- Carta Policy Insights: Decoding the Data | Emerging venture capital managers

- How policymakers can support emerging managers in venture capital

- Venture capital delivers superior returns

- Small funds often outperform large funds

- Small funds face rising investment demands

- Policy infrastructure

- Accredited investor criteria

- The DEAL Act

- Qualifying venture capital funds

- Bottom line

- Updates in your inbox

How policymakers can support emerging managers in venture capital

Emerging managers are private fund managers who are early in their careers as general partners. Typically, they are first-time fund managers. In venture capital, emerging managers are often former investors at larger or more established firms, or successful entrepreneurs who decide to capitalize on their networks and operational experience to become VC investors.

Emerging managers drive capital to more companies, sectors, and regions, and expand the venture model—along with its innovation—across the country. They also deliver returns to their investors.

Policymakers can take additional steps to lower barriers and help emerging managers raise competitive funds by:

Preserving and broadening accredited investor criteria beyond wealth and income thresholds

Expanding qualifying venture investments to include fund-of-fund investments and secondaries

Adjusting qualifying venture capital fund parameters to increase the cap on assets under management (AUM) for a qualifying fund

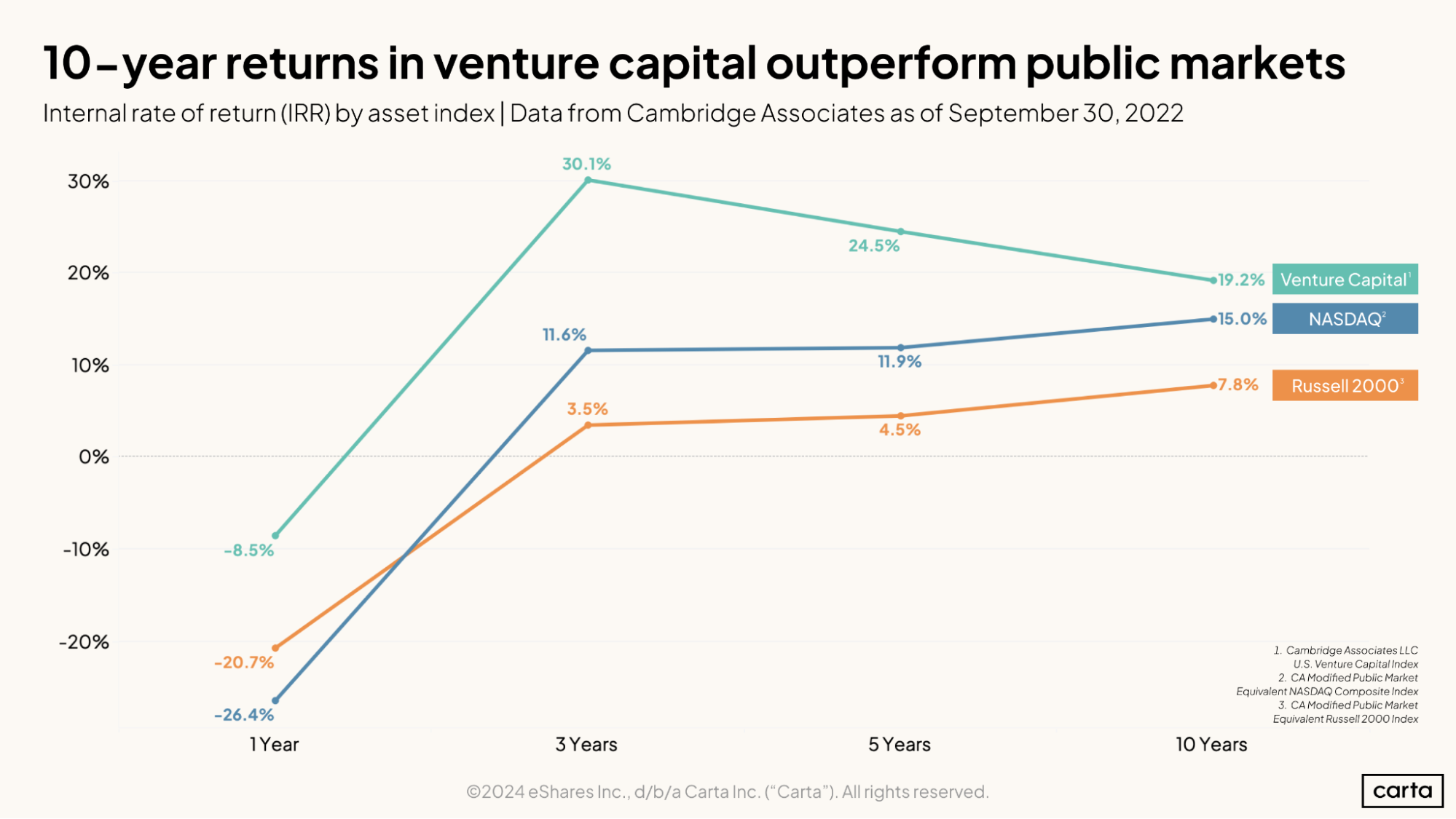

Venture capital delivers superior returns

Although performance varies from fund to fund, venture capital tends to deliver superior returns in comparison to public market indices, including the NASDAQ (which skews heavily toward public tech companies) and the Russell 2000 (an index of 2000 small-cap companies).

However, existing policy restricts investment in venture capital to accredited investors. The rationale behind this restriction is investor protection: Private markets are less transparent than public markets and private funds are less liquid, which means it is more difficult for investors to sell their stakes.

This “illiquidity premium” is baked into the design of private funds: Investments typically need time to mature, and fund managers require patient commitment to the fund. In venture capital, it usually takes years before the fund begins to distribute any returns, and the full return potential of the fund is often not realized until the fund has reached the conclusion of its lifecycle—typically ten years.

