For the most recent vintages of venture capital vehicles, fund performance gets better with age.

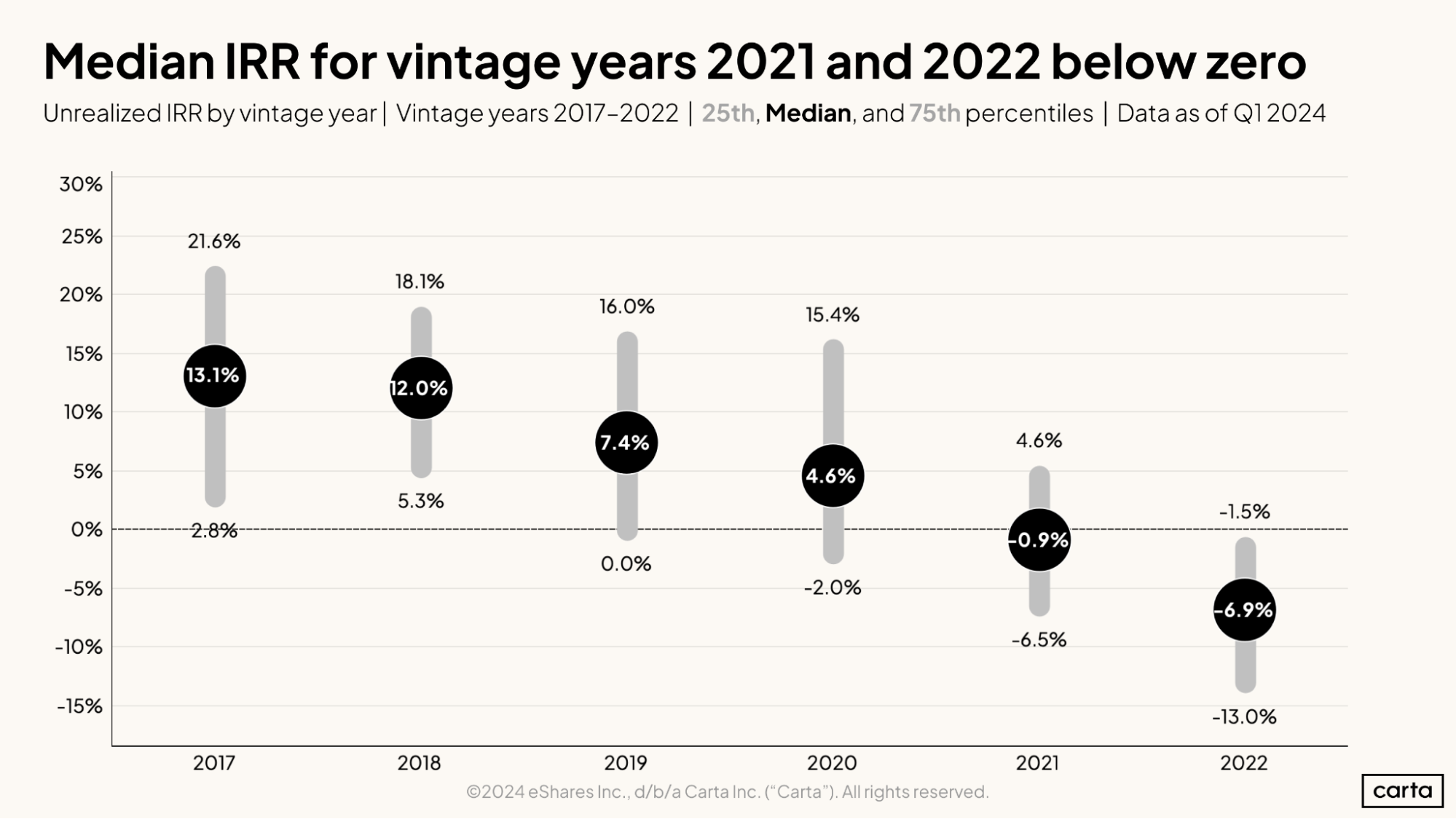

Carta analyzed more than 1,800 venture capital funds that closed from 2017 to 2022 for the inaugural version of our Q1 2024 VC Fund Performance report, offering industry benchmarks for three of the most closely watched performance metrics: IRR, TVPI, and DPI. Among this sample, there’s a clear age-related trend. The older the vintage, the higher the median IRR.

