Executive summary

When it comes to headline numbers like deals completed and dollars raised, many aspects of the venture capital landscape in Q3 2024 looked familiar.

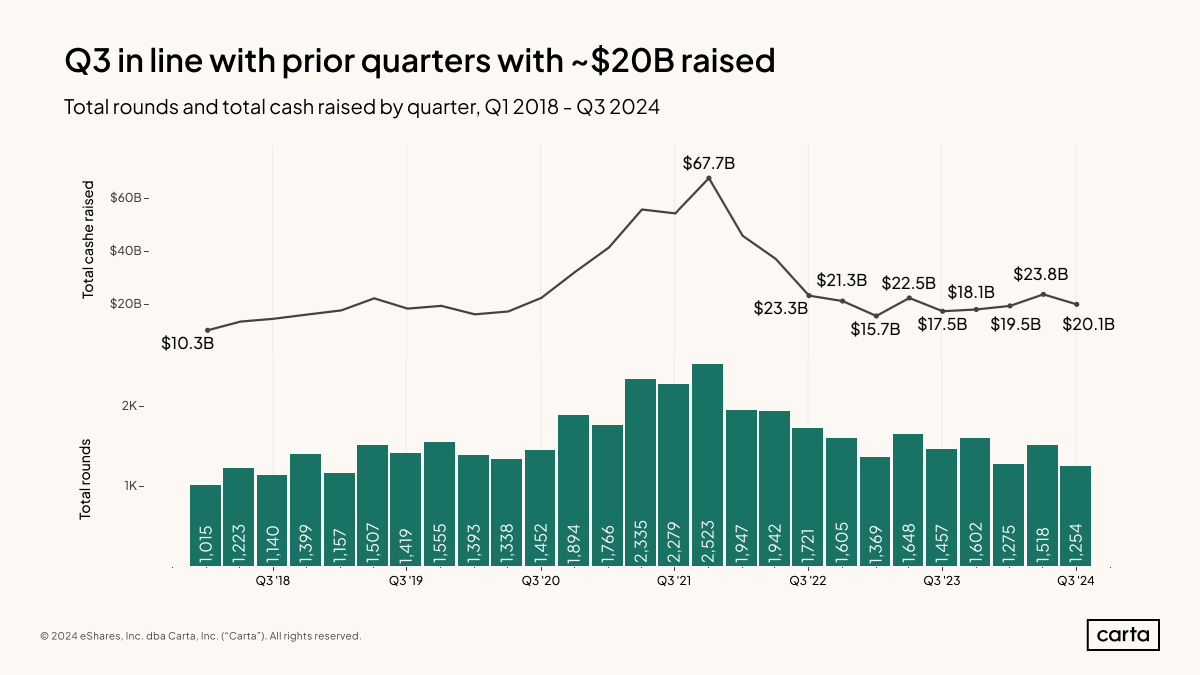

In the aftermath of the remarkable pandemic bull run of 2021 and early 2022, the venture market has settled into a new normal. For nine straight quarters now, private startups on Carta have raised somewhere between 1,250 and 1,650 new rounds and brought in between $15.7 billion and $23.8 billion in new capital. After the roller-coaster ride of the preceding two years, it’s been a notable stretch of high-level consistency.

But venture dealmaking data from Q3 also shows that much has changed within the startup world’s many nooks and crannies. At the seed stage and Series A, deal activity slumped in Q3. The median valuation at these stages, however, trended up. Raising an early-stage round today is no easy task—but some startups have been able to do so at increasingly high prices.

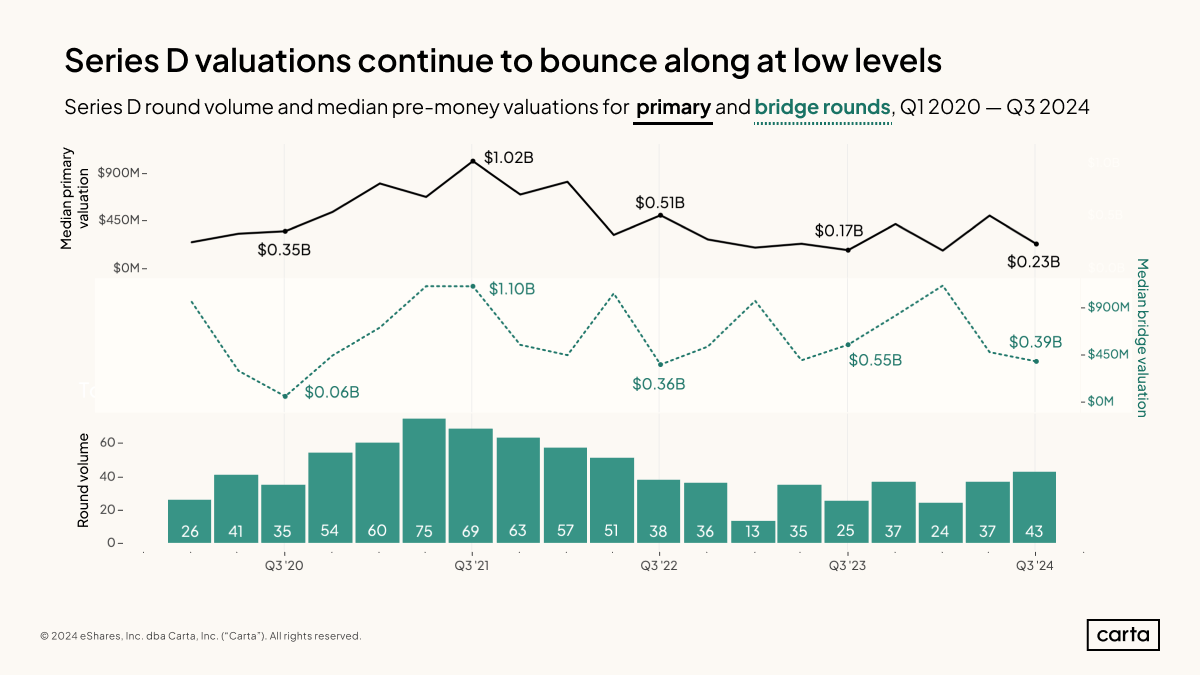

At later stages, meanwhile, deal activity trended up in Q3. Companies closed 43 new Series D rounds on Carta, the highest quarterly Series D count in more than two years. The number of M&A deals targeting startups also ticked up last quarter, providing welcome opportunities to generate liquidity. After activity plunged during the recent venture slowdown, the late-stage market may be heating back up.

Q3 highlights

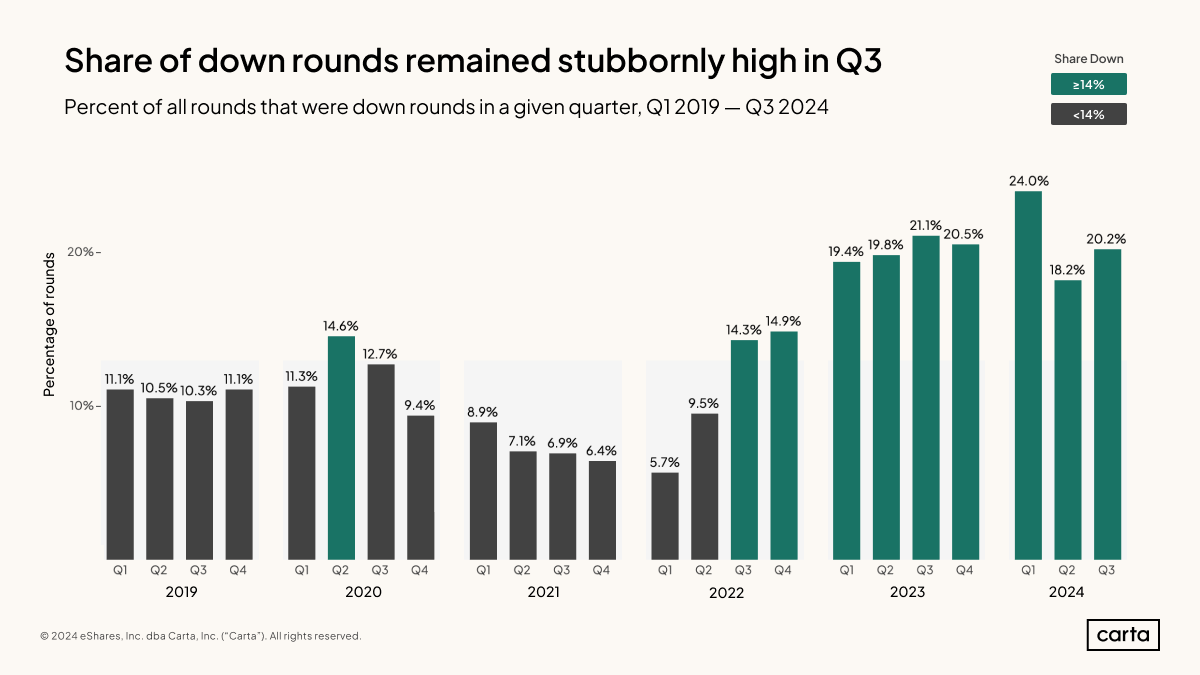

Down rounds are lingering: More than 20% of rounds closed last quarter were down rounds. The frequency of down rounds began to climb in late 2022, and it’s remained historically high ever since.

