- RSA vs. RSU

- What are RSAs and RSUs?

- What is a restricted stock award (RSA)?

- Why companies grant restricted stock awards

- What is a restricted stock unit (RSU)?

- Why companies grant restricted stock units

- RSAs vs. RSUs

- Vesting schedules for RSAs and RSUs

- RSA vesting

- RSU vesting

- How termination affects RSUs and RSAs

- Termination and RSAs

- Termination and RSUs

- Taxes on RSAs and RSUs

- RSA tax

- Section 83(b) election

- RSA with no 83(b) election

- RSA with an 83(b) election

- RSU tax

- RSU tax: liquidation scenario

Restricted stock awards (RSA) and restricted stock units (RSU) are two alternatives to stock options (such as ISOs and NSOs) that companies can use to compensate their employees. While stock options offer employees the “option” to buy shares at a fixed price, RSAs and RSUs are grants of stock. Although the employee sometimes pays nothing up front for the stock, they don’t take full ownership of it until they meet certain conditions.

Below, we’ll review RSAs vs. RSUs, the key differences between these two types of equity awards, and how each is affected by vesting, termination, and taxes.

What are RSAs and RSUs?

RSAs and RSUs are types of equity that companies award to employees and other service providers. While a stock option gives you the right or “option” to buy a set number of shares at the designated strike price, you don’t own the shares until you exercise your option to buy them.

With RSAs and RSUs, you’re the legal owner of the shares from the date they are issued to you (although exactly when the underlying shares are issued depends on the type of equity award).

What is a restricted stock award (RSA)?

Restricted stock awards (RSA) are a type of equity compensation that grants you company stock with certain restrictions. You’ll own the shares on the date the grant is issued and you satisfy any purchase price requirements, but typically, the shares will still be subject to vesting conditions. RSAs are considered “restricted” stock, because the shares cannot be freely transferred or traded, which allows the company to stay in compliance with securities laws.

Why companies grant restricted stock awards

RSAs are generally issued by very early-stage companies when the fair market value (FMV) of common stock is very low—this way, employees don’t need to pay a lot to have ownership in the company, and they won’t get hit with a significant tax burden if they receive the shares as compensation instead of purchasing them outright.

RSAs also have some advantages over certain types of options. Unlike options, RSAs don’t have to be exercised, and you start the long-term capital gains holding period when you acquire them. In addition, they don’t have to satisfy the additional ISO holding periods. RSAs help startups compete for talent against larger companies that can pay higher salaries by allowing the companies to offer equity with high upside potential.

What is a restricted stock unit (RSU)?

Restricted stock units (RSU) are rights to acquire shares of common stock, under which the shares will be delivered to you as you satisfy certain conditions. The vesting schedule and other conditions for an RSU grant are outlined in the RSU agreement.

Although you typically won’t have to pay anything to acquire the shares (outside of applicable taxes), the fair market value (FMV) of vested RSUs will be treated as compensation at the time they are delivered to you by the company and, as a result, will be considered taxable income. In other words, instead of receiving a bonus from your company in cash, think of vested RSUs as a bonus paid in company shares.

Why companies grant restricted stock units

When a company begins to enter its growth phase, it usually makes sense to use stock options (ISOs and NSOs) for the majority of a company’s equity compensation plans instead. Options also give employees flexibility when it comes to tax treatment.

But once a company is mature and successful, the high strike price to purchase company stock options can become unaffordable for most employees. RSUs then become a more viable tool for incentivizing employees through stock ownership.

RSAs vs. RSUs

The two types of restricted stock equity awards—RSAs and RSUs—have differences when it comes to purchase cost, vesting, taxes, and terms upon termination.

Restricted stock awards (RSAs) | Restricted stock units (RSUs) | |

Stage of company | Very early stage, low FMV | Later stage, mature companies, high FMV |

Price to purchase | Typically FMV, but can be in cash or as compensation for services | Typically no cost, but the recipient needs to pay tax withholding* |

Issued | Shares issued at grant (subject to the satisfaction of any purchase price requirements); the company maintains a repurchase right until the shares are fully vested | Shares issued upon settlement (usually, but not always, correlated with vesting) |

Vesting | Usually time-based and/or milestone vesting conditions | Can have standard time-based and/or milestone vesting or an additional required event for vesting, e.g. the company going public or getting acquired (“double-trigger”)** |

Section 83(b) election | Must be filed if the shares are subject to vesting | Is not applicable |

Termination | Unvested shares will be repurchased by the company. | Unvested RSUs are forfeited back to the company immediately |

Tax status | Help maximize capital gains; Taxed as ordinary income if not purchased in cash at FMV | Taxed mostly as ordinary income when settled |

*Employers are required to withhold 22% for federal income taxes on the first $1M in supplemental income for employees, and 37% of any amount exceeding $1M. Your RSUs are taxed as supplemental income.

**This differs from double-trigger acceleration for early-stage company equity

Vesting schedules for RSAs and RSUs

Timing is key with RSAs and RSUs: When you acquire the shares and when you sell them are important factors in determining the full value and tax implications of these equity compensation awards.

