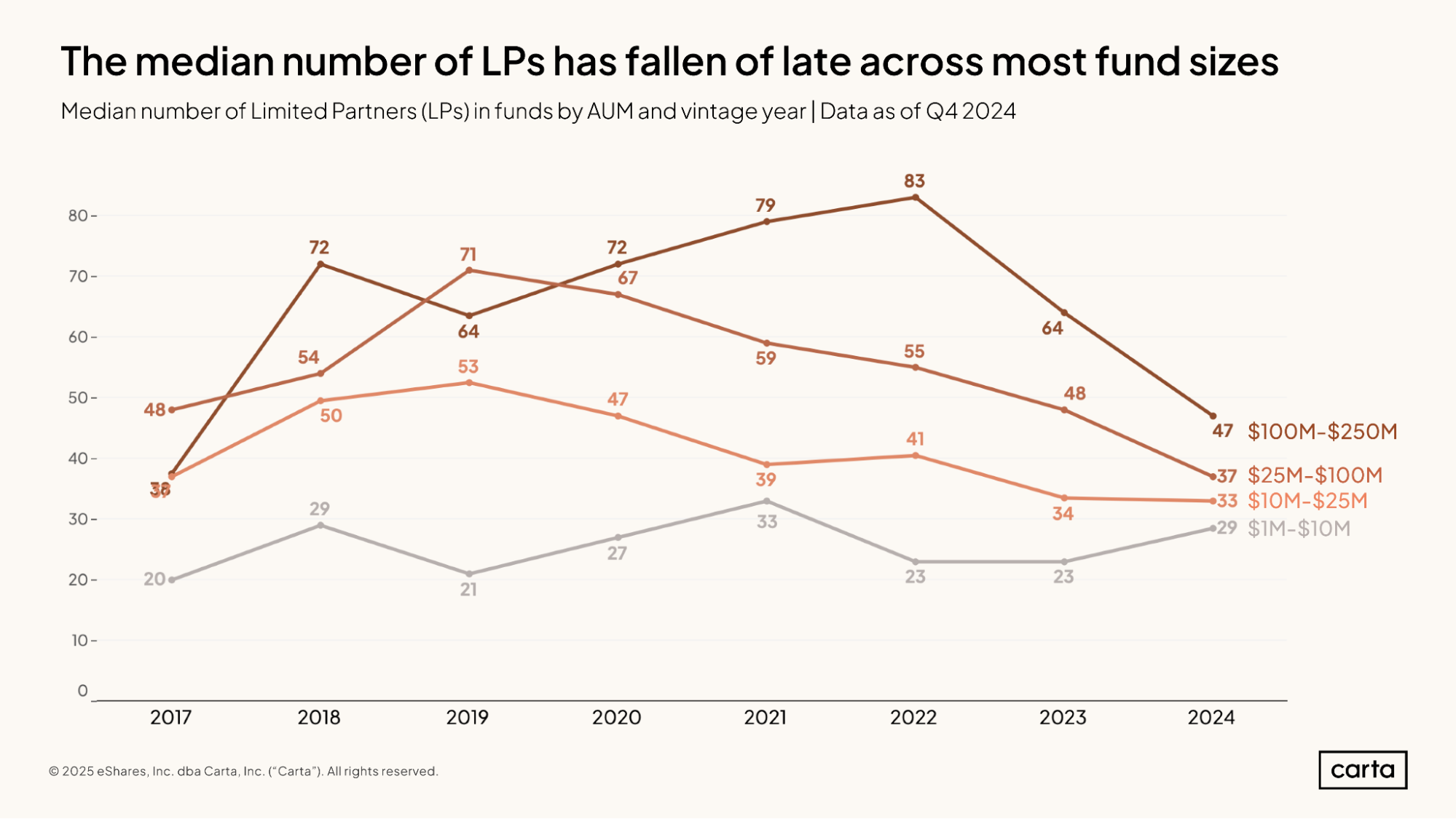

Back in 2022, the median venture fund with between $100 million and $250 million in assets under management had raised that capital from 83 different LPs, the highest number in recent history.

