- The alternative minimum tax (AMT), explained

- What is the alternative minimum tax?

- Who needs to pay the alternative minimum tax?

- History of the alternative minimum tax

- How is AMT calculated?

- 2026 AMT exemption amounts

- 2026 AMT exemption phaseout thresholds

- Free AMT calculator

- What does AMT have to do with exercising stock options?

- The bargain element explained

- What is an AMT credit?

- How can I minimize AMT related to my equity award?

- Frequently asked questions about AMT

What is the alternative minimum tax?

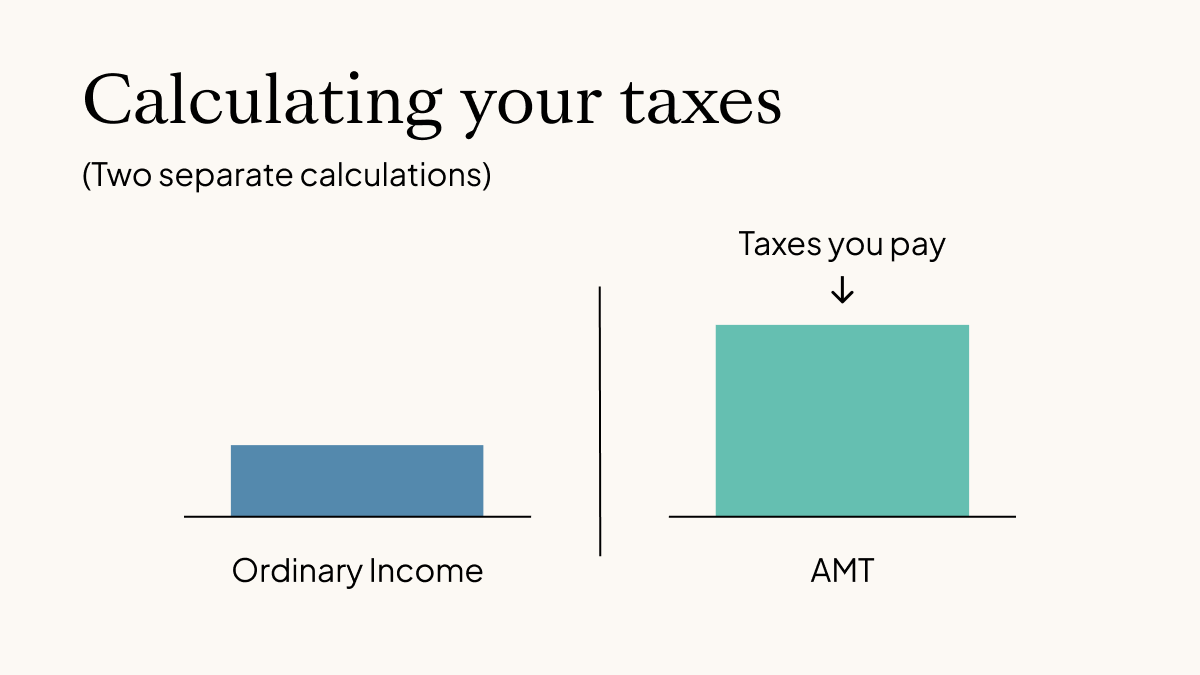

The alternative minimum tax (AMT) is a parallel tax system designed to ensure taxpayers can't use certain preferential deductions and tax breaks to eliminate their tax bill entirely.

The AMT calculation limits certain tax breaks, deductions, and credits that can reduce your regular tax bill, and if that secondary calculation results in a higher liability than what you'd otherwise owe, you pay the difference.

If you make more than the AMT exemption amount, you must calculate your tax liability twice—once under the regular tax system and once under the AMT rules—and then pay the higher of the two. Since AMT doesn’t allow for many deductions and credits, your taxable income under the AMT calculation is likely to be higher.

Common deductions and exclusions that are limited or disallowed under AMT may include:

State and local tax deductions: Fully disallowed

Miscellaneous itemized deductions: Generally not allowed

Medical expense deductions: Subject to a higher threshold under AMT rules

Depreciation adjustments: Slower depreciation schedule for assets

Incentive stock options (ISO): The difference between the strike price and fair market value (FMV) counts as AMT income

Tax-exempt municipal bonds: Interest from some municipal bonds is taxable under AMT

Who needs to pay the alternative minimum tax?

The AMT was originally designed to ensure high-income taxpayers couldn't use preferential tax breaks to eliminate their tax bill entirely.

