The secondary market for private stock continued to grow in 2019, building on the momentum generated in 2018 where an estimated $30B changed hands. In 2019, we saw an estimated $5B in notional volume in the tender offer market alone.1 In reviewing the transactional catalysts driving this volume, several indicators suggest this deal velocity is here to stay in 2020 and beyond.

A meaningful part of the secondary deal flow we have seen on Carta and across other platforms appears to be driven by the proliferation of growth equity and late-stage venture strategies in recent years. These strategies have triggered a series of second order effects that have fueled secondary deal volume in recent years, including:

-

IPOs occurring later in the company’s life cycle

-

The continued ascendancy of “mega rounds”

-

Increased demand for the best companies following primary rounds

-

Hybrid primary/secondary capital raises allowing large investors to meet ownership targets while controlling dilution

The new normal

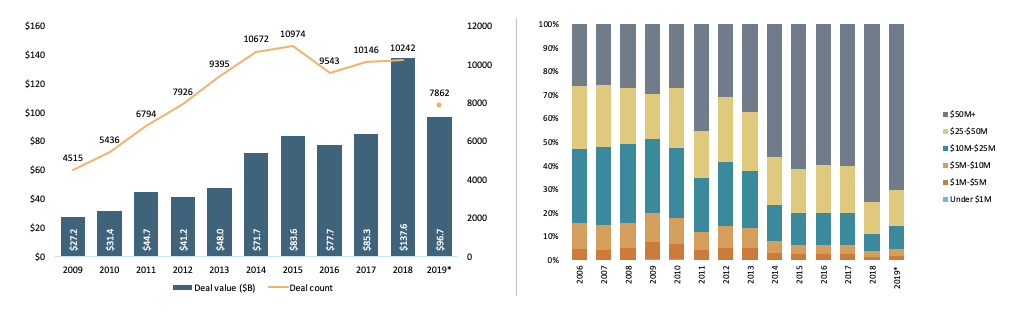

Growth equity deal value had a breakout year in 2018, and is expected to have surpassed $65B in 2019, with a meaningful allocation to tech and software. Similarly, late-stage venture strategies allocated nearly $60B through Q3 of 2019, and are expected to have eclipsed $80B. As growth equity has continued to flourish, we have also seen late-stage venture try to compete for deal flow with larger check sizes, with over 70% of late-stage venture deals being $50M+ in the last couple of years. The convergence of late-stage venture and growth equity has introduced a broader investor base that is seeking alpha from high growth startups.

Growth equity investments continue to trend towards new highs, and late-stage VC deals continue to get larger. Source: 3Q 2019 PitchBook-NVCA Venture Monitor.

