Venture capital funds can come in very different sizes. Some funds might manage a couple million dollars, using that capital to make relatively small early-stage bets on intriguing up-and-comers. Others might manage hundreds of millions or even billions of dollars, deploying their additional firepower to fuel mid-stage or late-stage startups that appear poised for lucrative exits.

VC funds of these various sizes tend to differ in some critical ways. One such variable is the size of the return they might be expected to produce for their limited partners (LPs)

Carta’s latest report on VC Fund Performance includes data from 687 funds closed with between $1 million and $10 million in assets under management, as well as another 210 funds with more than $100 million in AUM. These are all U.S. funds closed between 2017 and 2024 on the Carta platform.

Across most fund vintages and most performance thresholds, the results are clear: Recent $1 million-$10 million funds are posting better results than recent funds of more than $100 million.

Recent VC fund IRRs

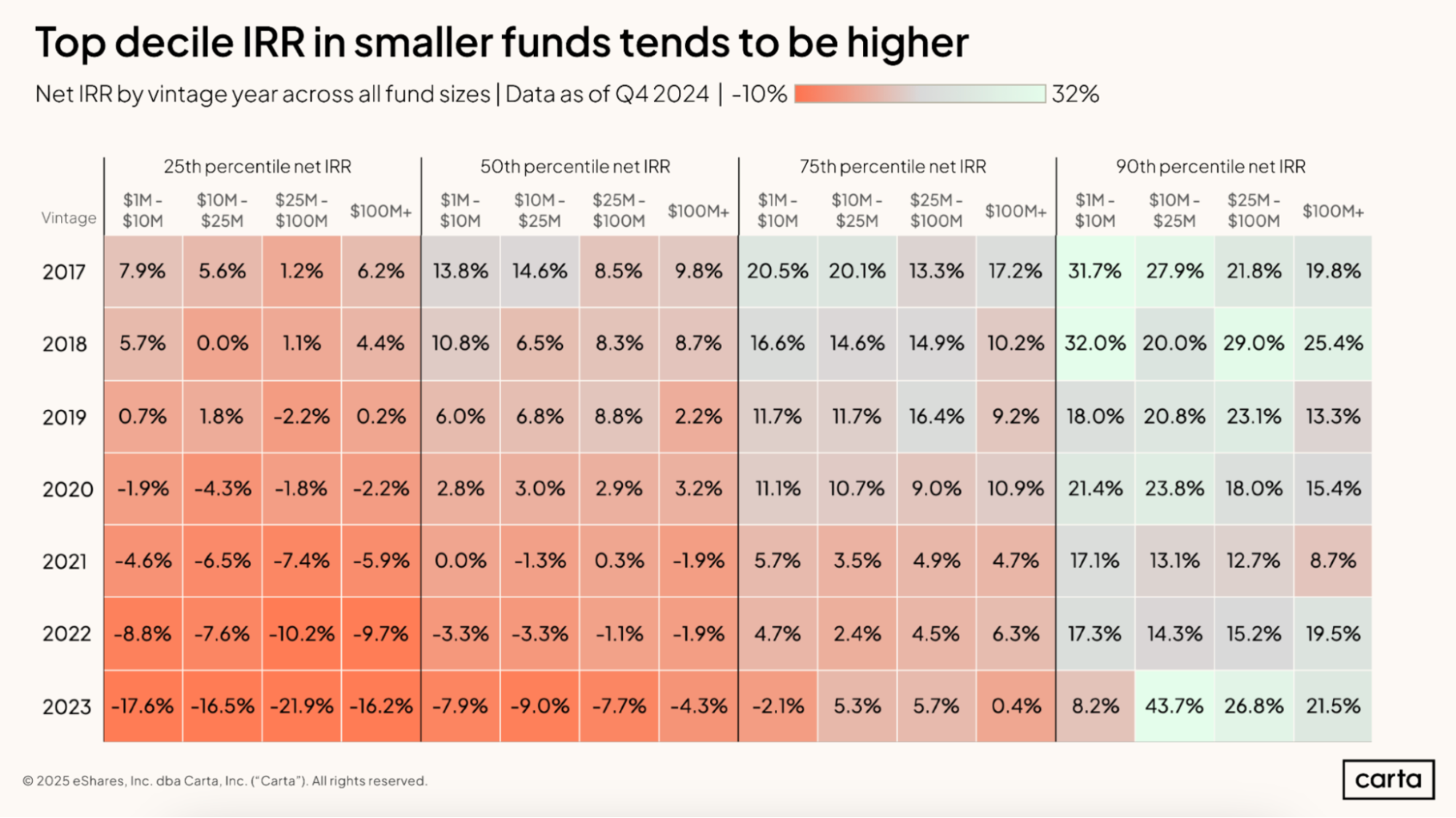

One of the primary metrics that venture firms and their LPs use to track fund performance is internal rate of return (IRR). This statistic shows the annualized percent return that a fund has already returned or expects to return.

