- Vesting: A guide to schedules, cliffs, and acceleration

- What is vesting?

- What does "fully vested" mean?

- Vesting for stock options

- Vesting for RSUs

- Vesting for retirement plan contributions

- How does vesting work?

- What is a vesting schedule?

- Time-based vesting

- Milestone-based vesting

- Hybrid vesting

- Accelerated vesting

- Vesting schedule example

- Why is vesting a founder's best friend?

- How should you structure vesting for your startup?

- For co-founders

- For employees and advisors

- What happens to equity when someone leaves?

- How to manage vesting schedules without the chaos

- Get your vesting right from day one

- Frequently asked questions about vesting

When you grant equity to an employee as part of their compensation package, you are offering partial ownership of the company. In most cases, their stock has to vest first, which means they typically need to work for the company for a period of time before they become an owner.

What is vesting?

Vesting is the process of earning full ownership of an asset over a set period of time. That asset can be equity, such as stock options and shares, or it can be employer contributions to a retirement plan like a 401(k). For startups, vesting almost always refers to equity: You earn full ownership of your grant by staying with the company as it grows.

Vesting has long been the standard for granting equity to founders, employees, and advisors, and companies use it to encourage people to stay longer. As those companies grow, so does their commitment to employee ownership. The median seed-stage startup has an employee stock option pool of around 13.5% of fully diluted shares, with that proportion rising to around 17.2% for the median Series D company.

The most common types of equity awards that use vesting are stock options and restricted stock awards (RSA). Both grant ownership that vests over time, but they have different rules and tax implications. Unless your company allows early exercising, you can only exercise stock options that have vested.

This video explains how vesting works for stocks and options.

What does "fully vested" mean?

When you are fully vested, you own 100% of a grant outright, and no future work is required to keep it. "Vested" describes what you have already earned. "Unvested" is what you have not earned yet and could forfeit if you leave. So if you have a 1,000-share grant and half of it has vested, you own 500 vested shares free and clear, while the other 500 remain unvested until more time passes on your schedule.

Vesting for stock options

When you grant stock options, like incentive stock options (ISOs) or non-qualified stock options (NSOs), employees are not yet getting actual shares of stock. Instead, they get the right to buy a set number of shares at a fixed price later on.

Vesting for RSUs

If you grant restricted stock units (RSUs), you are giving actual shares of stock that recipients can sell in the future. Grantees may have to stay at the company for a certain amount of time, and sometimes the holder or the company must also hit a stated milestone (like an initial public offering (IPO), for example) for RSUs to vest. But unlike stock options, they don't need to purchase them to own them.

Vesting for retirement plan contributions

For retirement plans like 401(k) plans and pension plans, employee contributions are always 100% vested, while employer contributions follow the vesting schedule set by the employee benefits plan. Sometimes, employees own these employer-matched contributions right away (immediate vesting), but often they have to work at the company for a certain number of years to fully vest.

How does vesting work?

The specific rules for earning equity are laid out in a formal document, usually called a Stock Option Grant Notice or Restricted Stock Award Agreement. This agreement details the total number of shares or options granted, which must comply with regulations like Rule 701, and the timeline over which the recipient will earn them. This timeline is known as the vesting schedule.

What is a vesting schedule?

A vesting schedule is a timeline that determines when an employee gains full ownership of their equity. It is typically detailed in the option grant (for example, 1,000 options over four years). There are three common types of vesting schedules: time-based, milestone-based, and a hybrid of the two.

For startups, vesting is almost always based on how long someone works at the company, which is called time-based vesting. Milestone-based vesting that ties to specific performance goals shows up in certain corners of the private markets, but it's far less prevalent for early-stage companies. According to Carta’s PE Executive Equity Report, nearly 61% of initial management grants at private equity (PE)-backed LLCs are tied to a specific performance metric. Even so, the standard for venture capital (VC)-backed corporations remains overwhelmingly time-based, usually a four-year grant with a one-year cliff.

If you are joining a company, review your vesting schedule before you accept an offer. The grant date, schedule length, and cliff size all determine how much equity you keep.

Time-based vesting

Time-based stock vesting is when you earn options or shares over a specified period of time. The two most common types of time-based vesting schedules are:

Graded vesting: You earn your equity in small increments over time, such as monthly or quarterly. This is the most common schedule at startups.

Cliff vesting: A waiting period passes before you earn your first portion of equity. After this initial cliff, the rest of your equity may begin to vest on a graded schedule.

Immediate vesting: You own the full grant right away, with no waiting period. It is rare for startup equity but common for some employer retirement contributions.

