A 409A valuation is an independent appraisal of the fair market value (FMV) of a private company’s ordinary shares (the underlying security reserved mainly for founders and employees) on the date of issuance. This valuation is based on guidance and standards established in section 409A of the IRS’s Internal Revenue Code (IRC).

If you offer equity to employees or advisors who are US citizens – even if they reside outside of the US – you need a 409A valuation to be compliant with the IRS. Understanding the fair market value before you issue equity is crucial, unless you want to risk severe penalties for your company and its equity holders.

We’ll help you understand the basics of a 409A valuation so you can choose a valuation provider with confidence. To see what one looks like, download a sample 409A valuation report below.

Do I need a 409A valuation?

If you plan to offer equity to employees who are subject to US tax law, it is best practice to obtain an independent 409A valuation before issuing your first share option grants. Early-stage companies and founders also need 409A valuations to prevent shareholders from paying tax penalties that may otherwise be imposed by the IRS. A reputable 409A valuation provider can help you take advantage of safe harbors (more on those below).

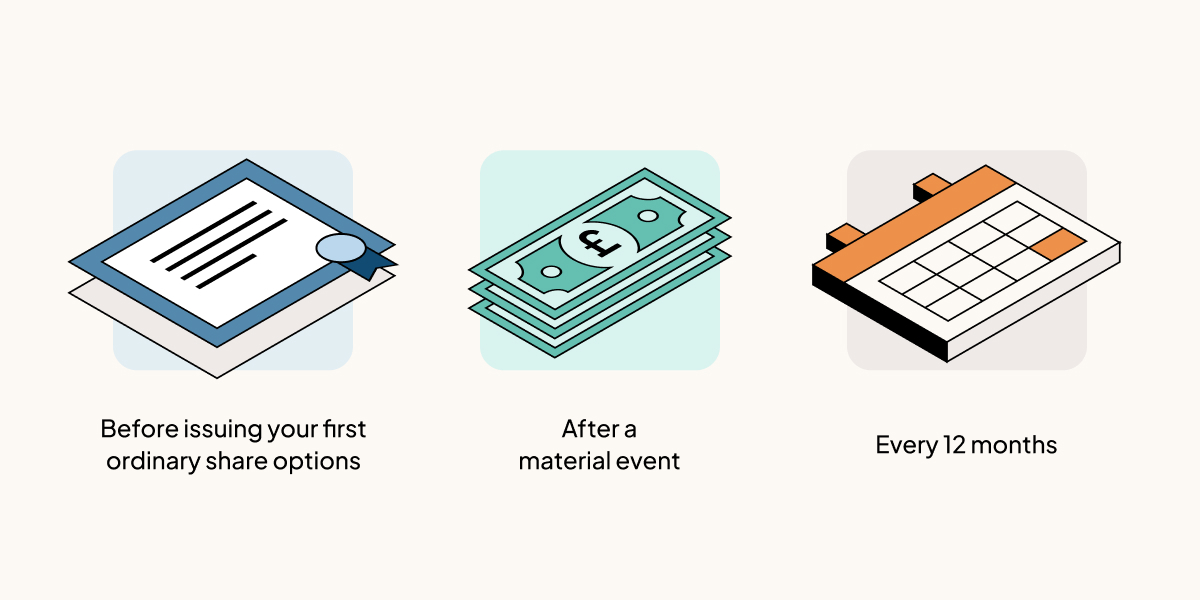

When do I need a 409A?

You should get a 409A valuation:

-

Before issuing your first ordinary share options

-

After raising a round of venture financing

-

Once every 12 months (or after a material event)

-

If you’re approaching an IPO, merger or acquisition

How long are 409A valuations valid?

IRC 409A valuations are valid for a maximum of 12 months after the effective date, or until a material event occurs. A material event is something that could affect a company’s share price.

For most early-stage startups, the most commonly encountered material event is a qualified financing. This event typically includes a sale of ordinary shares, preferred equity or convertible debt to independent institutional investors at a negotiated price.

What is a 409A material event?

Aside from a qualified financing, other events that may be considered material include:

-

A significant, new or lost contract that represents a material change in revenue, including annual recurring revenue (ARR)

-

Any material, closed acquisition with your company as the buyer or seller

-

A term sheet received from a potential acquirer

-

A strategic partnership that is likely to open new markets or improve margins

-

Regulatory changes that significantly increase or decrease your total addressable market (TAM)

If you aren’t sure, reach out to a 409A valuation provider or consult a lawyer.

What is IRC Section 409A?