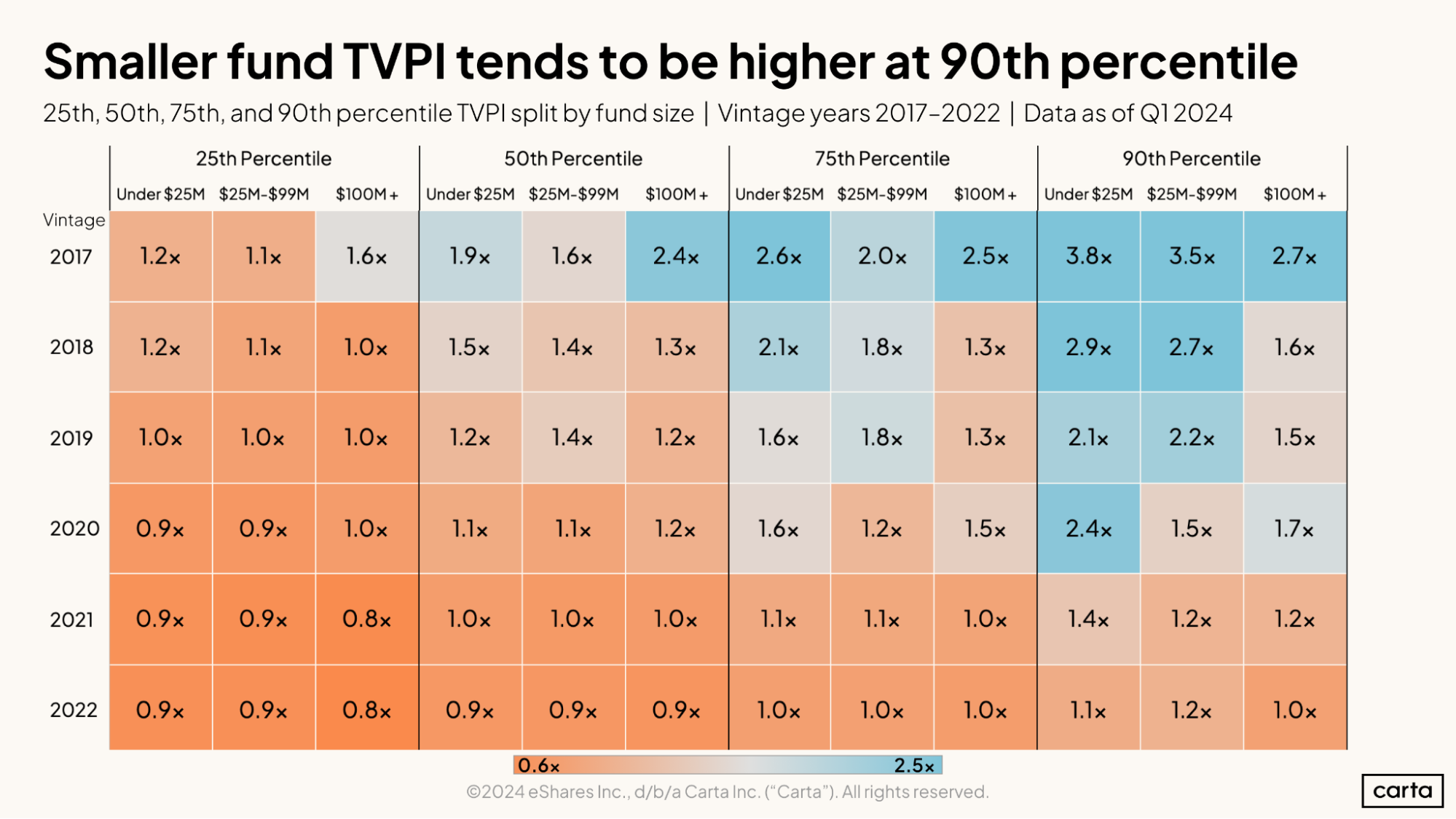

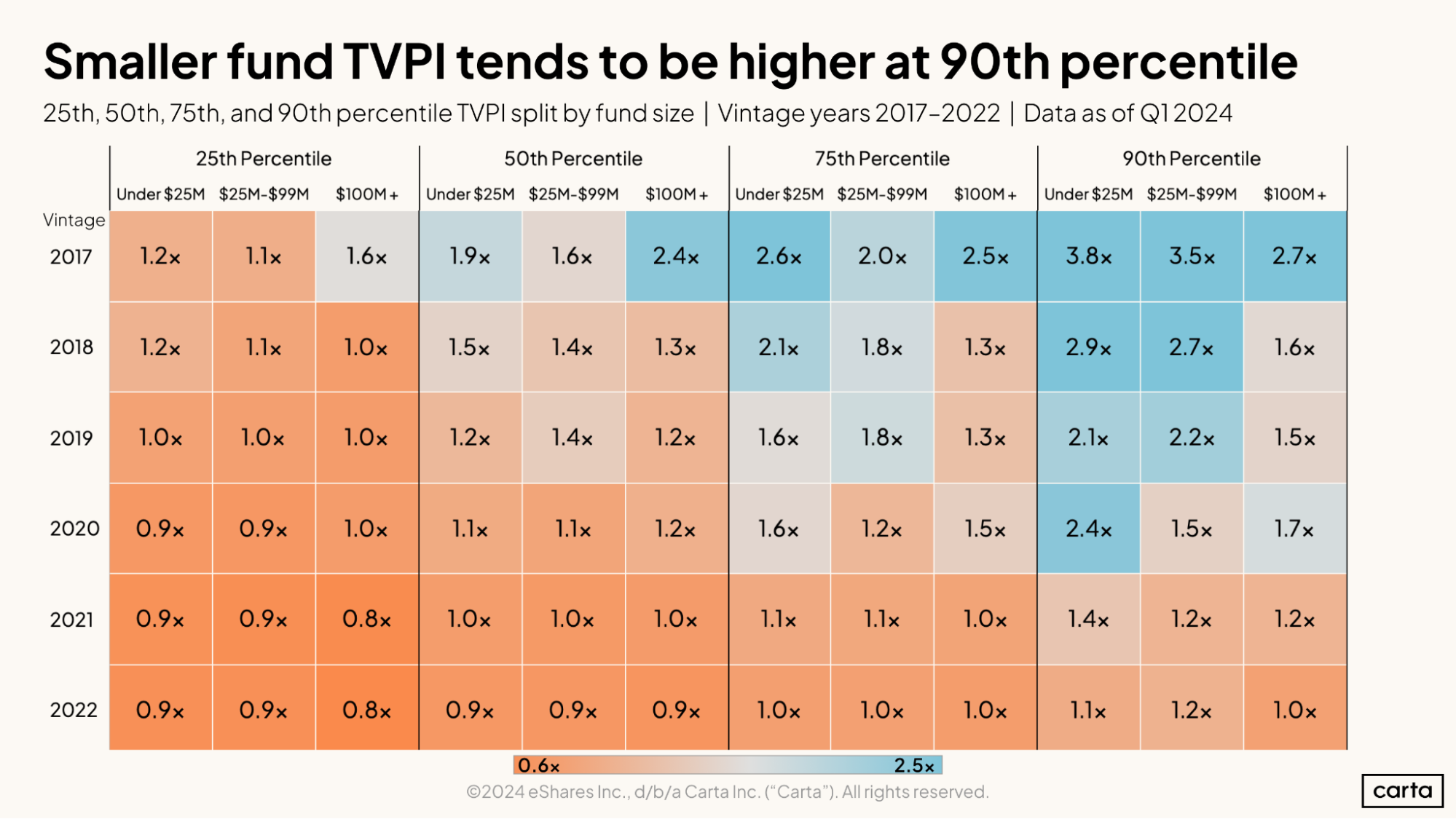

Small funds often outperform large funds

Carta data aligns with other industry findings in demonstrating that small funds often outperform larger funds. Total value to paid-in capital (TVPI) is one of the most important performance metrics for funds that have not yet reached the conclusion of their lifecycle. Carta data shows smaller funds typically have higher TVPI than larger funds of the same vintage:

In any cohort, there are always exemptions and outliers. But the general trend is for smaller funds to have better performance than their larger counterparts. Several factors contribute to this trend:

Early on the upside: Emerging funds typically operate at the earliest investment stages. Although early-stage investments have a higher risk of negative return, there’s a much greater possibility for high-multiple returns than at later stages.

