Policy is infrastructure—it can bind growth or unleash it. As a new Administration and Congress takes shape, the policy infrastructure is shifting dramatically. The Carta Policy Team will be releasing a series of issue deep dives in the coming months that detail the evolving landscape, what that means for private equity, and how investors and other stakeholders in the innovation economy can navigate this dynamic environment.

Each edition of this series, “Private Equity Regulatory Insights,” will look at the key issues, the background mechanics, and the players and the moments that will sway the debate, as well as offering practical tips.

Watch this space for deep dives on tax reform, carried interest, retirement, private credit, antitrust and Federal Trade Commission, state efforts, capital markets regulation, and more.

Today, we focus on tax policy.

Tax reform: The macro view

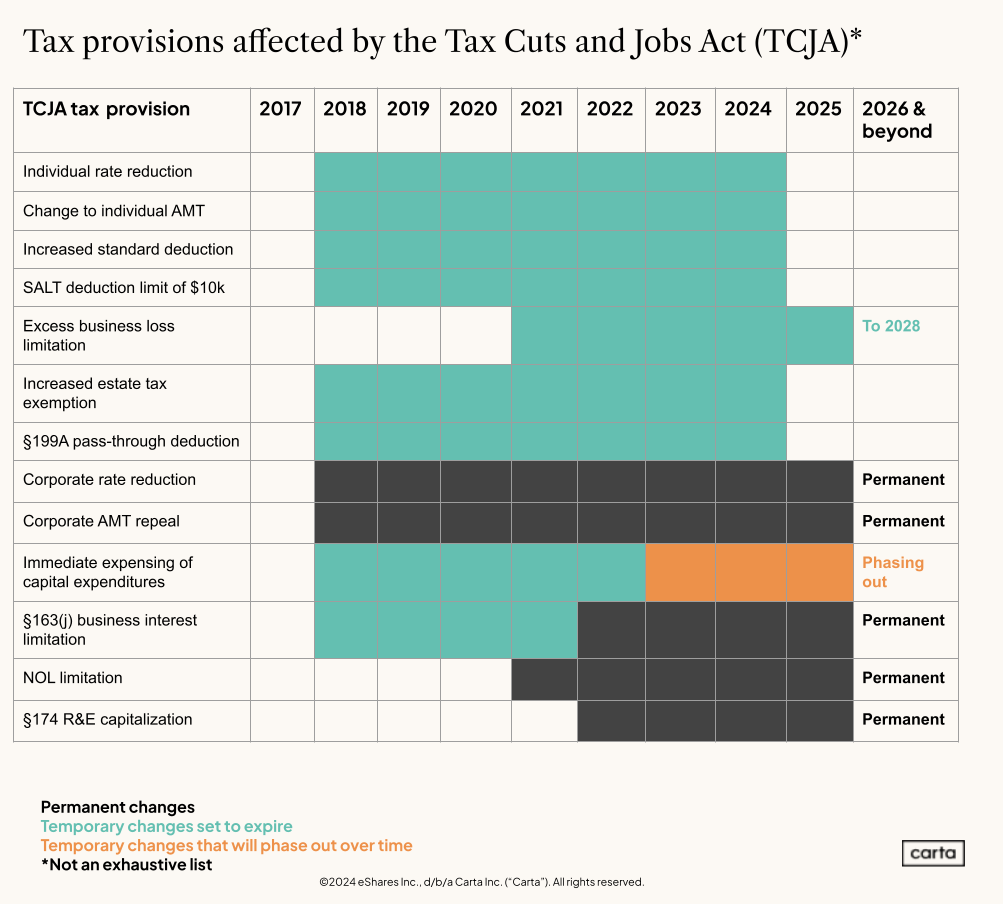

Key elements of the Tax Cuts and Jobs Act (TCJA) are set to expire at the end of 2025. TCJA aimed to drive investment and economic growth by simplifying and lowering taxes for individuals while reducing the corporate rate and revamping how international corporations are taxed.

