For venture capital, more money has led to new challenges. With U.S. venture smashing records for funds raised and funds deployed in 2021, the sector has become more competitive on both sides of the table: Entrepreneurs are able to be more selective about who they invite onto their cap tables, and VCs are fielding increased demand from limited partners (LPs) who want access to venture deals at earlier stages.

What does this mean for the future of the U.S. venture ecosystem? One place to look for new trends is the formation of first funds by new venture firms, which are developing unique strategies to compete for early-stage deals.

Carta’s Fund I report identifies trends in first-fund formation by offering a glimpse into our rapidly expanding data on initial funds. This report covers:

-

The number of new first funds on Carta’s platform by year

-

The size of first funds entering the market

-

Who’s investing in first funds at each size

-

Where new first funds are forming

Why first funds?

At Carta, we believe many of today’s emerging managers will become leaders in tomorrow’s venture ecosystem. Our goal is to support them however we can.

Data related to first funds can offer insights into the future direction of the venture sector. It can help emerging managers understand how their funds compare to other first funds in the market. But while the venture industry closely monitors VC investment and fundraising, very little analysis is dedicated to first funds, in part because so little data is available. By sharing our insights on trends in first-fund formation, we can help emerging managers better understand how their peers are forming and managing their first funds. And by raising transparency, we hope to lower barriers to entry in venture capital. When more people understand the basic mechanics of fund formation, fundraising, and venture investment, we’ll see a more diverse and inclusive venture ecosystem.

First funds on Carta

In this report, we’re including first funds from U.S. venture firms that made their first investment in a company in 2021. First funds are not necessarily managed by first-time VC fund managers: Some GPs of first funds may be experienced investors spinning out of more established firms.

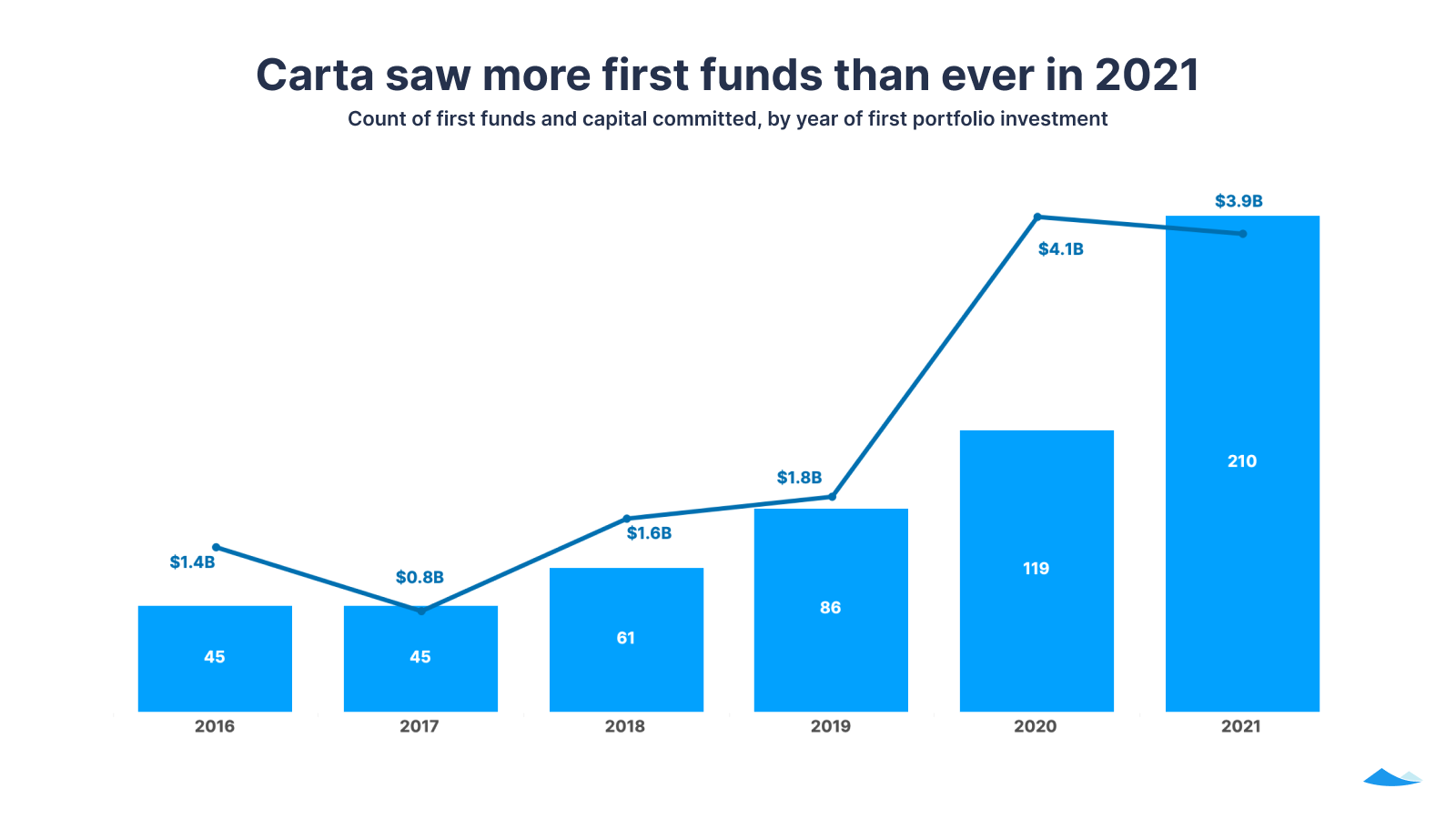

As of January 27, 2022, there were 664 first funds on Carta located across 36 states. These funds held a total of $17B in committed capital and had made a total of 9,996 investments. Nearly a third of these funds formed in 2021—a 76% year-over-year increase.²

The annual total of capital raised by first funds on Carta is also on the rise: In 2020, capital raised on Carta’s platform more than doubled. Capital raised by funds formed in 2021 is likely to exceed 2020’s record, as some funds formed in 2021 are still accepting new capital.

Note that because our historical data is limited, in some graphics years prior to 2021 are grouped (e.g. 2016-20) to increase sample sizes.