But it can affect a much broader range of people than many expect. For startup employees who receive stock options in particular, exercising incentive stock options can trigger a significant tax bill even if your cash income is modest, because the spread between your strike price and the stock's fair market value counts as income under AMT rules the moment you exercise, even if you haven't sold a single share.

You may be more likely to pay AMT if you:

Have a high income

Are married (or are married but file separately)

Live in a state with a high income tax

Recently exercised ISOs and didn’t sell them

If you think you may be subject to the AMT, you can refer to the instructions for Form 1040 (Schedule 2) and Form 1040-SR or work with a tax preparation specialist. To calculate whether you owe AMT, you will use Form 6251, also known as the Alternative Minimum Tax form.

History of the alternative minimum tax

The AMT was introduced in 1969 to prevent wealthy taxpayers from using excessive deductions and credits to pay little or no taxes. While initially targeting the wealthy, the AMT eventually began affecting middle-income earners due to inflation, cuts in ordinary income tax rates, and tax bracket creep.

In recent years, Congress has made several adjustments to reduce the number of taxpayers who are subject to the AMT. In 2012, AMT exemption amounts were adjusted under the American Taxpayer Relief Act, which also made future exemption amounts indexed for inflation. The 2017 Tax Cuts and Jobs Act (TCJA) increased AMT exemption amounts through 2025, at which point they were set to expire.

The 2017 AMT exemption increases were permanently extended under H.R. 1, One Big Beautiful Bill Act (OBBBA), which was enacted on July 4, 2025. However, the OBBBA reverts the AMT exemption phaseouts to 2018 levels ($500,000 for single filers and $1 million for married couples filing jointly) and increases the phase-out rate (50 cents vs. 25 cents) for every dollar AMTI exceeds the phaseout threshold. As a result, more higher-income taxpayers could be subject to the AMT.

How is AMT calculated?

To manually calculate your AMT, start by figuring out your alternative minimum taxable income (AMTI). This includes:

Your adjusted gross income (AGI)

Certain deductions and exclusions that reduce your regular taxable income, such as the standard deduction or the deduction for state and local taxes

Preference items, like the spread between the price you paid to exercise your ISOs and their market value when you exercised

Calculating your AMTI can get complicated, so we recommend using tax software, talking to a tax professional, or a combination of both. You can calculate your AMTI using IRS Form 6251.

While the standard deduction isn't allowed under the AMT system, the AMT provides its own exemption amount that you can subtract from your AMTI before calculating what you owe.

2026 AMT exemption amounts

Filing status | Exemption amount |

Single filers | $90,100 |

Married couples filing jointly | $140,200 |

Source: Internal Revenue Services (IRS)

However, these exemptions start to phase out once your AMTI hits a certain threshold:

2026 AMT exemption phaseout thresholds

Filing status | Threshold |

Single filers | $500,000 |

Married filing jointly | $1,000,000 |

Source: IRS

For 2026, AMT exemptions phase out at 50 cents per dollar earned once AMTI reaches $500,000 for single filers and $1,000,000 for married taxpayers filing jointly as shown in the table above. For every $1 above the threshold, your exemption is reduced by $0.50.

Once you reach your final AMTI, you can calculate your AMT liability.

| 26% AMT tax rate | 28% AMT tax rate |

Married filing separately | AMTI up to $122,250 | AMTI above $122,250 |

All other filers | AMTI up to $244,500 | AMTI above $244,500 |

Source: Tax Foundation

If this amount is higher than what you’d have to pay doing your taxes the usual way, you have to pay AMT.

Free AMT calculator

Calculating AMT can be complicated, but you may want to get an estimate before you exercise, as it could be a significant amount of money.

To help, we created a free AMT calculator you can use to estimate your potential tax bill. To use this calculator, all you need is the following information:

Your income

Filing status

Strike price

Current fair market value (FMV) of your shares

The number of options you exercised or plan to exercise

What does AMT have to do with exercising stock options?

For startup employees, the AMT most commonly comes into play when you exercise incentive stock options (ISO). Under the regular tax system, no income is recognized at exercise, but the AMT treats the spread between your strike price and the stock's fair market value as taxable income. So if you exercise your ISOs and don't sell in the same year, that paper gain gets added to your AMTI even though you haven't seen a dollar of actual cash.

For example, if you exercise 1,000 shares at $1 each when they’re worth $5 each, you need to add back $4,000 to your income when calculating AMT. You can report your spread on IRS Form 6251.

If you exercise your shares and sell them in the same year, the spread doesn’t count as income for AMT purposes and instead counts as regular income.