It seemed like allocators of all kinds were eager to gain access to an asset class in the middle of an unprecedented boom.

But that boom has since come to an end. For some LPs, this was cause to pull back. By 2024, the median number of LPs for VC funds between $100 million and $250 million had fallen to 47, a reduction of nearly 50%.

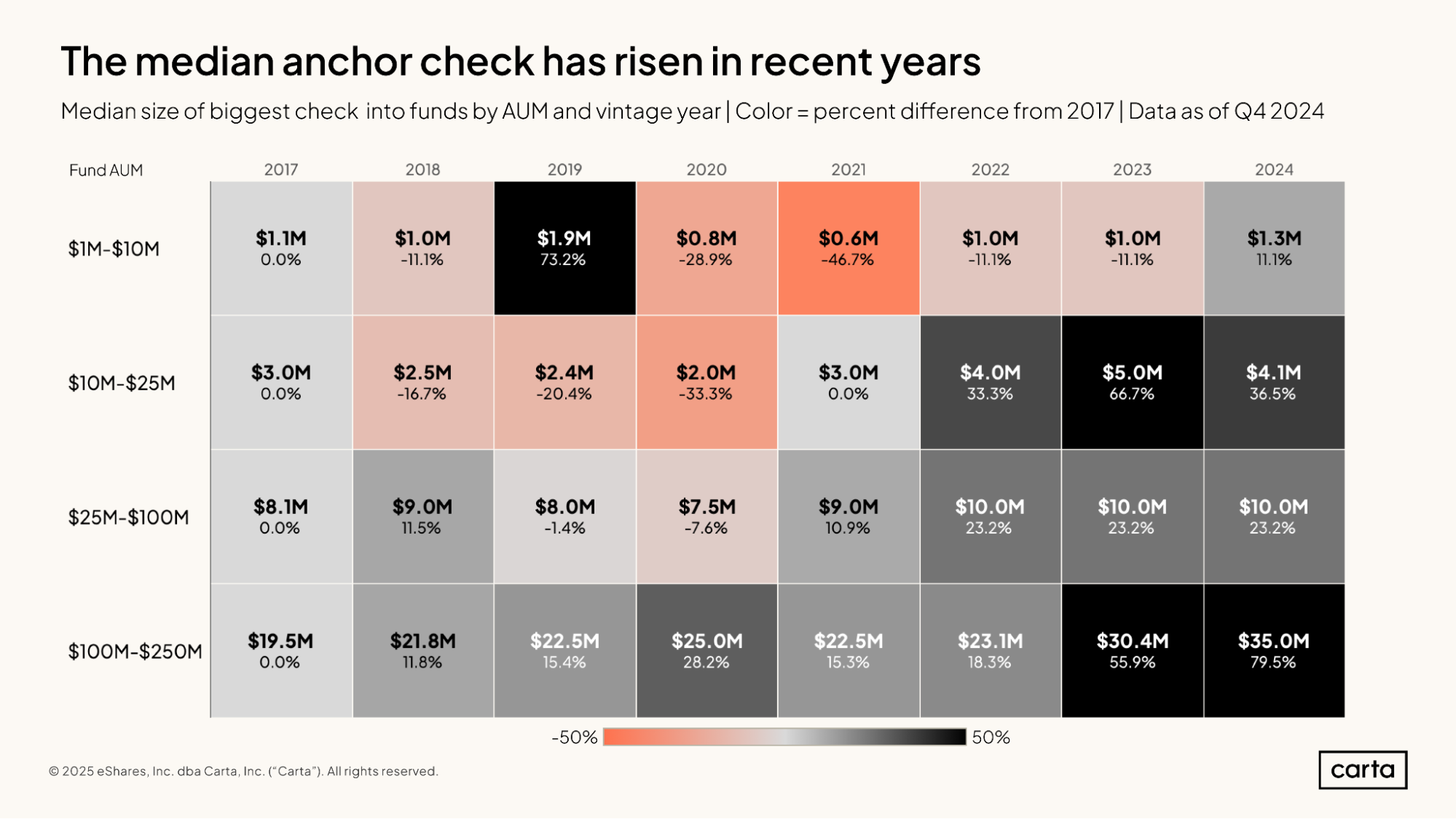

To make up for this downsizing of the typical investor base, some of the LPs that are still investing in new venture funds are writing significantly larger checks. In 2022, the median size of the biggest check written for funds with between $100 million and $250 million in AUM was $23.1 million. In 2024, it was more than 50% higher, at $35 million.

