- Election outlook: Tax

- Politics of tax reform

- Party positions

- Process considerations

- Tax Cuts and Jobs Act

- Tax rates

- Tax rates at a glance

- Individual income tax rates

- Corporate rate

- Capital gains tax rate

- Qualified small business stock (QSBS)

- QSBS: At a glance

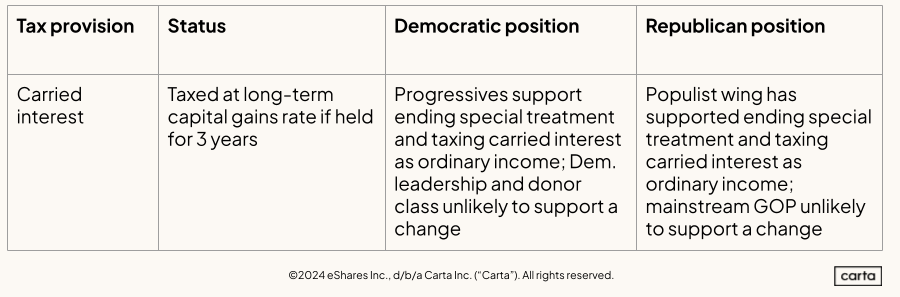

- Carried interest

- Carried interest: At a glance

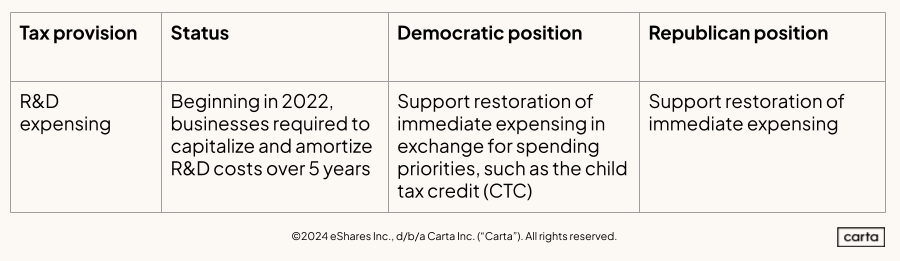

- Research & development

- R&D: At a glance

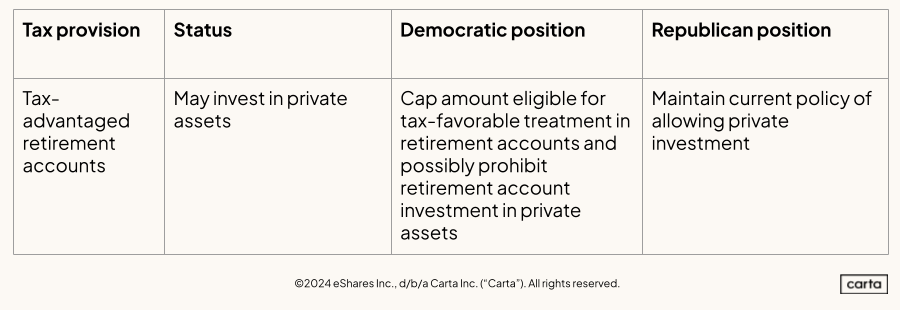

- Retirement investment in private assets

- Retirement investing at glance

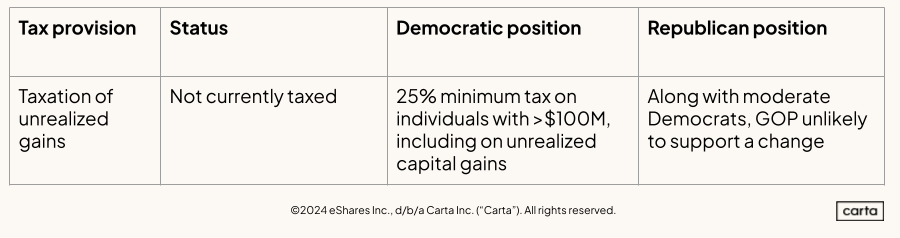

- Unrealized gains

- Unrealized gains: At a glance

- Scenario planning

- Unified government: Partisan action

- Divided government: the compromise-driver

- The backup plan: no broad deal, but narrow extenders

- The bottom line

- Get the latest updates

- Appendix: Tax policy issues for the innovation ecosystem

No matter the election outcome, policymakers will focus on tax reform in 2025.