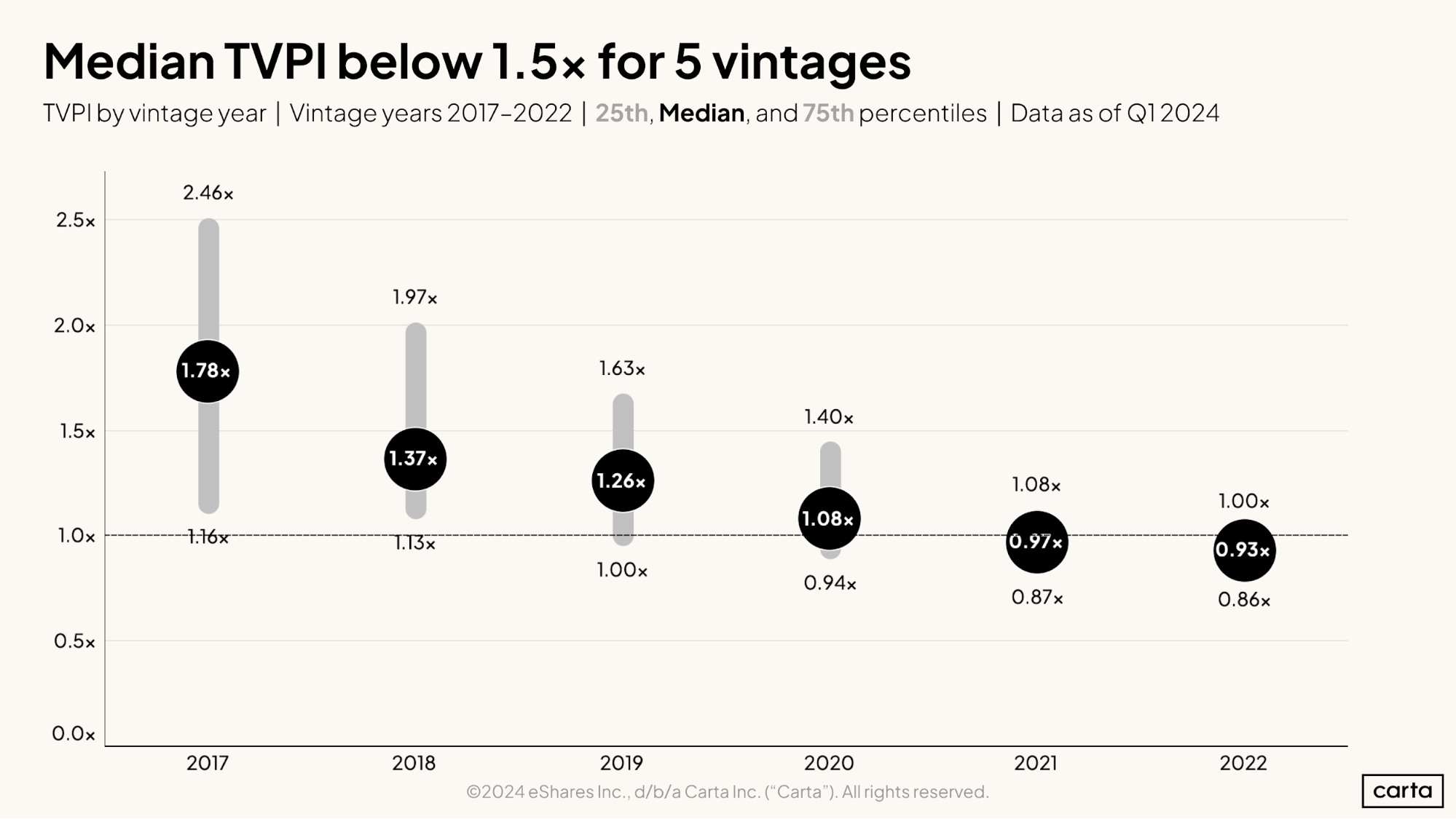

The same is true for median TVPI. The 2017 vintage has a higher median TVPI than the 2018 vintage, which in turn has a higher median TVPI than the 2019 vintage, and so on.