Over the past three years, venture fund managers and their LPs have had to adapt to a long list of new realities in the venture capital market—including shifts in the makeup of VC funds, the way that VC funds raise capital, and the typical fund performance that LPs might expect.

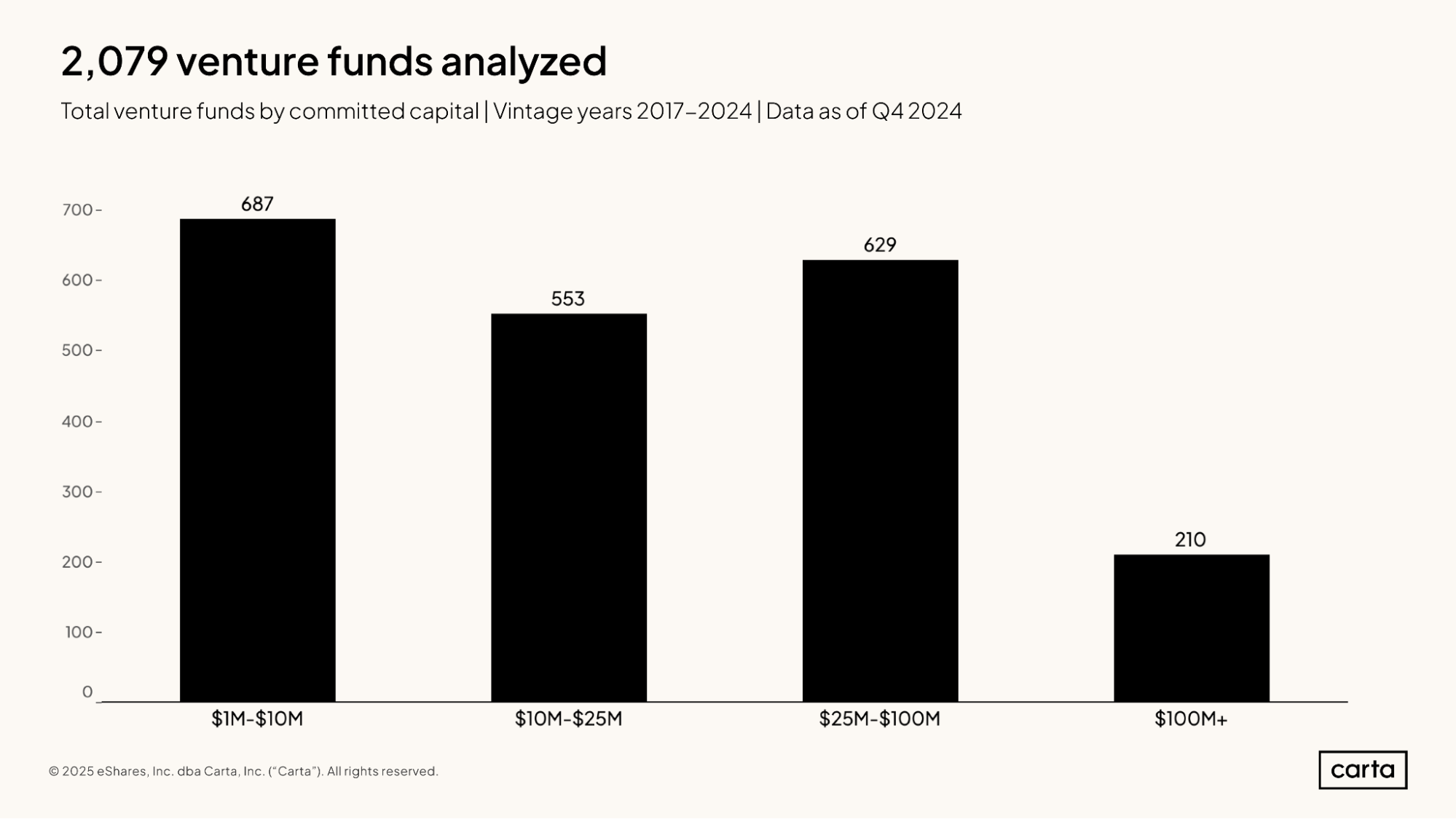

This report relies on data from more than 2,000 venture funds that currently use Carta Fund Administration to paint a picture of this new reality and examine its implications for VCs and LPs alike. Only U.S. funds are included in this analysis, and all included funds are direct venture investors, as opposed to funds of funds. Funds must have been in vintage years 2017 through 2024. More detail on our methodology can be found at the end of this report.

Highlights

The venture slowdown is leaving a mark: For every fund vintage from 2017 through 2020, the past two to three years have brought significant declines in median IRR. For the 2017 vintage, for instance, median IRR fell from 16.8% as of Q4 2021 to 12.0% at the end of Q4 2024.

Top decile TVPI is highest in smaller funds: In the upper tiers of performance, the smallest venture funds often post the best returns. In the 2018 vintage, the 90th percentile for TVPI among funds with $1 million to $10 million in assets is 4.03x. For funds in the same vintage with $100 million or more in assets, the 90th percentile for TVPI is 1.67x.

Most newer funds are still waiting for DPI: Half of all funds from the 2018 vintage have still not distributed any capital back to their LPs. For more recent vintages, distributions are even harder to find: Just 26% of funds from the 2020 vintage and 12% of funds from 2021 have begun to record DPI.

Fund details & deployment

This report features data from 2,079 venture funds from across the full span of the U.S. ecosystem. About 33% of these funds have between $1 million and $10 million in assets under management. Another 27% manage between $10 million and $25 million in assets, and 30% are between $25 million and $100 million in AUM. The upper echelon of venture funds—those larger than $100 million—comprise just over 10% of the sample.