However, only some of TCJA’s provisions were made permanent. The bulk of the changes will revert to pre-TCJA levels in 2026, and these changes will disproportionately impact individuals and small businesses.

If Congress does not act, over $4.5 trillion in tax increases would take effect in 2026, directly impacting over 60% of U.S. households and indirectly impacting almost every American. Both parties have a vested interest in preventing this from happening.

Process and dynamics

Republicans plan to use the reconciliation process to extend the slate of expiring TCJA provisions and expand tax relief to more areas such as SALT and tax on tips in H2 2025. This will require them to navigate parliamentary procedure, cost pressure, and competing demands.

Reconciliation strategy: Republicans plan to use the reconciliation process to enable them to pass tax reform with a simple (Republican-only) majority. To work, both the House and the Senate needed to pass an identical reconciliation package. And in April—after some tension between the House’s more aggressive cost-cutting approach and the Senate’s more flexible one—Congress passed the Senate-backed bill. This unlocks the procedural path to pass a tax bill with simple majority vote under reconciliation.

Price tag and pay-fors: The Congressional Budget Office announced that extending the TCJA as-is would decrease revenue by more than $4 trillion. Adding additional provisions such as raising SALT caps or the “no tax on tips” idea would increase that number.

The budget resolution would enable Congress to spend $4 trillion, but push Congress to cut $1.5 trillion in spending. The issue is that the reconciliation package instructs the House to cut $1.5 trillion, while only requiring the Senate to cut a minimum of $4B. The final legislative package (not reconciliation, but the actual tax and spending legislation) will have to align and will cut someplace in between. This is where the tough policy decisions come. But expect pay-for pressure, as Speaker Johnson has committed to his members that if they do not cut close to that $1.5 trillion, they can replace him as speaker.

Despite this increased flexibility on pay-fors, Congress will need to find some cuts to pay for this tax bill. Industry will need to engage to make the case for policy extension and expansion, as well as fend off any cuts to our key provisions.

Timeline: The House aims to pass its tax package as soon as late May/ June. The House Ways & Means Committee (the tax-writing committee) plans to outline the legislation in late early May with the aim of holding a Committee vote on it in May. If all goes to plan, the full House will vote on the bill in May/June. The Senate will likely take more time and then adjust the House package accordingly. The endgame is a package in H2, though it would not be a surprise if this slips as late as December.

>> Find out more about the Innovator Alliance and how it bolsters economic growth and U.S. competitiveness.

Path forward: The policy issues

Corporate rate: The TCJA lowered the corporate tax rate from 35% to 21% on a permanent basis to drive growth and equalize U.S. corporate tax treatment with other OECD nations. Despite pressure to pay for tax reform, it is likely policymakers maintain the current corporate rate.

Capital gains rate: The tax code treats capital gains more favorably than other forms of income: Long-term capital gains are taxed at lower rates (0%, 15%, or 20%, depending on income). Taxation only occurs when the asset is sold, and inherited assets receive a tax-free stepped-up basis at death. Similar to the corporate rate, there has been no substantive discussion in raising the long-term capital gains rate.

With the corporate and capital gains rates seemingly safe, a wide range of other potential offsets are in play that will matter to a variety of sectors.

We will home in on issues that affect the broader private equity fund ecosystem: carried interest, 199A pass-through treatment, research and development expenses, and qualified small business stock.

Carried interest

Issue: The fund manager’s economic model is built around carried interest. Under the current tax code, carried interest is treated as investment income and taxed at the long-term capital gains rate rather than the higher ordinary income rate. President Trump and this Congress may change that.

Background mechanics: Most fund managers operate on a “two and twenty” model or similar fee structure. They earn a 2% management fee based on assets under management (AUM) and then a 20% incentive fee—the carried interest, or carry—based on returns. Management fees are taxed at ordinary income rates, but because carry is derived from investment returns, it is currently taxed at the long-term capital gains rate if held for three years. Outright elimination of this treatment would push the tax rate of the carry to ordinary income levels, approximately doubling the tax rate.