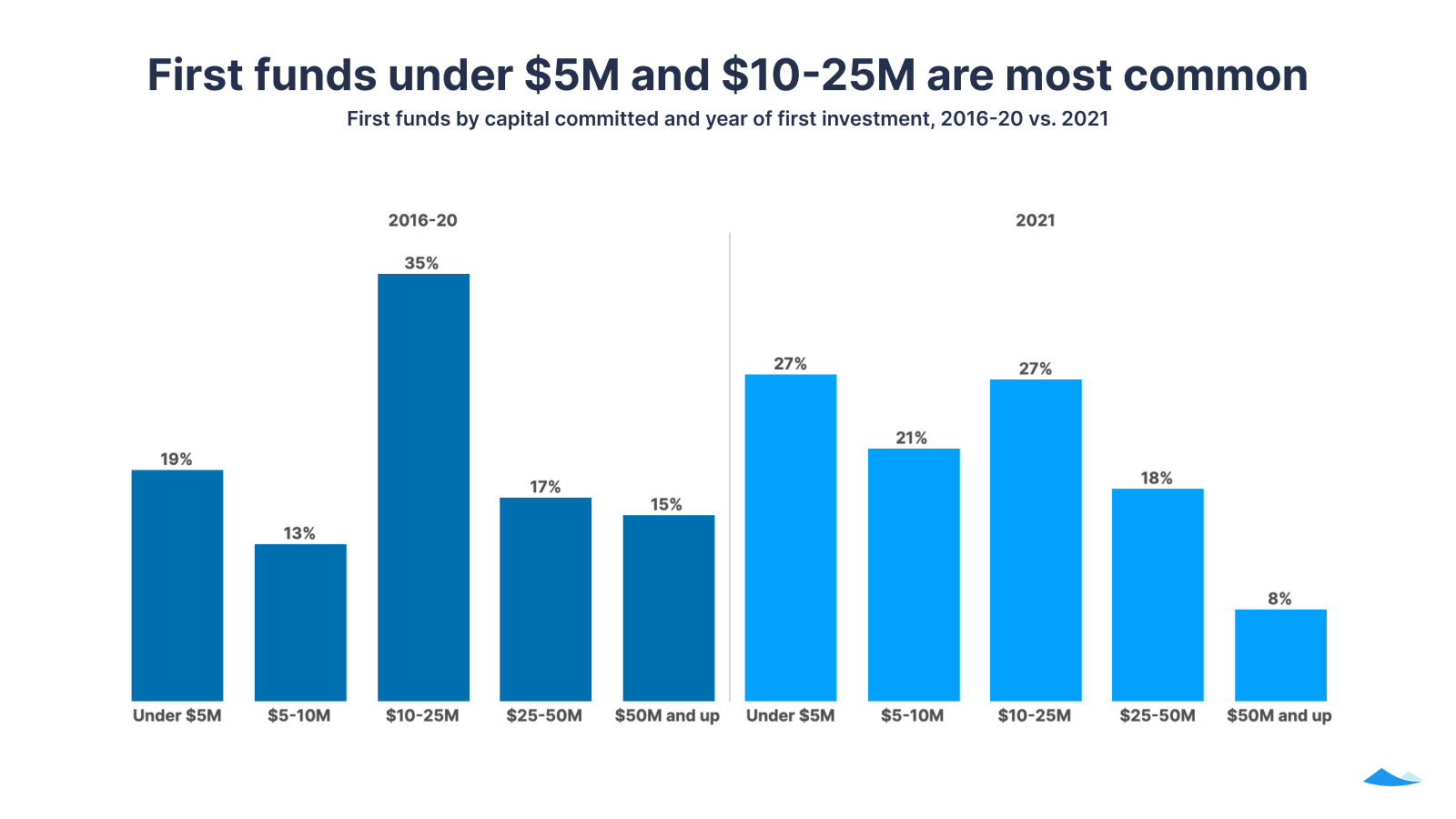

Fund size

Carta data shows there’s no such thing as a typical size for a first fund.

Nearly half (48%) of first funds formed on Carta in 2021 are below $10M in committed capital as of January 27, 2022. Another 45% are between $10M and $50M. Just 8% were $50M or more. Among funds in higher capital commitment tiers, most were formed in the first half of 2021 and have had more time to grow than funds formed in the latter half of the year. We expect to see more funds move into higher tiers in the coming months, as some continue to add LPs and committed capital.

While fund size varies considerably, the median size for a first fund has consistently been greater than $10M. Under Section 3(c)(1) of the Investment Company Act of 1940, funds remain exempt from the definition of an investment company (and related regulatory requirements) if they have no more than 100 beneficial owners. Venture funds can also remain exempt with up to 250 beneficial owners as long as they have $10M or less in committed capital. Carta data shows that while this broader exemption is available for funds of $10M or less, the vast majority of Fund I managers are raising larger funds with fewer LPs.

A median fund size consistently larger than $10M may reflect increased willingness among larger LPs—including some institutional LPs—to support emerging managers, as it is difficult to raise more than $10M without them.