Key tax provisions from the 2017 Tax Cuts and Jobs Act (TCJA) are set to expire in 2025. If Congress takes no action, more than $4 trillion in tax increases will take effect in 2026, including tax hikes on 62% of U.S. households—an outcome both parties will seek to avoid.

The looming tax debate will center on the TCJA, but negotiations will put the entire tax code on the table—including issues affecting startups, growth-stage companies, and investors in the innovation ecosystem.

This edition of Carta’s Election Outlook will cover key aspects of the coming debate, including:

Politics of tax reform

Tax policy is one of the biggest ideological divides between Republicans and Democrats, and the outcome of the 2024 elections will be consequential in shaping tax reform.

Party positions

Republicans: TCJA was a defining policy achievement of the Trump administration, and Republicans will push to extend as much of TCJA as possible, touting the bill’s success in driving economic growth and fostering investment. Republicans assert that driving overall economic growth expands the tax base, increases revenues, and lowers the deficit. To further offset the costs of these priorities, former President Donald Trump supports imposing a series of tariffs, notably a baseline 10% tariff and a 60% levy on goods imported from China. Republicans may also attempt to repeal or modify clean energy tax incentives included in the Inflation Reduction Act of 2022, passed under a unified Democratic government on a party-line basis.

Democrats: Democrats will push for tax “fairness,” arguing the “trickle-down” underpinnings of TCJA—which passed along partisan lines—disproportionately benefited the wealthy and corporate America over the working class. Vice President Kamala Harris supports extending aspects of the TCJA tax cuts and further expanding benefits like the child tax credit for lower and middle-income households (those earning less than $400,000), while pushing to raise taxes on high earners and corporations. Democrats are also pushing to impose new tax obligations on high-income earners by enacting a minimum tax on “billionaires” and taxing certain unrealized gains.

Within the broader “fairness” framing on tax policy, VP Harris is pushing for policy to support entrepreneurs, advocating to expand a tax deduction for new small businesses from $5,000 to $50,000. Further, access to capital is key for entrepreneurs, and she plans to break with President Biden’s current posture on raising capital gains to match ordinary income, and has instead proposed a smaller increase in the rate to maintain investment incentives. Democrats will also focus on robust tax enforcement and defend incentives that promote environmentally sustainable growth and other policy priorities.

Process considerations

Legislating is already challenging given the slim majorities and factionalism that characterize Congress—and tax legislation is even more complex due to the competing priorities of industry stakeholders. But policymakers face additional challenges:

Offsets—paying for tax policy: The Congressional Budget Office announced that extending the TCJA as-is would add more than $5 trillion to the budget. Although it is unlikely tax reform will lower the deficit (or break even), either party will balk at adding another $5 trillion to the deficit. So, some industries will need to pay a portion of continuing tax cuts or investments.

New faces: There has been substantial turnover among House and Senate members. Of the 535 elected members of Congress, less than 150 were in office in 2017, and this doesn’t include the impending wave of retirements at the end of this term. New members will need to get up to speed on tax policy and learn how to navigate a comprehensive package and process.

New leadership: Senate Democratic Leader Chuck Schumer will be the only congressional leader in the new congress who will have retained the same leadership position since 2017. Senate Republicans will have a new leader atop the caucus, as current Leader Mitch McConnell will step down as leader at the end of this term. In the House, both parties have almost an entirely new leadership slate.

Not your parents' party: Both parties have evolved over the years and become increasingly factionalized, with the more extreme wings of each conference demanding greater policy input—and willing to object and push back when it is denied. In an environment with slim majorities (which this is likely to be), these factions will be empowered, as every vote counts.