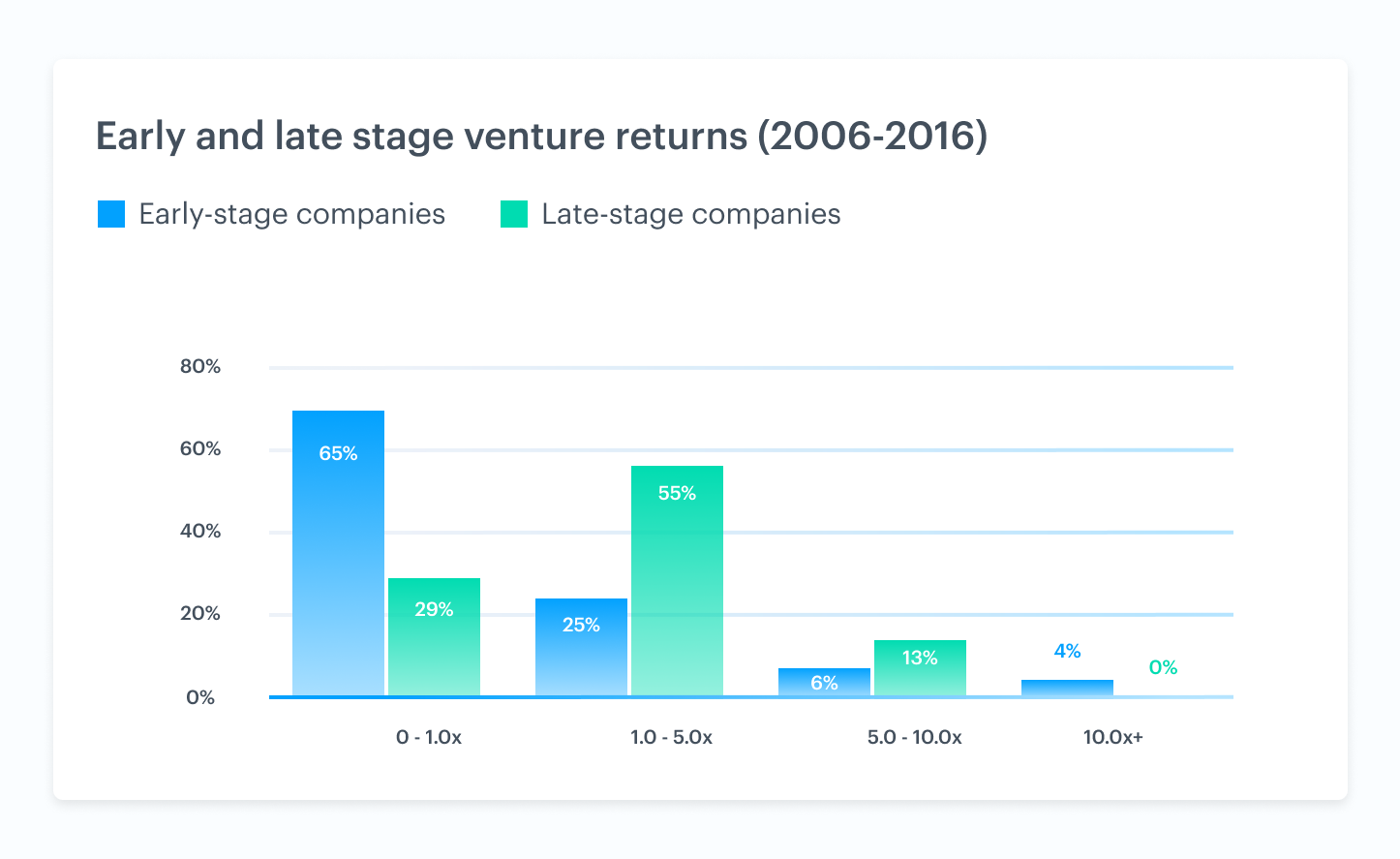

A closer look at the distribution of investment returns across early and late-stage venture strategies between ‘06 and ‘16 shows why late-stage investing has become so attractive to LPs. 68% of late-stage backed companies were likely to return 1-10x, while 63% of investments in early-stage companies won’t even return their initial committed capital. Additionally, aside from lower rates of capital impairment, recent years have shown that growth equity returns can rival those of traditional early stage venture. Against this backdrop, it’s no surprise that we have seen an explosion in growth equity and late-stage venture.

The return profile for late-stage companies has become increasingly attractive for investors seeking a mix of significant upside and mitigated downside. Source: Industry Ventures

|

Company |

Lead VC |

Deal Date |

Valuation (M) |

Current Valuation (M) |

Estimated IRR |

Time (Years) |

|---|---|---|---|---|---|---|

|

Zoom |

Sequoia |

1/17/2017 |

$885 |

$25,230 |

267% |

2.6 |

|

Crowdstrike |

Accel |

5/11/2017 |

$925 |

$19,273 |

283% |

2.3 |

|

Slack |

KPCB |

10/31/2014 |

$1,000 |

$15,518 |

77% |

4.8 |

|

PagerDuty |

Accel |

4/26/2017 |

$650 |

$2,720 |

86% |

2.3 |

|

Lyft |

Coatue |

4/2/2014 |

$721 |

$15,956 |

78% |

5.4 |

|

Uber |

GV |

8/23/2013 |

$3,460 |

$57,732 |

60% |

6.0 |

Larger rounds are marked by increased investor collaboration, as firms try to allocate capital to the likely category winner. Source: 3Q 2019 PitchBook-NVCA Venture Monitor.

What does all of this mean for the secondary market?