These trends in fund performance aren’t a surprise. And they certainly don’t prove that venture capital investing is going downhill. Rather, they reflect a mathematical truism of fund performance. Over time, most charts showing fund returns follow a J-curve: Performance starts out slow, then steadily improves over time as a fund matures and begins to realize its investments.

“There’s typically a J-curve, where your TVPI and DPI will be negative in the beginning of the fund life,” says Stephanie Choo, a partner at Portage, where she runs the firm’s North American investment team. “Because you’ve taken fees from your LPs, but you haven’t given it back yet in realizations.”

A time-sensitive look at IRR

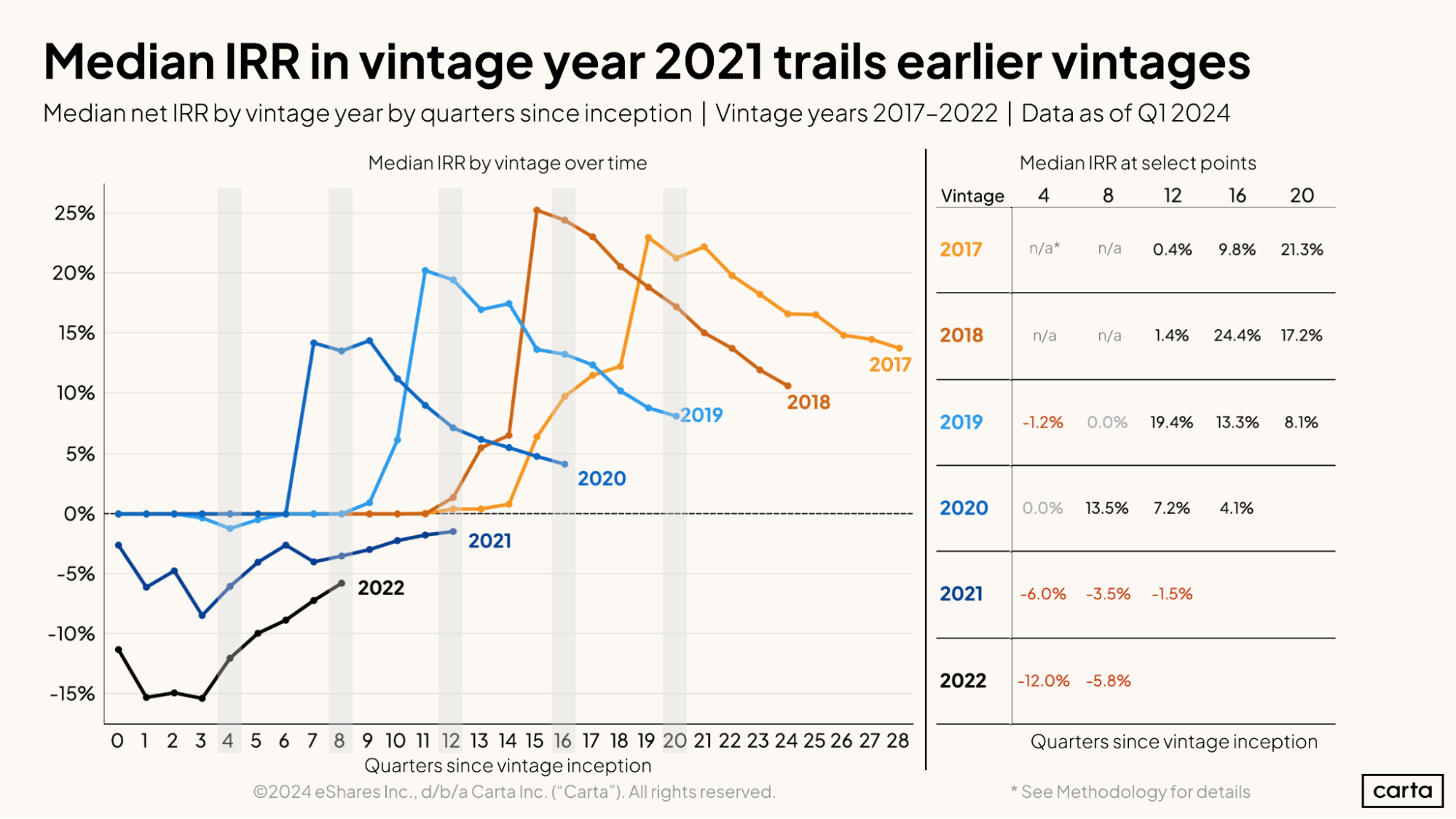

Yet this trend of older vintages outperforming newer vintages isn’t entirely due to J-curves and the timelines on which funds operate. It also holds true when we compare these vintages to each other at certain milestones based on their time since inception.