In response to the 2001 Enron scandal, regulators looked for ways to prevent executives from taking advantage of equity loopholes. The IRS subsequently introduced IRC Section 409A in 2005; a final version came into effect in 2009.

Section 409A contains a framework for private companies to follow when valuing shares. When the valuation is conducted by an unaffiliated or independent party, it establishes a “safe harbor”, meaning that it is presumed to be “reasonable” by the IRS – save for a few exceptions.

If a company doesn’t adhere to 409A rules and its equity is priced incorrectly, the IRS can issue penalties. Usually, employees and shareholders end up paying the price.

How much does a 409A valuation cost?

Some providers offer standalone 409A valuations, while others offer bundled services. Standalone valuations can cost thousands, depending on the size and complexity of your company.

At Carta, 409A valuations are included in an annual subscription along with cap table management.

What is a 409A refresh?

After 12 months (or sooner, if there’s a material event), your company will need a 409A refresh – in other words, an updated valuation. Any event that could change the valuation of your company means you need a new 409A.

Download sample 409A valuation report

What is a 409A safe harbor?

When your 409A is handled in a specific way, it’s eligible for safe harbor status. Think of it as peace of mind: a safe harbor valuation is one the IRS presumes to be valid, unless they can demonstrate that it’s “grossly unreasonable”.

The IRS provides three safe harbor methods for setting the FMV of private company ordinary shares:

-

Independent appraisal presumption

-

Binding formula presumption

-

Illiquid startup presumption

The most common approach to achieving safe harbor status is using the independent appraisal presumption (a qualified, third-party appraiser).

A 409A valuation is presumed reasonable if the shares were valued within 12 months of the applicable option grant date, and if no material change has occurred between the valuation date and the grant date. If these requirements are met, the burden is on the IRS to prove the valuation is “grossly unreasonable”.

Common 409A valuation methodologies

Independent appraisers have an obligation to ensure that your 409A and FMV are “fair”. There are three standard methodologies providers use during a 409A: market approach, income approach and asset approach.

1. Market approach (OPM backsolve)

When a company raises a funding round, valuation providers typically use the option pricing model (OPM) backsolve method. It can be safely assumed that new investors paid fair market value for their equity, but investors receive preferred shares so adjustments must be made to determine the FMV for ordinary shares.

Other market-based approaches use financial information like revenue, net income and EBITDA (earnings before interest, taxes, depreciation and amortisation) from comparable public companies to estimate the equity value of a business.

2. Income approach

For businesses with sufficient revenue and positive cash flow, valuation providers often use the straightforward income approach. This method defines a company’s value based on its expected future cash flows, adjusted for risk.

3. Asset approach

The asset approach is often used for early-stage companies that haven’t raised funding and don’t generate revenue yet. This methodology calculates a company’s net asset value to determine a proper valuation.

What do I need for a 409A valuation?

Once you’ve selected a 409A provider, you need to compile and share some important information about your business. As an example, Carta’s requirements are listed below.

Company details

-

Name of your CEO

-

Name of your external audit firm (if applicable)

-

Name of your legal counsel

-

Your amended and restated articles of association

Industry information

-

Your industry

-

A list of relevant and comparable public companies (most 409A valuations rely on some form of comparison to publicly traded companies)

Fundraising and options

-

The most likely timing of a liquidity event

-

Your company presentation, business plan or executive summary

Company financials

-

Historical financial statements

-

Forecasted annual revenue for the next two calendar years, starting from the valuation date

-

Forecasted annual EBITDA for the next two calendar years, starting from the valuation date

-

Non-convertible debt amount

Additional details

-

Any materially relevant events since your last 409A valuation (if this is your first 409A, you should provide a complete history of relevant events)

409A penalties

If your 409A valuation isn’t performed using one of the IRS-approved methods, you could fall outside of the 409A safe harbor. The penalties can be substantial for employees and shareholders:

-

Immediate tax on all deferred compensation from the current and preceding years

-

Accrued interest on the revised taxable amount

-

Additional tax of 20% on all deferred compensation

Most startups aren’t likely to be audited by the IRS. That said, as your company grows and approaches an exit – whether that’s a merger, acquisition or IPO – you could face IRS audits. You’ll save time and effort by working with a reputable valuation provider from the beginning.

Carta provides audit-defensible 409A valuations

Carta is the leading cap table management and 409A valuation provider globally, trusted with over 15,000 valuations each year. We leverage best-in-class software and industry expertise to deliver valuations faster and for less than traditional providers. Speak to a member of our team today if you have any questions or need a valuation.