Tax Cuts and Jobs Act

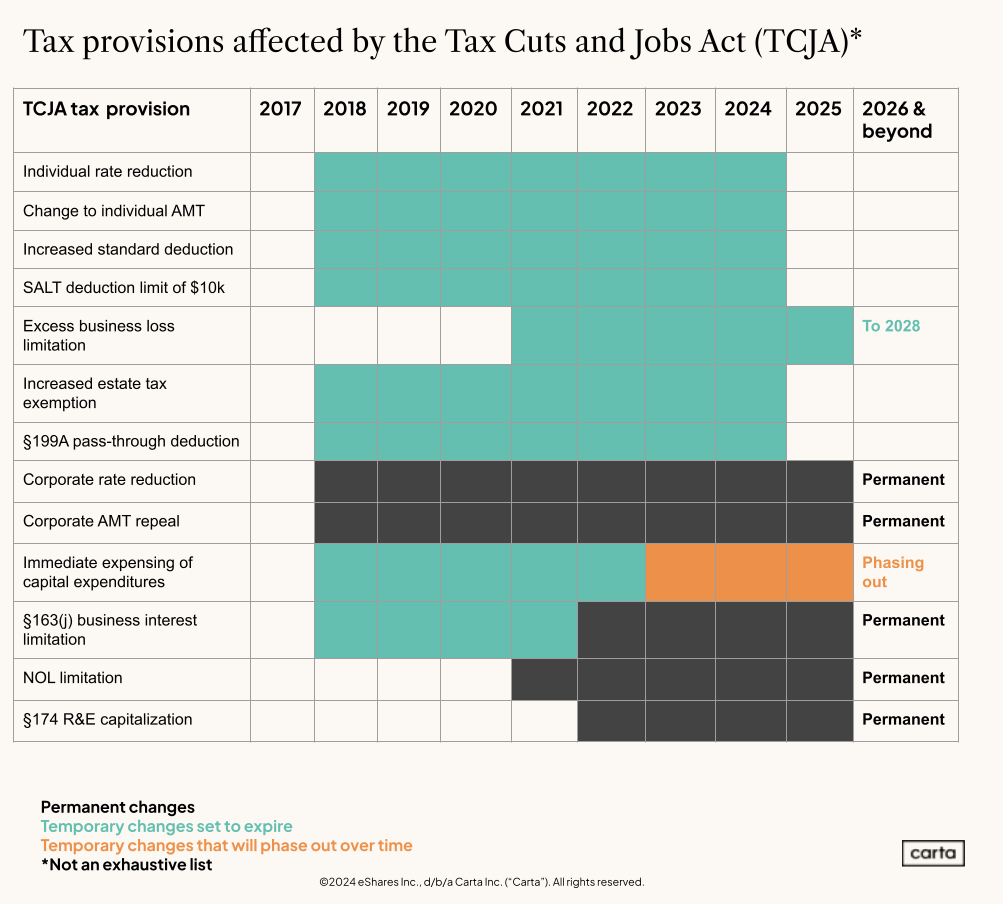

TCJA aimed to drive investment and economic growth by simplifying and lowering taxes for individuals while reducing the corporate rate and revamping how international corporations are taxed. However, only some of TCJA’s provisions were made permanent; the bulk of the changes will revert to pre-TCJA levels unless Congress extends them, and these changes will disproportionately impact individuals and small businesses, putting more pressure on Congress to act.

Here’s an overview of the status of key TCJA provisions:

Policymakers will debate issues affecting the innovation economy, including:

Individual and corporate income tax rates (and capital gains)

Qualified small business stock (QSBS) treatment

Carried interest

R&D expensing

Retirement investing in private assets

Tax treatment of unrealized gains

Tax rates

Income tax rates affect almost everyone—including most voters—so the expiring TCJA cuts and resulting tax hikes will drive the tax debate.

