Granting equity to employees and investors is not free. Even if it doesn’t incur an immediate cash cost, an equity award should be reported as a business expense because it represents the transfer of implicit value – which may increase over time as your company grows.

As a subset of financial reporting, expense accounting offers a valuable insight into your company’s overall financial health. Accurately accounting for share-based payments, even from an early stage, will help you build confidence with investors and prepare for future eventualities – whether an acquisition or an audit is on the horizon.

This article explains the what, the how and the why of accounting for share-based payments. We’ll outline the process and requirements that startups need to follow, and explore how you can save time with audit-ready expense reports from Carta.

What are share-based payments?

A share-based payment is a transaction that occurs when an entity offers equity instruments, other assets or a cash equivalent (based on the value of its equity) to a third party in exchange for goods or services. A typical example is when a company grants shares or share options to its employees as part of a compensation package.

There are different accounting requirements for transactions settled in cash versus equity, but for the purposes of this article we’ll focus on expense accounting for transactions related to outstanding equity awards.

Why do I need to report on share-based payments?

In accordance with IFRS 2, a share-based payment standard issued by the International Accounting Standards Board in 2004, companies are required to recognise share-based payment transactions – and the associated expenses – in their financial statements.

What this means in practice is that you’re expected to include share-based payment reports in your annual income statement, which may be shared with investors and filed with your local tax authority – such as HMRC in the UK.

However, you may need to generate expense reports more frequently in certain circumstances, including the lead-up to an IPO or during an acquisition. Expense accounting also plays a role in your fundraising preparations, as potential investors will use it to assess the financial health of your company before deciding whether to invest.

In the event of an audit – which is more likely as your company grows – any inaccuracies in your share-based payment records could invite further scrutiny into other areas of your accounting. Getting on top of expense reporting as early as possible will help you avoid the hassle and cost of rectifying any mistakes further down the line.

How to calculate the expenses incurred from share-based payments

The Black-Scholes model

The total expense of an equity award is usually calculated by feeding various data points into the Black-Scholes model. The inputs include strike price, interest rate, market volatility, expected term and the fair market value (FMV) of your company’s ordinary shares – which can be determined by a HMRC or 409A valuation.

Understanding when to recognise that expense comes down to an accounting technique called amortization, which spreads the cost of an asset over a period of time.