Return profile: The smaller amount of AUM increases the impact of a performing investment. Put simply, when a smaller fund notches a high-multiple return on a single portfolio investment, there’s a greater chance it can return the fund’s total invested capital.

Front lines: Managers of smaller funds tend to be earlier in their investment careers, and include many entrepreneur-turned-investors. This type of investor can be closer to the ground in terms of the development of frontier technologies, and have a better understanding of emerging talent pools.

Cost structure: Advisers of smaller funds typically operate as exempt reporting advisers (ERAs), subjecting them to a more tailored regulatory regime than registered investment advisers (RIAs).

Over the years, policymakers implemented provisions aimed at facilitating capital formation for small and emerging fund managers, with the understanding that the health of the innovation ecosystem depends on robust and competitive early-stage investment. But these provisions can be made more effective with targeted changes.

Small funds face rising investment demands

Regulators have created certain benchmarks for qualifying “small” funds based on their assets under management. One provision aimed at supporting emerging managers is the qualifying venture capital fund. A qualifying venture capital fund is a type of Section 3(c)(1) fund that is permitted to have up to 250 beneficial owners (instead of just 100) as long as the fund meets the regulatory definition of a venture capital fund and has no more than $12 million in assets under management. Congress expanded the number of beneficial owners to help emerging managers assemble competitive funds by collecting smaller contributions from a larger number of accredited investors.

When Congress created the qualifying venture capital fund exemption, it originally limited the size of the fund to less than $10 million in AUM but required the SEC to review this cap every five years. In 2024, the SEC updated the threshold to $12 million to reflect inflation.