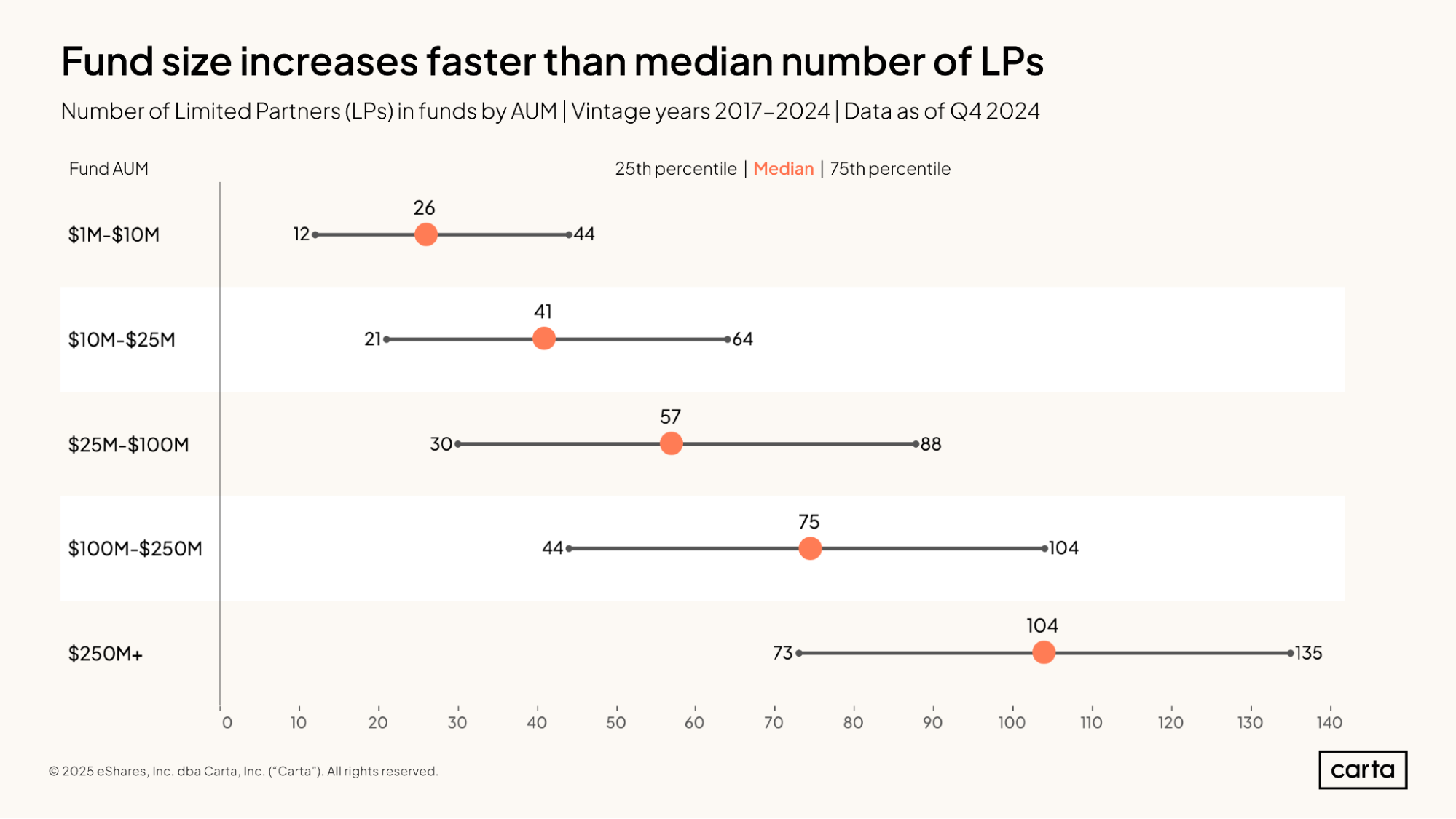

Venture funds with more assets under management also tend to have more LPs. The median fund with between $1 million and $10 million in AUM raises that capital from 26 different LPs, while the median fund with more than $250 million in AUM has 104 LPs.

While this trend of larger funds having more LPs tends to hold true across all venture fund sizes, there are also plenty of exceptions. In each of these fund size intervals, there’s a wide range between the 25th percentile for LP count and the 75th percentile. It’s possible for a $25 million fund to have more LPs than a $250 million vehicle.

Median LP count fell by 43% between 2022 and 2024 for funds with between $100 million and $250 million and by 33% for funds with between $25 million and $100 million in assets.

Compared to the highs of the venture market in 2021 and 2022, there are fewer LPs in the market today actively looking to commit cash to new funds. As a result, fund managers are having to concentrate their fundraising among fewer capital sources.