Political state of play: Trump has publicly pushed for Congress to end the favorable tax treatment for carried interest to pay for other tax priorities. Most in industry hoped carried interest would remain under the radar—and felt more confident after the Republican sweep. But this was always a risk: Both parties demagogue this issue each election, including President Trump in 2016. We believed the long-term risk was that progressives would use this to drive a wedge between the populist wing of the Republican party and its affluent tech and financial elite, but it appears as though President Trump may push this early to force resolution.

Many congressional Republicans were surprised by President Trump's push on carried interest and do not want to shift the tax rate on carried interest from long-term to ordinary income. But most have noted if the President really pushes for this, it will be difficult to withstand. Industry is holding the line — especially arguing about the tax treatments' importance for emerging managers — but Republican policymakers are requesting compromise ideas.

What to watch: Tax reform needs almost every Republican vote. Here are some signals to watch as the carried interest debate unfolds:

Profiles in courage: Keep an eye on whether any members make preserving carried interest their fight, like former Sen. Kyrsten Sinema, who saved carried interest when Democrats had unified control.

Populist faction: Will eliminating carried interest gain traction with the populist wing? If it does, President Trump likely keeps the drumbeat up.

The inner circle: Some of Trump’s strongest supporters (and cabinet leaders) have benefited from carried interest. But not all beneficiaries are in favor of maintaining the current tax treatment. If that cohort broadens, especially with major voices, it could weaken the industry’s long-held position and potentially end the favorable tax treatment of carried interest.

Discussions around alternatives: Currently, industry is pushing back against any changes. If policymakers start publicly talking about alternatives—whether further extending the holding period, limiting to managers under a certain AUM, or other options—assume the tide is moving against preserving carried interest.

What to do: Rather than react, prepare. Below are some things to consider as the tax debate unfolds.

On the policy side, engage. There are avenues, directly or indirectly, to make the case on what carried interest treatment does to align incentives between managers and their investors, drive capital into the innovation ecosystem, and bolster emerging managers that broaden the benefit of private capital.

On the practice side (this is not tax or financial advice)—stay connected. The tax bill is unlikely to get signed into law until late 2025 at the earliest. But if changes to carried interest happen, your firm will want to be aware in advance to ensure it can take appropriate action before any effective date and structure new funds to reflect changes to the economic model. A few plans to consider:

Retroactive v. proactive: Preparing will require understanding if any changes apply to existing funds and investments or on a go-forward basis.

Ready distributions: Although no fund should make a decision based solely on near-term tax changes, for investment and distributions that may be in play, funds should be prepared to act on opportunities prior to any effective date.

Model shifts: Funds may consider recalibrating their economic model, calibrating the mix between management fees and carried interest. Any changes would require engaging limited partners to preview and execute recalibration on existing funds, if retroactive (renegotiating limited partnership agreement), or new funds.

Flexibility: Changes may not be solely applied to tax rate, but what portion is eligible based on holding period, management investment, or reinvestment. Managers will need to stay engaged to understand these adjustments to plan.

Qualified Small Business Stock

Issue: The Qualified Small Business Stock tax provision, Section 1202, provides an exemption from capital gains taxes for shareholders who were issued shares in certain small companies and held those shares for five years. To qualify for QSBS tax treatment, the shares must be:

Issued by a U.S. C-corp with less than $50 million in gross assets

Issued by a company operating in a qualified trade or business

Acquired directly from the company

Held for at least five years prior to liquidation

QSBS drives capital and talent to the emerging market ecosystem, and although it tends to be focused on early-stage companies, we are increasingly seeing some PE firms find investments that can qualify.

Political state of play: Although this provision—created under President Clinton and expanded under President Obama—previously enjoyed bipartisan support, it has recently come under pressure from progressives and others who believe QSBS benefits wealthy investors. Carta and coalition partners defeated an effort in 2022 to curb QSBS, but we expect QSBS to come under scrutiny again.