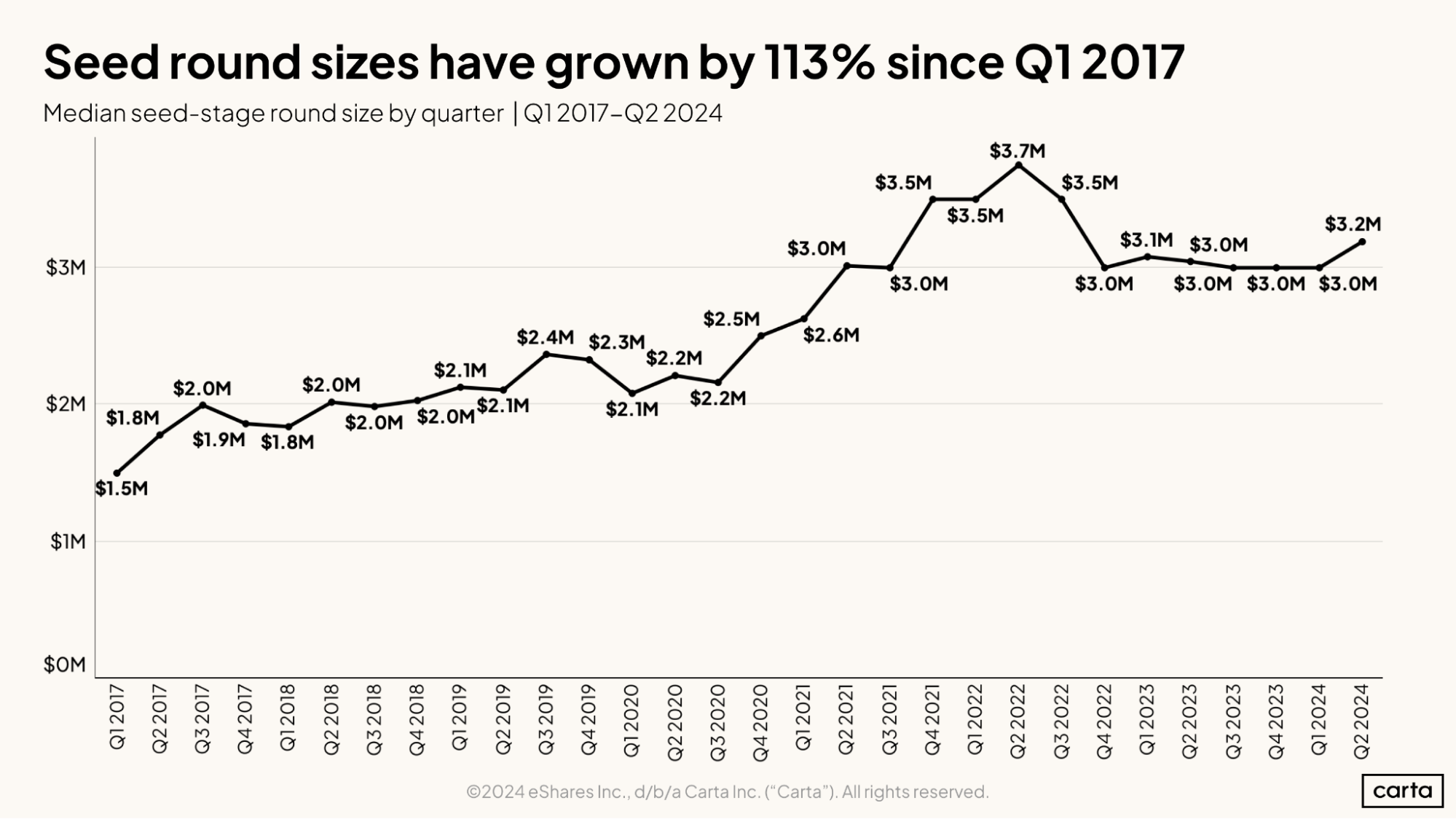

This is how policymakers perceive a small fund. But the market has a different idea of what a small fund looks like, given a twofold increase in seed-stage round sizes.