Amortization methods

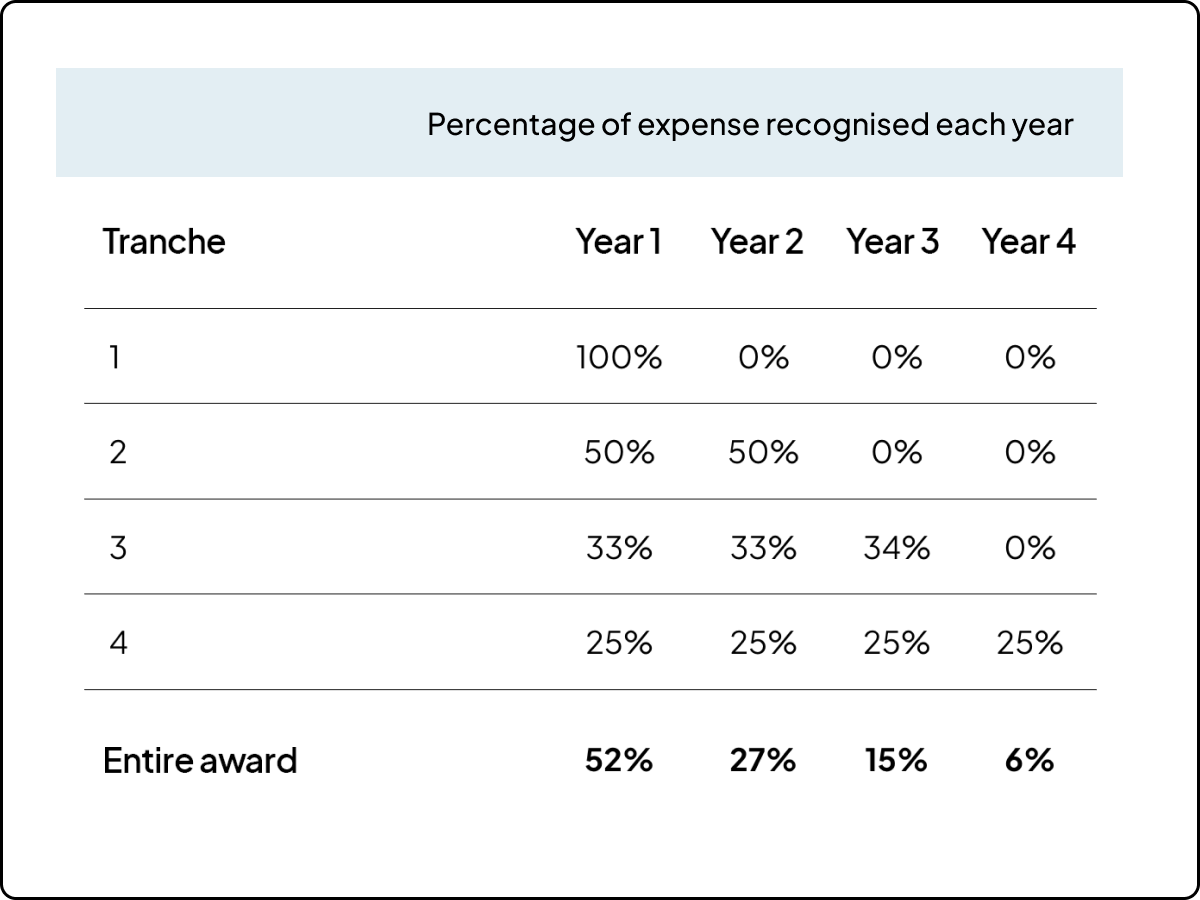

Amortization works by splitting an outstanding equity award into separate tranches according to the vesting schedule. For instance, a grant that vests 25% every year over a four-year period would have four equal tranches. How the expense of an award is distributed across each tranche depends on which amortization method you use: graded, straight-line or ratable.

Graded amortization, sometimes known as the “FIN 28” or “accelerated” method, treats the tranches as separate awards that all start vesting at the same time. The expense for each tranche is recognised from the initial grant date of the entire award to the vesting date of that specific tranche. As illustrated in the table below, the overall expense is front-loaded or accelerated.

By contrast, straight-line amortization spreads the expense of an equity award evenly over the total requisite service period (i.e. from the initial grant date to the final vesting date of the last tranche). Since the expense for each tranche is based on the number of days of vesting, the annual cost is the same regardless of tranche size. For grants with a standard four-year vesting schedule, 25% of the overall expense is recognised each year.

Ratable amortization considers each tranche individually, resulting in a staggered expense distribution based on the number of share options in each tranche. If the tranches are equally weighted, the ratable method produces a similar result to straight-line amortization. However, if more share options vest in the first tranche, the expense will be higher in the first year than the following years.

You’ll need to choose an expensing method that aligns with the accounting standard your company follows. Graded amortization is required for IFRS2 and is the preferred method under the UK's Generally Accepted Accounting Principles (UK GAAP), whereas straight-line amortization is mostly used in the US because it follows US GAAP. The ratable method is accepted by both International Financial Reporting Standards (IFRS) and GAAP. Note that for equity awards with a front-loaded or performance-based vesting schedule, graded amortization is recommended.

Share-based payments reporting from Carta

Calculating share-based payment expenses can be a time-consuming task, especially as your company grows. When you need to account for different vesting schedules, valuations, market conditions and changes to outstanding awards every time you generate a report, there’s a lot to contend with.

With Carta, expense reporting is one less thing to worry about. Our in-house experts use the information already logged on your Carta cap table to prepare an audit-ready report in accordance with the accounting standard followed by your company. They’re on hand to answer any questions from authorities and support you in the event of an audit.

A Carta Scale subscription gives you access to our proprietary tool and a fast, comprehensive service that you can trust. Whether you want to track your expenses monthly, quarterly or yearly, our team can deliver a report on demand – ready for you to review, share with investors and file with your local tax authority.

DISCLOSURE: This publication contains general information only and eShares, Inc. dba Carta, Inc. (“Carta”) is not, by means of this publication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. © 2024 eShares, Inc. dba Carta, Inc. All rights reserved. Reproduction prohibited.