For instance, at 12 quarters since inception, the median IRR was still negative for the 2021 vintage. At that same point, the median IRR was above zero for each of the 2017, 2018, 2019, and 2020 vintages. At 20 quarters since inception, the 2017 vintage had a median IRR of 21.3%, compared to 8.1% for the newer 2019 vintage at the same 20-quarter mark.

The markets for both startup investing and startup exits were in a state of steady growth during the late 2010s and early 2020s. The older vintages in this cohort had more time to take advantage of those favorable environments and produce higher returns. The 2021 and 2022 vintages, meanwhile, have largely operated in an environment marked by fewer deals, fewer exits, and falling valuations.

These newer vintages have had less time to produce returns for their LPs. And the time they have had at their disposal has been much less advantageous.

To be clear, the 2021 and 2022 vintages are still extremely early in their life cycles. A final judgment on their performance won’t be possible for many years. Yet at this current moment in time, they don’t compare too favorably to their slightly older counterparts.

A bright future?

There’s reason to think, however, that this current state of affairs won’t last forever. Investors believe that funds raised in the past few years might eventually come to be seen as some of the most attractive vintages in venture capital memory.

One of the primary reasons that new investments and exit activity have both slowed in recent years was the downturn in venture-backed valuations that occurred after the boom times of the preceding decade. Faced with the prospect of embracing a lower valuation—much lower, in some cases—many startups proved unable to find a deal at agreeable terms.

This reset generated short-term pain—and caused a rise in startup shutdowns. But for investors, it may foment a long-term bounty. As a VC, investing at lower valuations means a lower baseline, which means a higher potential for growth. If the market turns around in the ensuing years and valuations again start to rise, deals struck during the recent stretch of depressed activity might start to look like bargains.

“The best fund vintages have tended to be right after a bubble,” Choo says. “So, 2010 and 2011 vintages were really good. The 2003 and 2004 vintages were comparatively good. You would expect that 2022 and 2023 vintages will end up pretty good, as well.”

Choo pointed to interest rates as another key variable for fund performance. When rates are lower, LPs are more likely to invest their capital into VC funds, as they pursue the higher yields that venture can provide. This influx of capital can help drive up valuations, as it did during the late 2010s and early 2020s, when nontraditional venture investors such as hedge funds and sovereign wealth funds emerged as major players in the startup space.

“As rates come down over time, we’re going to see the venture market pick back up,” Choo says.

All eyes on exits

Marcos Fernandez is the managing partner at Fiat Ventures, an early-stage firm focused on fintech. He agrees with Choo: The enticing possibilities of the most recent VC fund vintages far outweigh any negatives brought on by early underperformance.

“Everyone seems to understand that these recent vintages will be some of the best times to make investments at this stage that we’ve had in the last decade or so,” Fernandez says.

If the current market is so appealing, then why are we seeing such relatively low levels of deal activity? Fernandez points to the lack of recent exits, which has gummed up the gears of the VC market. A lack of exits means fewer distributions from VC fund managers back to LPs, which means LPs have less capital to commit to new funds, which means VCs have less new cash to put to work.

No matter how appealing a market might be, an investor needs capital to be able to take advantage.

“You’re not seeing a ton of liquidity,” Fernandez says. “Investors and allocators are looking for distributions so they can recycle money back into the venture category.”

Because of the usual J-curve in fund performance, the IRR and TVPI data for the 2021 and 2022 fund vintages will likely improve in the years to come, regardless of the specific twists and turns of the wider venture market. But whether they can catch up to prior vintages will depend on whether—and when—the tech sector sees a true bounceback in exit activity.

Get the latest data

Sign up for the Carta Data Minute newsletter to receive the latest data on VC financings, valuations, compensation, and more:

DISCLOSURE: This communication is on behalf of eShares Inc., d/b/a Carta Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. ©2024 eShares, Inc. dba Carta, Inc. ("Carta"). All rights reserved. Reproduction prohibited.