Longer runways for companies

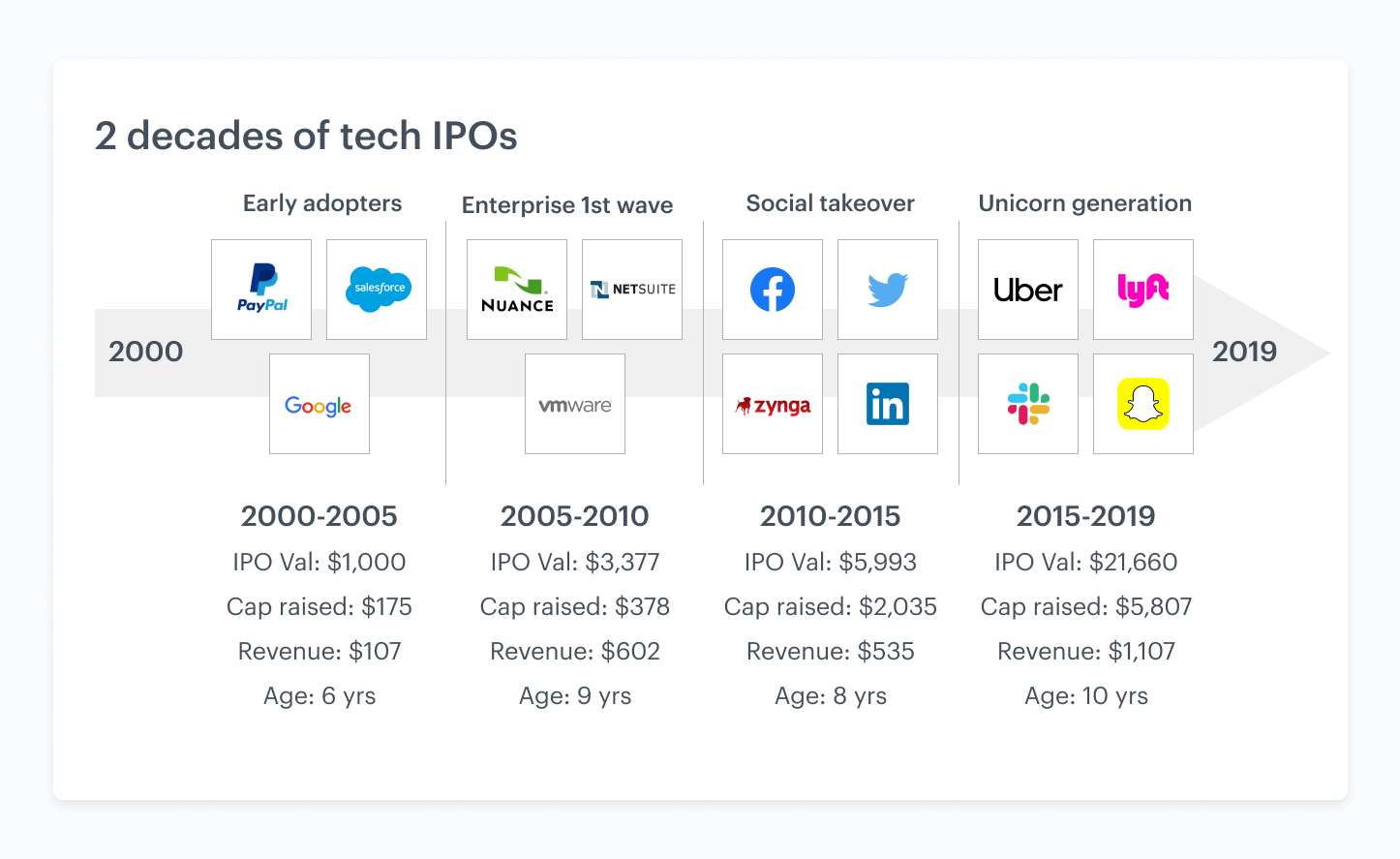

As more and more capital is piling into the most attractive companies later and later into their lifecycle, coupled with their ability to raise awareness and cultivate a powerful brand while private, the typical catalysts for going public are diminishing. This means that for early employees and investors, the time to exit is extending and as a result, pre-exit liquidity is increasingly important. A look at IPOs over the last two decades further evidences the evolution of the IPO company from hyper-growth startup, to mature operating business. As this lifecycle becomes the norm, companies will need tools like secondary liquidity to leverage in the intense battle to attract, incentivize, and retain top talent, and investors will need ways to realize gains and return capital to investors for the next fund.

Institutions continue seeking alpha

As companies stay private longer and growth and late-stage strategies continue to outperform on a risk weighted basis, traditional VCs will continue migrating to multi-strategy fund models, and the traditional institutional investors will continue seeking alpha in the private markets. However, for the most promising companies, secondary transactions are the only real option for many investors to take a position. In some ways, more traditional institutional investors are better positioned to drive secondary volume, considering they don’t face the same limitations on secondary purchases that many venture capital firms face under the law. For this reason, we expect more VC firms to register as Investment Advisors to avoid this limitation, like Andreessen Horowitz (an investor in Carta) recently did. As we continue to see a more diverse mix of investors enter the market for growth and late-stage companies, secondary liquidity events will continue to be an important entry point.

More big deals

As check sizes continue to grow and early investors, founders, and employees continue to be more expectant of pre-exit liquidity, we will continue to see companies with excess demand following large rounds that can be put to work in secondary transactions. In addition, because these large growth and late-stage rounds can carry heavy dilution penalties for investors, we also expect that some companies will continue structuring hybrid primary/secondary rounds that allow new investors to hit their ownership targets while controlling dilution.

“Megarounds” have become an increasingly prevalent part of the larger VC funding landscape. Source: Pitchbook.

Bottom line

As these trends in VC and private equity persist, we should expect for the secondary market to continue blooming, and companies and investors will need to develop and hone their secondary market strategies.

1 Our estimate represents an annualized figure derived from Carta tender offer volume, as well as reported tender offer volume statistics from Nasdaq Private Markets.

© 2021 Carta Capital Markets, LLC (“CCMX”). All Rights Reserved. CCMX Member FINRA/ SIPC. CCMX undertakes no obligation to update content herein. No business, investment, tax, or legal advice is provided by CCMX. Potential investors are advised to conduct their own due diligence and consult with their tax, legal, and financial advisors with respect to any investment. All securities involve risk and may result in partial or total loss. Investments in private securities are speculative, illiquid, and involve a high degree of risk, including the possible loss of the entire investment. There is no guarantee that a private company will conduct an initial public offering or provide an alternative exit strategy for invested capital. Images are illustrative and may differ from application experience.