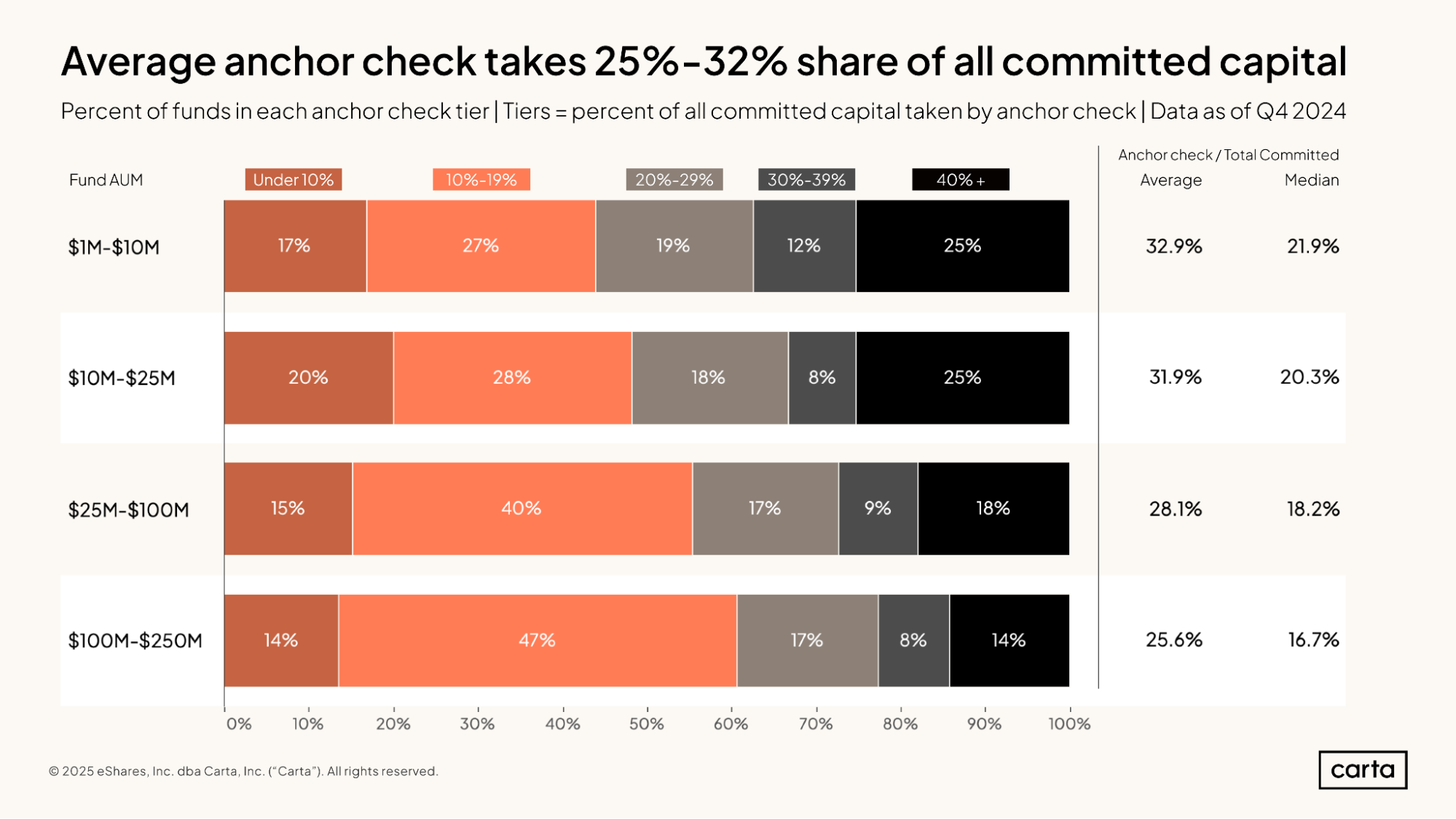

The largest contribution to a venture fund by any one LP is referred to as the anchor check. Across all fund sizes, the median size of this anchor check is rising in both the short term and the long term.

For funds with between $100 million and $250 million in assets, the median anchor check rose from $19.5 million in 2017 to $25 million in 2020. Since then, it’s continued to climb, reaching $35 million in 2024.

This trend is likely related to a “flight to quality” phenomenon, where LPs deploy capital into fewer funds, thereby increasing the median check size.

For funds with between $1 million and $10 million in AUM, the average anchor check accounts for 32.9% of the total capital committed to the fund. About 17% of the time, the anchor check accounts for less than 10% of total committed capital for funds in this smallest size interval. About 25% of the time, the anchor check makes up more than 40% of committed capital.

As venture funds get larger, the anchor check tends to make up a smaller proportion of the vehicle’s total firepower. For funds with between $100 million and $250 million in AUM, the average anchor check accounts for 25.6% of the total capital committed to the fund.

Full report available: Start reading now for free

Our complete VC Fund Performance report includes data on fund performance from more than 2,000 venture funds.

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. ©2026 Carta. All rights reserved. Reproduction prohibited.