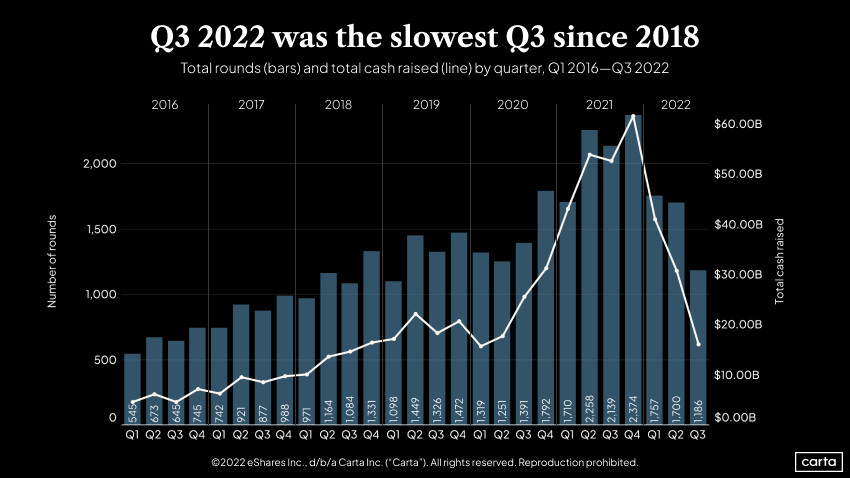

Both deal activity and deal value on the Carta platform have declined in every quarter of 2022, falling back to pre-pandemic levels. That’s a sharp reversal from last year, when startup investment was propelled to new heights. This year, deal volume in Q3 was down 30% from Q2, while cash raised by startups on Carta fell by 48% quarter over quarter. Those declines will likely grow less stark as more companies document their third-quarter deals in the weeks to come.

Nevertheless, startup funding activity remains high relative to most of the past decade, signaling that it might have been 2021—and not 2022—that was the outlier.

Q3 highlights

-

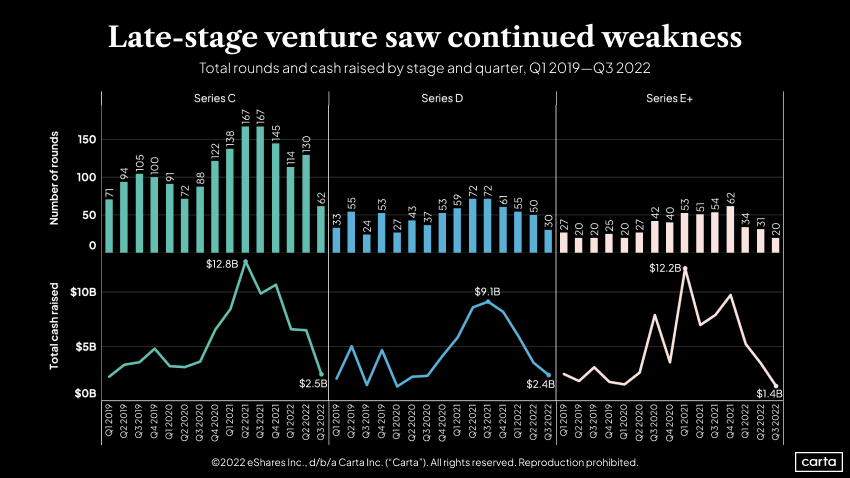

Deal count and cash raised fell most sharply at Series C. The volume of investments declined from last quarter at each stage, but a 52% dip for Series C was the steepest drop. The total amount of cash raised by Series C companies fell 80%, also more than any other stage.

-

The venture slowdown has reached the seed stage. While deal counts and round sizes began to trend down at most other stages in Q2, the seed stage had been resilient in terms of valuations. That changed in Q3, as median seed deal size dropped by 9%—the first decline in eight quarters.

-

Repriced option grants were more common than in any quarter on record. Companies repriced 18,629 stock option grants on Carta, surpassing the old quarterly record by 48%. With private valuations trending down, more companies are lowering the price of their options to make them more appealing to employees.

Note: If you’re looking for more industry-specific data, you can also download the addendum to this report to get an extended dataset.

Last year was largely a good one for the tech industry. Public tech valuations reached new heights—the Nasdaq 100 tech sector index gained 27% for the year—and private investors placed big bets on the tech-heavy startup space.

So far this year, though, the same index is down 40%. And the correlation with private market activity remains: This was the slowest Q3 for venture capital deal activity on the Carta platform since 2018, and the 30% dip in activity compared to Q2 is the largest quarterly decline since at least 2016.

One reason for the slowdown is diverging expectations between buyers and sellers. Investors are eager for a reset in private valuations that would reflect how public valuations have declined, but most companies are hesitant to raise a down round. As investors wait for clarity, companies are tightening expenses to reduce burn and wait for a more favorable fundraising climate.