Recently, third parties have pushed policymakers to consider cutting QSBS, noting eliminating the tax benefit would raise $80 billion. Carta disagrees (and outlines the positive impact of QSBS). But given pressure on policymakers to find revenue offsets and the third-party pressure, expect QSBS to come under fire.

To push back, we are working with policymakers to expand QSBS to more corporate structures and financing mechanisms, as well as adopt a phased-in approach that would start after three years. We are building coalitions to make this case(see Innovator Alliance), and sometimes the best defense is a good offense.

What to watch: Similar to carried interest, QSBS is likely on the “emergency pay-for” list. But we think policymakers may need to break that glass, so we are watching the following:

Bicameral legislation to expand QSBS: This is positive. We have legislation to expand QSBS introduced in both the House and Senate, by Rep. David Kustoff and Sen. Cornyn, respectively. This will help build bulwarks in both chambers. Our next push will be to educate and advocate for co-sponsors. The more support, the less likely it is QSBS gets curtailed.

Wealth threshold discussion: Previous efforts to curb QSBS would have limited the benefit for shareholders earning over $400,000/year (a misleading threshold because many employees forgo a portion of income for stock and hold those shares for 5 years). Republicans tend not to draw such lines, but if they start discussing differentiating tax treatment based on income, QSBS treatment could be cabined and curbed.

Carried interest losing ground: The populist sentiment that is targeting carried interest can also be applied here. Although QSBS applies to the more politically popular community of startups and early-stage companies, the narratives around investor benefits align. Rather than opponents picking one, we could see both carried interest and QSBS targeted.

What to do:

On the policy side, engage. QSBS bolsters entrepreneurs and the employees helping them build, along with the investors who back them; policymakers should hear from stakeholders to better understand its impact. We need to drive awareness, bill support, and build a network of champions.

On the practice side, stay connected to navigate a fluid dynamic. Here are a few steps to consider

QSBS attestation: First, review and confirm any existing QSBS treatment (Disclaimer: QSBS attestations are part of Carta’s revenue model). Even if the tax code does not change, QSBS designation can be tricky. Carta can help. This will be especially true if the tax code does change and filers have a bigger burden of proof around eligibility. (Pardon the sales pitch.)

Ready liquidations: Assess potential stock sales - if QSBS gets curbed and you are close to liquidation anyway, this is something to consider. The market may reflect this timing.

Communicate with your investors and portfolio companies: Make sure all affected parties are aware of any looming changes. A fund manager can do well by their portfolio companies by providing information to the employees who may be affected by changes to QSBS. The same is true for your limited partners, especially if the fund needs to make any decisions based on this dynamic.

Research and Development

Issue: American businesses were previously permitted to deduct 100% of R&D expenses from taxable income in the year those expenses were incurred. The TCJA changed that, requiring companies to capitalize those costs and amortize them over five years for domestic research and 15 years for foreign research. This issue is less about your fund and more about your portfolio companies’ tax strategies.

The policy focus is reinstating immediate expensing. Immediate expensing promotes innovation by powerfully incentivizing critical investments in research and technological advancement. Those investments lead to countless scientific breakthroughs, power economic growth, and produce significant commercial and military advantages for the United States.

Political state of play: Restoring immediate expensing of R&D has the necessary political support. President Trump even used his recent Joint Address to Congress to push for 100% expensing. There are, however, outstanding questions on whether the fix will be retroactive and whether it will include both domestic and foreign investments.

But the biggest threat to the broader R&D fix is that Congress cannot agree on a broad tax package and ultimately narrows its focus, does some short-term extensions, and leaves the TCJA R&D restrictions in place.

Congress almost restored Immediate expensing of R&D last year, but the House-passed bill foundered in the Senate because it was coupled with what Senate Republicans believed to be too large an expansion of the unrelated child tax credit. This broad political coalition in support of R&D stands today. The one detracting factor is that this longer-duration R&D treatment has taken effect and it did not visibly disrupt industry the way many feared. This reality is unlikely to erode the broad support, but industry continues to make a strong case on every issue, including this one, given the challenging political environment.