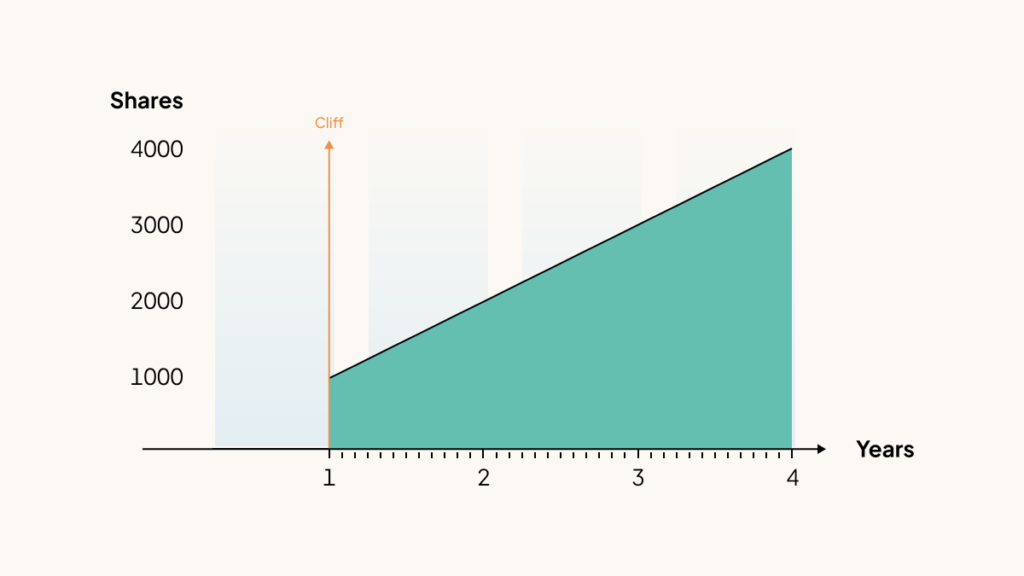

Here is how a five-year graded schedule works in practice. Say you receive 1,000 shares that vest 20% per year with no cliff. You earn 200 shares after year one, another 200 after year two, and so on, until all 1,000 shares are fully vested at the end of year five. Startups more often use a four-year version with a one-year cliff, covered below.

Most time-based vesting schedules have a vesting cliff to motivate employees to stay for at least a year. If you leave before the one-year mark, any unvested options are put back into the employee option pool.

Cliff vesting

A vesting cliff is an initial waiting period before any equity vests, which is typically one year in the startup world. This protects the company from granting ownership to someone who doesn't stay long enough to make a meaningful contribution.

Under a standard four-year time-based vesting schedule with a one-year cliff, 1/4 of your shares vest after one year. After the cliff, 1/36 of the remaining granted shares (or 1/48 of the original grant) vest each month until the four-year vesting period is over. After four years, you are fully vested.

Keep in mind each option grant has its own vesting schedule. Vesting isn't necessarily based on their overall tenure at the company. For example, if you received one grant with a four-year vesting schedule in 2025 and a second grant with a four-year vesting schedule from the same company in 2027, you wouldn't fully vest all of the options from both grants until 2031.

Milestone-based vesting

Milestone vesting is when you earn your options or shares after a specific milestone. Beyond an IPO, milestones could be completing a project, reaching a business goal, or hitting a certain valuation. Milestone-based vesting isn't as common as time-based vesting.

Hybrid vesting

Hybrid vesting is a combination of time-based and milestone vesting. To receive equity, you must both meet a time requirement and hit one or more milestones.

Accelerated vesting

Acceleration is a clause in the grant agreement that can speed up the vesting schedule if a specific event occurs. The most common event that triggers acceleration is an acquisition, and it can be a significant benefit for employees whether a company is sold or goes public.

There are two main types of acceleration triggers.

Trigger type | What it is | When it happens |

Single-trigger | All unvested equity vests at once | After a single event, which is almost always an acquisition |

Double-trigger | Vesting accelerates only if two events happen | Requires an acquisition (the first trigger) and the employee being terminated without cause (the second trigger) |

Double-trigger acceleration is more common because it protects the acquiring company from having employees leave immediately after the deal closes.

Vesting schedule example

Meetly, Inc. (a hypothetical company) hired Blake on January 1, 2026. As part of the compensation package, Meetly gave Blake an option grant with the following details:

Grant date: 1/1/2026

Options granted: 192

Vesting schedule: Time-based; monthly for four years with a one-year cliff

One year after Blake's hire date, on January 1, 2027, she reached the vesting cliff and 1/4 of the shares (48 shares) vested. At that time, Blake could have exercised those 48 shares (though she wasn't obligated to).

Date | Options vested | Cumulative |

1/1/2027 | 48 | 48 (192/4 = 48) |

2/1/2027 | 4 | 52 |

3/1/2027 | 4 | 56 |

4/1/2027 | 4 | 60 |

5/1/2027 | 4 | 64 |

6/1/2027 | 4 | 68 |

7/1/2027 | 4 | 71 |

8/1/2027 | 4 | 76 |

9/1/2027 | 4 | 80 |

Over the next three years, an additional four shares vest every month. By January 1, 2030, Blake's options will be completely vested, and she can exercise all 192 of the shares in the option grant if she chooses.