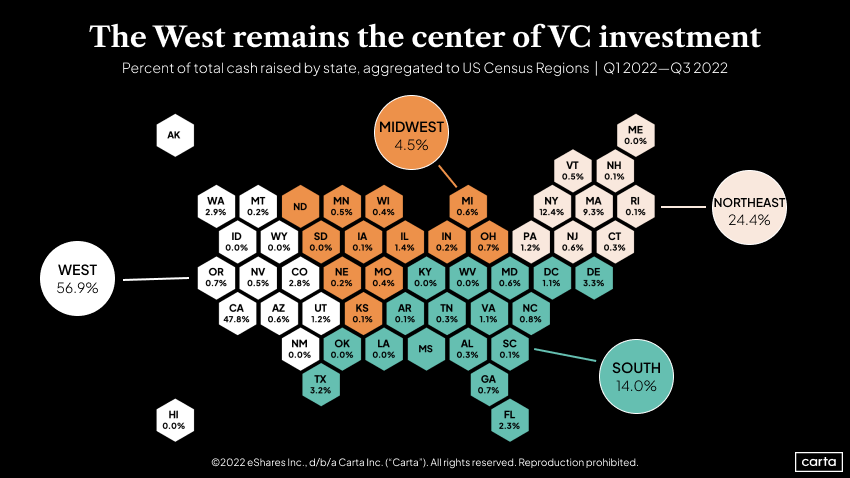

California remains the center of the VC universe, with nearly half of all equity funding raised over the past nine months. But the rest of the country is gaining ground. The South claims 14% of activity, up from 11.6% for all of 2021. Sun Belt cities like Atlanta, Austin, and Miami have led the way, while the likes of Raleigh and Dallas have also emerged as increasingly active cities for VCs and startups.

While the West claims 56.9% of all cash raised, it’s home to just 23.7% of the U.S population, according to the latest Census data. The South is the most populous region, with a 38.3% share.

New York raised 12.4% of all cash, trailing only California, while longtime biotech hub Massachusetts (9.3%) comes in third. Combined, those three account for 69.5% of all venture funding in the U.S. Although VCs still primarily look for deals in their traditional coastal stomping grounds, other locales are beginning to draw more dollars and attention. Nearly every state saw some activity in the past year—Alaska, North Dakota, and Mississippi were the only states that logged no deals at all.

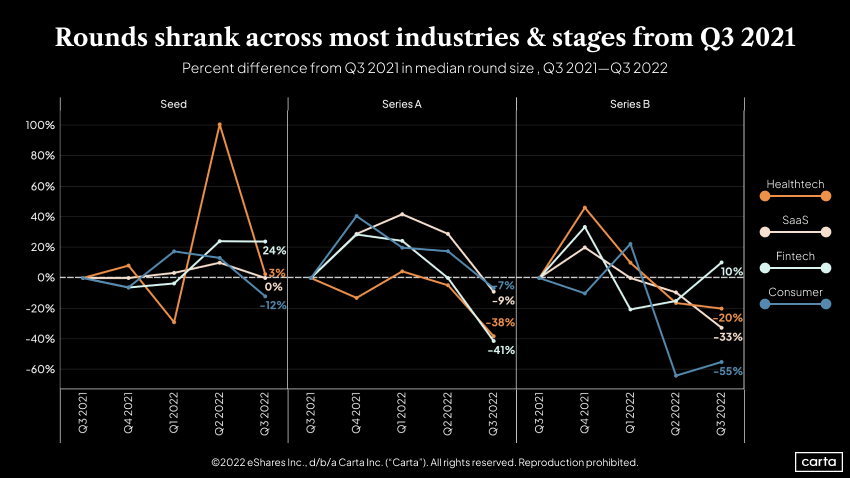

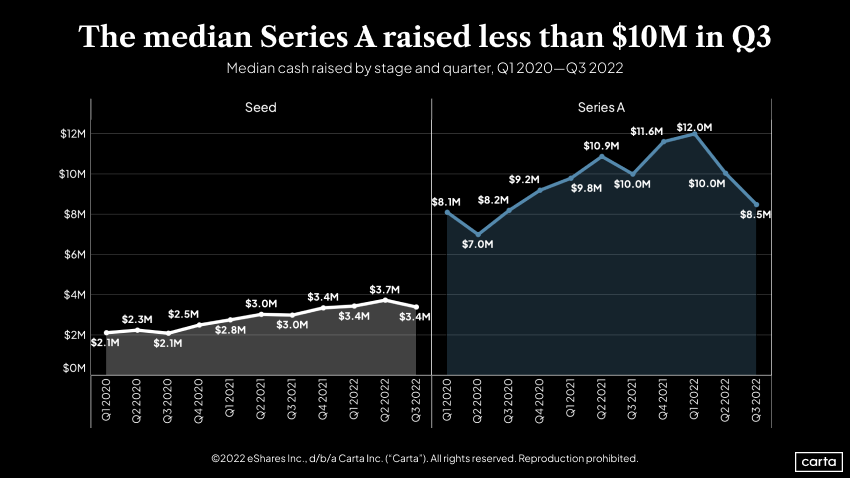

Series A and Series B companies had to adjust to smaller checks in recent quarters, as most median round sizes fell significantly.