LP types

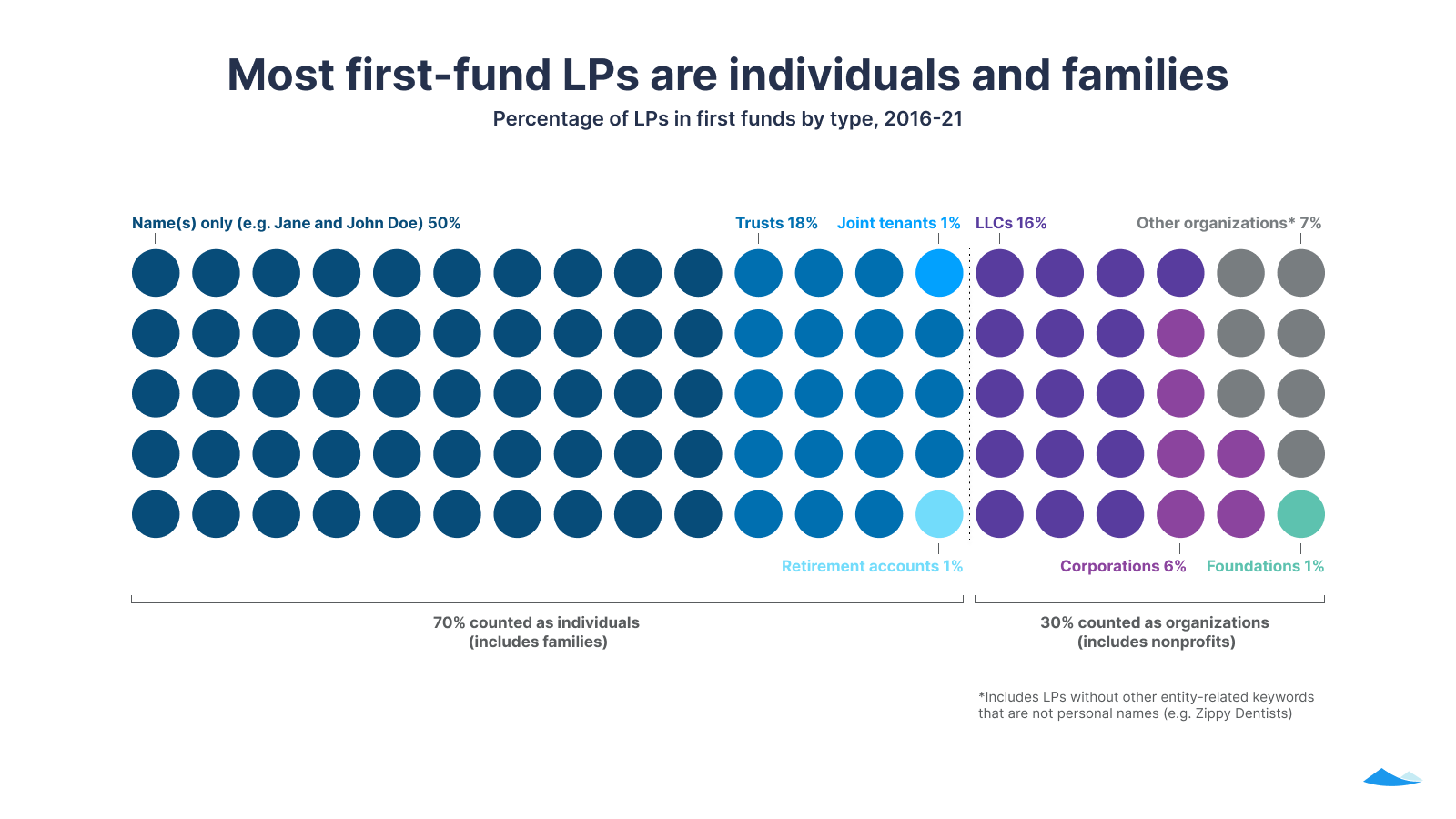

Though there are anecdotal signs that more large and institutional LPs are beginning to support first funds, managers of first funds remain more likely to work with individuals rather than organizations. Half (50%) of investors in first funds are identified on the Carta platform only by one or more people’s names, such as “Jane and John Doe.” Trusts comprise another 18% of investors, whether they hold the assets of an individual or family. By grouping individual names, trusts, retirement accounts, and joint tenancies together, we count 70% of LPs in first funds as unincorporated individuals and families.

The next largest entity type is LLCs, which comprise 16% of first-fund limited partners. LLCs include investment funds; individuals or families who choose to invest as an LLC, whether they have a family office or not; and a variety of other business entities, including some whose primary purpose is not investment.

LLCs are followed by corporations at 6% of LPs; foundations, museums, and universities together comprise another 1%. A final 7% have an unknown entity type, but their names indicate that they’re more likely to represent businesses than individuals or families. Altogether, for this analysis we counted 30% of limited partners as a business or other organization in one of these groups.

The flexible use of business entities like LLCs and corporations means these percentages are estimates based on the available data, rather than precise tallies. For example, an individual or family may invest via an LLC, corporation, trust, joint tenancy, or retirement account. We also see limited partners—whether they are individual people or organizations—operating under multiple entities, such as Jane Doe Investments 2020, Jane Doe Investments 2021, etc.

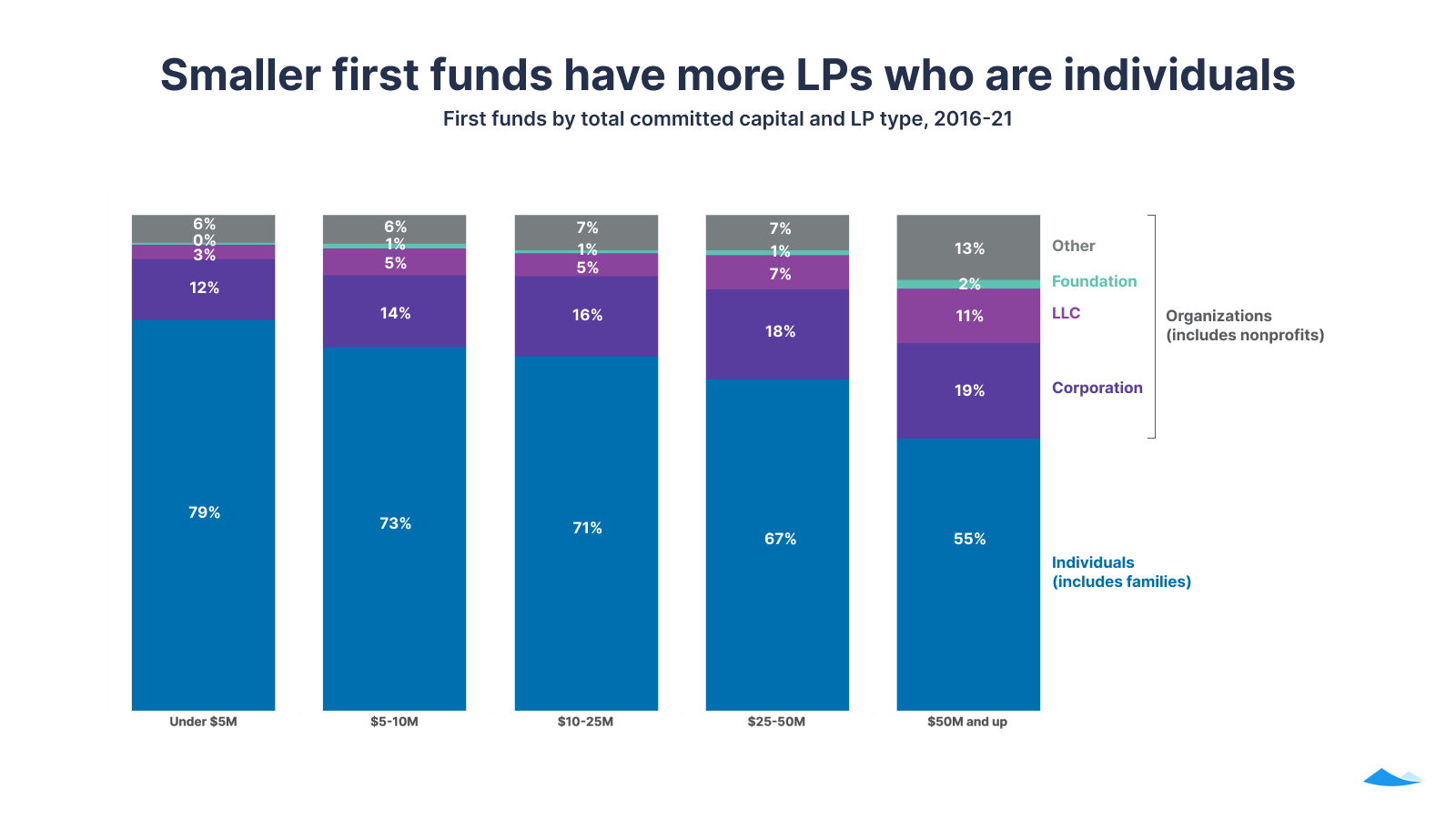

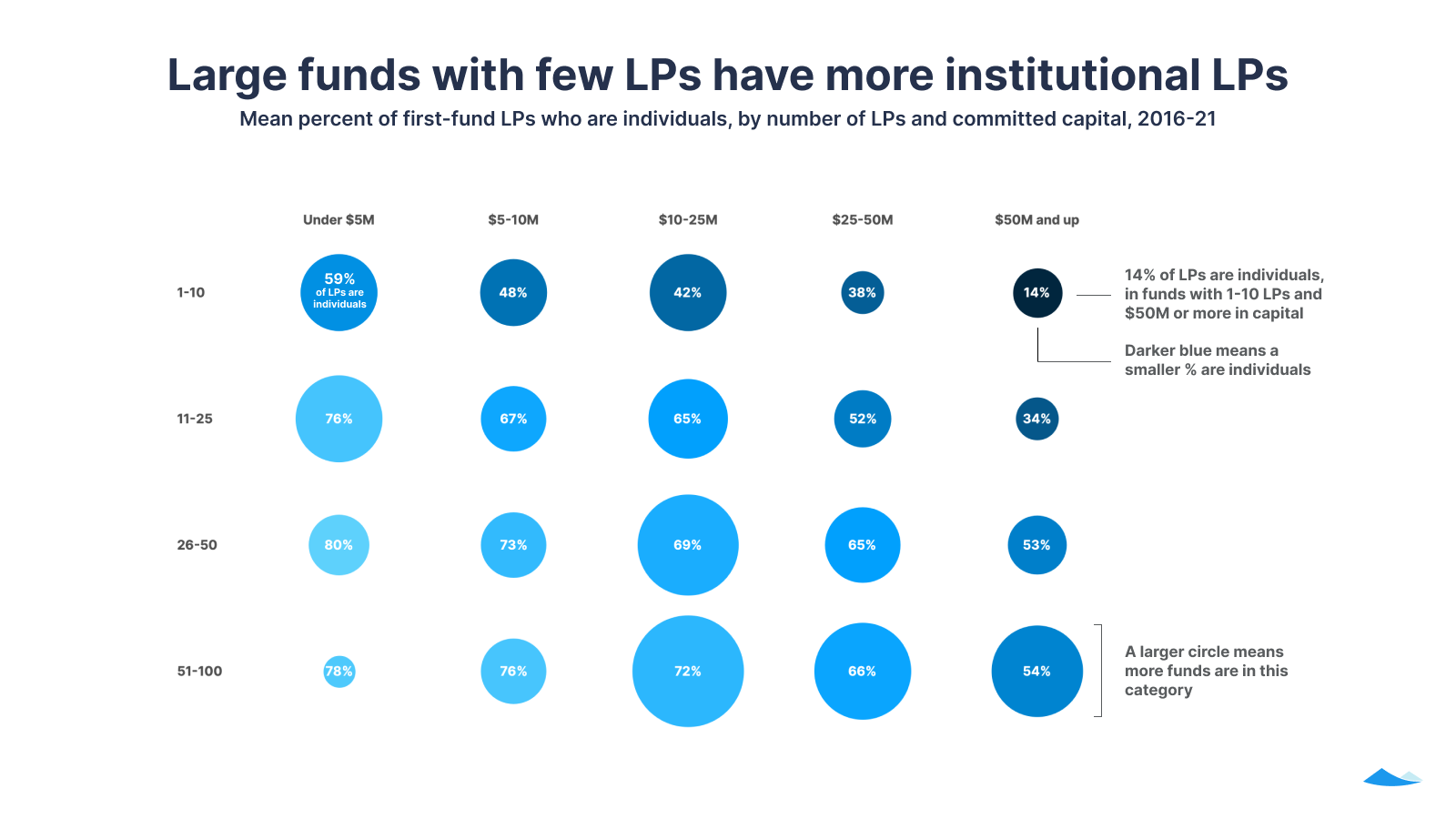

LP types by fund size

In general, the larger the fund, the smaller the share of its LPs who are individuals or families. Among the largest first funds, $50M and up, we classified nearly half (45%) of LPs not as individuals but as LLCs, corporations, foundations, or other entity types. This distribution has remained largely stable from 2016 through 2021.