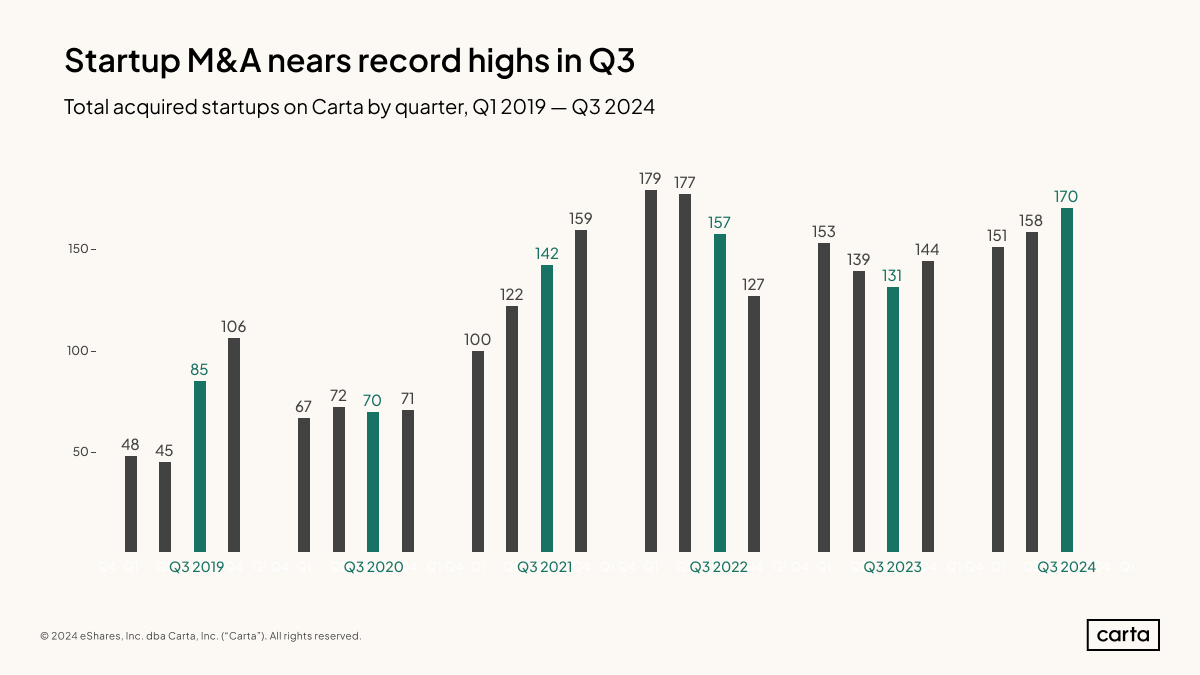

M&A activity is increasing: Startups on Carta were the target of 170 M&A transactions during Q3, the highest quarterly figure in more than two years. The number of startups exiting through M&A has now increased in four consecutive quarters.

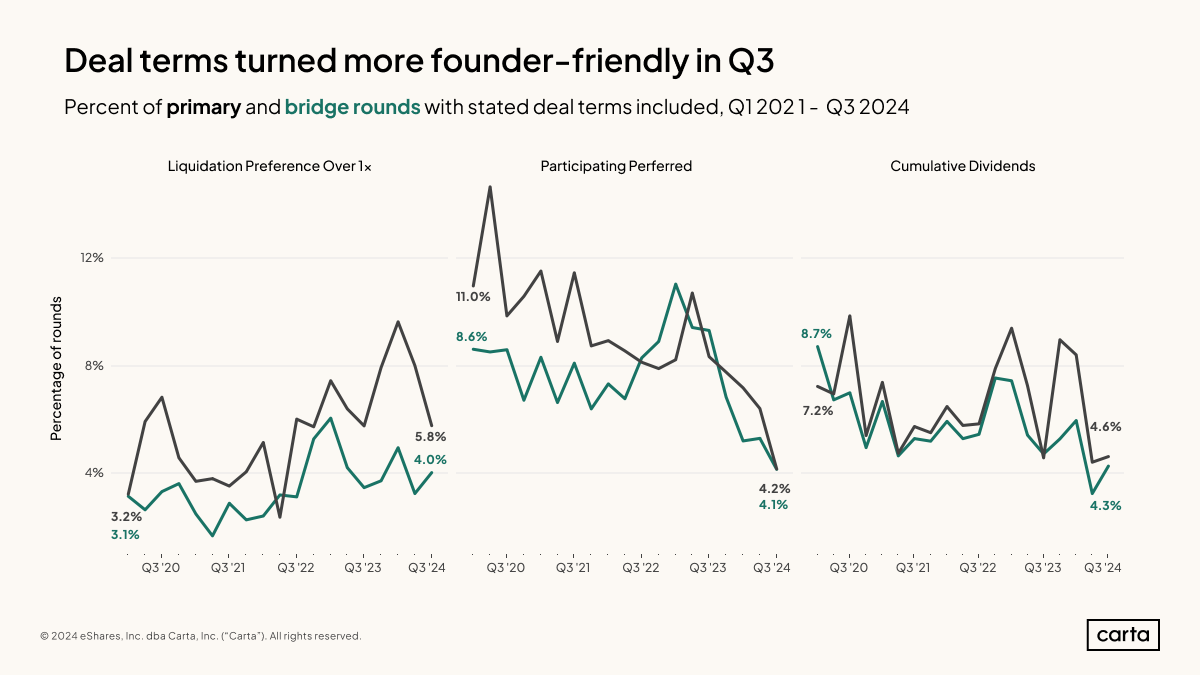

Deal terms are shifting: Just 4.1% of new term sheets signed in Q3 involved participating preferred shares, the lowest quarterly rate so far this decade. The frequency of participating preferred shares is down more than 50% since the start of 2020.

Note: If you’re looking for more industry-specific data, download the addendum to this report for an extended dataset.

Key trends

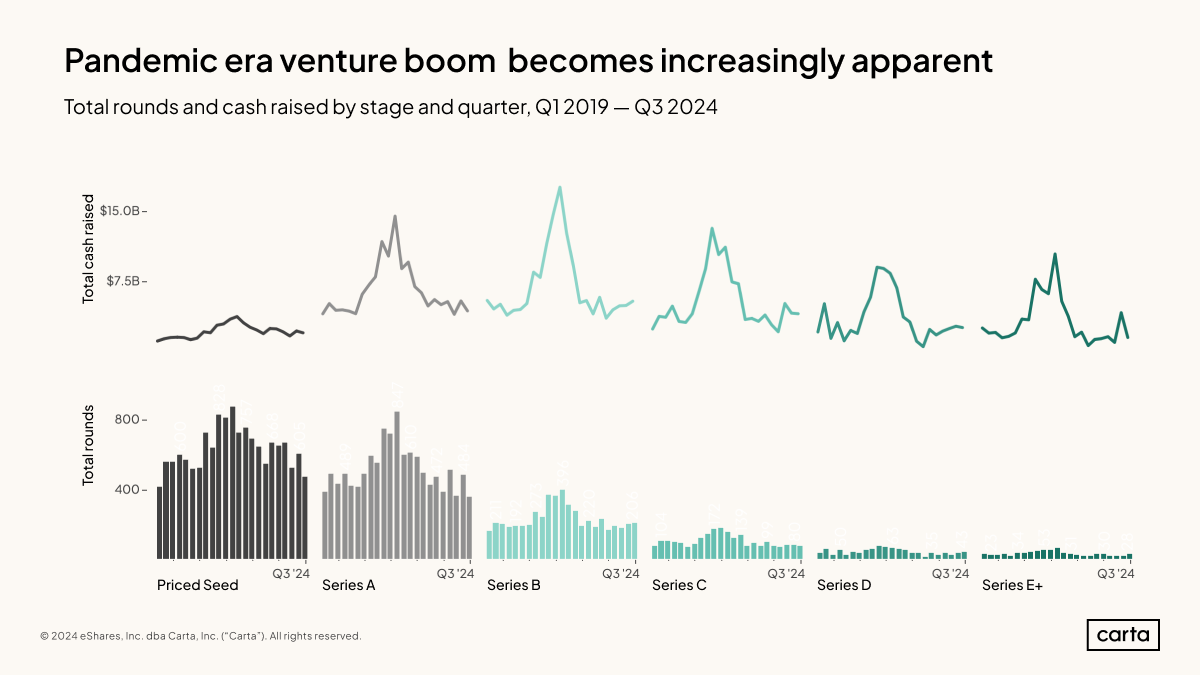

As time goes by, the anomalous nature of the pandemic venture boom grows more and more apparent.

Startups have so far recorded $20.1 billion in venture capital raised across 1,254 transactions on Carta during Q3, with both of those totals set to rise slightly in the weeks ahead as more companies report funding events. These headline numbers for venture fundraising have now looked fairly similar for the past eight quarters. They’re also fairly similar to where they stood throughout 2018, 2019 and early 2020, in the runup to the venture boom.

During that boom, from Q4 2020 through Q2 2022, startups raised more than $30 billion and completed more than 1,600 transactions for seven consecutive quarters. But it’s clear this was an outlier, not a new normal. In the other 20 quarters dating back to the start of 2018, quarterly capital raised has never finished above $23.8 billion, and deal count has topped 1,500 only once.

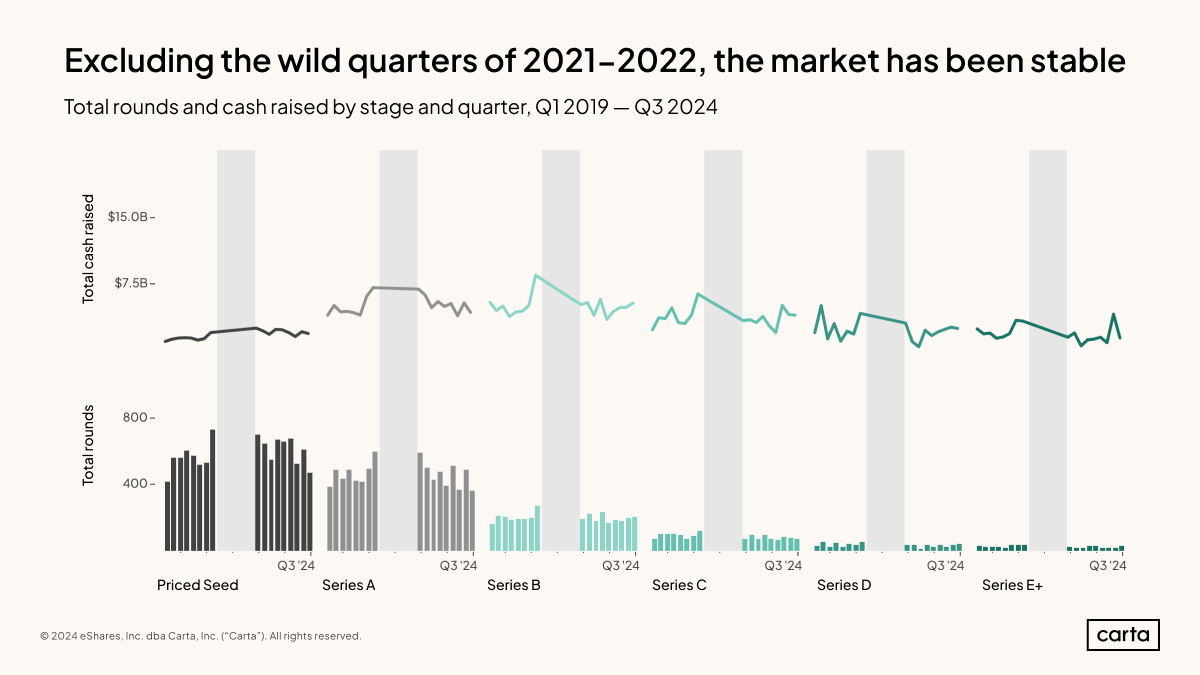

If we eliminate the six-quarter stretch of Q1 2021 through Q2 2022, recent trend lines for venture deal counts and dollars raised at different stages look very different. There have still been fluctuations in activity over the past five years, in some cases significant ones. But this image of the market is much more consistent.