The damage is most severe in the consumer sector, particularly at Series B, where the median round size fell 55% year over year—and that’s including a slight uptick from last quarter. Many consumer startups sell their products directly to shoppers over the internet. Due to factors ranging from an inflation-fueled dip in consumer spending to Apple iOS privacy changes that have made it more difficult to track advertising, the direct-to-consumer segment has taken a painful blow in 2022.

The fintech sector presents a counterpoint. While public fintech valuations plunged in 2022, early-stage valuations have been much more resilient—at least at seed and Series B. At those two stages, fintech fundraisings have actually grown year over year. At Series A, however, median fintech round size is down 41%, a larger drop than in any other sector.

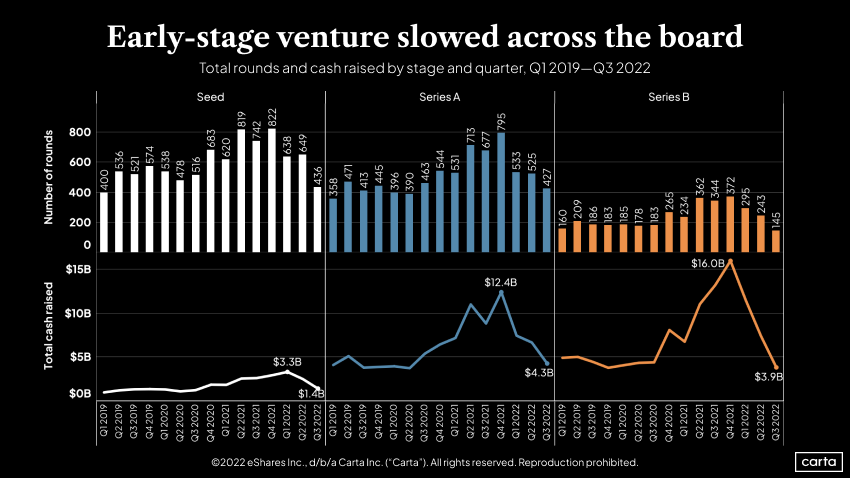

Both deal counts and total cash raised trended down across all three early stages in Q3. The number of seed investments on Carta fell 33% quarter over quarter, while Series A activity declined 19% and Series B plunged 40%.

Earlier in the year, seed fundraising looked more resilient than later stages. While Series A and Series B cash totals had already tailed off significantly by Q1, seed cash was still trending up. Six months later, all three are in a similar boat—although the dropoff at seed isn’t quite as severe. Cash raised by seed companies in Q3 was down 58% from its Q1 high, compared to 65% for Series A and 76% for Series B. While those are steep declines from 2021, the cash raised by all early-stage companies in Q3 is still mostly in line with pre-2021 trends.

In both 2020 and 2021, quarterly deal count peaked during Q4 across all three of these stages. The current quarter will test whether that seasonal trend will continue in a downturn.

The sharpest decline in activity at any stage in Q3 came at Series C, where deal count fell 52% quarter over quarter. Total cash raised at Series C also declined by more than half in Q3; it’s now down 80% from the all-time high in Q2 2021.

On a slightly longer timeline, Series E+ stands out. The number of investments at this late stage is down 68% since Q4 2021, falling to just 20 in Q3. The average size of those investments was about $70 million—less than the average Series D deal in Q3, which was $80 million. One factor in the pullback from Series E+ could be the near-total lack of exit activity so far in 2022, with just 14 U.S. tech companies conducting IPOs through the first three quarters. Investors might be less likely to back these mature private companies without the prospect of a rapid exit.

Valuations and fundraising

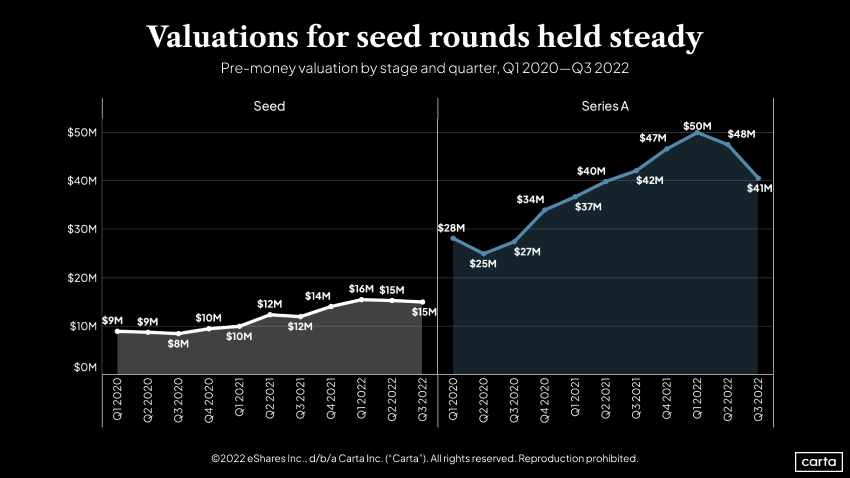

Seed-stage companies are the only ones that have avoided any substantial decline in median pre-money valuation. Seed valuations increased more slowly than later stages during the boom market of 2020 and 2021, and now they’re decreasing more slowly as the market has turned. Seed investors operate on longer horizons than later-stage VCs, which can make this stage more resilient to the market’s short-term twists and turns.