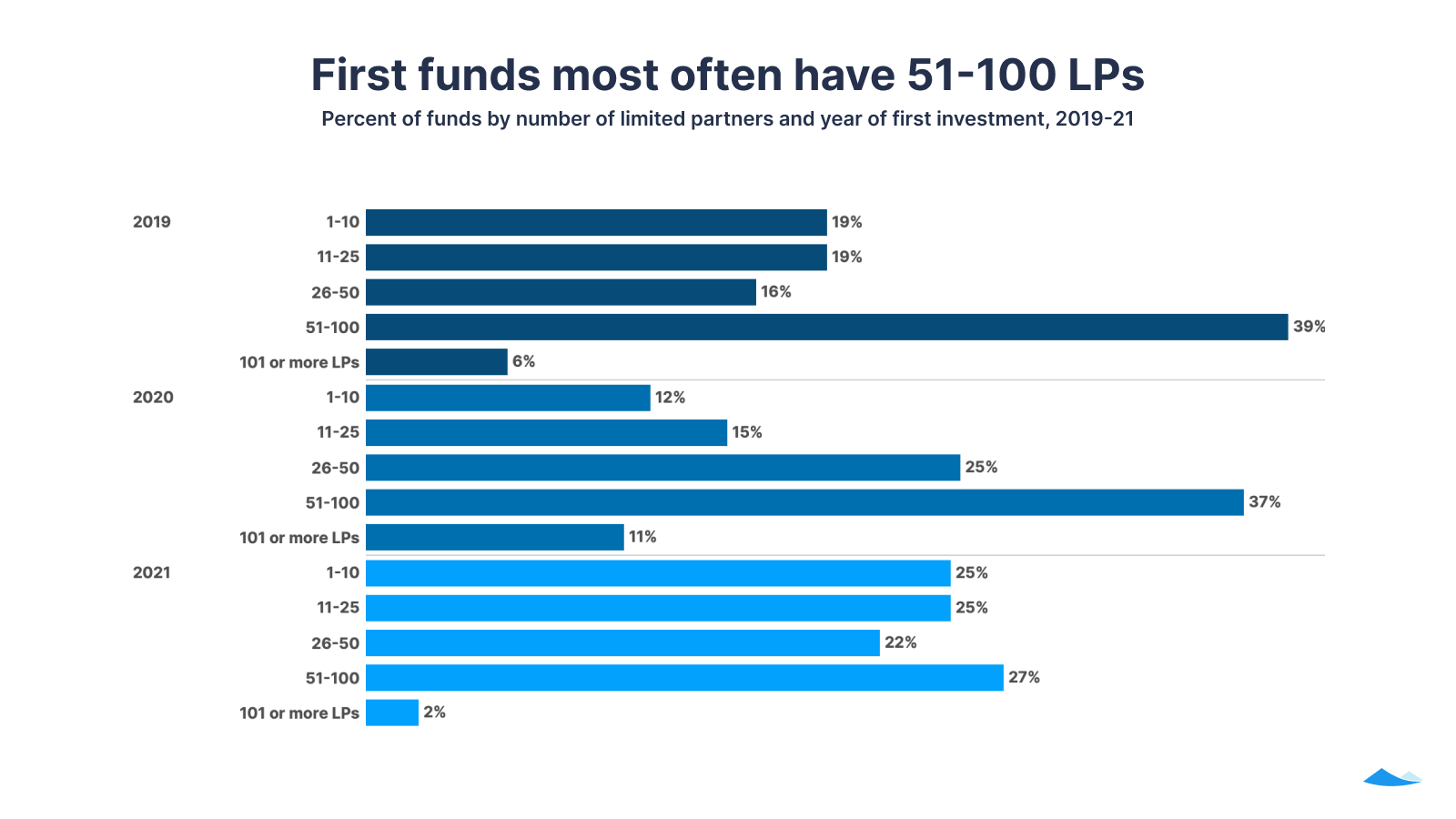

Number of LPs

Among funds formed in 2021, only 2% currently have more than 100 LPs as of January 27, 2022, as compared with 6 and 11% of funds formed in 2019 and 2020, respectively.

First funds included in this report have begun calling capital; they are not necessarily closed to investors. Funds formed in the latter half of 2021 have had less time to add LPs, and as of January 27, 2022 are considerably less likely than funds formed in the first half of the year to have 50 or more LPs. As in the two preceding years, we expect a strong plurality of 2021’s first funds to eventually have 51–100 LPs.

LP counts and types

Funds with 51 to 100 LPs and between $10M and $25M in committed capital comprise 11% of all first funds, making this the most common configuration.

While funds vary considerably in how they assemble their capital commitments, there are also some clear patterns, especially at the extremes. For example, no fund that reached $50M or more in committed capital with fewer than 10 LPs had more than four individuals among their investors. On average, 86% of investors in this group are businesses or organizations according to our analysis, and each of these investors would have had to contribute an average of $17M or more to create the funds in this tier.

In contrast, the median fund with under $5M in committed capital had 15 LPs, of which 11 were individuals. Among funds of this size with 51–100 LPs, the median fund had $4.5M in committed capital from 53 LPs, who would have had to commit an average of under $85,000 each.

