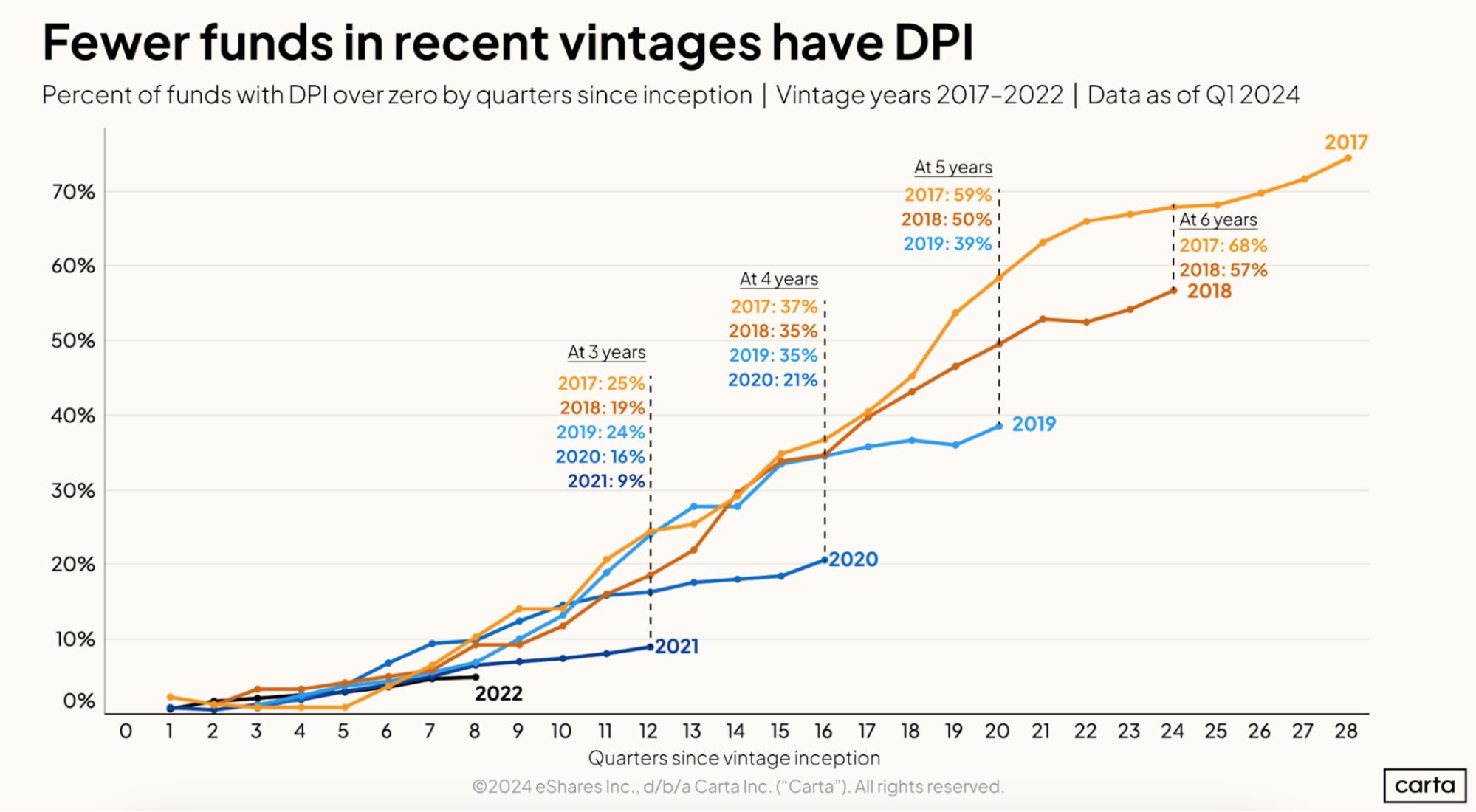

For an LP, the goal of investing in VC is to produce financial returns in the form of DPI. Among the most recent VC fund vintages, however, DPI has been difficult to come by. For instance, just 21% of funds from the 2020 vintage generated any DPI for investors during their first four years of existence, compared to a 37% rate after four years for 2017 vintage funds.

This is what Viveka means when she says some LPs are wondering about the viability of VC. If the hoped-for output from an investment fails to arrive, managers will be less inclined to keep inputting new capital.

And they’ll certainly be less inclined to make a new bet on an upstart manager.

"Venture capital hasn't delivered the same level of returns seen in the 2000s and early 2010s," says Viveka.

The impact of fewer funds

In this sense, the shrinking of the VC landscape may be a right-sizing. There was a surge of new funds in the late 2010s and early 2020s, as investors sought to capitalize on a booming market: The number of first-time funds raised nearly doubled between 2019 and 2021.

It’s possible that this was always unsustainable. In a less frothy market, there’s only so much alpha to go around.

But that doesn’t make the recent market consolidation any less painful for those who’ve felt the squeeze. It’s resulted in fewer fundraising opportunities for both less experienced founders and for newer investors.

And the reduction in first-time funds has knock-on effects throughout the ecosystem: Emerging managers are often more likely than larger brands to place a bet on first-time founders. Founders and investors from underrepresented backgrounds are among those who have been most affected by the shift.

“There are a lot of women who want to be writing checks, but because of the market, they just haven’t been able to,” Springate says. “And we need more women writing checks.”

On a macro level, however, Springate believes these recent years represent a healthy culling of the herd, a necessary correction for a VC market that had grown swollen after years of unabated success.

“I feel like a lot of the tourist noise in venture capital kind of went away,” Springate says. “And honestly, the strongest survived—whoever survived in the last four or five years of venture capital, I think they’ll be the ones that will stay around.”

Sign up for the Data Minute newsletter

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. ©2026 Carta. All rights reserved. Reproduction prohibited.