Earlier this year, Aziz Gilani, a managing director at early-stage venture firm Mercury, went on a listening tour with some of his LPs.

Several months earlier, Mercury had closed its fifth flagship fund with $160 million in commitments. In the meantime, the firm was actively managing the portfolio of its fourth fund, which closed four years earlier. For both of these funds, Gilani wanted to ensure that he and his colleagues were reporting back on all the metrics that their LPs most cared about.

He found that one metric in particular was on the tip of everyone’s tongue.

“DPI is the concrete thing that I think most folks are pretty focused on right now,” Gilani says.

Unfortunately, among the most recent fund vintages, it’s also in increasingly short supply.

A dearth of distributions

DPI (short for distributions to paid-in capital) measures how much capital a fund has returned to its LPs from exiting its investments, typically through IPOs and M&A. While other metrics like TVPI and IRR involve some level of projected financial performance, DPI measures only concrete results. Because venture firms often hold onto their investments for several years before finding an exit, it can also take several years for a venture fund to start generating significant DPI.

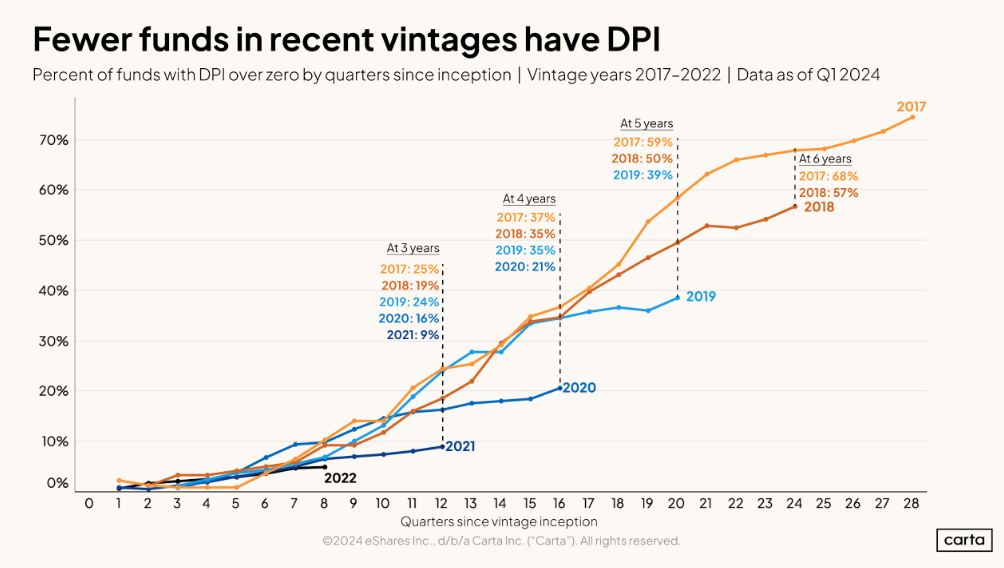

But this usual need for patience when it comes to DPI appears to be growing more extreme. Carta recently analyzed data from more than 1,800 venture funds from the years 2017 to 2022 to see how fund performance compares across these recent vintages. When it comes to DPI, there’s a clear trend: The more recent the vintage, the longer it’s taking for funds to find exits and begin returning capital to their LPs.

Among the 2017 fund vintage, for instance, 25% of funds had begun generating DPI after three years. Among the 2021 vintage, just 9% of funds had any DPI to speak of after three years.

After five years of investing, 59% of funds in the 2017 vintage had begun generating DPI. For the 2019 vintage, the rate was just 39%. In other words, more than three out of every five VC funds on Carta that closed in 2019 had not yet distributed any capital back to their LPs after five years.

The trend plays out across vintages: The 2020 vintage is lagging well behind where older vintages were after four years. The 2022 vintage is lagging behind where other vintages were after two years. It’s clear that, over the past year, these recent vintages have been falling behind the typical timeline for when venture funds start creating DPI.

Which, as Gilani and other early-stage VCs know, is not what many LPs want to hear.

“I tell my LPs all the time: We are fully focused on DPI,” says Marcos Fernandez, managing director at Fiat Ventures, an early-stage fintech firm. “Because until you realize that liquidity, we have failed.”

Why distributions are harder to find

The short answer to why distributions have slowed down over the past year-plus is that exit activity has slowed down, too.

So, why has exit activity slowed down? The primary reason is the valuation reset that has occurred across both public and private markets during 2022 and 2023. Faced with the prospect of lower valuations, many companies and their investors shied away from IPOs or M&A, hoping that valuations would start to trend up again and an exit would begin to look more attractive.

“At the end of the day, as you look toward the tail end of a fund, it’s really about DPI,” Fernandez says. “And that’s been one of the things that’s been lacking across the venture industry for a long time, largely because of a smaller IPO window and fewer liquidity events.”

In more recent months, valuations have begun to trend up. Late-stage startup valuations shot upward during Q2, and public valuation multiples are again nearing the highs of 2021. Yet so far, at least, no concurrent increase in exit activity has occurred.

Why DPI matters

DPI has always been one of the key metrics—if not the key metric—by which VC funds are measured. This is because generating distributions is the raison d'être of venture capital. LPs only invest in VC funds because of the promise of future returns. And without those returns, LPs will not have capital to reinvest in the next generation of funds.

“LP allocators into venture funds will often recycle money back into the category,” Fernandez says. “If they have a particular allocation to venture, when they get distributions from venture funds, then a lot of the time they re-allocate back to new venture funds. And because there’s been a limited amount of liquidity, you’re seeing slower allocation back into the category.”

But as Gilani heard in his recent survey, LPs are perhaps even more focused on DPI today than they have been in prior environments. And that’s precisely because exits—and therefore distributions—have grown more rare.

LPs will take all the information on fund performance they can get. If a fund is still in the early days of deploying capital and growing its portfolio companies, metrics other than DPI will suffice. But ask any investor: It’s hard to beat cold, hard cash.

“Some firms focus on intermediate IRRs. TVPI can be a great metric, especially when it’s validated by external marks,” Gilani says. “But from my perspective, DPI is the metric that rules them all.”