At both VC-backed and PE-backed companies, equity can be a key component in how executives are compensated. Regardless of which type of firm backs a business, issuing equity is often seen as one of the best ways for portfolio companies to make sure executives are working toward the same long-term goals as their investors.

“The biggest thing is aligning incentives,” says Anthony Georgiades, general partner at Innovating Capital, an investment firm focused on deep tech that pursues both VC and PE investments. “Beyond that, equity can drive decision-making behavior. It forces executives to think like capital allocators, not operators. It bridges a lot of the gap between short-term EBITDA and long-term value creation.”

Beyond these overarching similarities, however, executive equity can look quite different depending on whether a company is backed by VC or PE. At these different types of companies, equity can serve different specific purposes. It can come in different structures. And there can be significant variation in the amount of equity that executives receive—as well as which executives receive any equity at all.

Sizing up executive equity grants

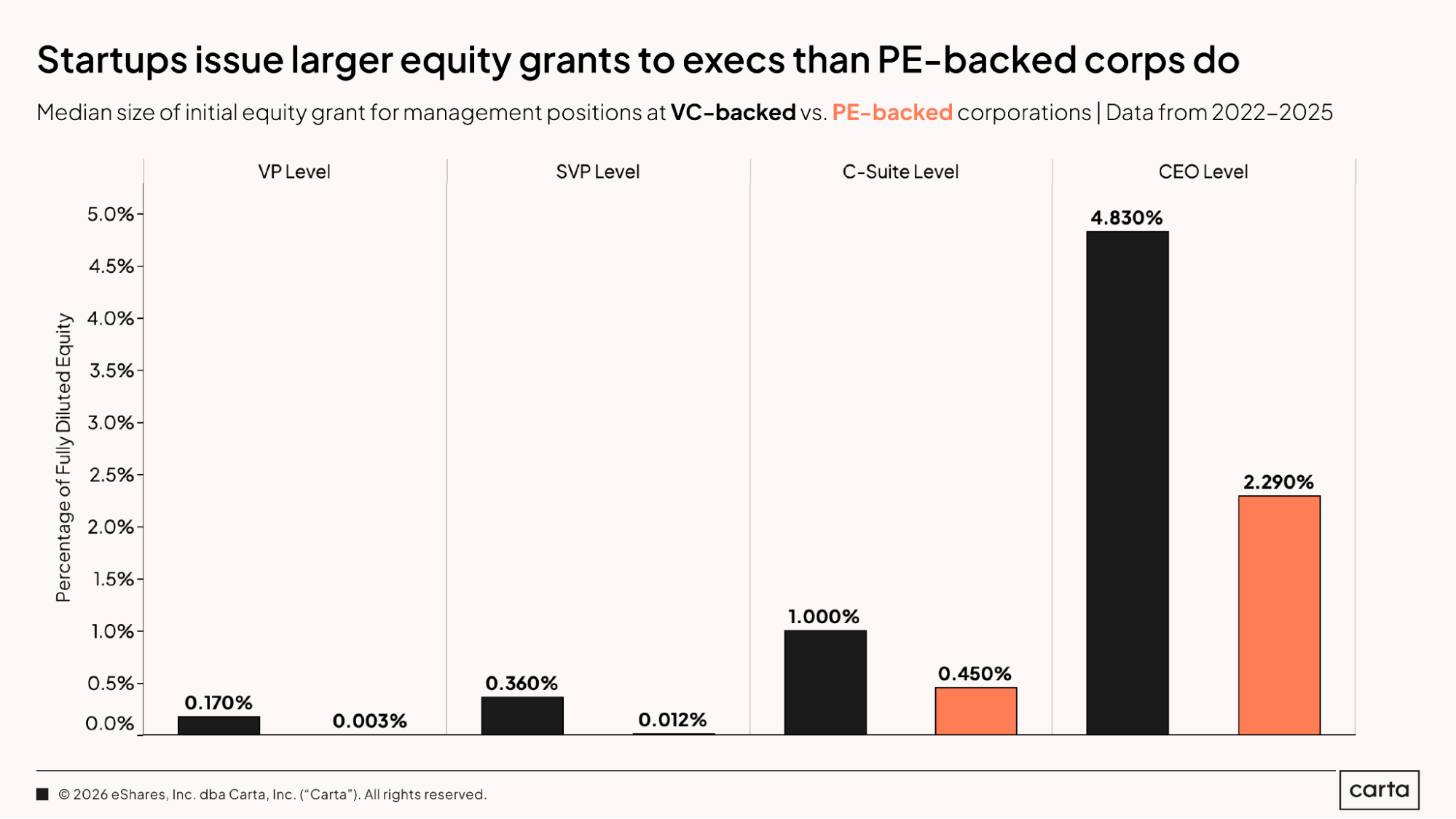

The scale of the typical executive equity grant at different types of portfolio companies is one of the easiest differences to measure. At VC-backed startups on Carta, the median non-founder CEO receives about 4.8% of the company’s fully diluted equity in their initial grant at the time of their hiring, according to Carta’s 2026 PE Executive Equity Report. At PE-backed companies, the median initial grant issued to CEOs totals about 2.3% of total equity.