Across recent funds that have been in the market for at least five years, IRRs tend to be higher for the smaller funds than the $100 million-plus funds.

For instance, in the 2017 vintage, median IRR among funds in the $1 million to $10 million interval is 13.8%, compared to 9.8% for funds larger than $100 million. The smaller funds also produce higher IRRs than the larger funds at the 25th percentile, the 75th percentile, and the 90th percentile. The same holds true across the 2018 and 2019 vintages, too.

Recent VC fund TVPIs

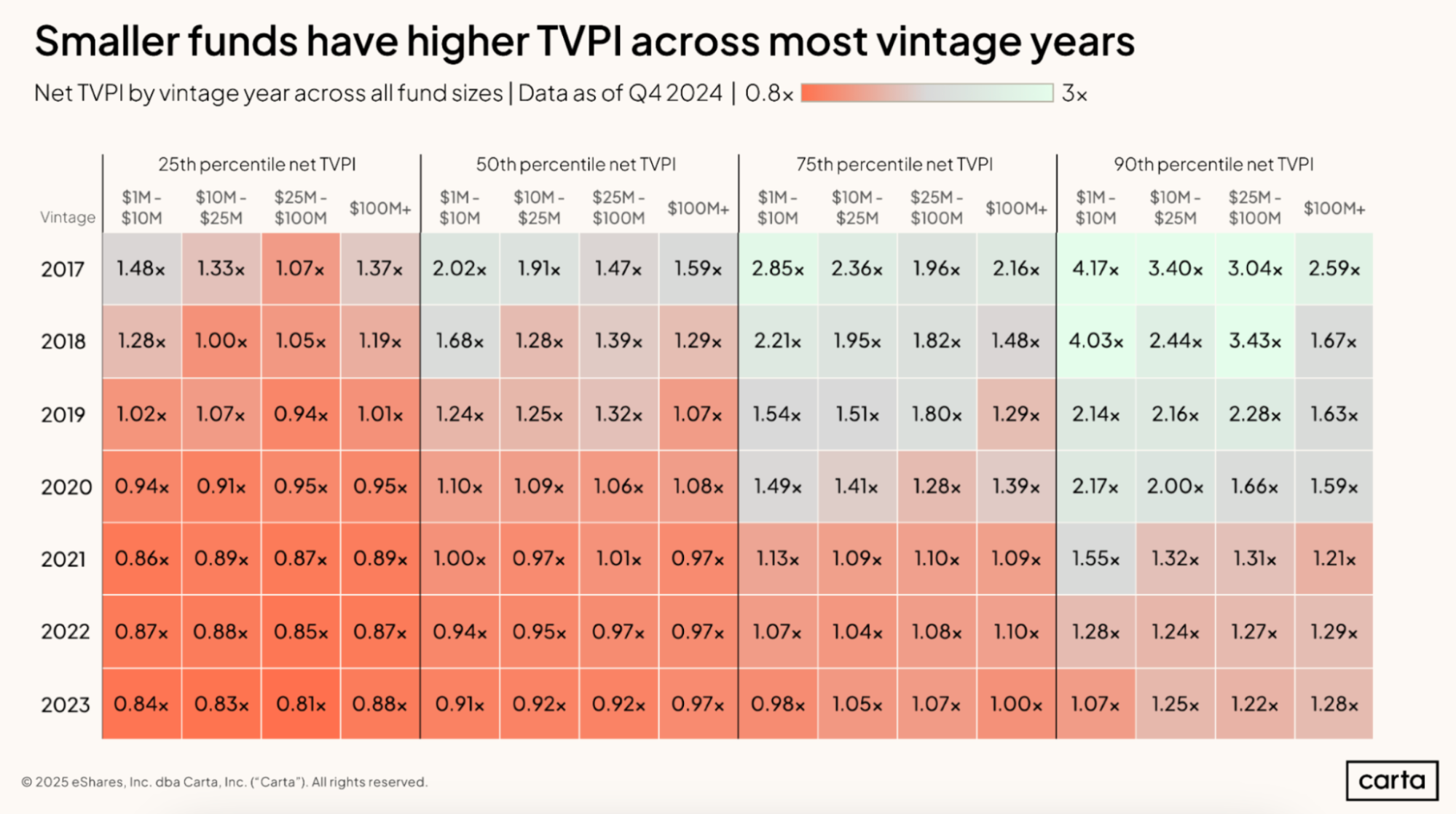

These same general trends apply to TVPI, another closely watched measurement of fund performance. TVPI is a multiple that expresses the present value of a fund (across both realized and unrealized returns) compared to the value of the capital paid in by LPs. A fund with a TVPI of 2x is thus on track to double the value of its LPs’ total investment.

For fund vintages from 2017 through 2021, $1 million-$10 million funds are producing better returns than funds of more than $100 million across most performance thresholds:

This outperformance among smaller funds does not exist in the most recent fund vintages, where many funds have TVPIs below 1x. In some ways, this is to be expected: TVPIs are typically lowest in the first years of a fund’s existence, as portfolio companies have had limited time to grow their valuations. But given the venture slowdown that began in 2022, the past two or three years have also been particularly unkind to new funds.

Why smaller funds tend to outperform

