- Capital calls

- What is a capital call?

- How capital calls work

- The capital call process

- Legal obligations for the GP

- Legal obligations for the LP

- Capital calls in private equity and venture capital

- Capital call strategies

- Timing a capital call

- Capital call lines

- What happens when an LP defaults?

- Example of a capital call

- How Carta can help

- Pro rata capital calls

- Subsequent close capital calls

What is a capital call?

A capital call is a formal request by an investment fund to its investors to contribute a portion of the capital they have previously agreed to commit, typically for new investment opportunities or operational expenses. Capital calls allow general partners (GPs) to draw down capital from investors as it’s needed, rather than all at once. This process improves a fund’s cash flow efficiency by aligning capital deployment with investment opportunities and minimizing idle cash.

Capital calls are a key feature of closed-end investment funds like venture capital funds, private equity funds, and real estate funds. When a private fund is raised, its investors, also known as limited partners (LPs), commit capital to the fund, but do not immediately transfer the money they commit. Their capital commitment—also called a “subscription”—is a legally binding promise that they’ll send the money they pledged when the fund manager requests it.

When LPs subscribe to a private investment fund, they commit a specific sum to the fund. The GP of the fund lists this amount of capital, along with any other rules and agreements, in the LP's subscription documents. This set of agreements includes the limited partnership agreement (LPA) and any side letters that modify the agreement. The LPA also outlines terms of the management fees the LP owes to the GP, and determines when and how the GP will distribute returns on the fund’s investments.

Since the lifespan of a private fund is typically 10 to 15 years, capital calls benefit both the investor and the fund manager. It takes time for a fund manager to deploy investment capital, and a fund’s initial investment period can last several years. During this time, LPs typically maintain control over their committed capital until the fund needs it to make an investment in a portfolio company. Since the capital drawdown happens in stages, LPs can continue earning returns on their capital by putting it to work in short-term investments.

A capital call involves more than just a wire transfer. There are legal obligations to consider, as well as best practices that will help GPs maintain good relationships with investors. Here’s everything you should know as you prepare to start calling investment capital into your fund.

How capital calls work

As the GP of a fund, when you decide to invest in a portfolio company, you might have enough cash on your balance sheet to do the deal. More often than not, though, you’ll need to call additional capital from the fund’s LP investors. The amount you’ll call depends on the size of the investment you want to make.

In practice, making a capital call means asking one or more of your LPs to transfer funds to the fund’s bank account. Rarely will a GP ask for all the committed money at once, as without a deal to deploy the funds to, this could damage fund performance metrics.

Instead, most GPs opt to make a pro rata capital call. This means that they’ll ask all of the fund’s LPs to send the same percentage of their committed capital, regardless of the amount they pledged, in order to have enough cash in total to be able to make the investment.

The capital call process

The specifics of a capital call can vary depending on the type of fund, but the general process is similar across private equity, venture capital, and other closed-end funds.

Commitment phase: At the beginning of the fund, investors agree to commit a certain amount of money to the fund over its lifecycle.

Issuing a capital call notice: The GP of the fund issues a capital call in order to fund a new investment opportunity, cover fund expenses, fund a follow-on investment, or meet other liquidity needs.

Funding and deployment: Investors transfer the requested funds, typically within 10 to 14 days. Once received, the GP deploys the capital.

Tracking capital contributions: The fund tracks the total paid-in capital of each investor so each investor meets their total capital commitment over time. The difference between an investor's committed capital and paid-in capital is known as “uncalled capital.”

Legal obligations for the GP

The LPA typically allows GPs to call capital from LPs in order to make new deals during the deployment period (or investment period). While the deployment period is usually about five years, many funds deploy their capital (meaning call commitments from LPs and use the funds) between 18 to 36 months. During the deployment period, the LPA may place limits on how much money can be committed for any one particular deal. Concentration limits can be based on the relative amount invested in a particular company, geographic limits on where companies operate, industry limits, or other factors.

The LPA also typically limits what a GP can call capital for after the deployment period ends. Usually, capital can only be called for things like follow-on investments, to pay expenses or fees, or to fulfill other obligations agreed to during the deployment period.

Legal obligations for the LP

When a GP initiates a capital call, the LP typically has between 10 to 14 days to wire the funds for the investment. The request is legally enforceable according to the details of the LPA, but LPs rarely default because it would cause both reputational damage and have severe financial ramifications.

Capital calls in private equity and venture capital

The amount of capital, timing, and frequency of capital calls will depend on the fund’s investment strategy.

Private equity funds often invest in growth-stage companies, public companies, and other mature businesses, aiming to improve operations and increase profitability before selling at a higher valuation. Capital calls in private equity are usually tied to investment opportunities or acquisitions and are typically larger and less frequent.