More than 20% of all new venture investments on Carta in Q3 were down rounds, the fourth-highest quarterly total dating back to at least the start of 2019. Startups are still grappling with the realities of the widespread valuation reset that began in mid-2022.

During 2021 and early 2022, venture-backed valuations soared to all-time highs after nearly a decade of steady growth. It was rare to see any startup raise new capital at a reduced valuation. But as valuations have undergone a reset in the past two-plus years, some companies have found it difficult to raise capital at the lofty valuations they once attained. Given how the average time interval between priced rounds has also increased in the past two years, many of the companies that raised capital in Q3 were doing so for the first time since valuations began to decline.

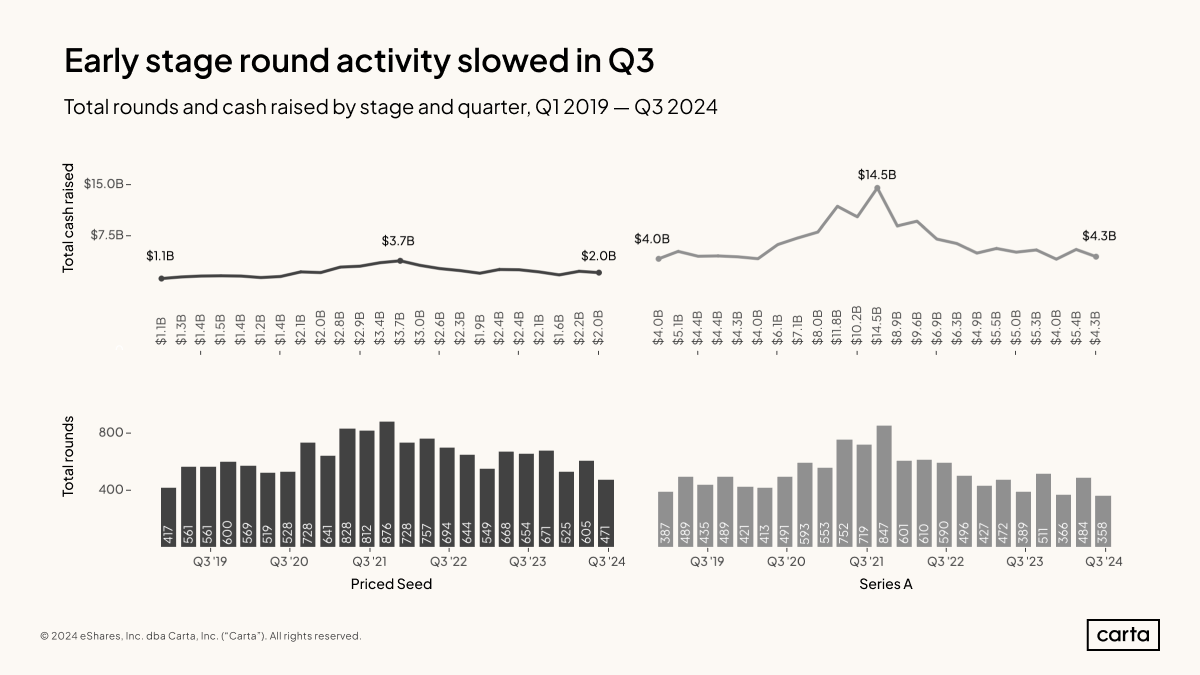

At current deal counts, the number of new seed investments fell by 22% in Q3 compared to the prior quarter, while the number of new Series A investments declined by 26%. Even though these totals will continue to tick up as more deals are reported in the weeks to come, it seems safe to say that early-stage activity experienced a slowdown in Q3.

The amount of capital going into those early-stage deals is also trending down. Cash raised in seed investments dipped by 9% in Q3, while Series A cash raised fell by 20%.

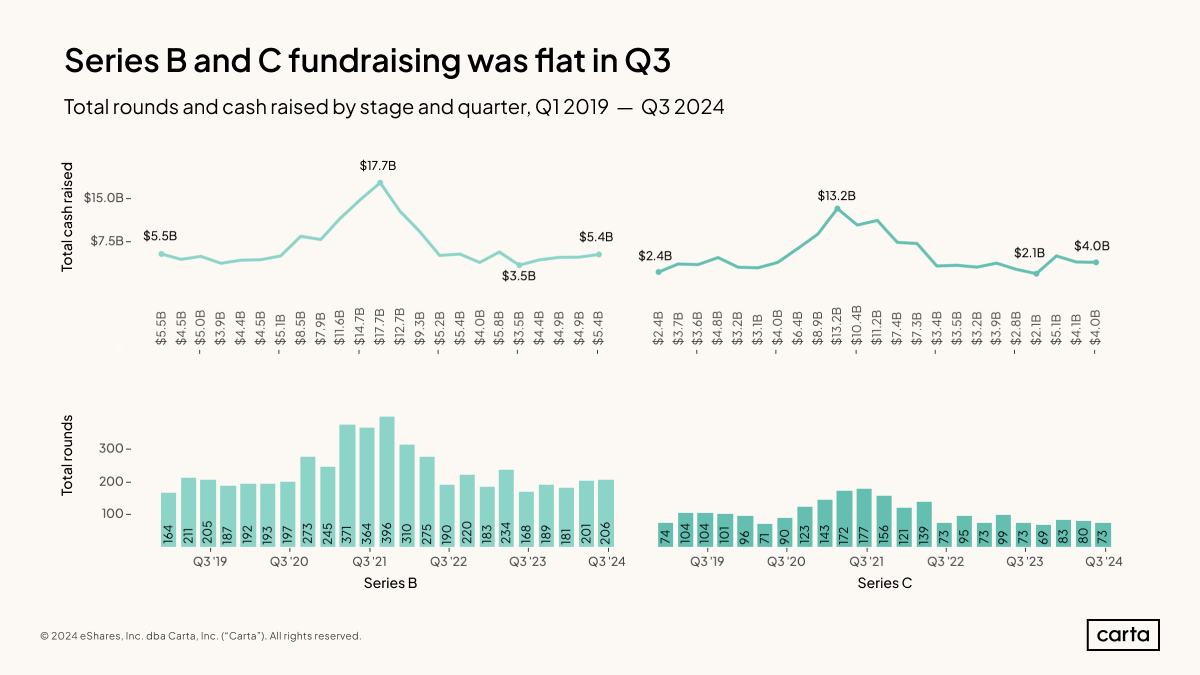

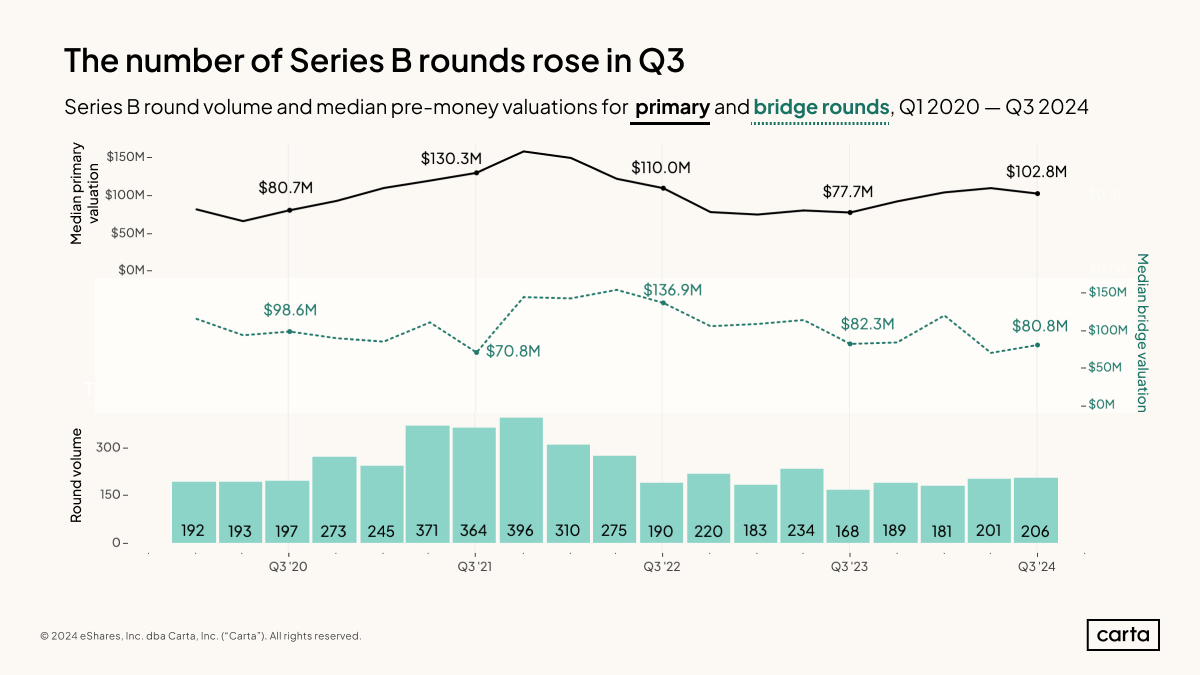

The Series B market experienced some positive momentum in Q3, with capital raised climbing by more than 10% compared to the previous quarter. It was the first time in the past five quarters that Series B startups on Carta have topped the $5 billion mark in quarterly fundraising.

There was some quarter-over-quarter variation in the number of deals getting done at these two stages, but the changes were slight. On a longer-term basis, there’s a clearer trend: Series B deal count is up nearly 23% year over year.