The most common vesting conditions placed on RSAs and RSUs are time-based and involve a vesting schedule, which means you earn full rights to the shares over time. Time-based restrictions incentivize employees to stay with the company. Other vesting schedules may be based on certain milestones or achievements related to the performance of the individual or the company.

RSA vesting

Because you acquire RSA shares when they are granted to you, RSA vesting only impacts whether the company can repurchase your shares if you leave or are terminated, and does not affect your tax obligations. Most companies have time-based vesting schedules in place to prevent individuals from joining a company, receiving their RSA award, and leaving immediately with the ownership of their full equity grant without having “earned” it. Vesting also aligns personal outcomes with company outcomes throughout the organization. While time-based vesting is the standard for RSAs, milestone-based vesting can also be used, but is more rare.

RSU vesting

RSU shares are not issued to the recipient until they vest and are settled by the company, and can have multiple vesting conditions. If your RSUs have a single-trigger vesting schedule, or if you have liquid RSUs, then you typically only need to satisfy a time-vesting requirement.

Single-trigger vesting | |

Time-based | Your equity grant vests over time |

Event-based | Your equity grant vests when a specific event occurs. |

RSUs can also be subject to double-trigger vesting. A common additional vesting condition for RSUs is a company liquidity event, such as an acquisition or initial public offering (IPO). With this type of “double-trigger” vesting, both conditions must be satisfied for your shares to vest. This allows the employee to delay their tax obligations until the shares are liquid enough that they can sell some shares to offset their out-of-pocket tax payments.

Double-trigger vesting | |

Time-based and event-based | Both conditions must be satisfied for your shares to vest: (1) the time-based component and (2) the event-based vesting condition |

How termination affects RSUs and RSAs

Take a look at what happens to RSAs and RSUs when you leave a company with vested shares vs. unvested shares:

RSAs | RSUs | |

Vested shares | You keep them | You keep them* |

Unvested shares | Subject to repurchase by your company | Forfeit at termination |

*Unless the RSU is structured to expire if termination happens before all vesting conditions are met (i.e; liquidity event does not happen before you leave the company). This is also known as “must be present to win.”

Termination and RSAs

You’ll keep all of your vested RSA shares when you leave, but any unvested shares are subject to a company repurchase. That means your company has the right (but not the obligation) to buy the shares back, usually at the lesser of the price you paid for them or the current FMV.

Termination and RSUs

You’ll also keep vested shares of RSUs when you leave, but there is one caveat: Because RSUs are often subject to additional vesting conditions (like a liquidation event), it is possible that any time-vested shares will expire before all conditions are met. If your shares expire, for example, before the company gets acquired, goes public, or holds a secondary transaction, you will not get to keep them. Regardless of liquidation conditions, any RSUs that are not time-vested are forfeited at termination.

If you’re earning RSUs, your grant agreement should explain what will happen to your RSUs in the event you leave the company—including if and when double-trigger RSUs will expire.

Taxes on RSAs and RSUs

There are two types of taxes to consider with equity compensation: ordinary income tax and capital gains tax. The long-term capital gains tax rate is currently lower than the ordinary income tax rate. If an employee holds stock for more than a year between acquisition and sale, any increase in value is taxed as long-term capital gains.

RSA tax

When you’re granted RSAs by a company, you have to pay a certain price per share to acquire them. If the cash purchase price you paid equals the FMV, you do not owe ordinary income taxes on the RSAs at the time of the grant.

Section 83(b) election

If your RSA includes vesting, then you will need to file an 83(b) election with the IRS.

Without an 83(b) election, you would owe ordinary income tax at each vesting event (e.g., at the cliff and every month thereafter for a standard four-year monthly vesting schedule with a one-year cliff). The taxes would be calculated on the difference between the FMV at the time of vesting and the initial purchase price. As the company’s value grows over time, this could lead to significant tax burdens in the future.

Sending an 83(b) election to the IRS means that you can choose to pay all of your ordinary income tax up front on an RSA, at a time when the FMV equals the strike price (so there is no taxable difference). RSA recipients should file an 83(b) election within 30 days of the grant date.