Venture capital funds typically invest in startups, early-stage companies, and high-growth companies. Capital calls in venture capital may be more frequent but smaller in size to support multiple fundraising rounds.

Capital call strategies

It’s important to know how much money to call and when to call it.

Timing a capital call

If you call capital before a deal is finalized and the agreement falls apart, the money will sit in your fund’s account and drag down two important metrics: the fund’s internal rate of return (IRR) and total value to paid-in (TVPI). These metrics are used to measure a fund’s performance. IRR calculates the annual rate an investment grows. TVPI is a formula that estimates the total value of an investment portfolio, including realized and unrealized investments.

If you issue a capital call without giving the LP sufficient notice, the LP may not be able to wire the money by the time you need it to close the deal. This can cause a deal to collapse. A seasoned manager will often give their LPs informal capital call notices when they enter into discussions to invest in a company, ensuring that the subsequent capital call doesn’t come as a surprise. Usually, LPs need 10 to 14 days to liquidate assets.

Capital call lines

Over the past decade, VC funds and private equity firms have increasingly used capital call lines of credit to make sure they’ll have the necessary capital on hand to complete a deal. A capital call line of credit is a short-term loan from a financial institution that you can use to invest in a company while waiting for LPs to transfer funds.

Capital call lines have benefits for both LPs and GPs. The LP saves money on management fees, since the GP holds their capital for a shorter period of time. And the GP can legally boost IRR metrics for the same reason.

What happens when an LP defaults?

LPs rarely fail to complete the capital call. But it can happen. What happens after an LP defaults depends on the LPA. A GP may:

Impose a penalty of a few percentage points on the capital called for each day the money is late—effectively charging steep interest for the late payment.

Use their own funds for the investment, sell the defaulting LP’s entire stake in the fund or defaulted stake to other investors in the fund, or sell the stake to a third party, with terms dictated by the GP.

Hold LPs accountable for liabilities incurred due to the default, potentially putting them on the hook if their payment falls through.

The penalties for missing a capital call are usually harsh. It’s important to have the consequences outlined in an LPA to prepare for a worst-case scenario.

Example of a capital call

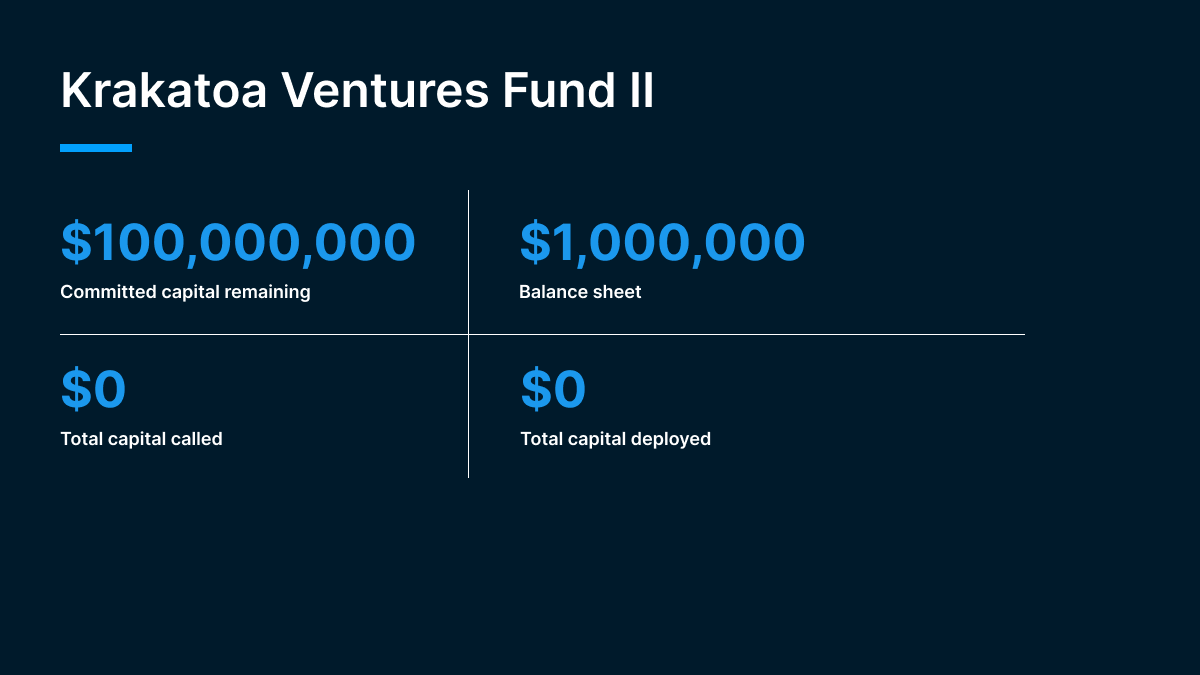

Imagine you’re the GP of Krakatoa Ventures Fund II, a $100 million fund specializing in early- to mid-stage biotech companies. You’ve just reached a deal to make a $5 million Series B investment in a startup called Genealogy Life Sciences, but you only have about $1 million on your balance sheet. To complete the deal, you’ll need to call capital from your investors.

