- Restricted stock units (RSU)

- What is a restricted stock unit?

- RSUs vs. options

- How do RSUs work?

- RSU vesting and conditions

- Single trigger vs. double trigger RSUs

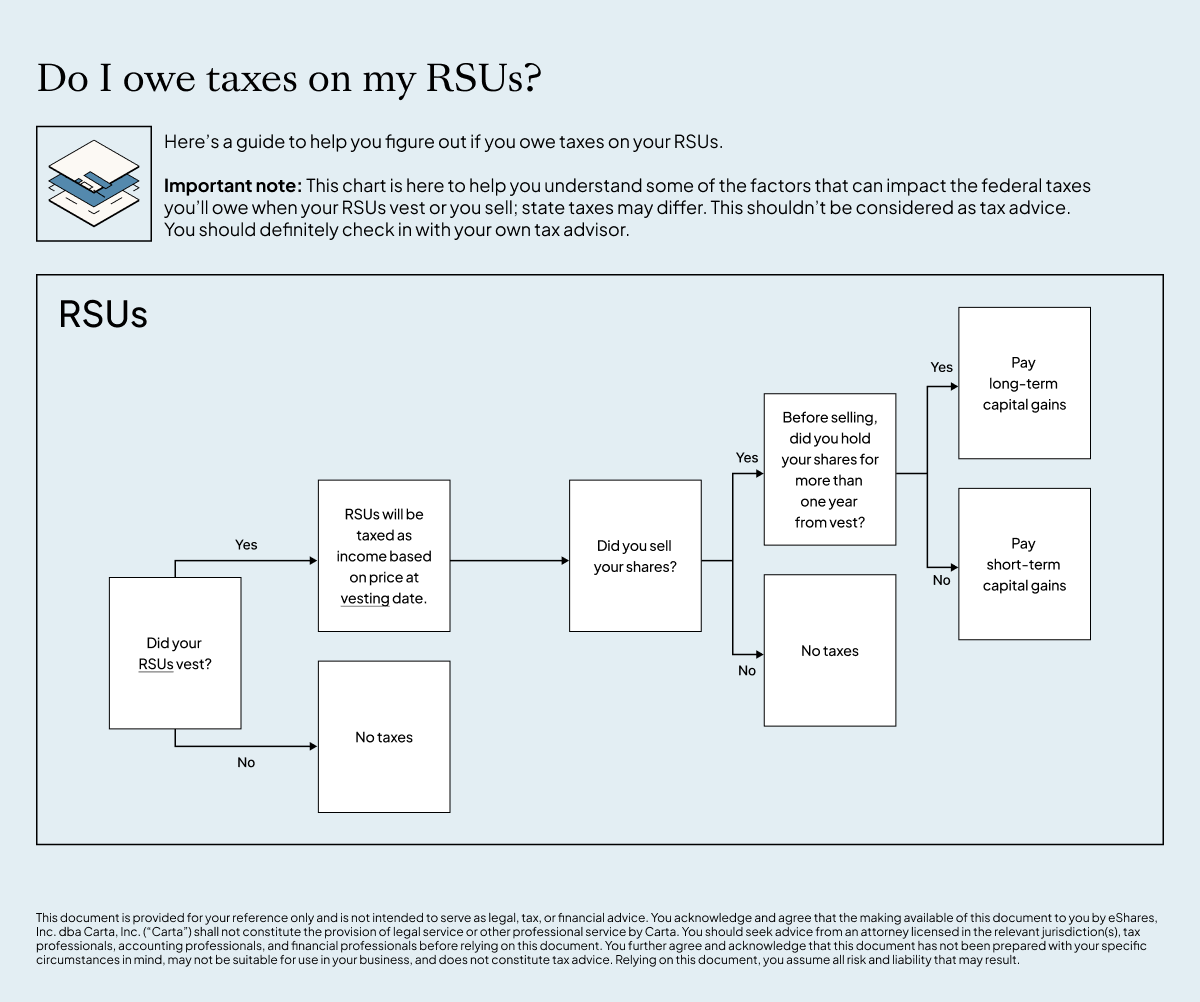

- How are RSUs taxed?

- RSU tax rate

- Sell-to-cover

- Capital gains tax

- RSU tax implications

- When can I sell my RSUs?

- Public company RSUs

- Private company RSUs

- What happens to RSUs when I leave a company?

- More questions about RSUs?

What is a restricted stock unit?

A restricted stock unit (RSU) is a form of equity compensation that companies issue to employees and other service providers. An RSU is a promise from your employer to grant you shares of the company’s stock (or the cash equivalent) on a future date—if certain restrictions are met. The process of meeting these restrictions is called vesting.

RSU grants are an alternative to stock options (like ISOs or NSOs), which give employees the chance to buy company stock at a set price. With RSUs, you don’t have to pay anything to get the stock. Instead, you are usually only responsible for paying the applicable taxes when you receive your shares. Unlike with restricted stock awards (RSA), you won’t acquire the shares underlying the RSUs until they vest.

→ Learn more about the differences between RSAs and RSUs

You typically don’t get to choose which type of stock award you receive; instead, what you receive depends on your role and the size, stage, and preferences of your company. RSUs are more commonly issued by larger, later-stage companies.

RSUs vs. options

Want to know more about the differences between RSUs and stock options? Read our guide or download the free calculator below to compare the possible payout from an option grant vs. RSU grant.

How do RSUs work?

In order for you to receive your RSUs, you have to meet the vesting conditions outlined in your RSU agreement.