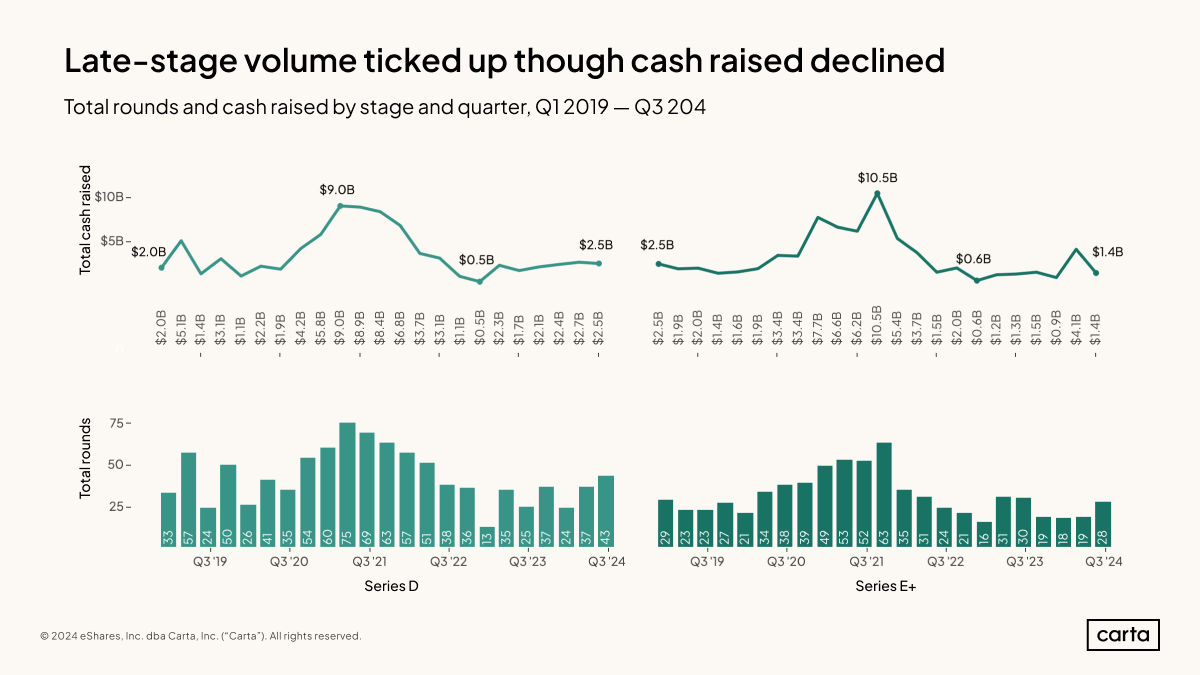

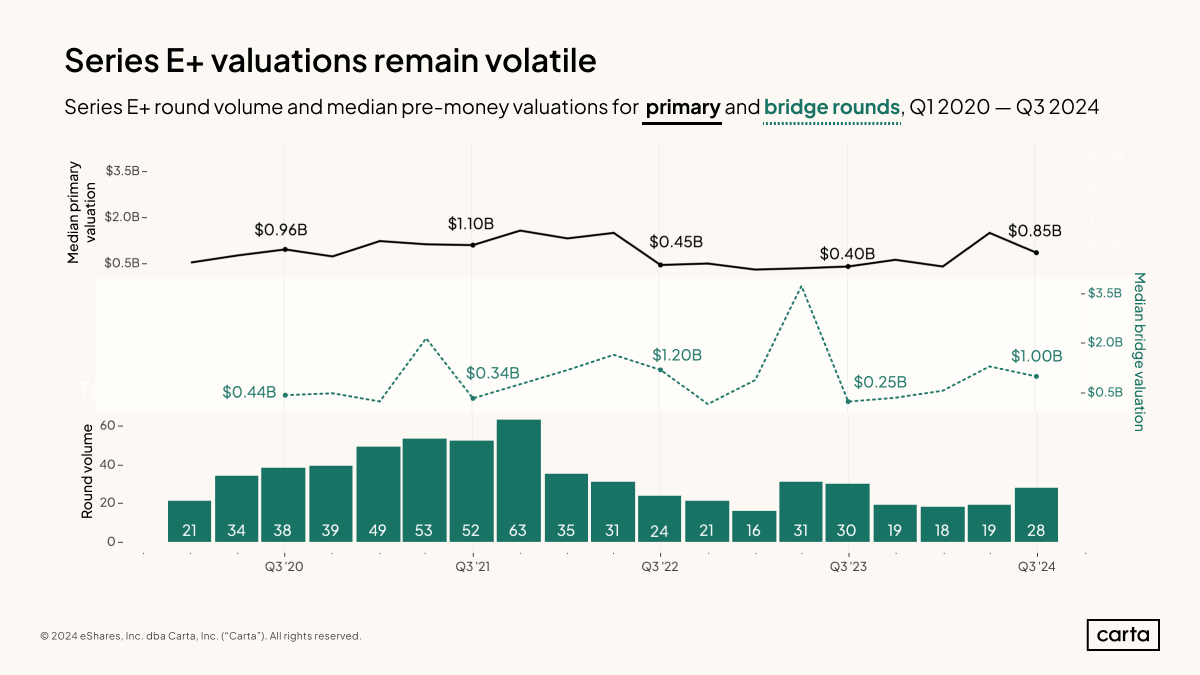

More late-stage deals took place on Carta in Q3 than in Q2: At Series E and beyond, total transaction count climbed from 19 to 28. The average size of those investments, however, fell considerably, from about $216 million to just $50 million.

Deal count also is on the rise at Series D. And there, transaction size has proven much more resilient. With $2.5 billion raised across 43 deals, the average Series D transaction size was $58 million in Q3, down slightly from $73 million in Q2.

The percentage of new venture term sheets that include participating preferred shares has plunged over the past several quarters. Last quarter, it reached a new decade low: Just 4.1% of primary rounds (and 4.2% of bridge rounds) in Q3 involved participating preferred shares.

Conversely, there was a slight increase in Q3 in the percentage of new primary rounds that include cumulative dividends or a liquidation preference higher than 1x. While both participating preferred shares and cumulative dividends are less common than they were at the start of the 2020s, liquidation preferences above 1x have grown more common.

Fundraising and valuations

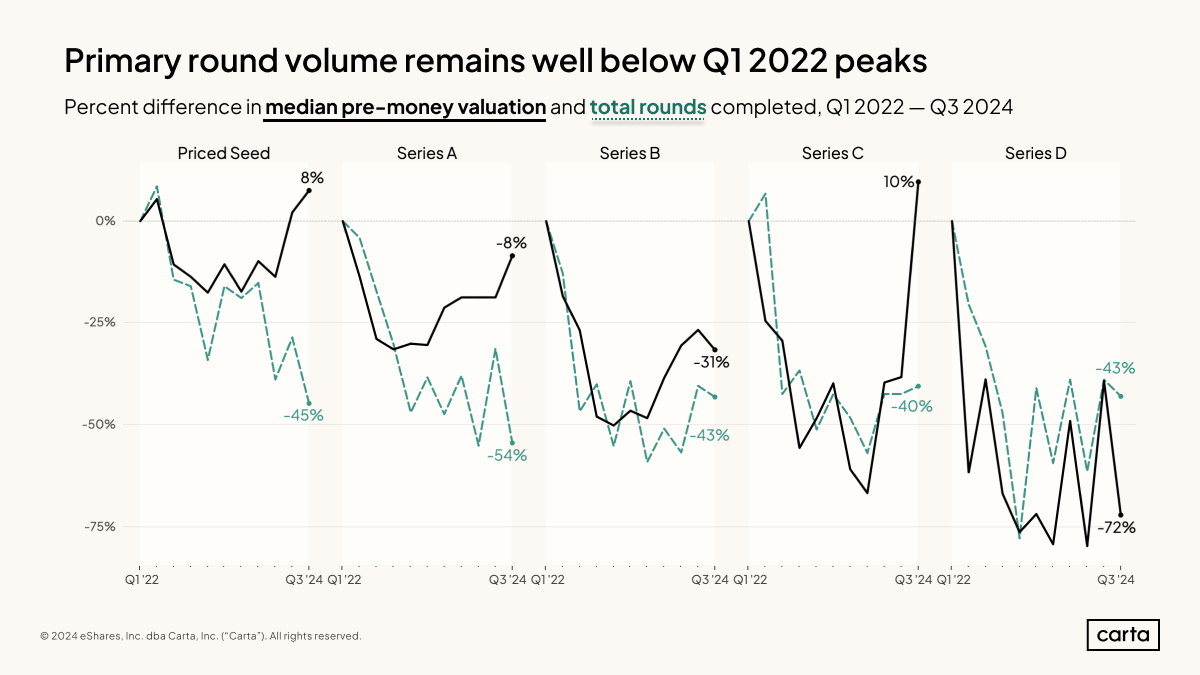

Back in the first quarter of 2022, the venture funding market was still flying near historic highs. So it makes sense that, since then, deal activity has slowed considerably across the whole of the venture lifecycle. Across every stage of startup life, the number of new startup investments that took place in Q3 was at least 40% lower than in Q1 2022.

The landscape of valuations is less consistent. At both seed and Series C, median valuations were actually higher in Q3 2024 than they were back in Q1 2022. At Series B and Series D, meanwhile, valuations still lag well behind figures from early 2022.

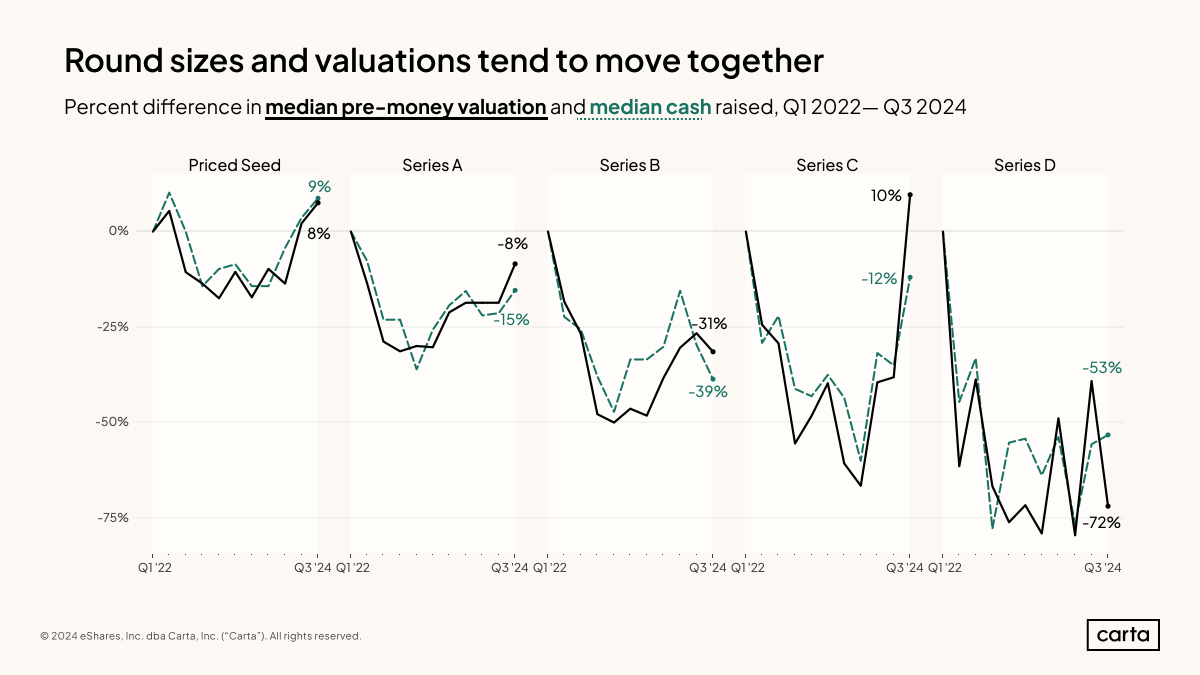

The correlation between median valuation and median round sizes, meanwhile, is still going strong. At most stages, the trend lines for these two statistics have mostly moved in concert over the past three years. At seed, they’re nearly identical.