You have 85 LPs in your fund, and their contributions range from $100,000 to $10 million. You could call $5 million from the anchor investor, the venture capital arm of a large biotech corporation. Doing so, however, might irritate an institutional investor you worked hard to recruit: They might rightly suspect that you’d only called capital from them and let the other investors continue earning short-term gains.

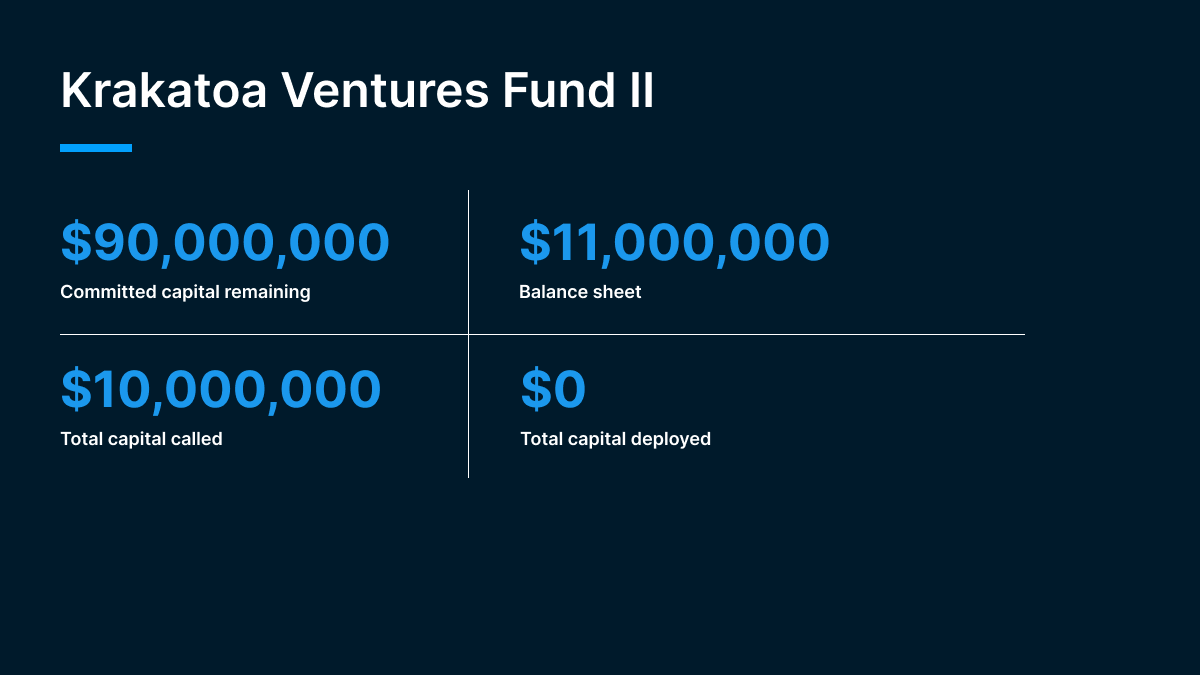

Instead, you decide to initiate a pro rata capital call, which means you’ll request the same percentage of committed capital from each LP in your fund. A 5% capital call would give you enough money to purchase the negotiated stakes in Genealogy Life Sciences, but you’re also in discussions for a smaller Series A deal. To make things easier for your LPs, you decide to make a 10% pro rata capital call.

The Librarians of America Pension Fund, which had pledged $1 million to your fund, is the first LP to respond: They wire you $100,000 to fulfill the capital call. The other LPs in the fund have a legal obligation to send their pro rata amount, as well—in this case, 10% of their respective commitments to the fund.

Now you have enough cash on your balance sheet to do the deal:

