- Proposed outbound investment screen will impact venture

- Topline

- Takeaways from the first presidential debate

- Supreme Court overturns Chevron doctrine, curtailing the power of federal regulators

- Treasury issues long-awaited outbound investment proposal

- SCOTUS limits use of SEC in-house tribunals

- IRS ETAAC committee recommends 83(b) e-file to Congress and IRS

- News to know

- Upcoming events

- Sign up below to receive Carta’s Policy Weekly Brief:

Topline

Takeaways from the first presidential debate

Supreme Court overturns Chevron doctrine, curtailing the power of federal regulators

Treasury issues long-awaited outbound investment proposal

SCOTUS limits use of SEC in-house tribunals

IRS ETAAC committee recommends 83(b) e-file to Congress and IRS

Programming note: Carta Policy Weekly will be off next week for the July 4th break. As always, let us know if you have any questions. See you back here July 12th.

Takeaways from the first presidential debate

The presidential candidates squared off in the first debate that covered everything from inflation to immigration, and reproductive rights to Russia. But what it revealed most was not a policy difference, but that this election is about them, their demeanor, and their ability to govern. Most political analysts believe President Biden did not hit the mark last night.

Campaign season is upon us—conventions, campaign trail, another debate, and many, many ads. Throughout, Carta will be providing insights on the election and what it means for the private markets ecosystem. Our first step, an upcoming virtual event: How the 2024 Election Could Shape Private Market Policy, which will touch on capital markets, taxation, and other key issues that undergird the innovation ecosystem. Join us at 10 am (PT) / 1 pm (ET) on July 31.

Supreme Court overturns Chevron doctrine, curtailing the power of federal regulators

This morning, the Supreme Court dealt a major blow to the power of federal regulators by overturning the nearly 40-year old Chevron doctrine, which governs judicial deference to agency interpretations of the laws they implement. Under Chevron, if a statute—the legislative language passed into law—is silent or ambiguous with respect to the issue at hand, the court must defer to the agency’s interpretation if it was based on a reasonable reading of the law. In the majority opinion led by the Chief Justice, the Court ruled that Chevron violated the Administrative Procedures Act, and it is the court’s responsibility — not the agency’s — to resolve and interpret questions of law. In an important caveat, the Court held this standard will apply moving forward, preserving previously decided cases and legal interpretations under Chevron, which will prevent disruptions to settled law.

How we got here: The Chevron doctrine was the result of a shortcoming that is inherent in the legislative process: Congress typically legislates in broad terms and cannot anticipate every issue that could arise, so the federal agencies charged with implementing the laws often resolve gaps or adapt policy to meet changing circumstances. As legislating has become more difficult, particularly in divided government, agencies have increasingly been setting policy through the regulatory process. As the power of the administrative state has increased, conservative scholars and industry have increasingly turned to the courts to rein it in.

Potential implications: As the administrative state has grown, the judiciary has been chipping away at its expanding authority and the Supreme Court’s decision to overturn Chevron is a pivotal shift. As we continue to review the decision and what it means for the ecosystem, here are a few initial reactions:

Courts: Post-Chevron, courts must use their independent judgment in interpreting the meaning of ambiguous laws, rather than deferring to agency interpretations. The shift in power from the executive to the judiciary is likely to lead to greater uncertainty around the stability and predictability of agency actions. More reliance on judicial interpretation may lead to more forum shopping.

Agencies: Eliminating Chevron will have significant implications for agency rulemaking efforts, particularly ones that trend controversial and do not have clear or explicit congressional authorization. More rules are likely to be challenged in court, and agencies will have to reevaluate their rulemaking processes to ensure they are operating within the bounds of their congressionally directed authority now that they no longer have wide latitude to interpret the statutes they enforce. This is particularly true for the SEC, whose regulatory authority is generally derived from broad statutory constructs—and has increasingly come under fire for exceeding its authority. The Court’s decision could also constrain the ability for regulators to adapt rules to address rapidly evolving technologies, such as AI.