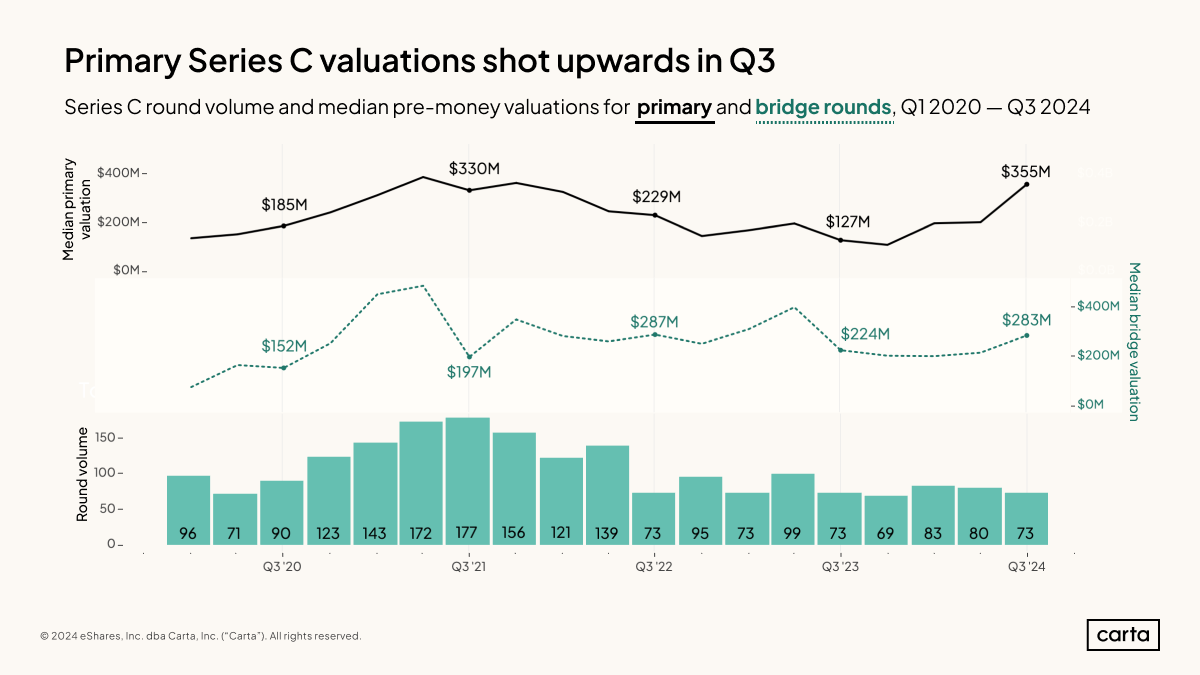

In most cases, both median valuations and median round sizes are lower than they were in Q1 2022. But there’s significant variation across the stages. Earlier stages have tended to be more resilient than later stages, with the notable exception of Series C, where both median valuations and median deal sizes have spiked so far in 2024.

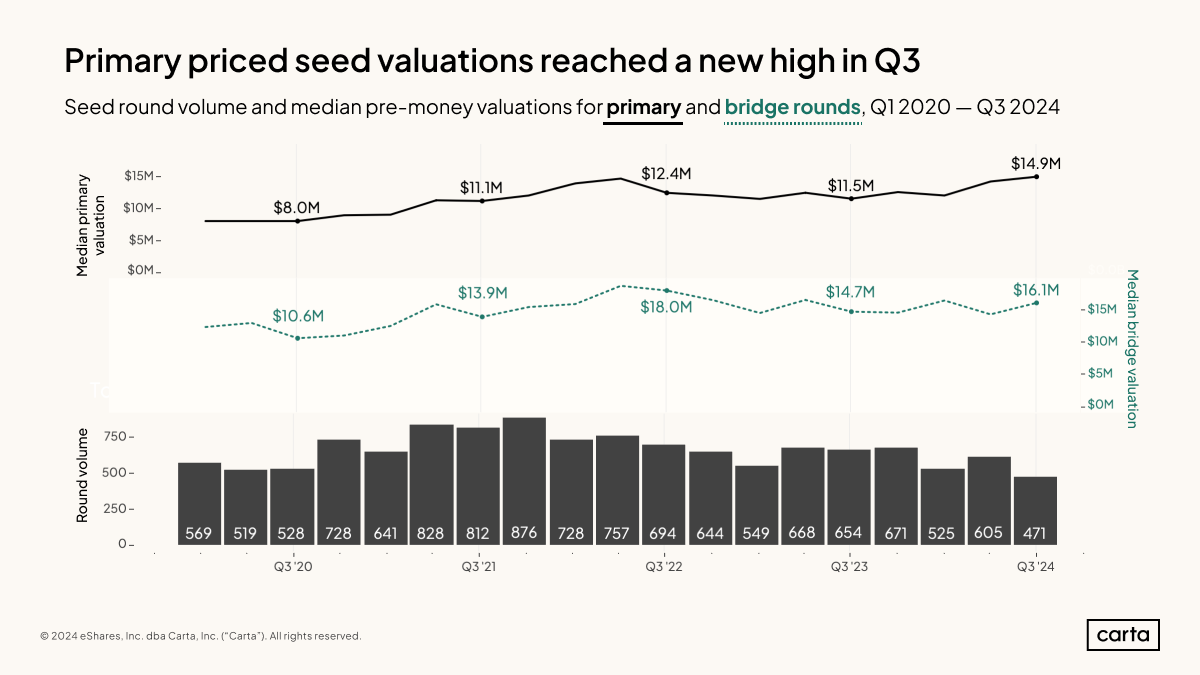

The median pre-money valuation on primary seed rounds climbed to $14.9 million during Q3, its highest point so far this decade. After previously settling somewhere between $11.5 million and $12.5 million for six consecutive quarters, primary seed valuations have been on the rise in Q2 and Q3.

The median valuation on bridge rounds raised by seed startups also ticked up in Q3, reaching $16.1 million. This was the first time in more than a year that the median seed valuation increased on both primary and bridge rounds in the same quarter.

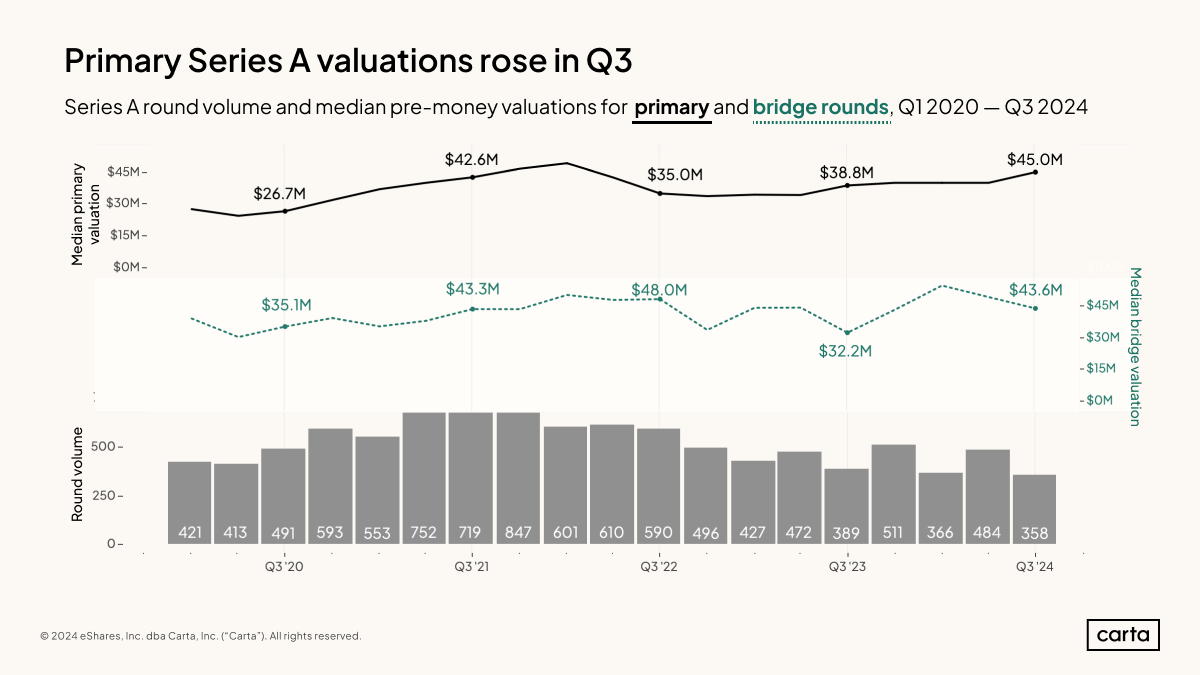

In terms of activity, it was a slow quarter in the Series A market, with fewer than 400 new transactions logged on Carta for just the third time so far this decade. But many of those companies that were able to raise new capital did so on attractive terms: The median pre-money valuation on primary Series A rounds jumped to $45 million in Q3, the third-highest quarterly figure of the 2020s.

Valuations for primary rounds and bridge rounds have been moving in opposite directions at Series A. Over the past two quarters, the median pre-money valuation climbed by 13% on primary rounds and declined by 20% on bridge rounds. During that span, the relative frequency of bridge rounds has remained similar. Bridge rounds made up 42% of all Series A activity in Q1 2024 and 40% in Q3.

The median valuation on primary Series B rounds was above $100 million in Q3 for the third straight quarter. Previously, it had been below $100 million for five straight quarters. The Series B market seems to have restabilized at a slightly higher level after bottoming out in late 2022 and into 2023.

Deal activity is also trending up at Series B, with 206 transactions currently logged for Q3. That’s the second-highest number of new quarterly deals at this stage since the start of 2023.