The bargain element explained

The main trigger for the AMT when you exercise ISOs is something called the bargain element. In simple terms, the bargain element is the on-paper profit you make the moment you exercise your options. It is the difference between the stock's fair market value on the day you exercise and the lower strike price you paid for it.

While this bargain element is not considered income under the regular tax system when you exercise, it is counted as income when calculating the AMT. This is the phantom income that can lead to a tax liability. The larger the bargain element, the more likely it is that you will be affected by the AMT.

What is an AMT credit?

If you have to pay the AMT, you may get an AMT tax credit, which you can use to reduce your tax obligation in future years. When you pay AMT because of exercising ISOs, the IRS gives you a credit for that amount, which is calculated and tracked using Form 8801. You can then use what the IRS calls a special minimum tax credit in future years to lower your regular tax bill. Typically, you can apply this credit in the year you eventually sell the stock and realize the actual cash gain. This helps offset the capital gains tax you will owe at that time, effectively returning the AMT you paid in a prior year.

One important caveat: You can only use this credit in years when you're not subject to AMT, so if you trigger AMT again the following year, the credit has to wait. The good news is the credit carries forward indefinitely until you're able to use it.

How can I minimize AMT related to my equity award?

To get ahead of tax planning for 2026 or if you have questions about how exercising may impact your tax liability, talk to a tax professional—ideally before you exercise your options. They should be able to tell you how many ISOs you can exercise without triggering AMT and generally advise you on whether to exercise or sell—and if so, when.

If you were to sell your shares (that used to be ISOs) in the same year you exercise, you won’t have to include the spread in your AMTI. Just keep in mind that if you do this, you won’t get to take advantage of the ISOs’ favorable tax treatment, since you need to hold them for at least a year after exercising to qualify for long-term capital gains tax benefits.

If your company allows early exercising (exercising before you vest), you could consider exercising your ISOs right when you’re granted them and filing an 83(b) election within 30 days. This allows you to be taxed on the day you exercise instead of having to wait until your shares vest. If you exercise your ISOs as soon as they’re granted, there usually won’t be a spread you need to add to your AMTI. However, in this circumstance, you’re paying cash now for shares that may depreciate in the future.

Other strategies to minimize your AMT obligation include lowering your adjusted gross income. Your tax advisor may discuss maxing out contributions to your retirement accounts and increasing your charitable contributions to nonprofits. However, the effectiveness of any strategy depends on your overall tax picture, so it's worth working through the numbers with a professional before acting.

Carta Equity Advisory helps the employees of our customer companies make informed decisions about equity ownership and taxes.

Frequently asked questions about AMT

The rules around the AMT and stock options can be confusing, but a few common questions come up frequently. Here are simple answers to help you better understand the key concepts.

What happens if I sell my shares in the same year I exercise?

If you sell your shares in the same year you exercise your ISOs your profit from the exercise will be generally taxed as ordinary income, but you will not have an AMT adjustment related to that specific exercise.

What is Form 3921?

Form 3921 is a tax document your employer provides after you exercise ISOs. It reports the key details you need to calculate your taxes, and companies on Carta can automate its delivery to employees.

Do I still get QSBS benefits if I pay AMT?

Yes, paying AMT on your ISO exercise does not prevent your shares from qualifying for qualified small business stock (QSBS) tax benefits later, as these are two separate tax rules that apply at different times.

What is the difference between the AMT and capital gains tax?

The AMT can be triggered by the exercise of ISOs based on the paper gain of the bargain element. Capital gains tax, on the other hand, is triggered by the sale of your shares and is based on the actual cash profit you make.

How do you avoid alternative minimum tax?

One common way to reduce AMT exposure is to carefully time your ISO exercises, ideally working with a tax advisor to model how many options you can exercise in a given year without triggering AMT. Because AMT resets each tax year, it's something that can be actively planned around, spreading exercises across multiple years to stay below the threshold each time. Beyond ISOs, you can also minimize other preference items by avoiding private activity bonds and being strategic about the timing of large capital gains and itemized deductions.

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. This post contains links to articles or other information that may be contained on third-party websites. The inclusion of any hyperlink is not and does not imply any endorsement, approval, investigation, or verification by Carta, and Carta does not endorse or accept responsibility for the content, or the use, of such third-party websites. Carta assumes no liability for any inaccuracies, errors or omissions in or from any data or other information provided on such third-party websites. © 2026 eShares, Inc. dba Carta, Inc. All rights reserved. Reproduction prohibited.