Tax rates at a glance

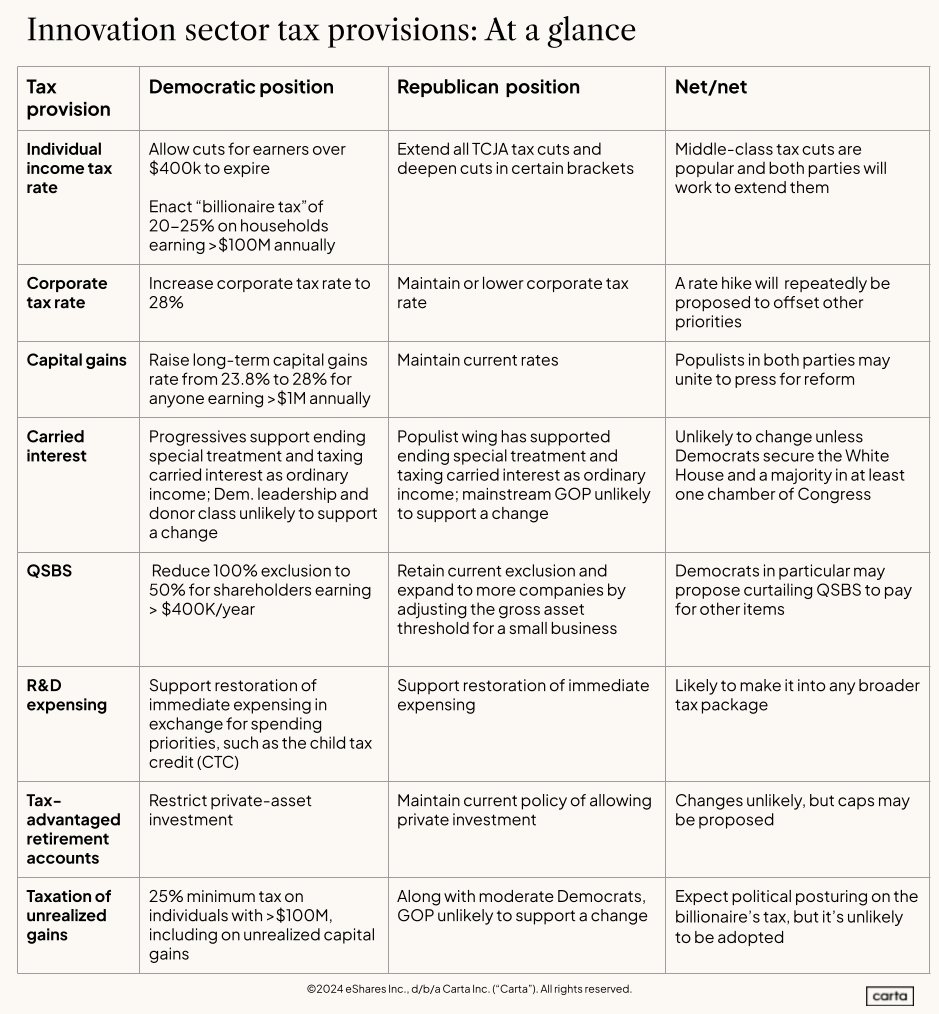

Individual income tax rates

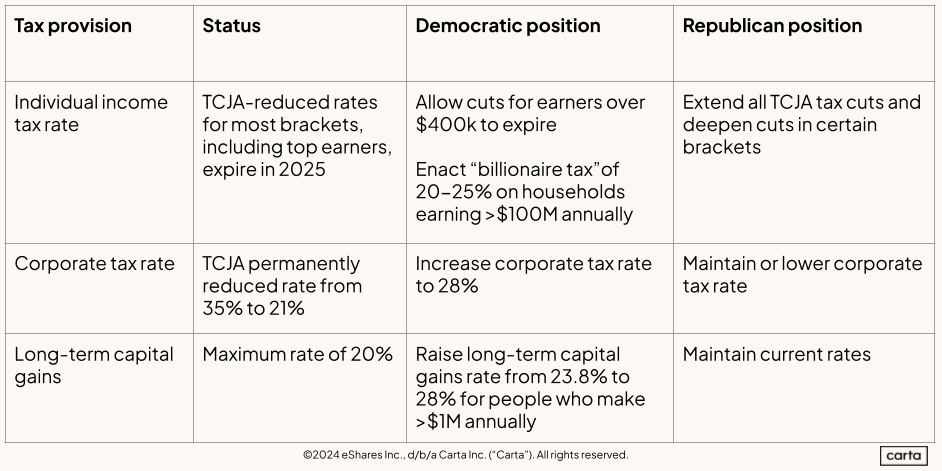

The TCJA made substantial changes to how individuals are taxed—it lowered the top tax rates, capped popular itemized deductions (SALT and mortgage interest) in exchange for an increased standard deduction, and increased the estate and gift tax exemptions. Unless Congress acts, these changes will revert to pre-TCJA levels.

Political posture: TCJA provisions benefitting the middle class generally enjoy bipartisan support. Preserving tax rate cuts and enhanced benefits is good politics for both parties, but Democrats will separately push to raise taxes on high-income earners. Republicans will push to make the TCJA income tax cuts permanent across the board.

Corporate rate

The TCJA lowered the corporate tax rate from 35% to 21% on a permanent basis to equalize U.S. corporate tax treatment with other OECD nations. To narrow the difference between the now-lower corporate tax rate and individual rates that apply to pass-through businesses, the TCJA provided a temporary 20% deduction on qualified business income (section 199A), which expires in 2025 along with individual rate cuts.

Political posture: Democrats favor bringing the corporate rate up to 28% or higher, arguing corporations need to pay their fair share. Republicans will push to maintain or possibly lower the current 21% rate, but the party’s populist wing has not written off a corporate increase. Both parties support extending the section 199A pass-through deduction, though Democrats will push to exclude higher-income taxpayers from the benefit. Democrats may also push to increase the corporate minimum tax or expand its reach to private equity, as was originally contemplated by the 2022 Inflation Reduction Act.