Series C valuations are soaring. The median pre-money valuation on primary Series C rounds rocketed to $354.5 million in Q3, up 77% from the previous quarter. On bridge rounds raised by Series C startups, the median pre-money valuation rose by 32% in Q3.

In general, Series C valuations have proven relatively volatile over the past two years—much more volatile, certainly, than Series C deal activity. Total Series C deal count on Carta has now landed somewhere between 69 and 99 transactions for nine consecutive quarters.

The median pre-money valuation on Series D deals plummeted in Q3, falling by 48% from the previous quarter. This continues a recent seesawing in Series D valuations, with the median rising sharply one quarter only to fall sharply the next.

Part of this variance in Series D valuations is due to the relative scarcity of transactions at this stage: Just 43 companies raised Series D rounds in Q3. But the size of that sample is growing. Since the start of 2023, Series D deal count has been slowly but steadily rising.

The number of deals getting done at Series E and beyond is even smaller than at Series D: Companies closed 28 transactions on Carta at these latest stages during Q3. Like at Series D, however, the recent trend is up. Previously, there had been fewer than 20 deals at Series E+ in the past three quarters.

The median valuation at Series E+ fell significantly in Q3—but it’s still much higher than it was for most of the past two years. After falling below $600 million for six quarters, the median pre-money valuation at Series E+ has now been above $900 million two quarters in a row.

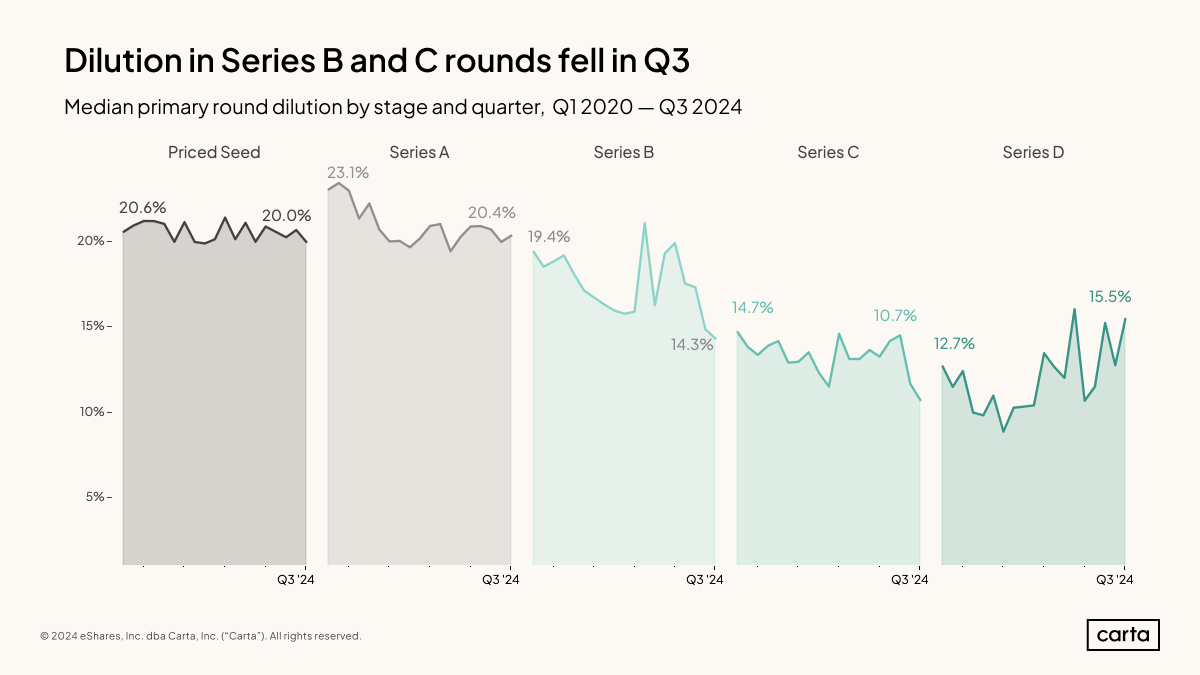

There have been some notable shifts on the dilution landscape in recent quarters. Chief among them, perhaps, is the recent declines in median dilution at both Series B and Series C, both of which reached new lows in Q3. This means that startups are selling off a smaller percentage of their company’s shares to investors when they raise new rounds at these stages.

Because of these declines, the gap in expected dilution between Series A and Series B has widened considerably. In Q4 2022, the median dilution at these two stages was nearly equal. In Q3 2024, they were more than six percentage points apart. In terms of median dilution, Series B is now closer to Series C than it is to Series A, a major change from the pre-pandemic norm.

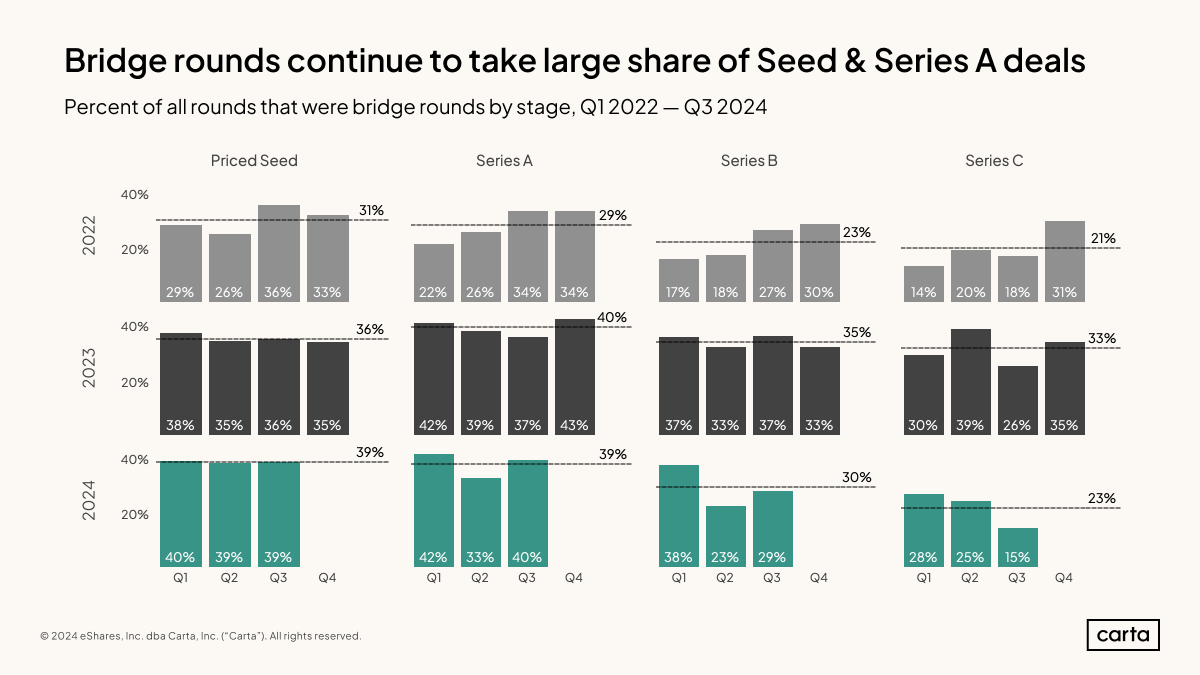

About 40% of all rounds raised in Q3 by seed and Series A startups were bridge rounds. At both stages, the latest bridge-round rates remain near historic highs, continuing a trend that intensified when the VC funding market began to slow down in 2022. Rather than raising new priced rounds, a large number of early-stage startups are still opting to raise capital through extensions to their most recent rounds—either out of choice, or out of necessity.

Conversely, bridge rounds may be falling out of fashion at Series C. There was a spike in Series C bridge rounds during late 2022 and 2023, just like there was at earlier stages of startup life. But in Q3, just 15% of deals closed by Series C startups were bridge rounds, the lowest rate in more than three years. The Series C bridge-round rate has now declined in three straight quarters.

Last quarter, 170 startups on Carta were the target of M&A transactions. That’s the highest total since the middle of 2022, and it’s the third-highest number dating back to the start of 2019. Total M&A activity targeting startups has now increased in four straight quarters.

In many cases, these transactions are providing a much-needed source of liquidity for the wider startup ecosystem. With IPOs remaining relatively few and far between for the third consecutive year, M&A provides another pathway for GPs to generate a return on their investment and redistribute capital to LPs.

Geographical trends

A note on methodology: For city geographies, we utilize Metropolitan Statistical Areas (MSAs), and for regions, we employ the U.S. Census-defined regions. Additionally, we exclude Delaware-registered corporations from our analysis at both the state and regional levels. We do not publish state-level data if the sample size falls below 10, but these states are still included in the region-level aggregation.

