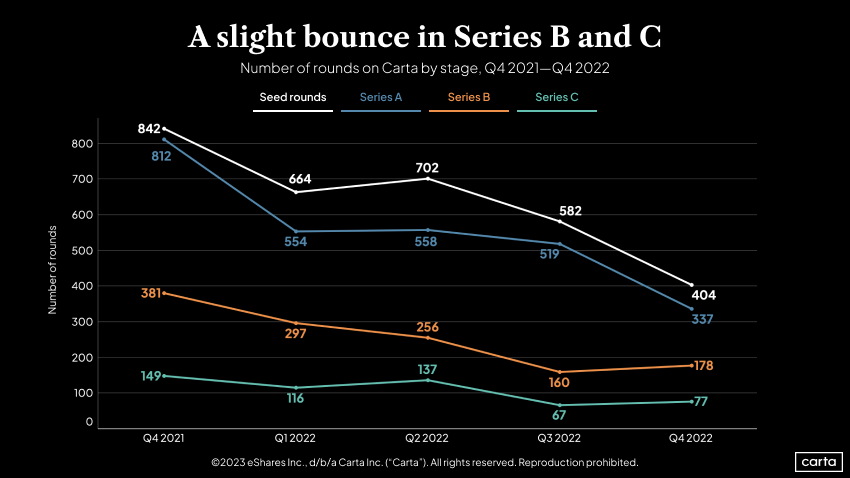

After several months of holding steady, the seed and Series A stages saw a significant pullback in deal count during the final quarter of 2022. A very different shift occurred at Series B and Series C, where investment numbers ticked up after having plummeted the previous quarter.

In the opening phases of the ongoing venture downturn, the earliest stages of the startup lifecycle showed surprising resilience, while later-stage companies saw demand for deals dry up faster—and to a much greater degree. In Q4, the landscape looked more level.

The number of new seed investments in companies on Carta fell 33% from Q3. At Series A, it was a 36% decline. But deal count actually rose by 7.5% at Series B in Q4, after falling 38% in Q3. At Series C, it was a 13% increase after a 51% falloff in Q3.

At every stage, companies are experiencing a much tighter dealmaking environment than a year ago. Year over year, deal counts at all four stages are now down between 48% and 58%.

During Q3, early-stage deals dominated the landscape: Seed and Series A investments accounted for 79% of all activity, the highest quarterly figure in the past three years. In Q4, that figure fell to 71%. Conversely, Series B and Series C deals went from 17% of activity to 25%. (Series D and Series E+ maintained a 2% share across both quarters.)

Those same trends—an early-stage retreat and a mid-stage resurgence—were apparent in the size of venture deals in Q4. Seed and Series A deals had climbed from 26% of all invested capital in Q4 2021 to 39% by Q3 2022. But last quarter, that proportion fell back to 33%. The share of Series B and Series C capital had fallen from 45% to 40% over the previous nine months, but it soared to 48% last quarter.

Why were earlier stages initially more resilient to plunging deal totals? The answer begins on the public markets. Investors often closely compare late-stage private companies to public tech companies, because those mature private companies might theoretically go public soon themselves. So when public tech valuations began to sink last year, investors sought corresponding discounts in late-stage private companies. But many companies were hesitant to raise a down round. Disagreements on price made it harder to get deals done, thus reducing deal counts.

Valuations for early-stage companies, meanwhile, are typically not so closely tied to public comparables, because early-stage companies are still so far away from potentially going public. Earlier last year, investors thought the broader market would have plenty of time to recover before it could affect the exit prospects of these younger startups. But as fears of an extended and more severe economic slowdown mount, these earlier stages are no longer so insulated.

You can think of the VC funding market as a mountain. At the base are early-stage deals, which make up the vast majority of all investments. In the middle are Series B, Series C and Series D, with the mountain narrowing at each stage. In the rarefied air at the top are the few companies that eventually raise rounds at Series E and beyond.

Venture downturns such as the current one are like an avalanche. It started at the very top of the mountain, hitting late-stage companies first. For a time, it appeared younger startups might be outside the fallzone. But as the downturn lingers, the avalanche is continuing down the slopes. Now, even the earliest stages are feeling the chill.

Learn more

Get weekly insights in your inbox

The Data Minute is Carta’s weekly newsletter for data insights into trends in venture capital. Sign up here: