When venture fund managers want to demonstrate how an active vehicle is performing, one of the most common tools they use is TVPI.

Short for total value to paid-in capital, TVPI is a metric that measures the current estimated value of a fund’s holdings in relation to the amount of capital contributed to the fund by its limited partners (LPs). A TVPI of 2x means that a fund’s estimated value is twice as high as the amount of capital that its investors put in. A TVPI of 1x means the fund has not increased the value of its LPs’ initial capital at all.

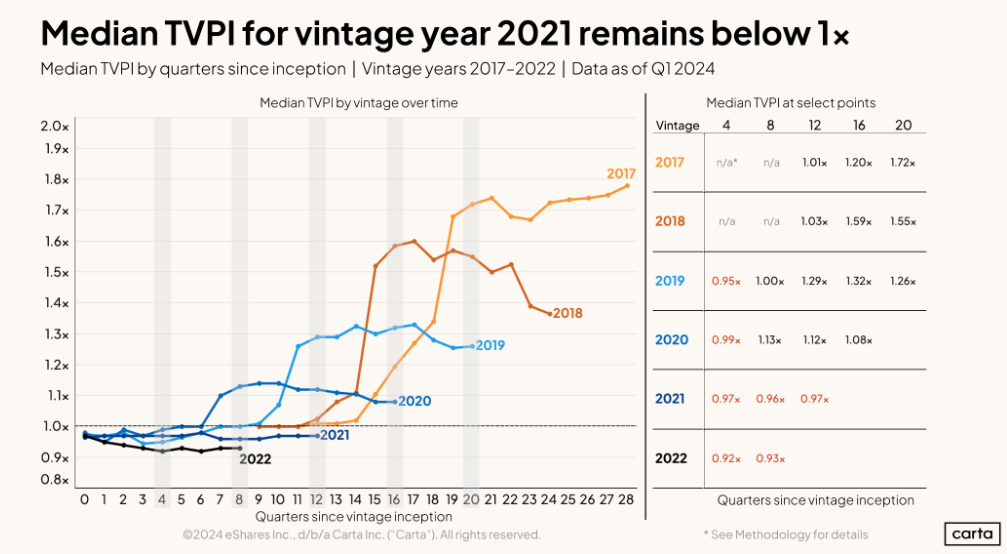

By this measure, last year was a challenging one for some of the most recent vintages of venture capital funds. As of Q1 2024, median TVPI for each of the 2018, 2019, and 2020 vintages had declined over the four most recent quarters (see left side of below chart). The dip was most significant for 2018 funds, where the median TVPI fell from 1.55x to 1.37x. That’s a decline in total fund value of more than 11%.

Another recent fund vintage, however, managed to avoid last year’s damage. The below chart shows that median TVPI among 2017 funds actually increased during the four most recent quarters, rising from 1.73x to 1.78x.

Funds from 2017 are older than other recent vintages, and have thus had more time to realize gains, which can improve current metrics. But the trend remains even if we take this difference in time into account. For instance, as you can see on the right side of the above chart, the median TVPI for 2017 funds was much higher at 20 months after inception than it was for 2018 or 2019 funds at the same point.