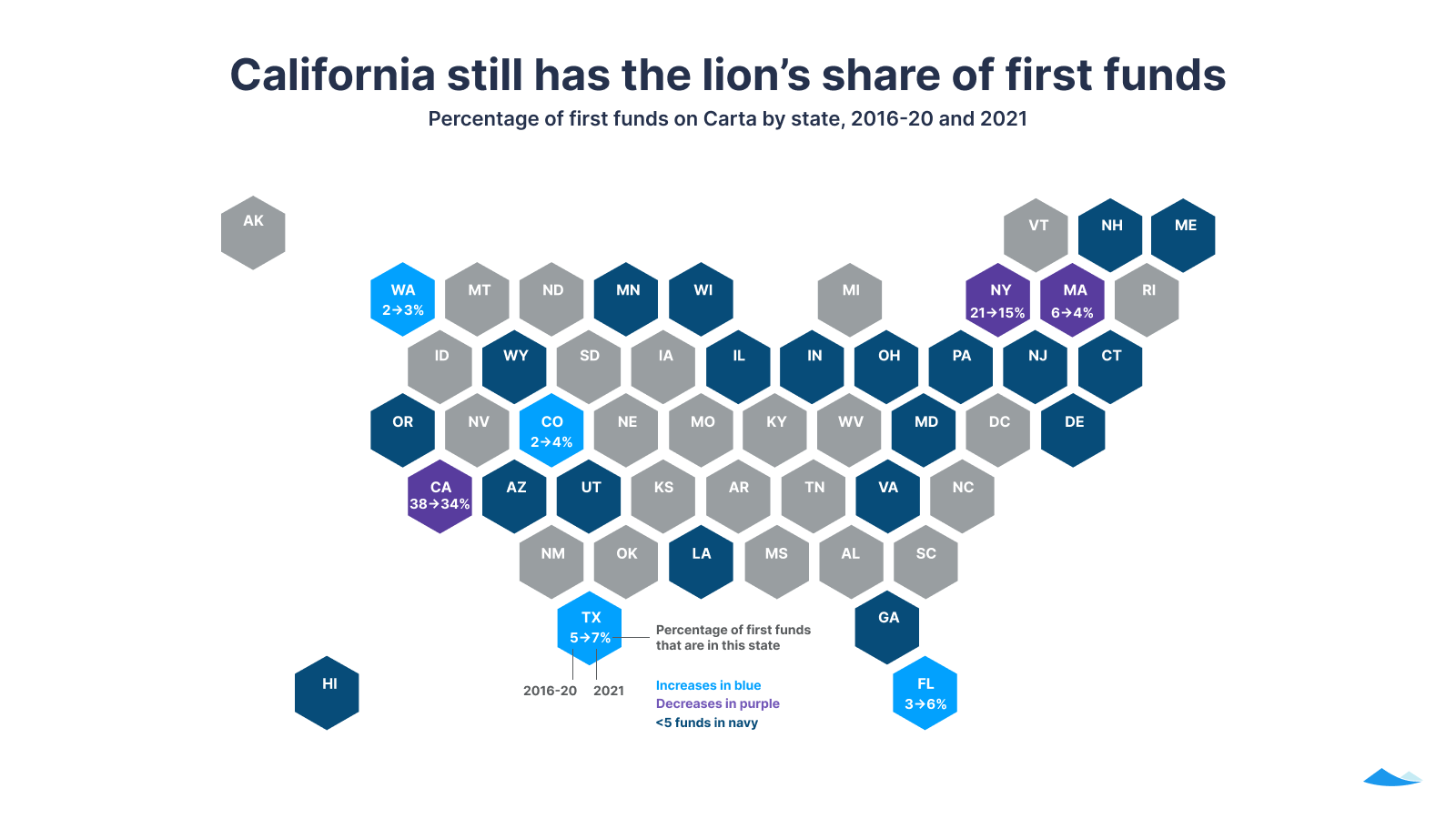

First funds by state

The geographic distribution of first-fund formation in 2021 suggests that new regional venture hubs will continue to grow as venture capital firms spring up far from traditional enclaves like Manhattan and Silicon Valley.

This map shows first-fund formation by state from 2016 to 2020 compared with 2021, and provides evidence of increasing geographic diversification in funds launched by new venture firms.³ While California and New York remain dominant in first-fund origination, both states saw a smaller percentage of the total number in 2021. Declines in New York (six percentage points) and California (four percentage points) mark a shift of ten percentage points to other states. Increases in Texas (two percentage points) and Florida (three percentage points) account for half of the gains outside California and New York.

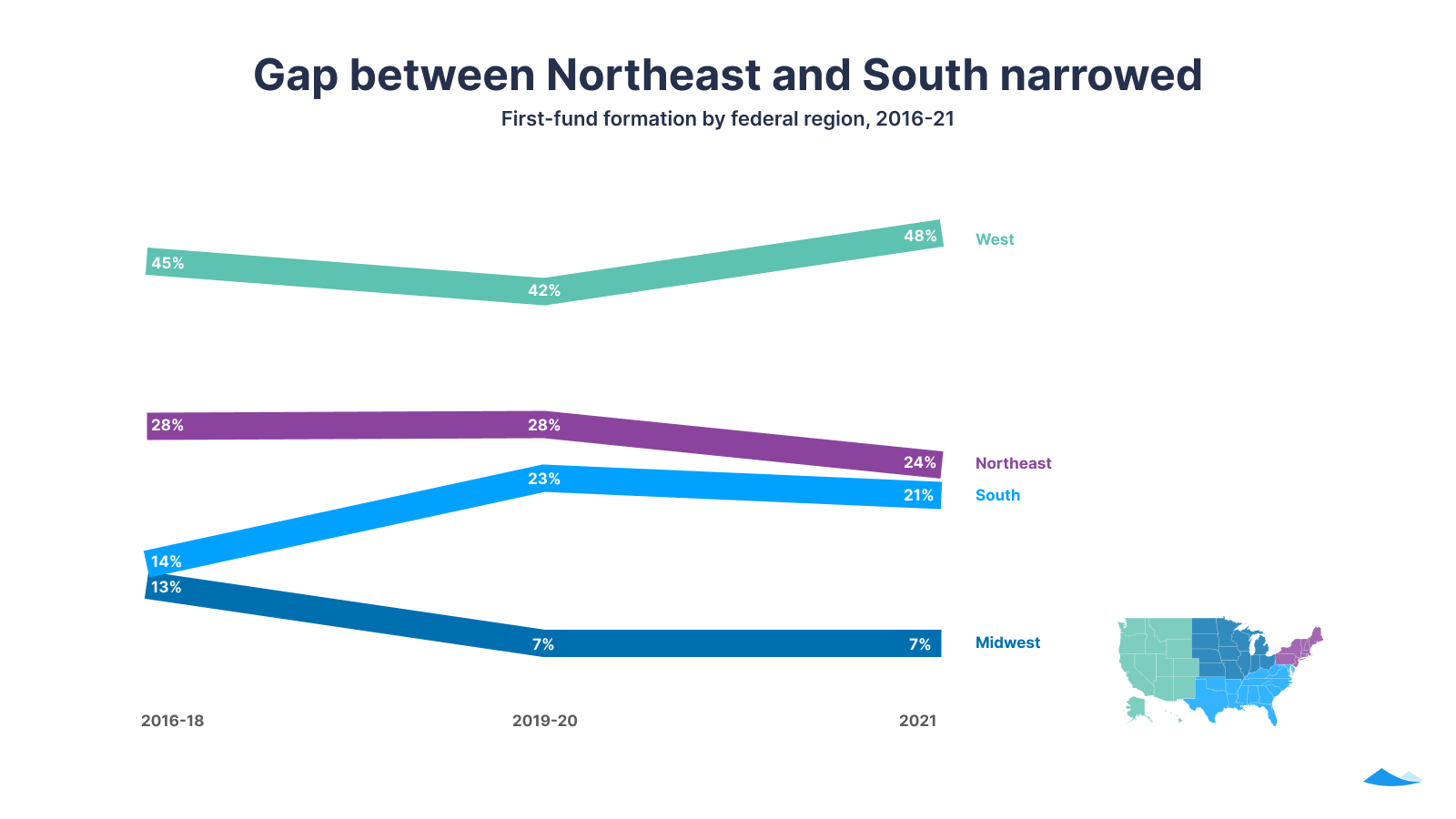

First funds by region

Looking at a broader regional scale, we see that while the West continues to see nearly half of all new first funds, the South now rivals the Northeast.