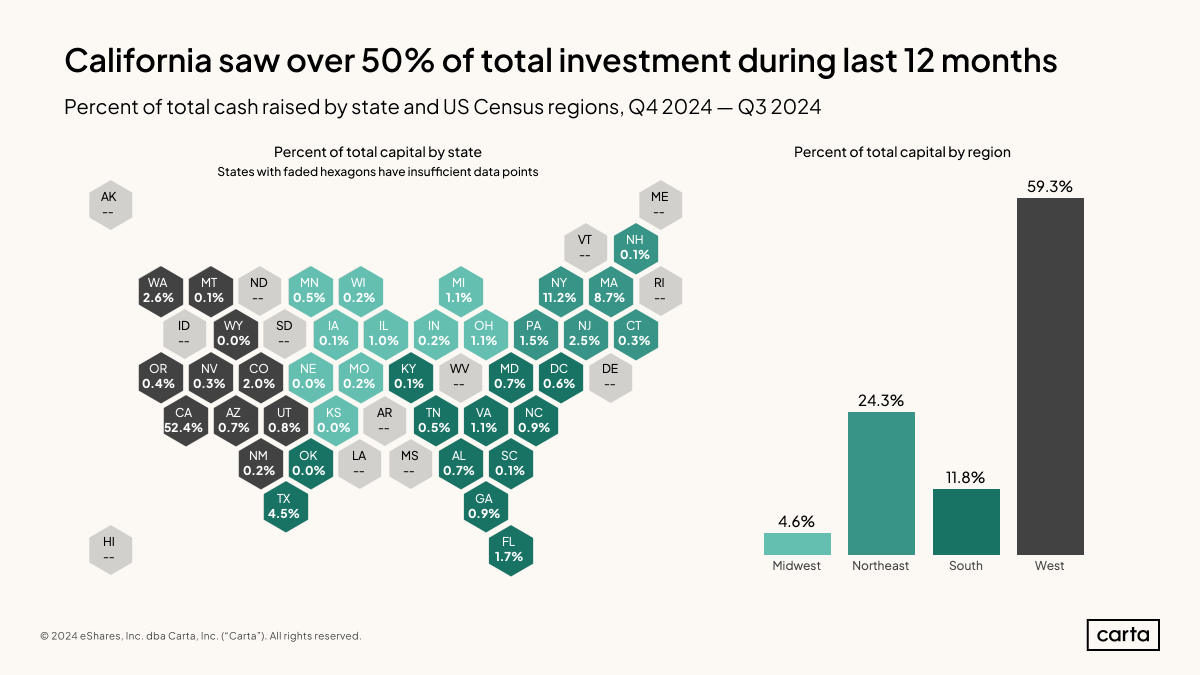

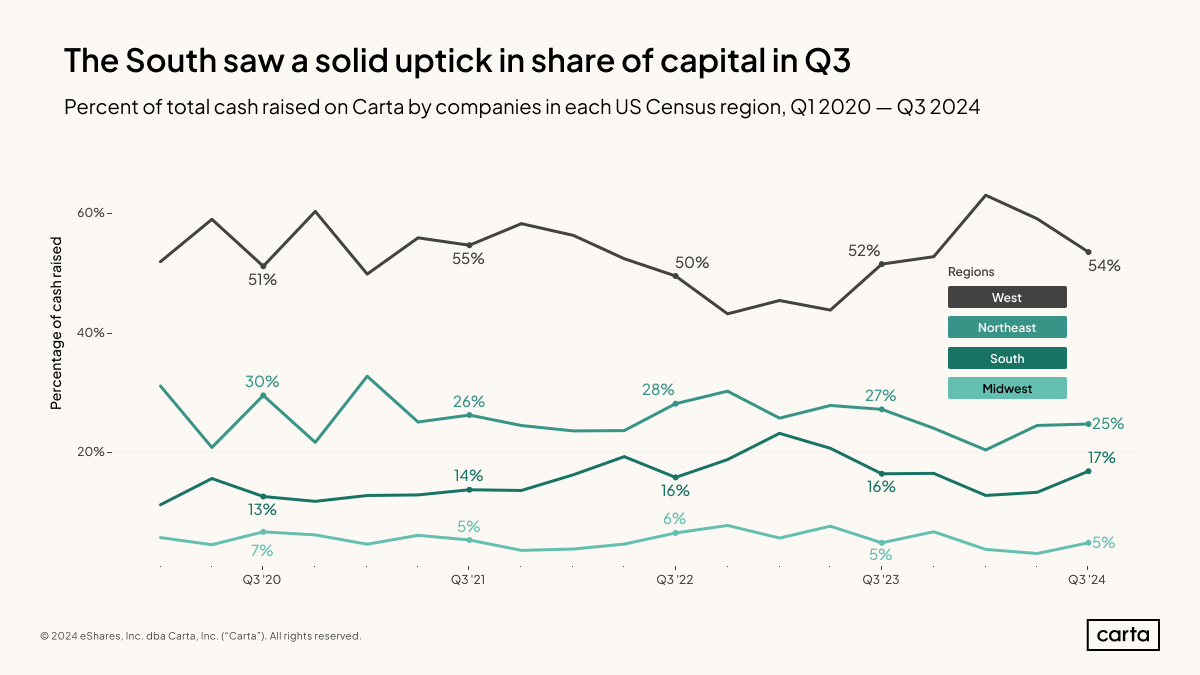

Startups based in California were responsible for more than half of all venture capital raised on Carta over the past 12 months. At 52%, California’s share of all VC raised is nearly five times bigger than the next-busiest state (New York, at about 11%).

Seven different states claim at least 2% of all venture dollars raised in the past 12 months. Three of those states are in the West census region: California, Washington, and Colorado. Three more are in the Northeast: New York, Massachusetts, and New Jersey. That leaves Texas as the only state from either the South or the Midwest that cracks a 2% market share.

Startups from the West have now raised at least 50% of all venture capital on Carta in five consecutive quarters. The region’s share has declined the past two quarters, however, falling from 63% in Q1 2024 to 54% in Q3.

The South regained a notable slice of activity in Q3, as its proportion of all dollars raised climbed to 17%. Previously, the South’s share of the market had been declining steadily for a year and a half. Both the Northeast and Midwest have also gained some ground in the past two quarters.

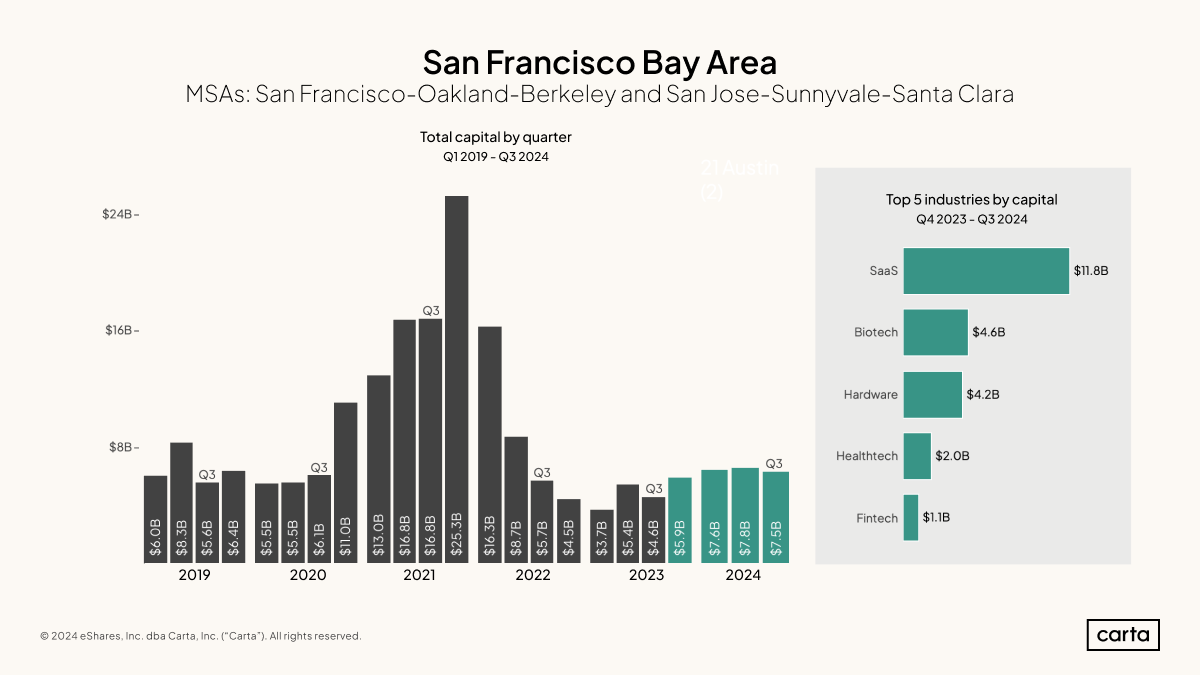

The Bay Area has heated back up in 2024, with startups raising somewhere between $7.5 billion and $7.8 billion in new capital each of the past three quarters. This new normal is significantly higher than the sorts of fundraising totals the region had seen in the previous six quarters.

Bay Area startups in the SaaS industry raised about $11.8 billion over the past 12 months, or about 40% of the regional total. Combined, the SaaS, pharma/biotech, and hardware industries are responsible for more than 70% of all venture dollars raised in the Bay Area.

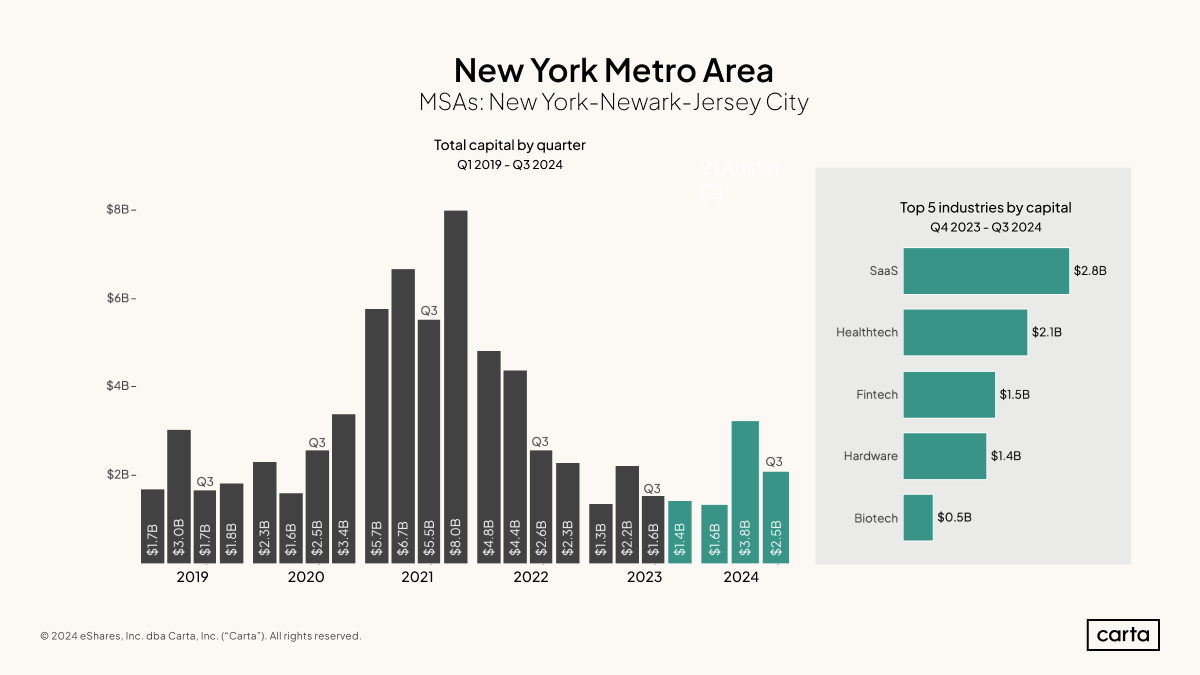

The SaaS industry is also the most popular sector for startup fundraising in the New York metro area, but by a much smaller margin than in the Bay Area. Healthtech, fintech, and hardware are all hot on software’s heels.

The past six months have been strong ones for venture fundraising in and around the Big Apple. The region has now topped $2.5 billion in total capital raised in two straight quarters after falling below $2.5 billion in the previous six quarters.