Congress: There will be more pressure on Congress to take more responsibility in the legislative process and make its intentions clear as there will be more scrutiny on agency efforts to fill in the gaps without explicit congressional authority. Defining a crypto and AI regulatory framework just got harder.

Industry: Businesses—particularly those who are subject to more regulation—could face uncertainty, compliance challenges, and costs in navigating the changing regulatory landscape. But they could also face more autonomy and freedom to innovate if regulatory hands are tied.

Treasury issues long-awaited outbound investment proposal

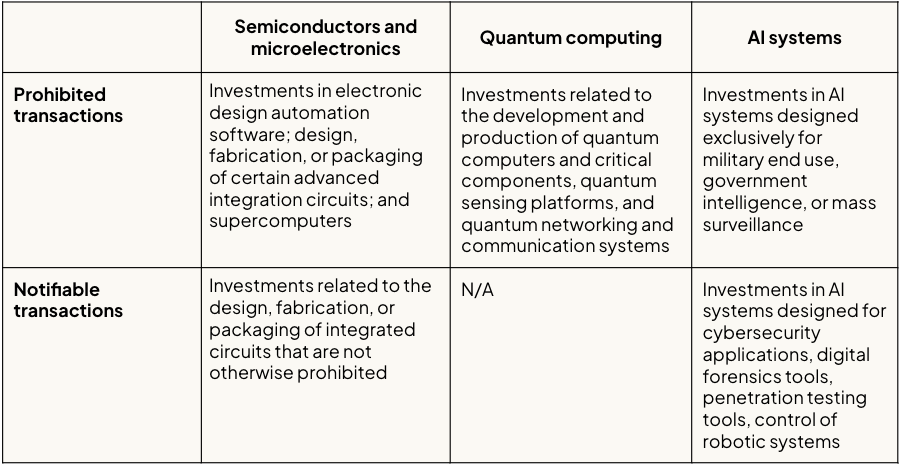

As mandated by President Biden’s 2023 executive order (EO), the Treasury Department proposed rules for a program to oversee outbound investments in sensitive technologies and products that pose a risk to national security. The proposed rule would prohibit—or in some cases, require notification of—private equity and venture capital investments in China-related entities involved in the development of sensitive technologies in three targeted sectors: semiconductors, quantum computing, and artificial intelligence (AI) systems. The program does not have a retroactive component, so its reporting requirements and prohibitions would only be applied to transactions that take place after its effective date, though Treasury can request information on covered transactions entered after the August 2023 EO.

Other key elements:

Knowledge standard: The proposed rules impose a knowledge standard, which will effectively mandate pre-investment due diligence.

Covered transactions: The proposal would apply to acquisitions of equity interests (mergers and acquisitions, private equity, and venture capital) and contingent equity interests (SAFEs); certain debt financing transactions that are convertible to equity or afford certain management rights (convertible notes), and certain LP investments in non-U.S. funds (among others) that involve U.S. persons and China-related entities engaged in the covered technologies.

Exemptions: Publicly traded securities (companies and funds), full buyouts, LP investments that do not exceed $1,000,000 or 50% of fund AUM, and binding, uncalled capital commitments entered into prior to the issuance of the August 2023 EO (among others). The proposal also contemplates an exemption process for transactions that are of “national interest” to the U.S.

Compliance and enforcement: Information related to notifiable transactions must be filed with Treasury no later than 30 days after the transaction is completed. Prohibited transactions would not be allowed after the effective date of the final rules. Violations could result in civil penalties, criminal sanctions (for willful violations), and potential divestment.

Why it matters: The outbound investment proposal will affect how venture capital and private equity diligence deals in key emerging technologies, and potentially increase notification requirements or prevent them from participating. The proposal estimates that U.S. investors made around 318 investments in China-related entities in the semiconductor, AI, and quantum science sectors between 2021 and 2023—the bulk of which are likely occurring at the venture stage. While the proposal may not cover a large number of deals, VC and PE fund managers will have to incorporate measures in their due diligence process to ensure compliance.

