What is MOIC?

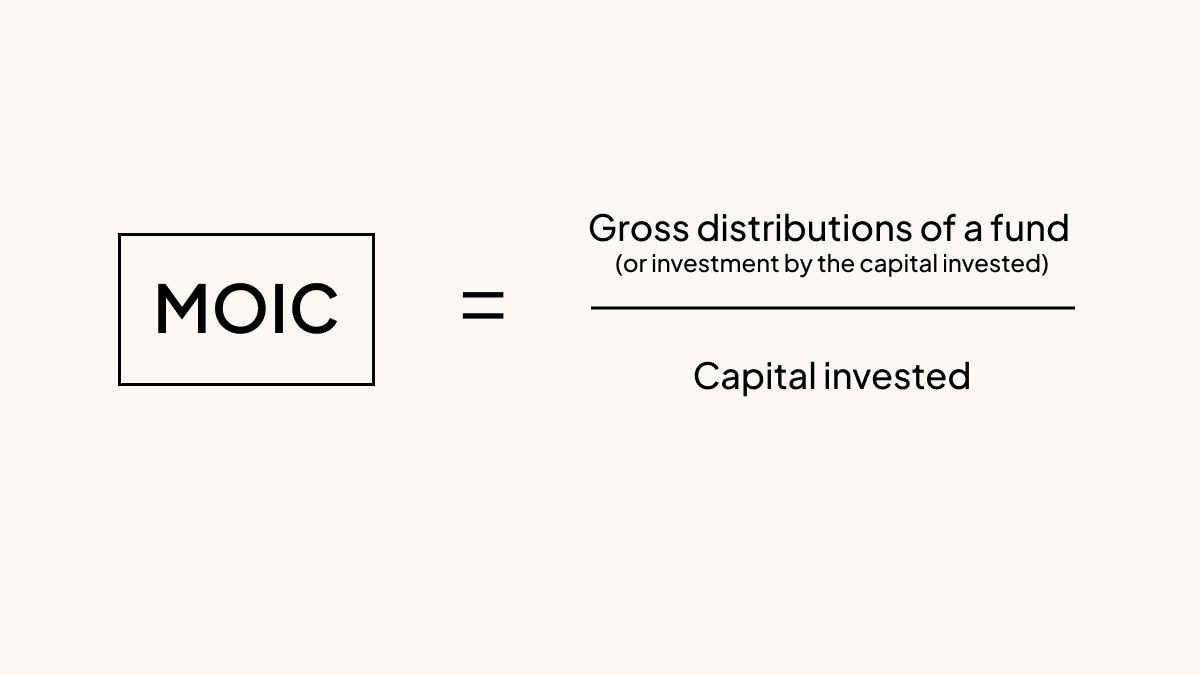

Multiple on invested capital (MOIC) is a financial metric that measures the returns of an investment relative to the amount of capital initially invested. MOIC is calculated by dividing the gross distributions of a fund or investment by the capital invested.

MOIC is one of the most commonly used metrics that private fund managers of venture capital funds, private equity funds, and hedge funds use to report the performance of their investments. Investors use MOIC to evaluate the relative success of individual investments, as well as the performance of entire funds.

How to calculate MOIC

The formula for MOIC is very simple: Divide the gross distributions of a fund or investment by the capital invested and you have the multiple on invested capital.

Distributions

The numerator in the formula for MOIC represents the distributions that have resulted from the investment or fund under consideration. These are capital gains that derive from interest, dividends, or the liquidation of investment holdings through an initial public offering (IPO), M&A transaction, or secondary sale of equity stakes in a portfolio company.

MOIC is always a gross metric, meaning that distributions are considered without subtracting any associated fees the fund manager may charge for its advisory services.

Invested capital

The denominator in the formula to calculate MOIC is invested capital: For individual investments, this is the total amount of capital fund invested in that particular investment. For the fund, it’s the total capital paid into the fund to date. In both cases, MOIC includes any reinvested capital.

How to interpret MOIC

MOIC is typically expressed as a multiple, such as 1.3x. Generally speaking, a successful investment or fund is one that returns more capital than investors paid in, so the MOIC for successful funds and investments exceeds 1.0, while unsuccessful investments and fund portfolios yield a MOIC lower than 1.0.

MOIC vs. DPI

MOIC is similar to another investment metric: distributions to paid-in capital (DPI). But whereas MOIC expresses a gross multiple of returns on invested capital, DPI expresses the multiple of returns net of any associated fees or expenses.

MOIC vs. TVPI

During the early years of a fund’s lifecycle, DPI and MOIC are not as meaningful as other fund metrics because the fund is usually still in the process of calling committed capital, making investments, and waiting for suitable liquidity events. For this reason, fund managers also look at other fund metrics that better reflect their holdings, such as total value to paid-in (TVPI). TVPI is the ratio of the fund’s total value (the sum of distributions and net asset value) to paid-in capital.

Similarly, considering MOIC for an individual portfolio company investment is not usually relevant before the company has experienced an IPO or been acquired by another company.

MOIC vs. RVPI

Whereas MOIC and DPI measure a fund’s value by comparing distributions to capital paid into the fund, residual value to paid-in (RVPI) measures the remaining value of the fund’s holdings against capital paid into the fund. Unlike MOIC, DPI, and TVPI, which express the value the fund has already returned, RVPI tries to forecast how much the fund might still return by the end of its life, when it will have liquidated all remaining investment holdings.

MOIC vs. IRR

MOIC and IRR can both be used to measure fund performance. Whereas MOIC measures returns against paid-in capital at a certain point in time, internal rate of return (IRR) accounts for the speed the fund is able to acquire those returns. LPs prefer a return sooner rather than later, so an investment that secures a 10x return within five years is better than one that takes 10 years to secure the same return. IRR attempts to quantify the value of this speed using an accounting formula called a discounted cash-flow analysis.

Reporting MOIC

The SEC’s Marketing Rule requires SEC-registered investment advisers (RIAs) to report net performance metrics if they’re also reporting gross performance metrics (and vice-versa). It also requires RIAs to use the same methodology and timeframe for both figures. This means that RIAs that report MOIC (which is equivalent to gross DPI) must also report DPI using the same timeframe and methodology.

Download Carta's VC Regulatory Playbook

Even the most experienced fund managers have a hard time keeping up with the pace of regulatory change in private market regulation. Download the Carta VC Regulatory Playbook, an end-to-end resource for understanding the basics in venture capital regulation.

DISCLOSURE: This communication is on behalf of eShares Inc., d/b/a Carta Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. ©2024 eShares, Inc. dba Carta, Inc. ("Carta"). All rights reserved. Reproduction prohibited.