This fund performance data follows the law of large numbers, which is the mathematical truism that it’s easier to produce a large multiple on a smaller initial outlay of capital than a larger one. For instance, generating a 10% return on a $1 million fund requires only $100,000 in profit, while a 10% return on a hypothetical $100 million fund requires a $10 million profit. Finding scalable investment opportunities with the same return potential grows more difficult as dollar amounts grow larger.

The strategies of small VC funds compared to large VC funds may also play a role. Smaller funds are more likely to invest at the earliest venture stages, where deals tend to bring both more risk and more upside potential, while larger funds are more likely to invest at later stages, where companies are already more established and some growth has already taken place.

Despite this trend of outperformance, smaller funds are not always a superior investment option for LPs. Again, this is due in part to the math of large numbers. A $1 million VC fund might be looking for commitments of only tens of thousands or hundreds of thousands of dollars from its LPs. For a pension fund or endowment that manages hundreds of billions, an investment on this scale is probably not worth the time and effort it would require, even if it might produce a higher multiple. Because larger funds tend to accept much larger investments from their LPs, they may have the potential to create more meaningful returns at scale.

Other differences between large and small funds

In addition to this gap in current performance, there are several other notable differences between seven-figure VC funds and nine-figure funds. These include the number of LPs who contribute to these funds and the size of the contributions those LPs typically make.