What’s next: The proposal is out for public comment until August 4, after which Treasury will incorporate feedback and issue final rules. While disagreements persist on the appropriate structure and duration of the program, there is strong bipartisan support for imposing additional scrutiny on Chinese outbound investments, which makes it likely some program is implemented even if the timeline extends beyond the 2024 election.

SCOTUS limits use of SEC in-house tribunals

In a 6-3 decision in SEC vs. Jarkesy, the Supreme Court invalidated the use of in-house administrative proceedings for securities fraud claims and affirmed defendants have a right to a jury trial when financial penalties are on the table.

The Jarkesy decision does not preclude the SEC from bringing securities fraud actions, but it will now have to do so in federal court, potentially creating inefficiencies and a slower enforcement process. Practically speaking, this may not be a large change for the SEC, as it has recently pursued most of its litigated securities fraud cases in district court as administrative proceedings have come under scrutiny.

The Jarkesy ruling is limited to cases where the SEC pursues civil penalties; it does not apply to non-monetary relief or sanctions, such as bars and limitations to practice before the Commission—meaning the SEC can continue to pursue these remedies against fund managers and gatekeepers in-house.

Why it matters: Jarkesy is another blow to the administrative state that could have even larger impacts on agencies that rely more heavily on in-house forums to adjudicate claims. This could impact disputes over Social Security benefits, labor issues, and workplace safety claims. Federal courts, who already face significant backlogs, may be under-resourced to handle the influx of new claims.

IRS ETAAC committee recommends 83(b) e-file to Congress and IRS

The IRS Electronic Tax Administration Advisory Committee (ETAAC) released its 2024 annual report, and Carta’s Amy Miller, member of ETAAC, joined the committee to present its 12 recommendations aimed at issues such as identity theft, refund fraud, and paperless filing. Among this year’s items is a recommendation for the IRS to consider providing a portal or document upload tool for electronic filing of certain forms and elections, including 83(b) elections.

An 83(b) election lets taxpayers accelerate a portion of their tax liability on equity ownership to the date of acquiring the shares—which can have a substantial impact on tax liability for new business owners and employee-owners.

Although the IRS has made improvements enabling electronic signature, the highly manual election filing process continues to create hurdles for timely submission within the short 30-day window and uncertainty around the filing status.

Why it matters: Carta is exploring every opportunity to enable e-filing for 83(b) elections. The tax code should incentivize more employee owners to realize and optimize the full value of ownership. As tax policy becomes the focus with 2025 drawing near, Carta and its coalition partners will continue to work to shape policies that bolster and make equity ownership meaningful. To get engaged in the tax reform debate, contact us at policy@carta.com.

News to know

SEC’s top cop concerned about private credit valuations, opacity (Bloomberg)

SEC proxy firm rule changes violate law, Fifth Circuit says (Bloomberg Law)

CFPB extends compliance dates for Small Business Lending Rule (CFPB)

DOL report inconclusive on pension risk transfer market, needs more research (Pensions & Investments)

Coinbase sues SEC and FDIC over document requests related to past crypto industry actions (Axios)

Data markup canceled after House leadership opposition (The Hill)

Upcoming events

July 3 - Point Zero Forum: CFTC Commissioner Pham Pham will participate in a “Capital Meets Policy” dialogue on the global AI regulatory landscape

July 10 - Semafor event: Banking on the Future: The Next Era of FinTech

July 17 - Carta event: Startup Fundraising 101: Crafting a Winning Pitch

July 23 - Carta event: NYSE: Getting your Company IPO Ready

July 24 - Carta event: Essential Tools for Startup Success: Equity Management

July 25 - SEC event: SEC's Office of Minority and Women Inclusion is hosting a fireside chat with SEC Chair Gary Gensler

July 31 - Carta event: Policy Playbook: How the 2024 Election Could Shape Private Market Policy