RSU vesting and conditions

Vesting conditions within your RSU agreement may include any of the following:

Time-based (e.g., you must stay at the company for a certain amount of time)

Milestone-based (e.g., your company must IPO or be acquired, or you have to complete a performance milestone or project)

A combination of the two

After a RSU is vested, it must be settled. Settlement is the actual conversion of the RSU into shares. Sometimes, vesting and settlement occur at the same time. Other times, the settlement date is distinct, often for administrative purposes (for example a company may decide that all RSUs that have vested during a quarter settle on the same day).

Single trigger vs. double trigger RSUs

Private companies have two options to help their employees cover taxes for their RSU awards: single-trigger or double-trigger. The main difference between the two is that single-trigger RSUs only have one type of vesting condition, whereas double-trigger RSUs have two types (usually both time-based and milestone-based).

→ Learn more about single-trigger vs. double-trigger RSUs

How are RSUs taxed?

With RSUs, you usually have to pay ordinary income tax on the fair market value (FMV) of the shares when you acquire them, which is when they settle. This differs from how stock options are taxed. With ISOs, you sometimes don’t pay taxes until you sell your shares. With NSOs, you could pay taxes both when you purchase and sell your shares and taxes may not be due if the sale price is less than the purchase price.

RSU tax rate

Your RSU shares are initially taxed as supplemental income. Employers are required to withhold 22% for federal income taxes on the first $1 million in supplemental income for employees, and 37% of any amount exceeding $1 million.

You may end up owing more in income tax on your shares depending on your effective tax rate: If it’s higher than 22% for the year you vest your shares, you’ll owe more than your employer has withheld. In addition, you’ll owe Social Security, Medicare, and state income taxes on your shares.

Sell-to-cover

Your company may allow you to sell a portion of your vested shares to cover the tax obligation your employer must withhold, a strategy called “sell-to-cover.” Often, you’ll then need to hold the remaining shares. Sometimes, you can choose whether to hold the remaining shares or sell them right away.

Capital gains tax

When you sell RSUs, you may also need to pay capital gains tax on the spread. The spread is the increase between the cost basis (the FMV of the shares when you received them) and the sale price. How long you hold the shares usually determines whether you will pay short-term or long-term capital gains tax. If you sell right after your shares vest, you probably won’t experience a gain and may not have to pay additional tax.

RSU tax implications

Action | Tax implication |

Your company gives you an RSU grant. | No immediate tax implication. |

Your RSUs vest and are settled. | You’ll owe ordinary income tax on the FMV of your shares at the time of settlement. |

Your RSUs are settled and you sell the shares immediately at the FMV. | You’ll owe ordinary income tax on the FMV of the shares you acquired and no capital gains tax on the sale of the shares (because the sale price was the same as your tax basis). |

You sell your shares within one year of receiving them. | If you sell at a price higher than the FMV of your shares at vesting, you’ll also likely owe short-term capital gains tax on the difference. |

You sell your shares after holding them for more than a year. | If you sell at a price higher than the FMV of your shares at vesting, you’ll also likely owe long-term capital gains tax on the difference. |

When can I sell my RSUs?

Depending on your own financial situation or your confidence in your company’s future success, you may consider selling your RSUs to access immediate liquidity. When thinking about whether to sell your RSUs, consider things like:

Your company’s trading policy: Not all companies allow you to sell RSUs, or if they do, they may have restrictions around when or how to sell

How you think the stock will perform in the future: If you believe in your company’s future success, it might make sense to hold onto your RSUs for longer so the stock can appreciate more before you sell.

Your cash-flow needs: If you need immediate cash, selling your stock can be a great way to access liquidity.

How much you’ll be taxed: You’ll need to hold your RSUs for more than a year to qualify for lower long-term capital gains tax rates. If you haven’t held your stock for a year, you may want to consider holding onto it for longer.

How diverse you want your portfolio to be: Owning stock in a single company can be higher risk. If you want to diversify your investment portfolio, you may consider selling some of your RSUs in order to make other investments.

Public company RSUs

If your company is public, you can usually sell the shares you receive from your RSUs as soon as you meet the vesting criteria and receive your shares, as long as you comply with your company’s trading policy (e.g., with some companies, you’re only allowed to trade stock during certain times of the year).

Private company RSUs

If your company is private, you’ll need to wait for a liquidity event (like an acquisition, IPO, or company-led secondary transaction, such as a tender offer, to sell your shares). Or, if your company approves the transaction, you can find a third-party buyer to buy your shares.

What happens to RSUs when I leave a company?

Most times, if you leave your company, you’ll get to keep your fully vested shares. You’ll likely lose any shares that aren’t time vested. Generally, this is the same whether you leave a company voluntarily or are laid off.

Generally, if your RSUs are time-vested, but not settled at the time you leave, you will still receive them whenever they settle in the future. But some companies with double-trigger RSUs have a “must be present to win” condition in the employee’s RSU award, which restricts the second trigger to only current employees at the time of the exit event. An employee who leaves the company before the exit event takes place will lose all of the equity in their compensation package.

In addition, it’s possible for your time-vested shares to expire before they “fully” vest (by meeting the milestone-based conditions of the second trigger, such as a liquidation event). Your RSU agreement should indicate if and when unvested double-trigger RSUs will expire.

More questions about RSUs?

Carta offers equity advisory services to employees of participating companies. Founders and leadership teams that want to help employees make informed decisions about their equity ownership can reach out for a demo.

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. ©2026 Carta. All rights reserved. Reproduction prohibited.