What to watch for: Retroactive treatment of immediate expensing is possible, but this may be harder with the cost pressure. Here are the signs to watch as a gauge of where R&D expensing stands:

Narrative shift: As mentioned, R&D amortization took effect, and the industry kept moving forward. As policymakers struggle to offset the tax package, it will be important to monitor—and reverse—any sense that immediate R&D expensing is a luxury, not an imperative to economic growth and competition.

Narrow aperture: The tax deal likely drags until late in the year, but if those conversations move towards short-term, smaller alternatives, R&D risks being left behind.

What to do:

Anecdotes resonate. Work with companies to understand and scope the quantitative and qualitative impact, and be willing to share those stories with policymakers. When policymakers understand the tax bill rose dramatically and unexpectedly, or the amount of R&D investment declined, this reinforces the case.

On the practice side, educating your portfolio companies on the changing dynamics may help them on R&D investment decisions that may inform tax treatment. Understanding how any changes affect certain time periods of investment may help shape that investment; for instance, if a change is made on a forward-looking basis, do companies wait until after that effective date to invest and take advantage of the change. This could delay immediate R&D-related spend. This will not be clear immediately, but is something to stay engaged with to help guide portfolio companies.

199A

Issue: Under TCJA, Section 199A provided a deduction on 20% of qualified business income for pass-through entities defined as sole proprietorships, partnerships (and LLCs taxed as partnerships), and S corporations. This was established to narrow the gap between the now-lower corporate tax rate and individual rates that apply to pass-through business entities. This treatment expires in 2025 and forces the question of whether Congress will extend it.

Section 199A does not apply to Specified Service Trades or Businesses (SSTBs), which include financial services or services involving investing or investment management. Further, even for businesses that qualify, there are limitations based on W-2 wage levels and assets relative to the qualified business.

Put simply, in most situations, PE funds do not qualify. PE funds, however, may benefit from this deduction when they invest in pass-through entity portfolio companies that qualify.

Political state of play: Extending 199A—and even making it permanent—has strong support. Legislation in both the House and Senate have been introduced, and possess large numbers of co-sponsors, including Senate Republican Leader John Thune. The national stakeholder community of covered businesses across the country has driven the political support for this legislation and makes the economic case that covered entities create 2.6 million jobs and account for $325 billion of GDP. Expect the treatment to be extended, though it’s not clear if it will be made permanent given the increased cost of doing so.

What to watch: The biggest risk would be if the tax negotiations fall apart and policymakers need to agree on a short-term, narrow extension. But even in that scenario, this is a core priority for many policymakers and small businesses across the country, so it would still have a shot at being included in the narrow package.

What to do: The 199A benefit for funds is not about the fund, but whether its portfolio company benefits. Our thesis is that the existing treatment will be extended, so fund managers will not need to adjust their behavior, assuming they have understood and implemented the practices around the current construct. But here are some additional considerations:

Monitor progress: The Carta policy team is optimistic this treatment will be extended, but that can change. Stay engaged and aware of developments (Carta Policy Weekly can help).

Apply the treatment: The 199A pass-through deduction can lower the effective rate, increasing the fund’s returns to investors in some scenarios. This is case-by-case, so it is recommended funds affirmatively assess the tax structure of their portfolio companies.

Tax policy is a direct reflection of the importance of the policy infrastructure. Tax policy incentivizes or disincentives behavior, and it affects investment, capital flows, and the bottom line. We will need to drive policy to unleash private capital and the innovation and economic growth it drives.

We also need to prepare stakeholders to navigate the policy framework. This helps drive the broader macro economic journey and your own outcomes. That is the aim of this brief, and one we will continue to pursue in future efforts.

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. © 2026 Carta. All rights reserved. Reproduction prohibited.