At Series A, a decline that began last quarter accelerated in Q3. The median valuation fell 15% quarter over quarter, and is down 18% since the end of Q1. Before that, the median valuation had increased for seven straight quarters.

Just like with median valuation, the median size of seed rounds has held up better than any other stage. Q3 marked an 8% quarterly drop, compared to a 15% dip at Series A.

Before that, the median seed round had either increased or stayed the same for seven straight quarters. The median Series A, meanwhile, has now fallen 29% from its recent high in Q1 2022.

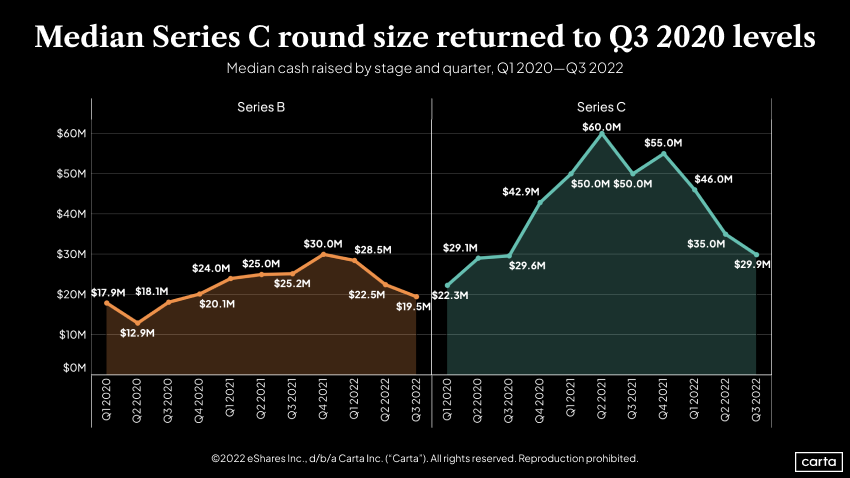

The median Series B pre-money valuation has now declined in two straight quarters, while the median Series C has fallen in four of the past five. On a year-over-year basis, though, the Series B median actually rose 3%, while Series C slipped 24%.

The median Series C valuation climbed much quicker than other earlier stages during 2020 and 2021, more than tripling in the span of five quarters. Now, it’s also declining more quickly.

The median Series C round size fell 15% this quarter and is now down 50% from its peak in Q2 2021. Just like with valuations, the trend is similar but less severe at Series B.

Smaller venture rounds have material impacts on the companies that raise them. A founder with less cash on hand may need to focus on cost cutting over growth initiatives, in order to extend the company’s runway.

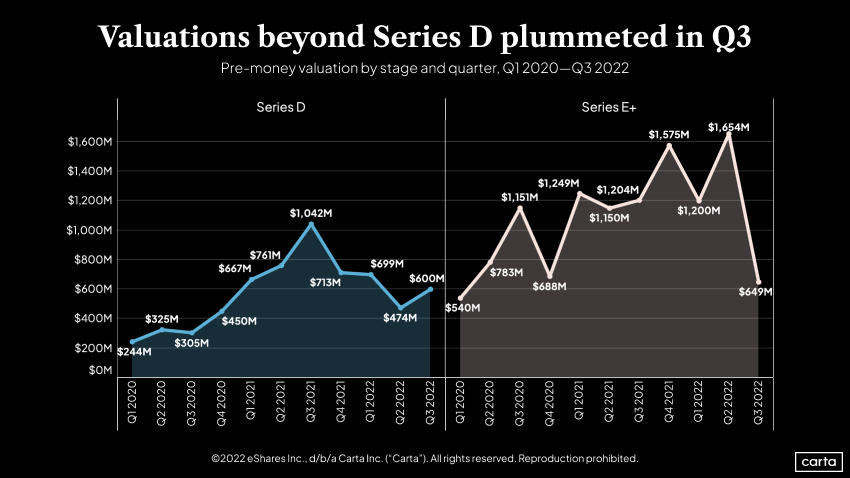

Series D was the only stage to see median pre-money valuation tick up in Q3, gaining 27% over the previous quarter. However, that increase came after the median valuation had declined by 55% over the previous three quarters. Series D valuations are still higher than at any point in 2020.

