What is DPI?

Distributions to paid-in (DPI) is one of the core financial metrics that private fund managers in private equity, VC, and hedge funds use to evaluate their investment performance. Also called the realization multiple, DPI is the ratio of cumulative distributions to the total capital investors have paid into the fund.

DPI is expressed as a multiple above 1.0. By the end of their lifespan, successful funds distribute more capital back to investors than investors paid in, meaning the multiple will be something above 1.0, such as 2.3x. Earlier in the fund's lifecycle, before investments have had sufficient time to yield returns, the multiple is typically below 1.0.

How to calculate DPI

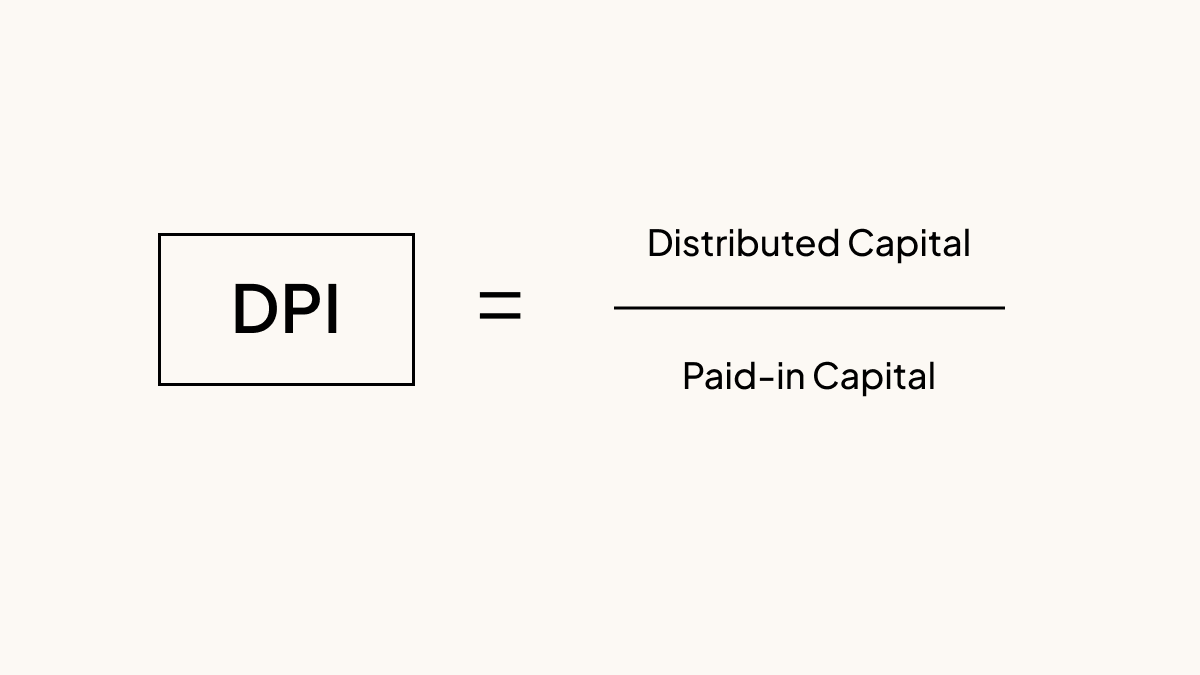

The formula to calculate DPI is:

DPI = Distributed capital / Paid-in Capital

Distributions

Distributions are any capital gains that the fund realizes and returns to investors. Gains can result from interest and dividends on invested capital, or from the sale of fund assets through an M&A transaction or an initial public offering (IPO) for one of the fund’s portfolio companies.

Paid-in capital

Paid-in capital is the total sum that investors have paid into the fund to date, including any reinvested returns. General partner (GP) contributions to the fund don’t count toward paid-in capital.

How interpret DPI

Any DPI value above 1.0 means that total distributions (net of any management fees) exceed the sum of limited partner (LP) capital invested. For example, a DPI of 2.3 means that the fund’s investments returned $2.30 for every dollar of LP capital invested.

A value below 1.0 means that once fees and carried interest have been subtracted from returns, the fund has paid out less than investors paid in.

DPI vs. IRR

Both DPI and IRR measure investment performance. Unlike internal rate of return (IRR), which accounts for the speed of returns by factoring in the time it takes for LPs to receive distributions, time is not a factor when calculating DPI.

DPI vs. TVPI

While DPI measures the ratio of distributions to capital paid in, total value to paid-in (TVPI) is the ratio of the fund’s total value to capital paid in. That means TVPI also accounts for the fund’s net asset value (NAV), or the value of investments that the fund still holds.

At the end of a fund’s lifecycle, when it liquidates all remaining holdings and distributes the proceeds to investors, TVPI becomes irrelevant because it’s equal to DPI.

DPI vs. RVPI

Residual value to paid-in capital (RVPI) is an expression of the remaining value of the fund’s holdings to the total amount of capital investors have paid in to date. RVPI doesn’t account for fund distributions at all, while DPI only accounts for distributions (and not any remaining fund holdings).

DPI vs. MOIC

DPI is similar to another fund metric: multiple on invested capital (MOIC), but there are some important differences:

First, MOIC expresses the gross returns of the fund to invested capital, whereas DPI only includes distributions net of any fees and expenses in the numerator.

Second, investors and LPs sometimes analyze MOIC at the level of individual portfolio investments. MOIC is usually only considered at the fund level after the conclusion of the fund’s life, when TVPI becomes irrelevant. After the end of the fund’s lifecycle, DPI and MOIC are the net and gross metrics of the same ratio: DPI is net of fees and expenses, while MOIC is the gross return on the capital invested.

Advantages of DPI

Unlike IRR, which requires a complex formula called a “discounted cash flow analysis,” calculating DPI is relatively simple. The DPI ratio also makes it easy for investors to understand when they’ve started to receive a positive cash return on the capital they’ve invested in the fund, and by what factor they’ve multiplied that capital.

Reporting DPI

For registered investment advisers (RIAs), the Security and Exchange Commission’s (SEC) Marketing Rule requires that fund managers report net performance metrics if they’re also reporting gross performance metrics, and that the same methodology and timeframe be used for both reported figures. This means that fund advisers reporting MOIC (which is equivalent to gross DPI) must also report DPI using the same timeframe and methodology.