This same rough ratio also applies to other members of the C-suite, with non-founder C-level executives at VC-backed companies receiving initial grants that are about twice as large (1% of total equity) as those issued to C-level executives at PE-backed businesses (0.45%).

There are a few clear reasons for this divide. One is related to the different profiles of executives at these different company types. At VC-backed startups, non-founder CEOs and other top executives are more likely to be brought on when the company is still in a true growth period, when the range of potential business outcomes is still very wide. They often will have significant input—or are the ultimate decision-makers—in what direction the company will go.

VC-backed businesses also typically have several minority owners, rather than a single majority shareholder, which can change the nature of the CEO role. Rather than reporting back to one outright owner, the CEO is more likely to be an independent decision-maker on their own.

At PE-backed companies, executives are much more likely to be professional operators who have been brought in by investors to steer a well-established business toward some particular signpost. And they’re more likely to have been appointed by a majority owner to help drive that owner’s interests. With less ultimate decision-making authority than some VC-backed CEOs, they also tend to receive less equity.

“You’ve got to think about majority control versus minority control,” Georgiades says. “With VC-backed businesses, a lot of the time, the management teams are still making a lot of decisions.”

Corps vs. LLCs: How structure impacts executive equity

This difference in the typical size of equity grants is also related to company structures and maturity levels. The startups in VC portfolios are often structured as S corps or C corps that have been built from the beginning with equity issuance in mind, with specific pools of equity that have been set aside to be used as compensation. It’s typically much easier for these types of businesses to issue restricted stock units (RSU) or stock options, the two most common types of company equity.

The companies in PE portfolios, meanwhile, are much more likely to be structured as LLCs, which cannot issue RSUs or options so easily. PE-backed companies are also more likely to be mature businesses with full cap tables that do not have preestablished pools of equity that are bookmarked for executives and other employees.

Because of these structural differences, PE-backed companies sometimes use tools other than traditional equity to align incentives among executives and investors. These can include profit interest units (PIU), phantom equity, or other equity-like instruments.

Frequently, these instruments are linked to performance metrics related to the company’s exit or the financial outcome it ultimately achieves, with the goal of aligning incentives as closely as possible between managers and investors. At VC-backed companies, equity is more likely to be open-ended—executive equity is less likely to be conditional on the company achieving a predetermined outcome.

“On the VC side, the goal is less about a very specific exit formulation and more about a long-term horizon,” Georgiades says. “In PE, it’s heavily structured. It can be a lot more formulaic. There’s very tight cap table discipline in PE, and the equity performance instruments are usually tied to exit math.”

How executive equity differs by role

These structural variations can also help account for another difference between VC-backed and PE-backed companies—the typical size of equity grants received by VPs and SVPs.

At VC portfolio companies on Carta, the median SVP receives an initial equity grant equivalent to 0.36% of total equity, while median grant size for VPs is 0.17%. At PE portfolio companies, these numbers are so small as to be nearly insignificant. The median initial grant for SVPs at PE-backed companies is 0.012% of equity, which is 30 times smaller than the median grant size for VC-backed SVPs. For VPs at PE-backed companies, median initial grant size is just 0.003% of total equity.

Again, at VC-backed startups, cap tables are typically structured from the beginning with the goal of issuing equity to many different kinds of employees, from the C-suite all the way down to members of the rank and file. At PE-backed companies, the math tends to be tighter, and significant equity is usually issued only to the very top-level leaders who are best positioned to drive specific outcomes. For VPs and SVPs at these businesses, compensation usually comes mostly or entirely in the form of cash.

If a PE-backed company is structured as an LLC, it might be particularly hesitant to issue standard equity to executives, rather than alternatives like PIUs. For tax purposes, issuing equity to an LLC employee turns them into a partner, instead of a standard W-2 employee. Thus, those LLC executives who do receive equity are no longer traditional employees—instead, they’re official partners in the business, with all the motivational implications this kind of change can bring.

“For PE executives, it often becomes a kind of psychological shift from employee to investor,” Georgiades says.

Subscribe to the Data Minute newsletter

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. ©2026 Carta. All rights reserved. Reproduction prohibited.