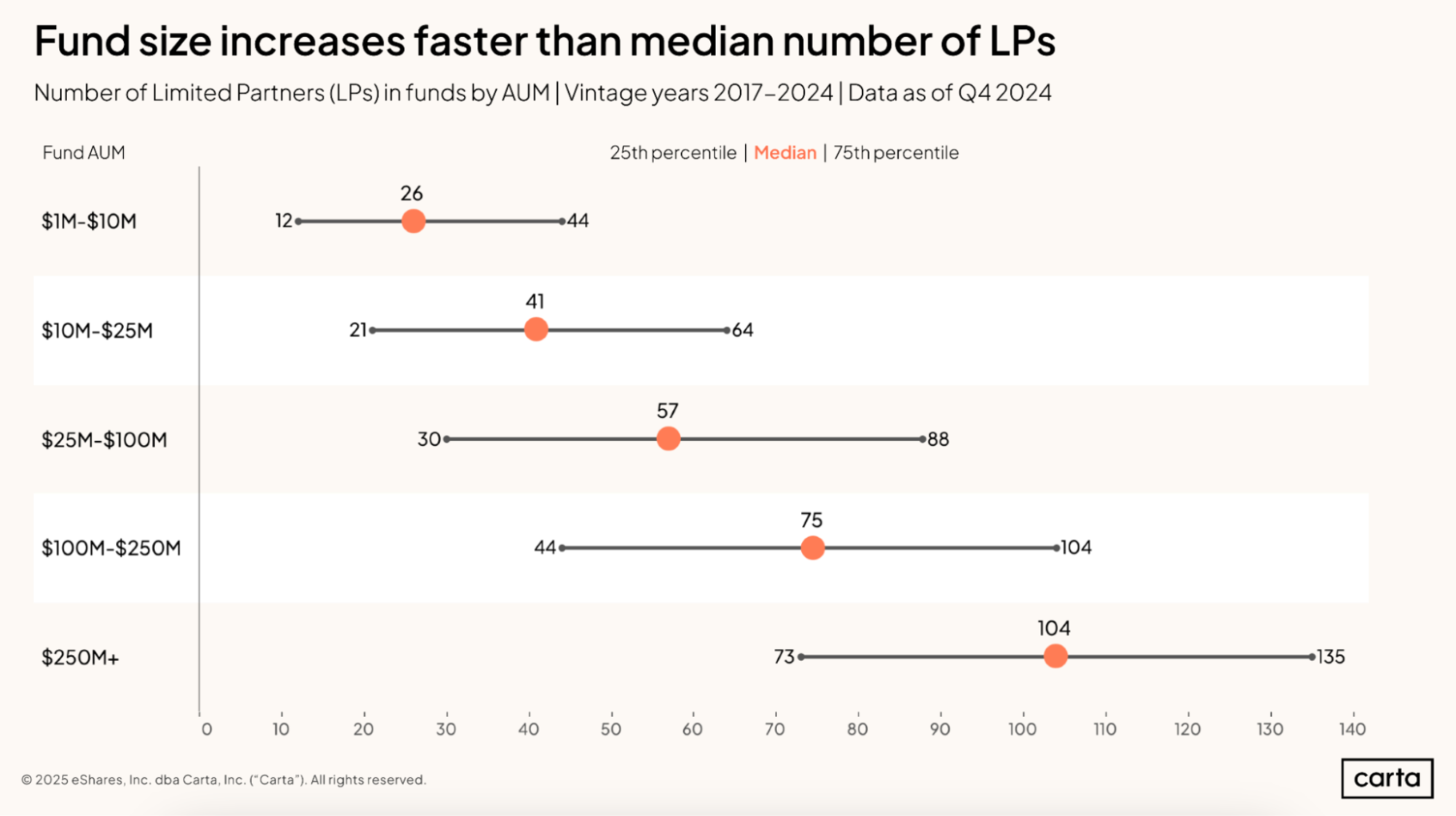

Number of LPs

Smaller funds typically have fewer LPs. In the $1 million to $10 million cohort, the median VC fund raised over the past eight years has 26 LPs, and half of all funds have somewhere between 12 and 44 LPs. For funds between $100 million and $250 million, the median investor base comprises 75 LPs, with 50% of all funds landing between 44 and 104 in LP count.

In more recent years, however, the gap in LP count has been closing. For funds from the 2022 vintage, the median $1 million-$10 million fund had 83 LPs and the median $100 million-plus fund had 23, a difference of 3.6x. In the 2024 vintage, median LP count had declined to just 47 for the larger funds and increased to 29 for the smaller funds, a difference of 1.6x.

This contraction in the number of LPs contributing to the largest VC funds is likely a symptom of lessening demand for the asset class among some allocators. When the broader venture market entered a downturn in 2022, many LPs chose to reduce their exposure to VC or else pull out of the space entirely, reducing the pool of potential investors from which VC fund managers could draw.

LP check sizes

Smaller funds tend to have smaller LP bases than $100 million-plus funds. And the investors in smaller funds also tend to write significantly smaller checks.

At the low end of the range for seven-figure funds—$1 million—the 26 LPs in a hypothetical median fund would have an average contribution of about $40,000. At the low end of the range for larger funds—$100 million—a fund with median LP count would have an average contribution from each LP of about $1.3 million.