Valuations at Series E and beyond were relatively resilient during the first half of the year. But the median fell 61% during Q3, reaching its lowest point since Q1 2020. Struggles in the public market—such as slumping valuations and a lack of exit opportunities— are dampening investor sentiment at these latest stages of the private market.

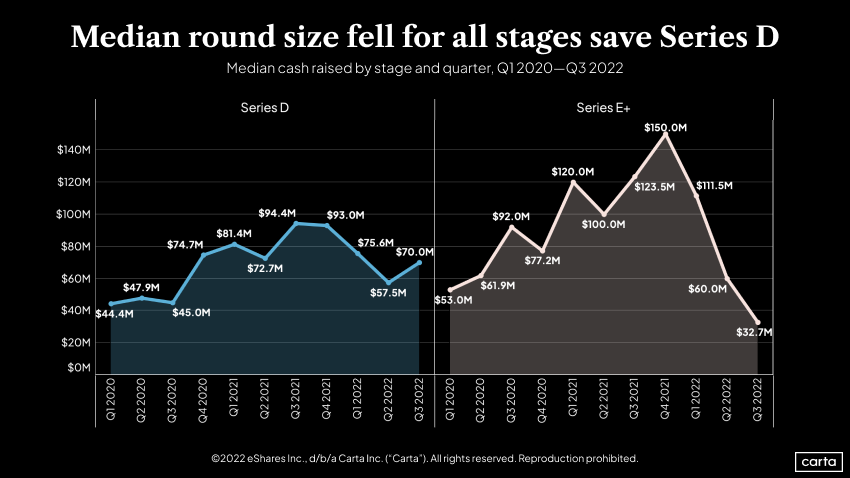

Series D was the only stage at which the median round size increased during Q3—and it climbed a significant 22%. This corresponds to the uptick in median Series D valuation. Some volatility in Q3 may be due to smaller sample sizes, considering that deal counts declined by 40% quarter over quarter at Series D and 35% at Series E+.

While companies and investors at this stage may be thinking about an exit in the medium term, the pressures of the current public market environment haven’t been as strong at Series D as at Series E+.

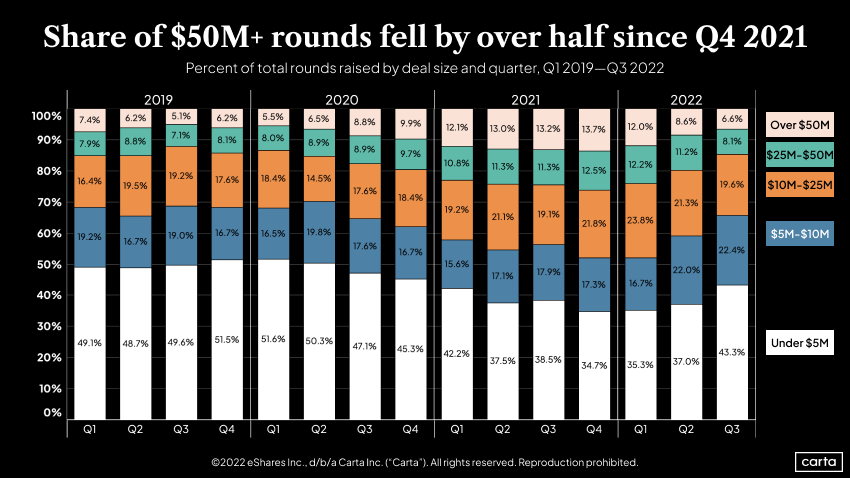

After the onset of the pandemic, a clear trend emerged: The percentage of financings over $50 million started climbing, while venture deals of less than $5 million were becoming less common. The past two quarters, however, the trend has reversed. Deals smaller than $5 million accounted for their largest share of activity since 2020, while deals over $50 million accounted for their smallest share since Q2 2020.

In this metric, as in many others, the current venture market looks more like the pre-pandemic landscape than it has for the past two calendar years.

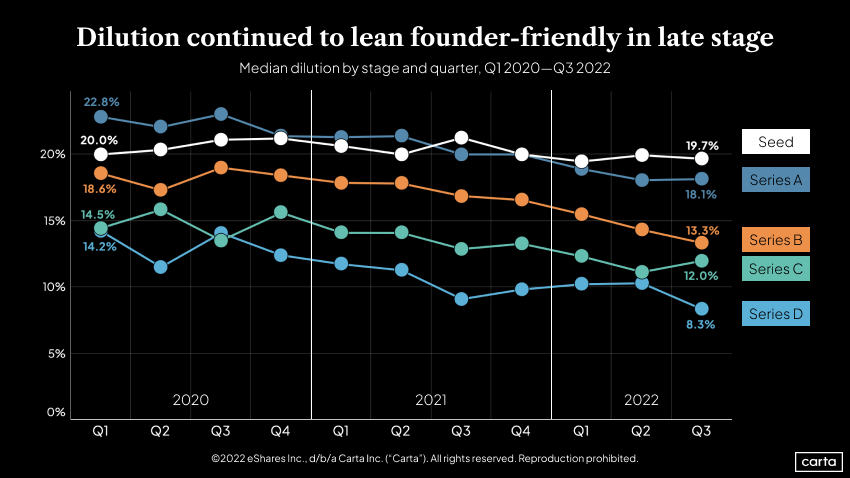

When valuations decline, the terms of venture rounds typically grow more investor-friendly. Yet in terms of median dilution—the percentage of a company’s equity that is sold in a round—the market continues to trend in the opposite direction. At every stage, founders today are giving up a smaller percentage of their company than they did a year ago.

The biggest decline over the past few years came at Series D, where median dilution has dropped 42% since Q1 2020. Seed stayed the steadiest, with a dilution drop of just 2% over that span.

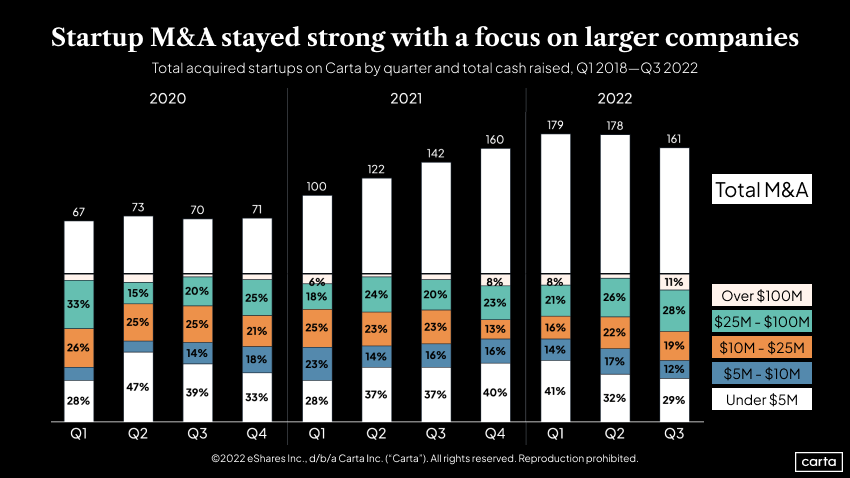

The makeup of startups being acquired through mergers and acquisitions (M&A) has shifted this year. In Q1, 55% of acquired startups had raised $10 million or less in prior venture funding, while 29% had raised more than $25 million. In Q3, only 41% of acquired startups had raised $10 million or less, while 39% had passed the $25 million mark. At the upper end of the spectrum, 11% of all acquired startups in Q3 had raised more than $100 million in prior funding, the highest rate of any quarter of the past three years.

A total of 518 startups on Carta were acquired through the first three quarters, almost equaling 2021’s full-year total of 524. With the markets for IPOs and SPAC mergers in a state of dormancy, more companies are turning to M&A as an exit option.

Employee equity and movement

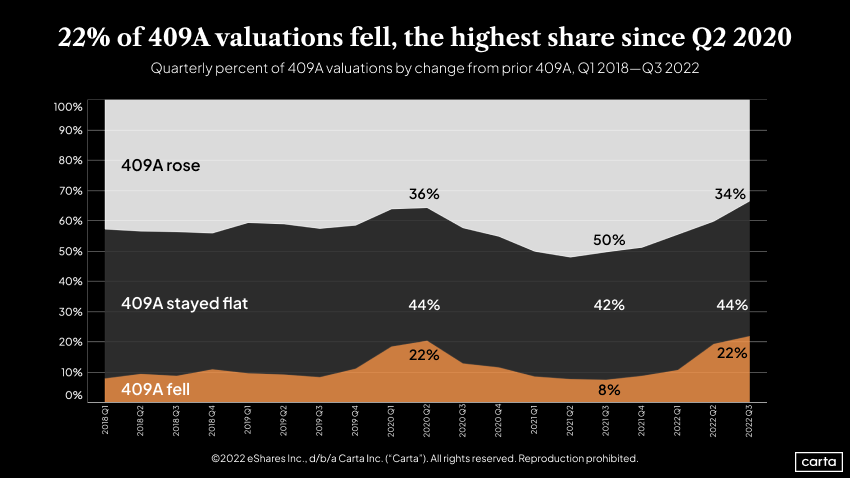

Carta’s 409A valuation appraisals reflected sinking valuations across the public markets and in the venture capital market. The percentage of companies with reduced valuations nearly tripled year over year, rising from 8% to 22% in Q3. That’s tied for the highest rate of the past five years. Meanwhile, the percentage of companies that saw higher valuations fell from 50% to 34%—its lowest point of the past five years.

Companies repriced more than 18,000 stock option grants on Carta in Q3—the highest quarterly figure on record and a 260% quarter-over-quarter increase. This is likely a response to sinking private valuations. Companies typically reprice their option grants when the current value of those grants has fallen below the exercise price. A repricing can thus make previously underwater options more enticing to employees.

