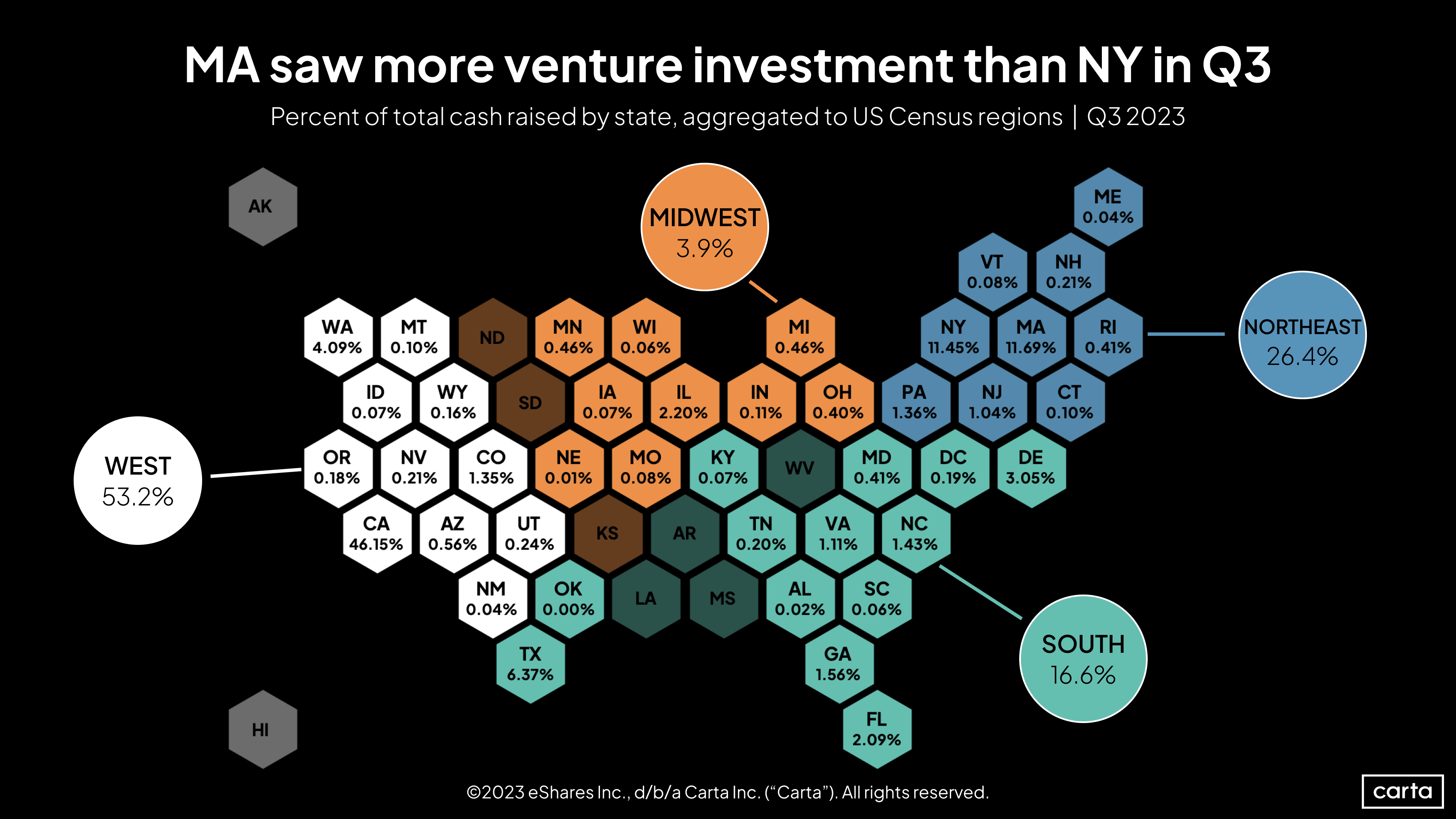

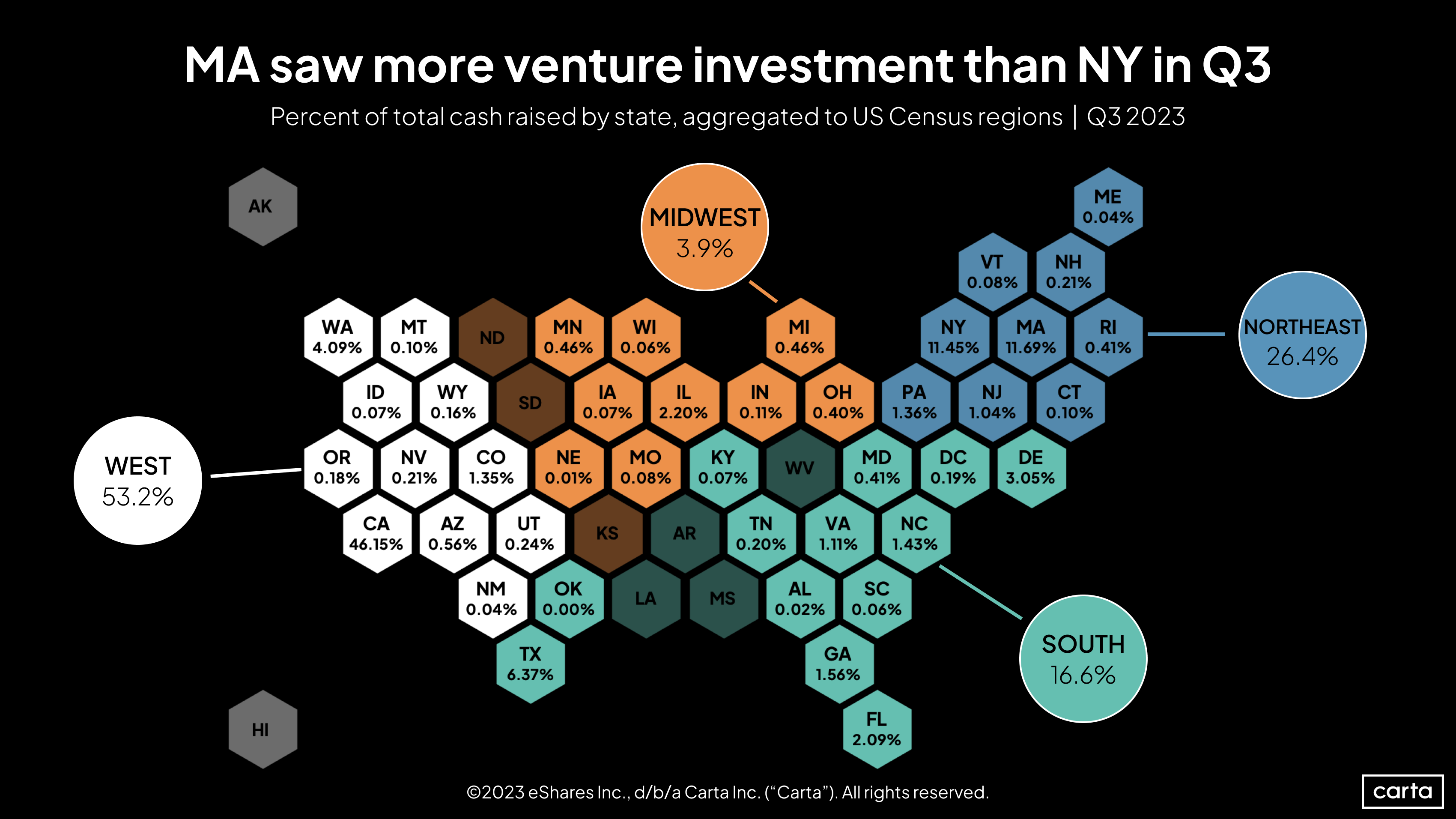

The map of venture capital funding in the U.S. is always changing. During the third quarter of 2023, startups headquartered in the West census region raised 53.2% of all venture capital recorded on Carta, an increase from 44.3% during Q2. Meanwhile, each of the other three census regions—the Northeast, South, and Midwest—saw notable declines in their share of funding raised.

Within these major regional shifts, several states saw their share of all VC dollars rise or fall by a substantial margin in Q3. Here are six states that experienced the most significant changes, beginning with the largest leap of all:

1. California

Q3 market share: 46.15%

Q2 market share: 35.99%

California’s portion of all venture activity on Carta climbed by more than 10% in Q3. That’s a big jump, even when taking into account the huge amount of activity the state already commanded.