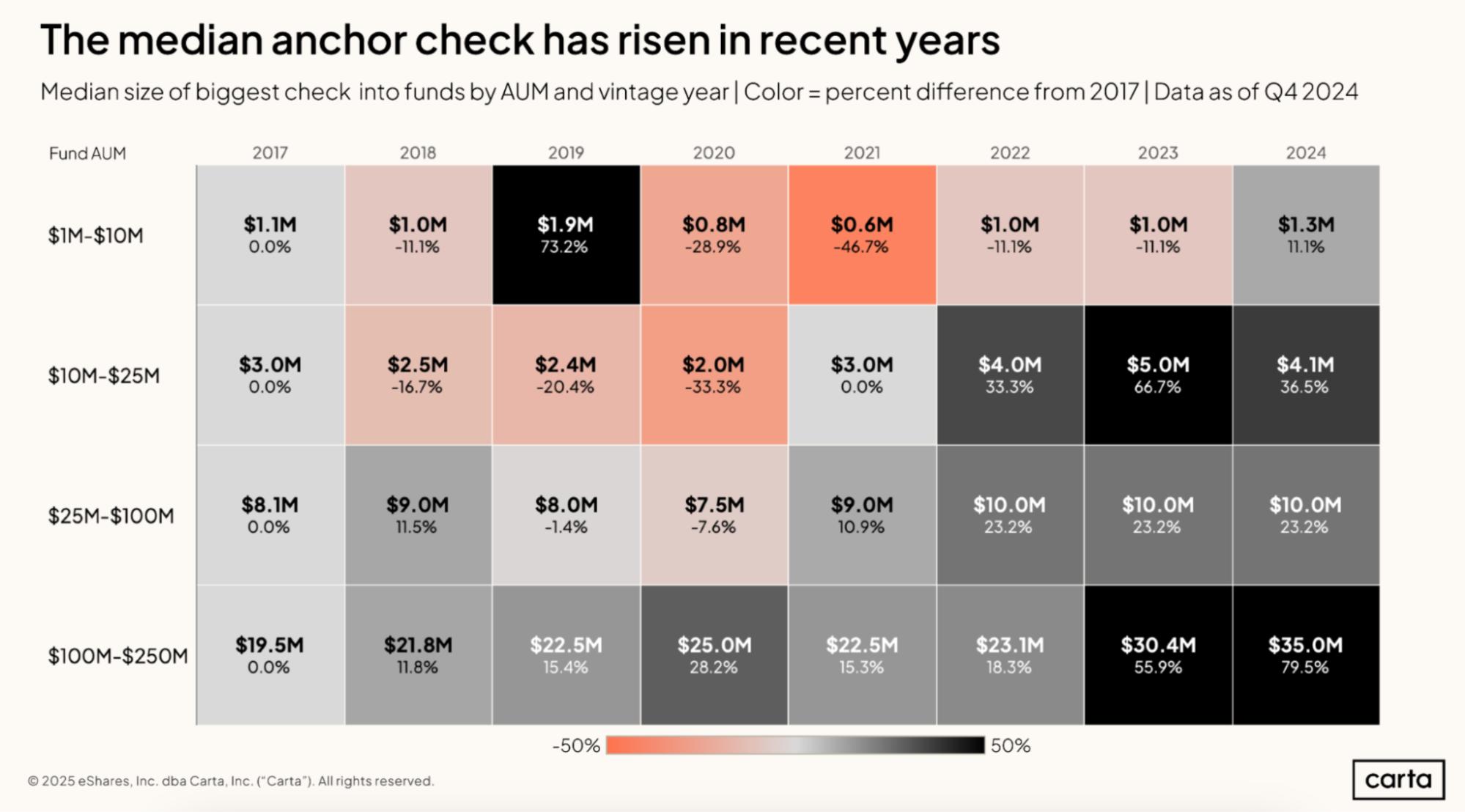

In reality, of course, some LPs contribute more to a VC fund than others. The largest single LP contribution to a fund is referred to as the anchor check. Comparing the sizes of these anchor checks across time and across fund sizes can provide insight into how fund managers opt to structure their LP bases.

Back in 2017, the median anchor check was $1.1 million for a $1 million-$10 million VC fund and $19.5 million for a $100 million-plus fund. Since then, the gap has widened considerably.

By 2024, the median anchor check for funds between $1 million and $10 million was at $1.3 million, an increase of 11.1% compared to seven years prior. For funds between $100 million and $250 million, meanwhile, the median anchor check in 2024 was $35 million, up nearly 80% from 2017.

The median anchor check for the larger funds has mostly been steadily rising from one year to the next, with a small blip in 2022 and 2023. Anchor checks for the smaller funds, on the other hand, got significantly smaller in the early 2020s, but have since begun to rise.

Across all of the above vintages combined, the average anchor check for the smaller funds accounts for 32.9% of the vehicle’s total capital. For the larger funds, the average anchor check covers 25.6% of the total fund size.

Subscribe to the Data Minute newsletter

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. ©2026 Carta. All rights reserved. Reproduction prohibited.