Capital gains tax rate

The tax code treats capital gains more favorably than other forms of income: Long-term capital gains are taxed at lower rates (0, 15 or 20%, depending on income). Taxation only occurs when the asset is sold, and inherited assets receive a tax-free stepped-up basis at death.

Political posture: Much of the rhetoric on ensuring the wealthy pay their “fair share” will focus on favorable capital gains tax rates. The recent Democratic policy platform contemplates taxing long-term capital gains for individuals with income over $1 million at ordinary income rates instead of the favorable rates they enjoy today.

Net/net: Election outcomes will largely determine where rates ultimately fall: if Republicans control Congress and the White House, an extension of the status quo is likely, though there will be fiscal pressure to address the ballooning deficit. In a divided government, there is a greater likelihood taxes on corporations and high-income earners will rise, though changes must be modest enough to garner bipartisan support.

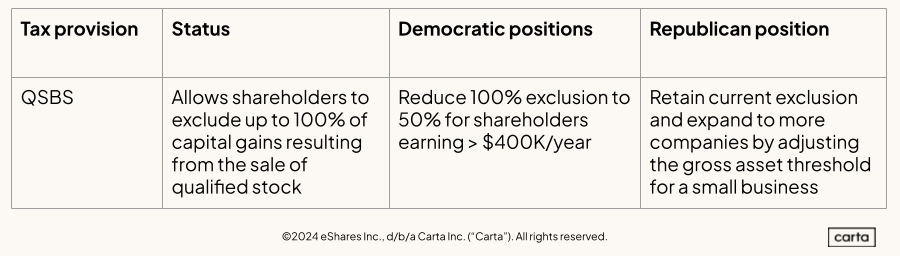

Qualified small business stock (QSBS)

Section 1202 of the Internal Revenue Code exempts shareholders—investors, founders, and employee-owners—from capital gains tax on proceeds from qualified small business stock (QSBS) if they've held the eligible stock for at least five years. This incentive helps drive capital and talent to startups and growth-stage companies.

Political posture: Although QSBS has been supported on a bipartisan basis historically, Democrats sought to curtail the benefit in 2021 to raise revenues to pay for spending priorities. The criticism primarily focused on QSBS being an unnecessary benefit for wealthy investors rather than a lever to drive capital and talent to the innovation ecosystem.

QSBS: At a glance

Net/net: QSBS will come under scrutiny to pay for other items, and given the laundry list of tax issues, policymakers may not fight hard to protect it. Engagement by founders and investors will be key to preserving the beneficial tax treatment.

Learn more: Carta Policy Insights | QSBS

Carried interest

Carried interest is the share of a private fund’s investment profits that a fund manager receives as compensation. Because carry is derived from investment returns, it is currently taxed at the long-term capital gains rate rather than as ordinary income. This encourages investment in private markets by supporting the fund economics—particularly for smaller and emerging fund managers. The TCJA changed the one-year holding period required for capital gains tax treatment to three years.

Political posture: Carried interest tax treatment comes under fire from both parties every election cycle, but it has historically been saved following bipartisan engagement from fund managers. Taxing carried interest at the ordinary income rate would only raise approximately $6.5 billion over 10 years, so it helps close a potential shortfall, but policymakers primarily use this as an example to promote tax fairness. Opposition has been growing, so the innovation economy—and the funds that invest in it—should remain alert and engaged. The key message will be the alignment of fund managers with their limited partners around financial results, the long-term nature of investing in startups and growth-stage companies, and the importance of this treatment for emerging and smaller fund managers where the carry is the bulk—if not the entirety—of their compensation.

Carried interest: At a glance

Net/net: If Democrats have the upper hand, we could see aspects of carried interest be curtailed or at least who benefits from it—emerging managers v. larger, established managers — be limited.

Research & development

IRS Code Section 174 incentivizes innovation by allowing businesses to recoup some of the costs of developing new products and services. This provision previously allowed companies to immediately expense research and development (R&D) costs in the year they were incurred. In 2022, that changed: now companies are required to capitalize those costs and amortize them over five years for domestic research and 15 years for international.

Learn more: R&D expensing: issue brief

Political posture: Congress negotiated a deal this congressional session to revert to immediate R&D expensing, but Senate Republicans opposed the package because of the way it expanded the child tax credit.