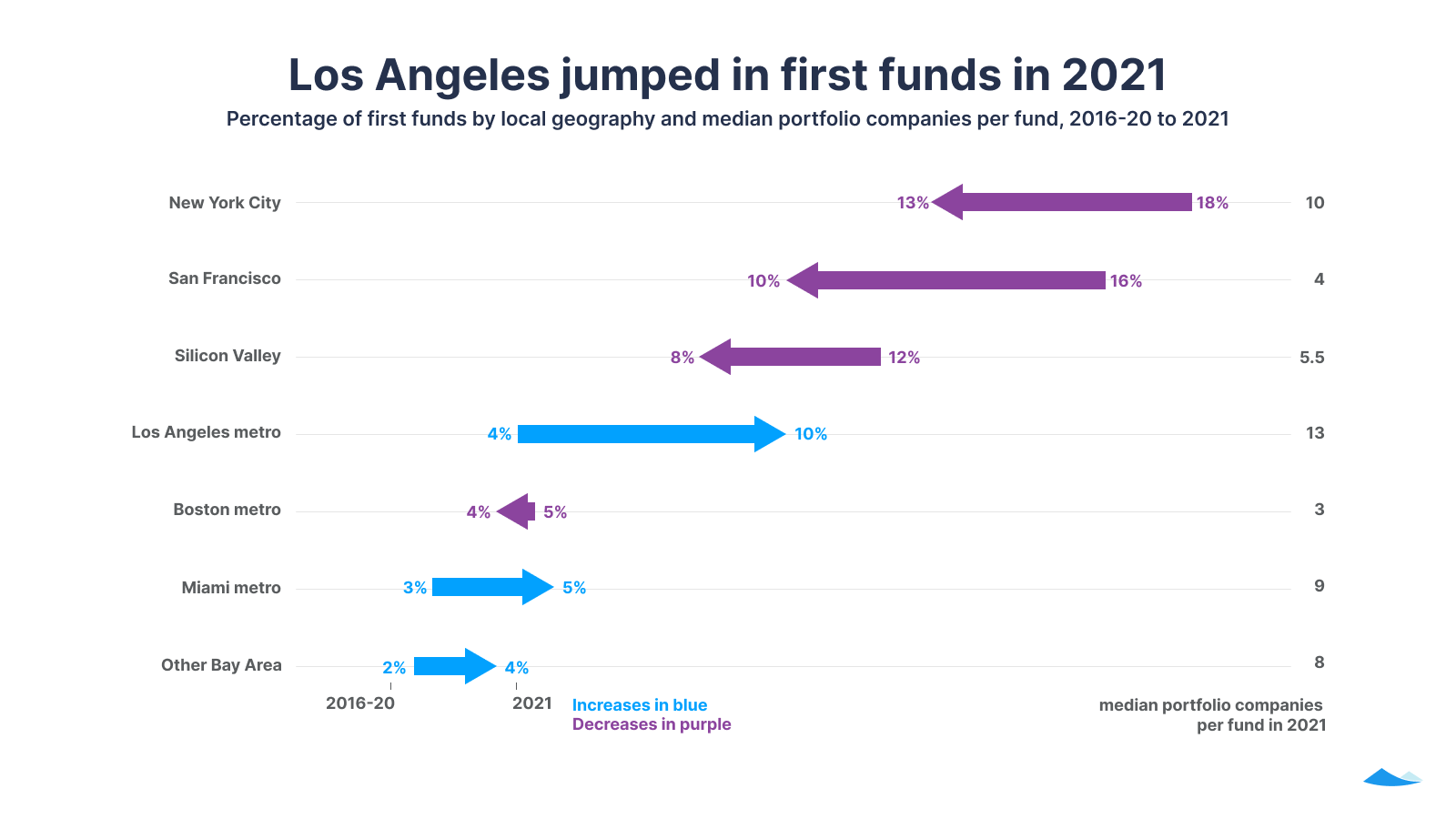

First funds by local geography

When we shift our focus to cities and metropolitan areas, we find more detailed evidence for the geographic diffusion of first funds.

While New York City continues to lead with 13% of first funds formed in 2021, this represents a decrease of five percentage points from 2016-20. San Francisco and the neighboring Silicon Valley region also declined by six and four percentage points, respectively. Taken together, the combined Bay Area region declined from 30% of first funds formed in 2016-20 to 22% formed in 2021. (See our methodology section for geographic definitions.)

Meanwhile, the Los Angeles metro grew by six percentage points. First funds in LA also made more portfolio company investments than their counterparts in other metro areas, with a median of 13 portfolio companies as compared with five for funds across all other regions (including those not shown here). The growth of first funds in the Los Angeles metro, combined with the high number of companies they support relative to other regions, suggests that the hype surrounding VC flight to Miami may have distracted from another trend: the rapid growth of the Southern California venture ecosystem. This is a pattern we’ll monitor as our dataset grows.