The previous high for quarterly repricings came in Q2 2020, when the startup market was sorting through the implications of a global pandemic. In between these two spikes, repricings dropped as valuations soared during the first half of 2021.

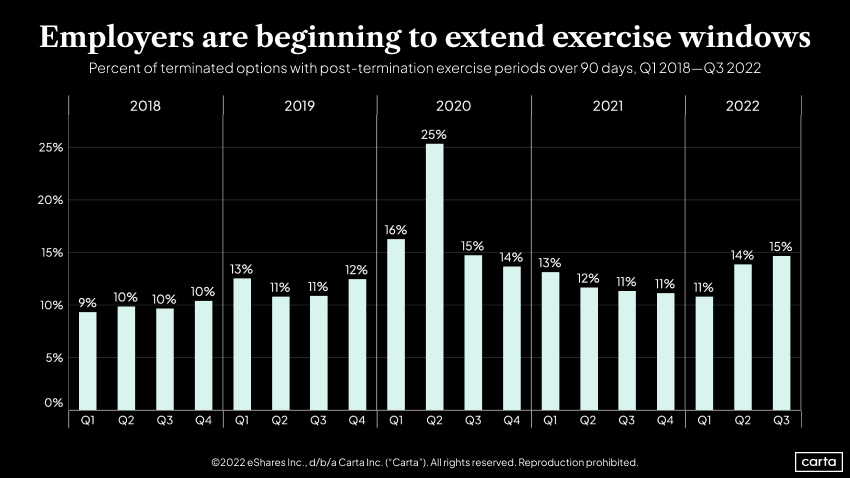

When employees leave a company, either by choice or involuntarily, they typically have a 90-day window to exercise any vested shares or else lose those options forever. Over the past two quarters, the percentage of employees receiving longer than that standard 90-day window is ticking up, reaching 15% in Q3, the highest rate in more than two years.

As was the case when layoffs spiked around the start of the pandemic, some companies are giving employees a longer post-termination exercise period (PTEP) as a benefit during a more difficult economic climate. Sinking stock prices in 2022 have made it even more difficult for some employees to come up with the lump sum of cash required to buy ( and pay taxes on) their shares within 90 days.

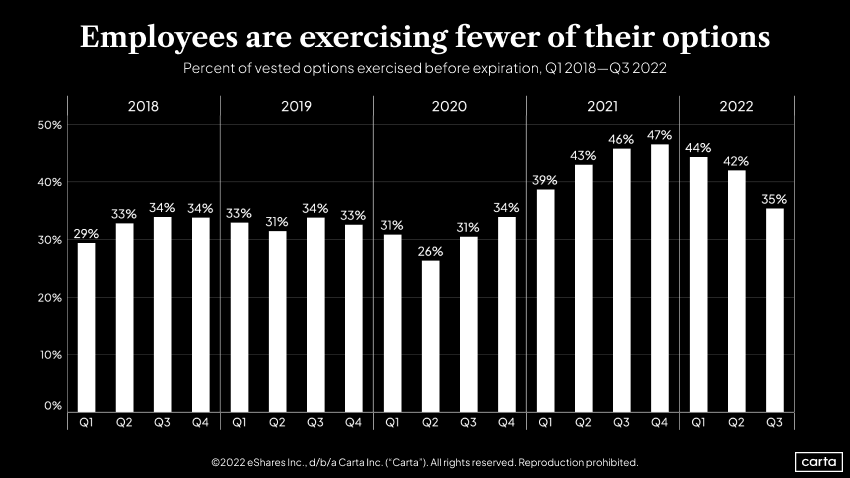

Falling stock prices and inflationary pressures may also help explain why the percentage of all vested stock options on Carta that were exercised before expiring fell for three straight quarters. If employees are feeling any kind of financial crunch, they’re less likely to have the cash needed to exercise. They’re also less likely to exercise if they aren’t as optimistic about the potential upside of their shares.

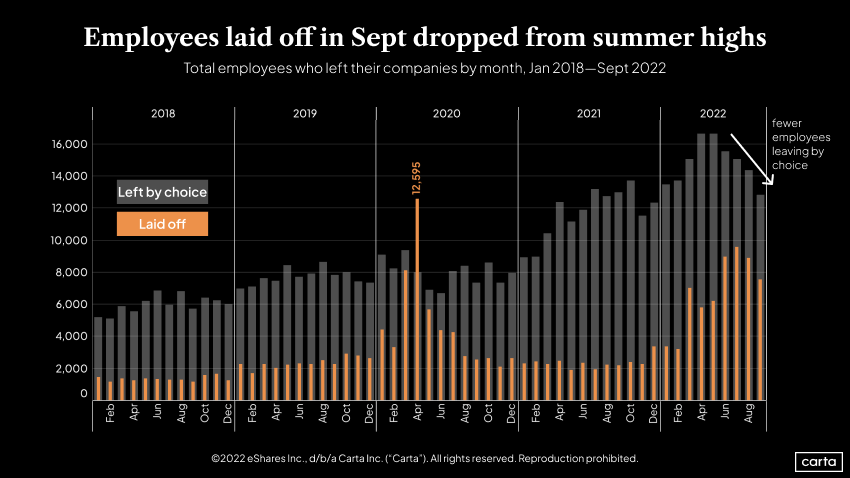

The number of newly terminated employees declined in both August and September after reaching a new yearly high in July. But the percentage of all job departures that were involuntary is inching up. It settled at 37% in September 2022, compared to 15% of all departures that were involuntary in September 2021.