Date | Options vested | Cumulative |

1/1/2027 | 48 | 48 (192/4 = 48) |

1/1/2028 | 48 | 96 |

1/1/2029 | 48 | 144 |

1/1/2030 | 48 | 192 |

If Blake leaves the company before January 1, 2030, she will surrender all unvested shares, which will be returned to the company's option pool.

Why is vesting a founder's best friend?

For founders, vesting isn't a formality. It helps you build a committed team and maintain a clean, investor-ready cap table. There are two main benefits of vesting for a founder:

Aligning incentives: Vesting ensures co-founders, employees, and advisors are all motivated to stay with the company and contribute to its long-term success.

Protecting your cap table: Imagine a co-founder leaves after a few months but keeps a large portion of the company's equity. A vesting schedule prevents this by making sure early leavers only walk away with the small amount of equity they have earned, if any.

How should you structure vesting for your startup?

For VC-backed and bootstrapped corporations, the most common setup for equity grants is a four-year vesting schedule with a one-year cliff. This structure applies to both founders and early employees. While not every grant includes a cliff, data shows about half of management grants have a cliff, and that figure rises to nearly 70% for employees. When a cliff is used, it's almost always for one year; in fact, the vast majority of cliffs (at least 95%) are set at the one-year mark.

For co-founders

It can feel awkward to put vesting schedules on your co-founders. However, it's a professional standard that protects everyone involved if one founder decides to leave the venture for any reason. Without it, a departing co-founder could walk away with a significant piece of the company they are no longer helping to build.

The industry standard for founders is a four-year vesting period with a one-year cliff. Investors expect to see this structure, and having it in place shows your company is built to last.

For employees and advisors

The market standard for early employees is also a four-year vesting schedule with a one-year cliff. Using this standard helps you compete for talent and signals you run a well-organized company. Some companies are exploring more creative vesting schedules to attract and retain talent. However, for early-stage companies, sticking to the standard is often the simplest and most effective approach. As noted during Carta's Startup Compensation in 2024 webinar, longer vesting schedules can sometimes be more employee-friendly by locking in a low strike price for a larger grant, essentially building in an equity refresh from the start.

Advisory shares often have shorter vesting periods, such as two years, aligning with the typical length of an advisor engagement.

What happens to equity when someone leaves?

Vesting also defines what happens to vested stock and unvested equity when an employee leaves the company. Any unvested equity is returned to the company's option pool, so it can be granted to future hires. This recycling of equity is a key mechanism for continuing to attract new talent as your company grows.

For the equity that has already vested, the former employee has a limited window for exercising stock options. While a 90-day post-termination exercise period (PTEP) has historically been common, many companies now offer longer periods as an employee-friendly benefit.

How to manage vesting schedules without the chaos

When you're just starting out, tracking a few vesting schedules in a spreadsheet might seem manageable. But as your team grows, each with their own grant date, cliff, and schedule, that spreadsheet quickly becomes a source of risk. A single formula error or an outdated version can lead to massive headaches and costly legal fees to clean up the cap table.

As your company grows beyond a few grants, you'll need more than a spreadsheet to track ownership, manage equity plans, and stay audit-ready. To help you build a scalable system for equity management, this section covers the tools and services that support founders at every stage of growth.

Get your vesting right from day one

Getting equity management right from the start builds trust with investors and your team. A clean cap table with standard vesting terms tells future investors your company is well-run and worth backing.

Carta helps founders look professional from the start. With Carta Launch, our free plan for early-stage companies, you can set up your cap table and issue your first equity grants with proper vesting schedules at no cost. It's built for founders who want to get equity management right without paying for infrastructure they don't yet need.

Request a demo to see how Carta's platform can support your company as it grows.

Frequently asked questions about vesting

What does a four-year vesting schedule mean?

A four-year vesting schedule means an employee earns their full equity grant over a four-year period. It often includes a one-year cliff, meaning no shares vest until the first anniversary, after which shares typically begin to vest monthly.

Can a vesting schedule be changed?

Once an equity grant is approved by the board and accepted by the recipient, the vesting schedule is legally binding, and any amendments must comply with IRC regulations.

What is the difference between vesting and exercising?

Vesting is the process of earning the right to buy your shares over time, which will have a strike price based on the fair market value of the stock at the time of the grant. Exercising is the separate action of actually purchasing those shares at the predetermined strike price.

What happens to my unvested shares if I leave?

Any unvested shares go back to the company's option pool for future hires. Depending on your plan, you keep only what has already vested, and you usually have a limited window to exercise vested options after you leave.

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. ©2026 Carta. All rights reserved. Reproduction prohibited.