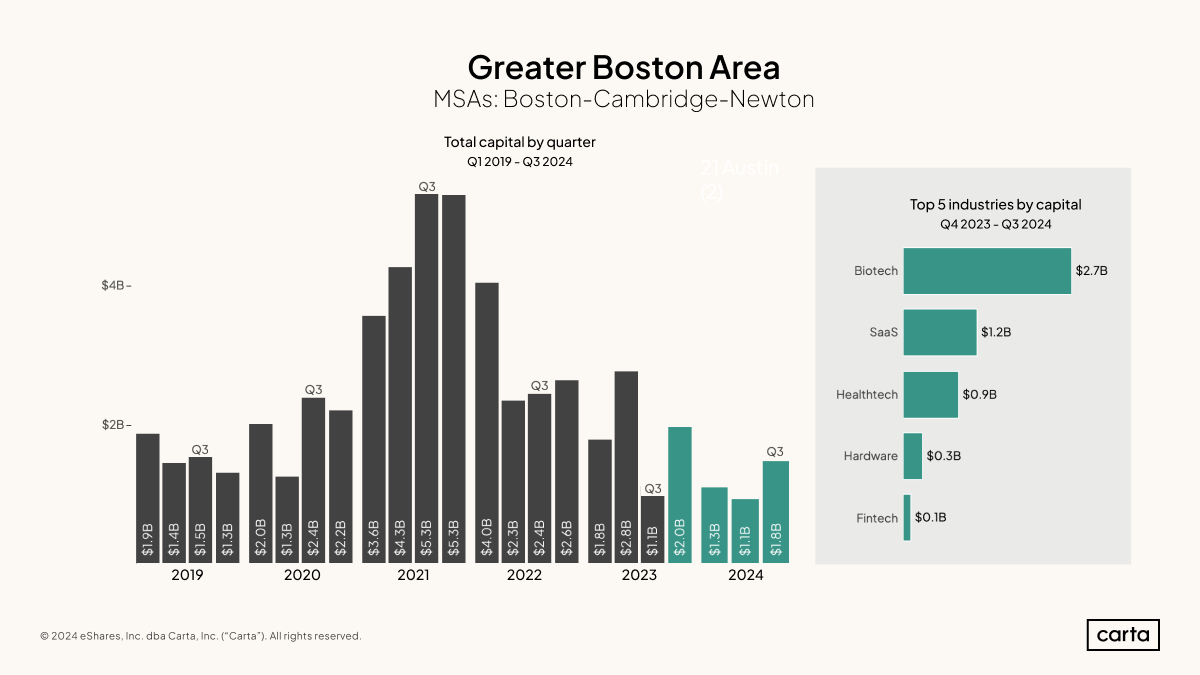

Startups in the Boston metro area raised $4.2 billion in funding in Q3, trailing only the Bay Area among U.S. metros. That represents a healthy 56% year-over-year increase, but it’s a slight decrease from Q2, when Boston startups brought in $4.9 billion.

Boston still lives up to its reputation as a hotspot for the healthcare and medical fields. Boston-area startups in pharma/biotech and healthtech combined to raise about $6.2 billion over the past 12 months, about 40% of the regional total across all industries.

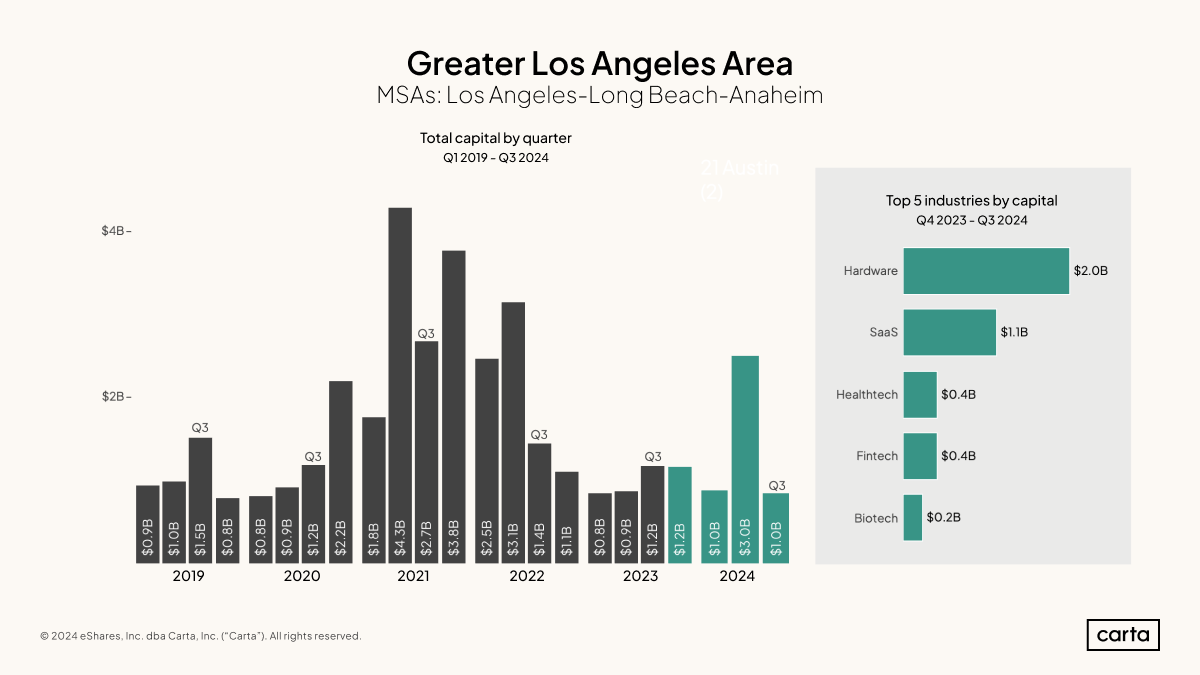

Los Angeles is the only one of the five metro areas included in this report where SaaS is not the most popular sector for venture funding. Instead, hardware takes the top spot, with $2 billion in venture dollars raised over the past 12 months—nearly a third of all fundraising.

In Q2, Los Angeles startups closed about $3 billion worth of new investments, a sum that wouldn’t have been out of place during the height of the pandemic bull market. Besides that outlier, much of the past two years in the region have looked fairly similar, with somewhere between $800 million and $1.2 billion in cash raised in six of the past seven quarters.

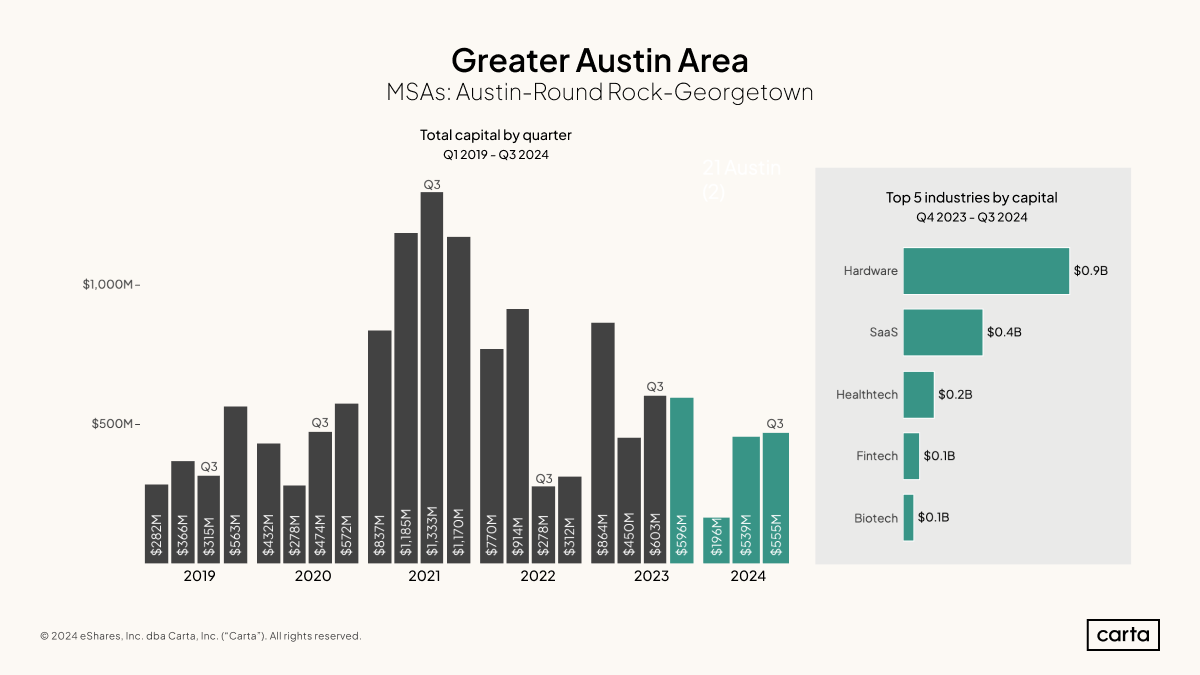

Startups headquartered in Austin and the surrounding environs have now combined to raise $1.1 billion in consecutive quarters. Funding in the metro area fell to a new decade lowpoint back in Q1, but since then, the market has bounced back.

Over the past 12 months, venture fundraising activity in Austin has largely been dominated by two industries. Besides SaaS and hardware, no other sector claims more than 5% of the region’s total capital raised.

Get industry-specific data

Download the addendum to this quarter's report to get industry-specific data on fundraising and valuations:

Methodology

Carta helps more than 45,000 primarily venture-backed companies and 2,400,000 security holders manage over $3.0 trillion in equity. We share insights from this unmatched dataset about the private markets and venture ecosystem to help founders, employees, and investors make informed decisions and understand market conditions.

Overview

This study uses an aggregated and anonymized sample of Carta customer data. Companies that have contractually requested that we not use their data in anonymized and aggregated studies are not included in this analysis.

The data presented in this private markets report represents a snapshot as of October 31, 2024. Historical data may change in future studies because there is typically an administrative lag between the time a transaction took place and when it is recorded in Carta. In addition, new companies signing up for Carta’s services will increase historical data available for the report.

Financings

Financings include equity deals raised in USD by U.S.-based corporations. The financing “series” (e.g. Series A) is taken from the share class name in their applicable certificate or articles of incorporation. Financing rounds that don’t follow this standard are not included in any data shown by series but are included in data not shown by series. Primary rounds are defined as the first equity round within a series. Bridge rounds are defined as any round raised after the first round in a given series.

In some cases, convertible notes are raised and converted at various discounted prices within a series (e.g. Series A-1, Series A-2, Series A-3). In these cases, converted securities are not included in cash raised, and only the post-money valuation of the new money is included.