R&D: At a glance

Net/net: R&D expensing is likely to be restored in a new tax package if industry remains engaged and does not trade this policy for another provision. However, it’s uncertain whether any shift would be retroactive.

Retirement investment in private assets

Congress has recently shown interest in capping the amount that can be held in tax-favorable retirement accounts and limiting the ability of retirement accounts such as IRAs to invest in private assets. Any such prohibition would adversely affect investment outcomes and portfolio diversification for retirees, but also reduce capital available to funds and companies.

Political posture: This is not a headline issue, but it was referenced in the Democratic economic plan. Sen. Ron Wyden, the top Democrat on the Senate tax-writing committee has pushed this—and he will continue to wield power.

Retirement investing at glance

Net/net: We are likely able to maintain the ability of retirement accounts to invest in private assets, though we could see caps put in place if Congress needs revenue.

Unrealized gains

Democrats have floated—and Democratic nominee Kamala Harris has endorsed—a so-called “billionaire's tax” that would assess a 25% minimum tax on individuals with more than $100 million dollars, which would apply to unrealized capital gains as well as traditional taxable income.

Political posture: Taxing the affluent’s unrealized gains is a popular charge among progressives, though its application is difficult—mark-to-market calculations, imposing divestiture to cover tax liability, etc.—and a recent Supreme Court decision raises questions about its constitutionality. Despite some populist sentiment, Republicans are unlikely to embrace such a proposal, and moderate Democrats are not necessarily championing it, either.

Unrealized gains: At a glance

Net/net: Expect political posturing on the billionaire’s tax, but it’s unlikely to be adopted.

Scenario planning

Unified government: Partisan action

If either party wins the presidency and both chambers of Congress, it would enable the majority party to use the budget reconciliation process to pass tax and spending legislation with a simple majority of 51 votes.

Budget reconciliation can be wielded by a unified government to advance a broad slate of qualifying policy goals in one fell swoop, like the Democrats’ Inflation Reduction Act and Republicans’ TCJA.

A trifecta scenario would produce a tax deal that more narrowly reflects the priorities of the majority party and does not necessitate bipartisanship.

Divided government: the compromise-driver

Tax negotiations could more easily stall out or fall apart in a divided government, but this scenario also forces both sides to come to the table to compromise.

The slimmer the margins, the more difficult the task of legislating a large tax package. The dynamics will also be different depending on the presidential victor. Trump would likely try to protect his signature legislative achievement, while Harris would likely try to make her own mark on tax and spending.

Some key dealmakers from the TCJA era will not be around next session. Others would need to step in to help facilitate the horse-trading that gets major deals across the finish line.

The backup plan: no broad deal, but narrow extenders

Tax writers often turn to “extenders packages” to stave off expirations of temporary tax credits and some other tax provisions, but even these packages are increasingly done retroactively and reinstitute the provisions well after their “expiration.”

If broader efforts fail to materialize by the end of 2025, this option is an escape hatch that could save key bipartisan pieces of TCJA, like R&D expensing.

Even these more narrow negotiations are difficult and require compromise, but limit the deal space in an effort to reach agreement. This is not ideal, but buys some time while keeping key tax pillars in place.

The bottom line

Tax reform will dominate the policymaking process next year no matter the election outcome.

That engagement has already started, and Carta is working with our coalition partners to shape and drive the policy debate on issues that matter to our ecosystem, including:

Expand QSBS

Restore R&D expensing

Maintain carried interest

Align taxation on capital gains to time of sale

Policymakers are increasingly scrutinizing private capital, as progressives on the left and populists on the right are skeptical of many of the innovation economy’s policy priorities. As they search for revenue offsets to pay for tax cuts and investments, we will need to build a bulwark of moderates on both sides who will support and fight for these policy priorities.

Get the latest updates

To stay up-to-date on the latest in public policy affecting the private-market ecosystem, subscribe to Carta's Policy Weekly newsletter:

Appendix: Tax policy issues for the innovation ecosystem

DISCLOSURE: This publication contains general information only and eShares, Inc. dba Carta, Inc. (“Carta”) is not, by means of this publication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. All product names, logos, and brands are property of their respective owners in the U.S. and other countries, and are used for identification purposes only. Use of these names, logos, and brands does not imply affiliation or endorsement. ©2024 eShares Inc., d/b/a Carta Inc. (“Carta”). All rights reserved. Reproduction prohibited.