Tech layoffs have continued to make headlines in the early weeks of Q4. High-profile names like Lyft, Stripe, and Twitter all cut their workforces by more than 10% in recent downsizings.

The number of employees leaving their jobs by choice rose for six straight quarters beginning in November 2021. But as private market instability continues into the second half of the year, that trend has reversed, with job departures by choice now falling for four straight quarters.

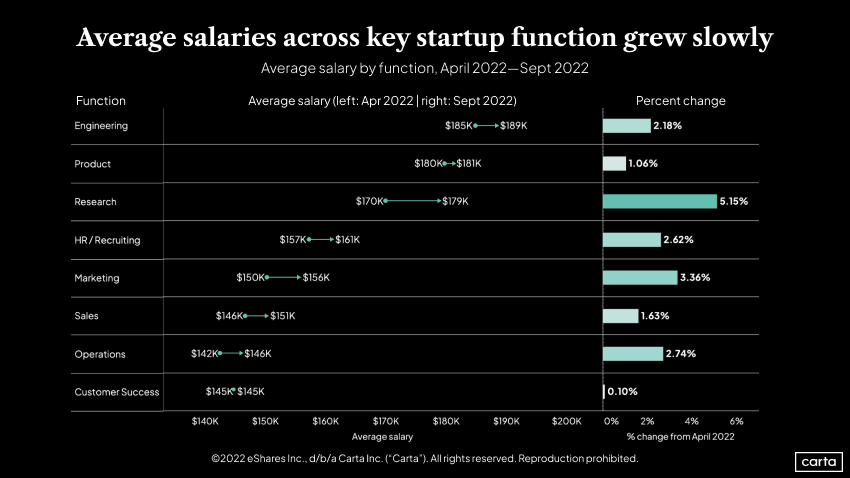

Average salary for researchers grew more than for any other job function between April and September, both in terms of dollars and percentage change. The average operations salary is now higher than customer success after the latter remained stagnant over the past two quarters.

Industry-specific data

For more industry-specific details on Q3 fundraising, download the addendum to the Q3 report.

Methodology

Carta helps more than 30,000 primarily venture-backed companies and 2,100,000 security holders manage over $2.5 trillion in equity. We share insights from this unmatched dataset about the private markets and venture ecosystem to help founders, employees, and investors make informed decisions and understand market conditions.

Overview

This study uses an aggregated and anonymized sample of Carta customer data. Companies that have contractually requested that we not use their data in anonymized and aggregated studies are not included in this analysis.

The data presented in this private markets report represents a snapshot as of November 2, 2022. Historical data may change in future studies because there is typically an administrative lag between the time a transaction took place and when it is recorded in Carta. In addition, new companies signing up for Carta’s services will increase historical data available for the report.

Financings

Financings include equity deals raised in USD by U.S.-based corporations. The financing “series” (e.g. Series A) is taken from the legal share class name. Financing rounds that don’t follow this standard are not included in any data shown by series but are included in data not shown by series. Primary rounds are defined as the first equity round within a series. Bridge rounds are defined as any round raised after the first round in a given series. If there is no indication that a round is a Primary or Bridge round, both are included.

In some cases, convertible notes are raised and converted at various discounted prices within a series (e.g. Series A-1, Series A-2, Series A-3). In these cases, converted securities are not included in cash raised, and only the post-money valuation of the new money is included.

Industry groupings

We grouped industries as follows: “SaaS” includes CRM software, edtech, and HR software in addition to other software as a service companies; “health & biotech” also includes healthcare devices and healthcare tech; “consumer” includes consumer products and services, such as food, cannabis, and video games; “hardware & logistics” includes electronics as well as renewable energy, semiconductors, telecom, and transportation; “fintech” includes financial exchanges; “data & security” includes cloud distribution, analytics, and cybersecurity; and “adtech & marketplace” also includes ecommerce and social media.

Terminations

Terminations entered into Carta must include a reason. Involuntary terminations include both terminations for performance and company layoffs. Voluntary terminations are employees who decided to leave of their own accord. Other termination reasons, including for cause, death, disability, and retirement were not included in the data and make up less than 1% of all terminations combined.

Salary

Salary data derives from Carta’s compensation management software, Carta Total Comp.