That said, it represents more of a return to recent market realities than something entirely new. During the full year 2022, California claimed 46.2% of all cash raised in the U.S., almost the exact same sum as in Q3 2023. During the first half of 2023, the state’s market share had begun to fall: first to 40.7% in Q1, then to 36% in Q2. But that trend reversed in the late summer and early autumn, as California consolidated its position as the leading locale for venture activity in the U.S.

2. Washington

Q3 market share: 4.09%

Q2 market share: 1.99%

Washington’s share of all VC raised in the U.S. more than doubled between Q2 and Q3. Only four other states were home to larger fundraising sums in Q3: California, Massachusetts, New York, and Texas. Just one quarter earlier, in Q2 2023, Washington ranked 12th on the list of state fundraising totals.

Venture dealmaking in Washington is of course nothing new: Led by behemoths like Amazon and Microsoft, the Seattle metro area has long been a prominent tech hub. The SaaS sector was home to about 50% of all capital raised by Washington startups in Q3—software’s largest slice of the state’s funding pie in more than two years.

3. Florida

Q3 market share: 2.09%

Q2 market share: 4.05%

In recent quarters, Florida has been one of the states gaining a larger share of the venture funding market. But Q3 was a fallow stretch. With just 2.09% of capital raised, Florida ranked eighth among all states, compared to a fifth-place ranking in Q2. As has often been the case in recent years, the most popular sectors for VC investment in Florida in Q3 were SaaS, consumer, and fintech.

The whole South census region experienced a similar pullback, but the region is still on pace for a modest annual increase in venture allocation—and the broader trend of increased geographic diversification in VC is continuing. The most populous of the four census regions accounted for 16.6% of all startup fundraising in Q3, compared to 20.1% in Q2. Both of those figures, though, are higher than the South’s 15.5% market share for full year 2022.

4. Ohio

Q3 market share: 0.4%

Q2 market share: 2.34%

The home to the Cleveland and Columbus metro areas saw venture investment almost dry up entirely in Q3. But the change may be more of a return to historical norms than a blip on the radar—if there is a blip, it seems likelier to be Q2. For the full year 2022, Ohio claimed 0.6% of venture activity in the U.S., and its share of all activity in Q1 2023 was 0.5%.

Overall, last quarter was a quiet one around Lake Erie. Ohio neighbors Michigan and Pennsylvania also saw their share of venture cash decline in Q3, although by smaller margins than Ohio.

5. New Jersey

Q3 market share: 1.04%

Q2 market share: 2.73%

Like Ohio, New Jersey experienced a spike in its VC market share in Q2 only to see most of those gains disappear in Q3. Startups from the Garden State raised just 0.6% of all capital in the U.S. in the full year 2022, and that rate actually dipped to 0.3% in Q1. In that context, Q2’s rate of 2.73% looks like an outlier.

Further north in the Tri-State area, Connecticut’s market share declined from 1.12% in Q2 to a scant 0.1% in Q3. The Northeast region as a whole saw its share of U.S. venture funding dip from 29.9% in Q2 to 26.4% in Q3.

6. Texas

Q3 market share: 6.37%

Q2 market share: 4.79%

The Lone Star continues to rise. Startups based in Texas raised 3.2% of all new venture capital on Carta in 2022. By Q2 2023, that figure had reached nearly 4.8%, and in Q3 it climbed even higher. In each of the past two quarters, Texas ranked fourth among all states in terms of percentage of capital raised—but Texas has a ways to go to catch New York, which ranked third in Q3 with an 11.45% market share.

Texas is home to several burgeoning startup hubs, including Austin, Houston, Dallas, and San Antonio. One factor working in the state’s favor: Compared to other major metros, those cities can boast an attractive combination of average compensation and cost of living. In terms of population, Texas is also one of the fastest-growing states in the U.S.

Get the latest data

For weekly insights into Carta's unparalleled data on the private markets, sign up for Carta’s Data Minute weekly newsletter:

DISCLOSURE: This communication is on behalf of eShares Inc., d/b/a Carta Inc. (“Carta”). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. ©2023 eShares Inc., d/b/a Carta Inc. (“Carta”). All rights reserved. Reproduction prohibited.