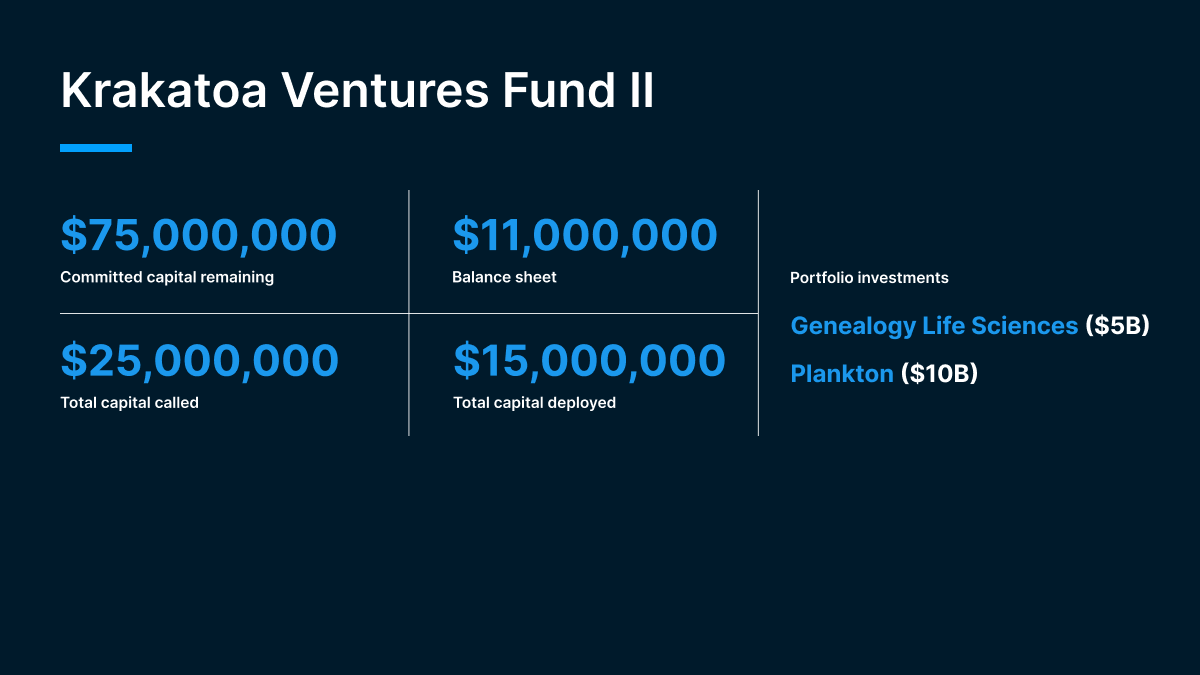

After closing the $5 million deal with Genealogy Life Sciences, you’ll still have $90 million in committed capital to call at a later date, plus $6 million in the bank.

Two months later, you’re about to close another deal. This time it’s a $10 million investment in the Series B round of a bioinformatics company called Plankton. You’re down to $6 million on the balance sheet. Your fund doesn’t have the cash on hand to lock in the deal, so it’s time to make another capital call.

Since you also have that Series A deal in the works, you decide to call 15% pro rata from your LPs. The Librarians of America Pension Fund sends another $150,000, and the rest of your LPs follow suit by sending 15% of their total commitment. Your balance rises to $21 million, and you wire $10 million to Plankton to close the deal, bringing your balance sheet to $11 million.

After two capital calls, you still have 75% of your $100M fund available for subsequent investments. Your fund also has ownership in two promising biotech companies, and has enough cash on hand to make your planned Series A investment.

How Carta can help

Carta’s capital calls request tool is designed to make capital calls fast and easy.

Pro rata capital calls

For pro rata capital calls, you can simply enter the total dollar amount or pro rata percentage you’d like to call. The tool will automatically calculate the amounts to be called from each investor.

Subsequent close capital calls

Sometimes LPs subscribe to a fund or increase their commitments after the first capital call. In such cases, you’ll need to initiate a capital call that will bring these LPs up to a level pro rata contribution with the other investors in the fund.

When you select a subsequent close capital call, Carta will list out new investors and those with changed commitments since the last capital call. Next to each, you’ll see an optional text box for your additional notes. After inputting the capital call details for each investor, you’ll have the opportunity to conduct a final review before initiating the call.

Carta has partnered with Coastal Community Bank to offer capital call lines of credit to VC investors using a transparent offer with standardized fees and pricing terms.

To learn more about Carta’s fund administration services, including our capital calls tools, contact a fund administration associate.

DISCLOSURE: This communication is being sent on behalf of Carta Financial Technologies, LLC (“Carta Financial”), an affiliate of eShares, Inc. dba Carta, Inc. (“Carta”). Carta Financial offers capital call lines through a strategic partnership with Coastal Community Bank, a Member, FDIC (“Coastal”). If you are approved for a capital call line of credit, Coastal will be your lender. Carta Financial is not providing legal, financial, accounting or tax advice or any other professional advice or service. Neither Carta nor Carta Financial assumes any liability for reliance on the information provided herein. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Coastal’s obligation to provide a capital call line of credit to you will be subject to customary conditions, including but not limited to Coastal’s satisfactory completion of due diligence on you, your general partner and your LPs, there being no material adverse change in your business/financial condition, and final, executed loan documents. Also, by submitting an application for a capital call line of credit, you authorize Carta Financial to review all information about you and your partners that you provide to or receive from any Carta Financial affiliate.