Median seed-stage round sizes have increased 113% since 2017, growing 2.64% per quarter since Q1 2017. The policy framework has largely remained the same, not effectively adjusting to reflect this new reality.

Seed investors typically need to invest in 25-35 companies for their funds to be viable and perform. Their portfolios contain a larger number of smaller investments because investors at the earliest stages need to take more “shots on goal” than funds investing in later-stage companies with revenue and product-market fit. A 113% rise in the cost of seed-stage investment over seven years means that funds capped at $12 million are less able to keep up with rising investment expectations to compete for deals. Smaller investment checks can make emerging managers less attractive to companies raising capital and less competitive in the market.

The market has adjusted; the policy framework should as well.

Policy infrastructure

To help bolster emerging fund managers—and broaden their impact in driving capital to companies and innovation across the nation—the policy framework should help them attract capital and better tailor a regulatory regime to these smaller, but impactful managers.

We can do this in three ways:.

Preserve accredited investor thresholds and expand pathways to becoming accredited

Pass the DEAL Act, expanding qualifying VC investments to include fund-of-fund investments

Increase parameters for qualifying venture capital funds

Accredited investor criteria

One way to facilitate capital formation is to broaden access to venture capital investment by retail investors. Congress can do this by creating additional on-ramps for becoming an accredited investor. Venture funds, and emerging managers, deliver returns. More investors beyond the already affluent should have access to these returns and this diversification.

Learn more: Issue brief | Accredited investor criteria

The DEAL Act

Funds of funds are often critical lead investors in the early-stage funds raised by emerging managers. Investors at larger firms will make fund-of-fund investments to gain access to deal flow, as well as exposure to new verticals and geographies. However, current policy excludes fund of fund investments from the definition of a qualifying venture capital investment, which means funds are limited in the portion of their AUM they can allocate to fund of fund investments without triggering a different regulatory treatment. This disincentivizes funds seeking certain regulatory exemptions from investing in other funds raised by emerging managers.

Learn more: Issue brief | The DEAL Act

Qualifying venture capital funds

To further facilitate capital formation for emerging managers without elite connections and in geographies without strong investor bases, Congress can raise the AUM limit for qualifying venture capital funds along with a corresponding increase in beneficial owners to help maximize utility of this provision. Proposals in both the House (with caps of $150M AUM and 600 beneficial owners) and Senate (with caps of $50M AUM and 500 beneficial owners) would provide meaningful updates to the qualifying venture capital fund parameters. The SEC’s Small Business Capital Formation Advisory Committee and Office of the Advocate for Small Business Capital Formation have recommended similar changes.

Increasing the AUM and beneficial ownership thresholds to levels that more accurately reflect market conditions would make it possible to broaden the investor base for a venture capital fund by soliciting contributions from accredited investors, as contemplated by Rule 506(c) of Regulation D.

Learn more: Issue brief | Qualifying venture capital fund parameters

Bottom line

Congress recognized the importance of emerging venture capital funds when it created the qualifying venture capital fund exemption under Section 3(c)(1). To help emerging managers raise the capital they need to drive innovation, Congress can:

Expand on-ramps for becoming an accredited investor

Increase the AUM limit for qualifying venture capital funds

Allow fund-of-fund investments into venture capital funds to qualify as VC investments, to facilitate capital access for emerging managers

Learn more at /sg/en/policy/

Updates in your inbox

Sign up below to receive the Carta Policy Team's weekly roundup of public policy developments impacting the private market ecosystem:

DISCLOSURE: This publication contains general information only and eShares, Inc. dba Carta, Inc. (“Carta”) is not, by means of this publication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein.

All product names, logos, and brands are property of their respective owners in the U.S. and other countries, and are used for identification purposes only. Use of these names, logos, and brands does not imply affiliation or endorsement.