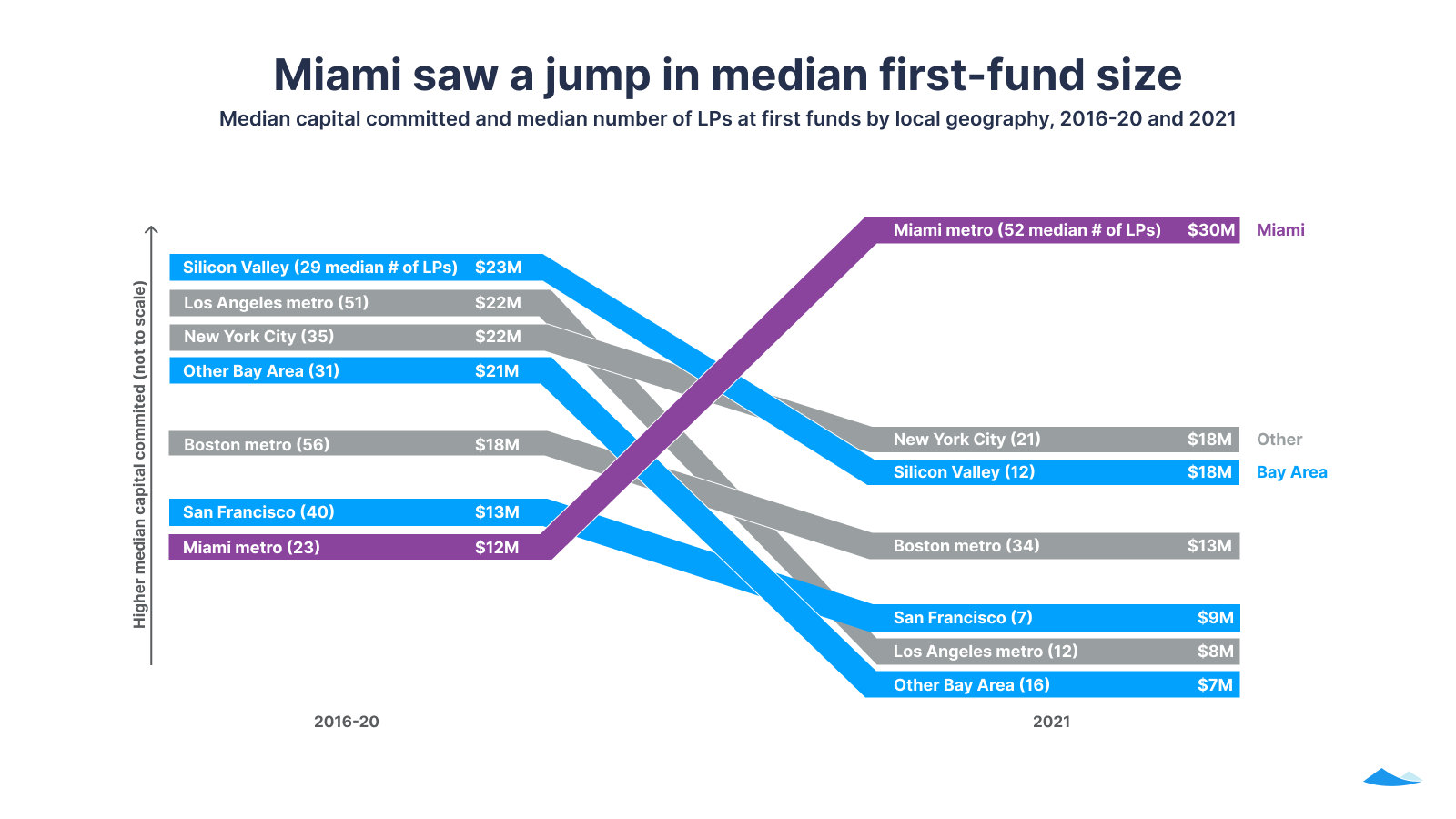

Fund size by local geography

Median fund size surged in Miami as it declined in other major regions, offering evidence for the heightened pace of venture fundraising in Miami relative to other top locations. Some, but likely not all, of this difference may be due to funds in Miami starting earlier in the year, with a median first investment date three weeks earlier than funds elsewhere.

Other possible reasons for this leap include the possibility that a larger share of first funds in Miami were launched by venture capitalists spinning out of more established firms, or established firms incorporating under a new entity for a new fund. Our finding is based on relatively few data points, with Miami having nine new first funds on the Carta platform in 2021. We will watch to see if this apparent trend solidifies in 2022.

Regional differentiation

The growth of first-fund formation outside traditional venture centers in Manhattan and the Bay Area reflects a stated ambition we’ve heard from emerging fund managers: specializing in sourcing deals from overlooked geographies and populations.

As Marcus Stroud, general partner of the Texas-based TXV Partners (founded 2018), explained on Carta’s podcast, The First Close, last year, Texas “is a very innovative, diverse, and unique place where people from all over the world come to create.” Being in Texas, he says, helps TXV take a more active role in leveraging their network to help portfolio entrepreneurs connect with advisers and hire talent.

Many funds formed on Carta in 2021 have a strategy that relies on privileged access to local deal-flow in the partners’ networks.

Conclusion

As our dataset grows, we’ll learn even more about Fund I formation in the U.S. When the data presents new patterns and insights, we’ll continue to share them.

The Fund I report is one among several reports the Carta data team produces. Visit the Carta Data Desk for the latest reports, and for additional updates on data findings related to startup capital raising, venture investment, and equity dilution.

Download a PDF of the Fund I report: 2021 year in review.

For questions about this report, write to us at insights@carta.com.

Methodology

Carta’s Fund I report examines the first funds of venture firms to provide more transparency into the basic mechanics of first-fund formation, fundraising, and venture investment. This report uses aggregated and anonymized data of 664 funds—which represent $17B in committed capital and a total of 9,996 investments in the startup ecosystem.

Overview

Carta provides fund administration services for more than 5,400 funds, representing over $70B in assets under administration. This study uses an aggregated and anonymized sample of Carta’s data related to first funds. Customers that have contractually requested that we not use their data in anonymized and aggregated studies are not included in this analysis.

The data presented in this report represents a snapshot as of January 27, 2022. Historical data may change in future studies because there is typically an administrative lag between the time a transaction or material change to a company takes place and when it is recorded in Carta.

Note that because our historical data is limited, some graphics in this report group years prior to 2021 (e.g. 2016-20) to increase sample sizes.

Regions

We use the word “metro” as shorthand for “metropolitan statistical area.” As such, the Los Angeles metro refers to the Los Angeles-Long Beach-Anaheim metropolitan statistical area; Miami metro refers to the Miami metropolitan statistical area; Boston metro refers to the Boston-Cambridge-Newton metropolitan statistical area; and New York metro refers to the New York-Newark-Jersey City metropolitan statistical area. For the Bay Area, we include the San Jose-San Francisco-Oakland combined statistical area. We also look at subsets of the Bay Area as follows: the city of San Francisco; Silicon Valley, in which we include Santa Clara and San Mateo counties; and Other Bay Area, in which we include Alameda, Contra Costa, Marin, San Benito, San Joaquin, Stanislaus, Sonoma, Solano, Merced, Santa Cruz, and Napa counties (the counties of the San Jose-San Francisco-Oakland combined statistical area that are not San Francisco or Silicon Valley).

Categorization of LPs

LP types were categorized by parsing the LP’s name. Natural person(s) refers to LP names that contain one or more personal names without other prefixes or suffixes, except name-related ones such as “Dr.,” “Mrs.,” or “Jr.” Trust refers to LP names that include the word “trust.” Retirement accountincludes LP names that include terms such as “401(k),” “IRA,” or “retirement.” Joint tenancy includes terms such as “JTWROS” and “TIC.” LLCs are LPs whose names include “LLC.” Corporation includes LP names with terms like “corp,” “limited,” and “inc.” Foundations, universities, and museums are LPs with these specific terms in their names. Names that indicate a non-natural-person entity such as “Zippy Dentists,” but that did not include other entity information, were included in the Other entity type. Spelling variants of the above keywords were included, and efforts were made to properly categorize LP names that included keywords within larger words.

¹ Carta’s dataset partially overlaps with first-fund studies by other organizations, such as PitchBook and NVCA. While Carta analysis is based on aggregated and anonymized data from Carta’s fund administration clients, other sources depend on publicly available information or self-reported data from funds; each source represents a portion of all first funds.² Some of this increase may reflect Carta’s increasing market share within what PitchBook recently characterized as a declining first-fund market. However, because available data on this segment is thin, the full picture is likely more complex. For example, PitchBook reported 87 funds in 2020, but Carta saw 119 funds call capital for the first time that year. While our datasets overlap, neither count is complete.³ Fund locations here are based on firm mailing addresses; percentages are calculated from the 82% of first funds in our database that list a mailing address.