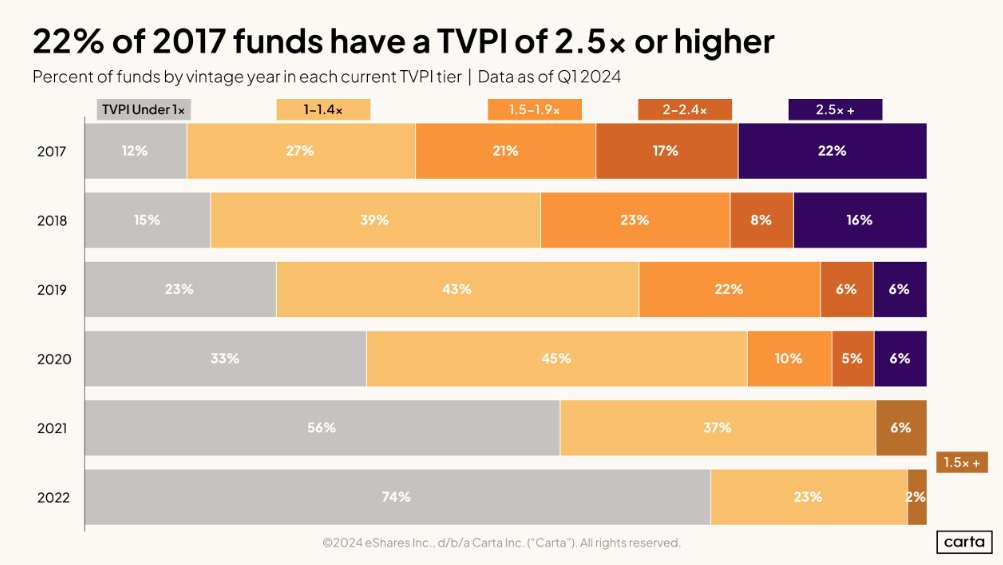

As of the end of Q1 2024, about 39% of all 2017 funds on Carta had a TVPI of 2x or higher, compared to 24% of 2018 funds and just 12% of 2019 funds. And a mere 12% of funds from 2017 had a TVPI lower than 1x. For more recent vintages, the picture isn’t quite so rosy.

The calculus of TVPI

While TVPI is one popular way to track fund performance, it’s not the only way. And it comes with certain limitations.

To calculate TVPI, fund managers use a mix of realized and unrealized gains. If the fund has already exited a portfolio company, then the gains on that particular investment are easy to measure: Just divide the realized return by the initial amount of capital paid in.

But if a fund still holds a company in its portfolio, calculating the value of potential unrealized gains is much trickier. To do so, fund managers typically mark the value of the company against the known valuation of other comparable companies in the market. The valuations of a company’s closest peers, the thinking goes, are probably a good proxy for valuing the company itself.

But fund managers use a different methodologies for marking the values of their portfolio companies. There is no widely accepted industry standard. And no matter how accurate these marks are, they remain estimates and projections. A private company’s value will almost certainly change between any private mark and its ultimate exit. Accurately marking the value of private startups has grown even murkier in recent years, when valuations have seesawed across much of the tech landscape.

For LPs, knowing an active fund’s latest TVPI is certainly useful context. But it’s far from the only context required.

“With TVPI, a big question for LPs is, what are individual companies marked at?” says Stephanie Choo, a partner at fintech investor Portage who runs the firm’s early-stage team in North America. “Because it’s very hard to know how and when things will eventually exit.”

Marks have grown more uncertain

TVPI for more recent fund vintages can be heavily reliant on unrealized marks. And over the past few years, investors say that determining accurate marks for active portfolio companies has grown more difficult than ever.

If a startup raised capital in recent months, determining a fair valuation is often fairly easy: Just use the valuation that was assigned to the company during its fundraising. If it’s been a while since a startup last raised, then its owners will likely look to recent funding events from similar private companies as a comparison, or to valuations for peer companies that are publicly traded.

Over the past two years, however, the number of venture funding events taking place has steeply declined. Startups are waiting longer than ever between raising new rounds. And something of a dislocation has occurred between public and private markets, with stock indexes soaring to record highs while venture-backed valuations still struggle to recover from recent falloffs.

For fund managers—and for their LPs—all this upheaval has made the process of marking portfolio company valuations more uncertain.

“If the last round that a company raised was in 2021, how do you value that company?” Choo says. “You’d expect to have already seen some markdowns on these companies in 2022 and 2023. But some of these companies could have also potentially grown into their previous valuations.”

How VCs are approaching marks

As part of his work as the managing partner at early-stage fintech firm Fiat Ventures, Marcos Fernandez regularly reports back on fund performance to his LPs. He thinks the purpose of those reports is twofold: To keep those LPs informed, and to maintain strong investor relations.

In his view, the best way to achieve both those goals is to be conservative when it comes to estimating portfolio company valuations—and, whenever possible, to focus on realized gains.

“In this market, sometimes you’ll see these crazy markups where MOICs (Multiple on Invested Capital) and TVPIs are high. But they don’t necessarily realize those gains,” Fernandez says. “Nothing is done until there are distributions.”

Choo agrees. While it might be tempting in the short term to err on the side of marking their investments too optimistically, that sort of philosophy might ultimately backfire.

“If you’re in it for the long game, you ought to be conservative on markups and conservative on markdowns,” Choo says. “Your LPs will question your credibility if you’re trying to mark things up in a way that’s too aggressive.”

Fernandez and Choo agree on another point, too: While a conservative approach can help, there’s no inherently correct way for a fund manager to mark the value of their active investments. Different metrics and different tools can have different uses.

The most important thing is transparency. No matter how you decide to go about valuing your companies, make sure it’s consistent—and make sure all of your LPs are on the same page.

“There are a bunch of tools you can use to assess the true value of a company,” Fernandez says. “It’s really up to the individual fund managers to decide on their approach and indicate that to LPs.”

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. ©2026 Carta. All rights reserved. Reproduction prohibited.