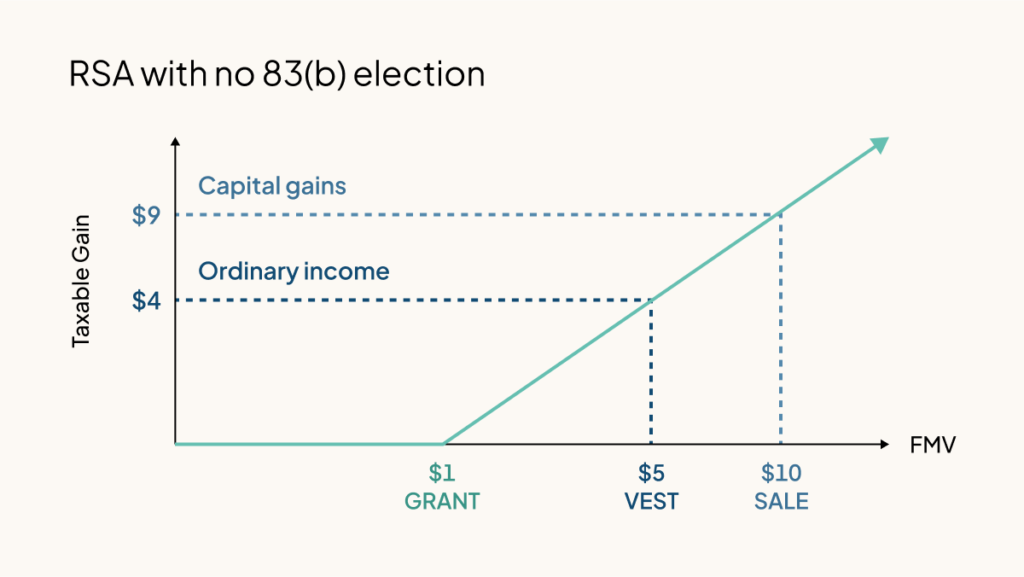

RSA with no 83(b) election

As the FMV increases over time, you’ll owe taxes on the difference between the FMV and the purchase price if you did not file an 83(b) election within the first 30 days of receiving your shares (more on that below).

The graph above shows a RSA’s taxable events over time, assuming a single vesting event. On the x-axis is the FMV of the shares. The y-axis (taxable gain) is the current FMV (at the time of the event) minus the FMV on the grant date ($1). As you can see, when shares are initially purchased at a cost equal to their FMV, the taxable amount at that time is zero.

Without an 83(b) election, for each vesting event after the grant date, the vested shares are subject to ordinary income tax on the increase in value from the purchase price. When the vested shares are then sold, any gain between tax basis set by the previous taxable event (vesting) and the proceeds from the sale is subject to capital gains tax. (Whether it’s at the short-term or long-term capital gains rate depends on whether you hold the shares for more than a year.)

The FMV of the stock could just as well decline after vesting, and the shares could end up being almost worthless. In the example above, the FMV has increased to $5 at the vest date, yielding taxable income of $4 per share.

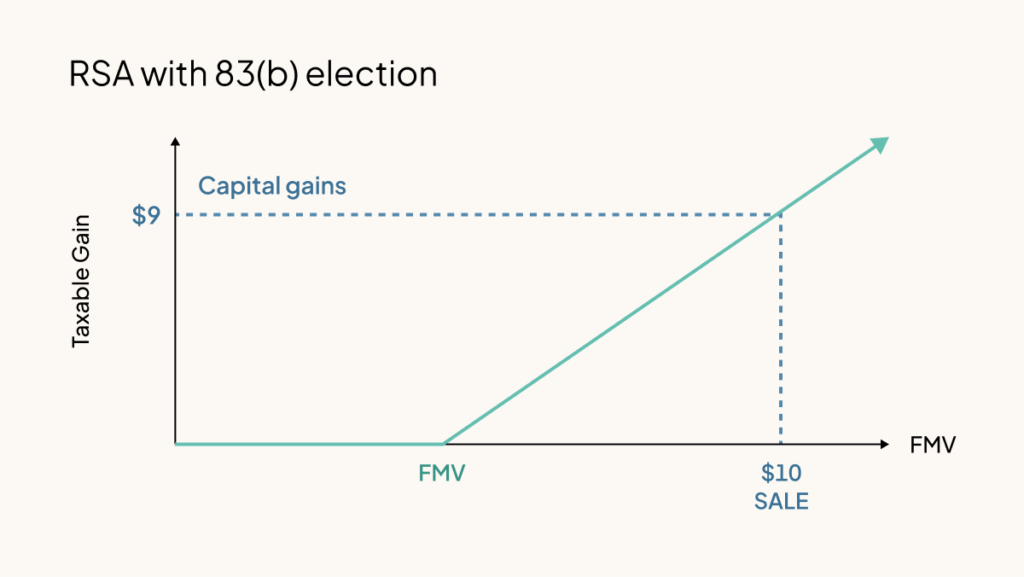

RSA with an 83(b) election

As shown in the example below, the taxable income is usually zero when you pay in cash and make an 83(b) election. This is because the FMV of the shares should be equal to what you paid for them.

Here, the taxable income is zero at grant because the FMV is the same as what was paid in cash: $1. By filing an 83(b) election, you choose to recognize ordinary income tax up front. Since the taxable amount above is $0, no tax is owed. (Note that if you had received the shares for services instead of cash, then you would owe income tax on the value of the shares at grant.)

Even as the RSA shares vest, no income tax is owed. Instead, you’d pay capital gains taxes on the full $9 gain when you sell the shares.

This is favorable for two reasons:

1) The long-term capital gains tax is currently a lower rate than the ordinary income tax.

2) Eliminates the risk of paying hefty additional taxes on illiquid shares that cannot be sold to offset the tax burden.

RSU tax

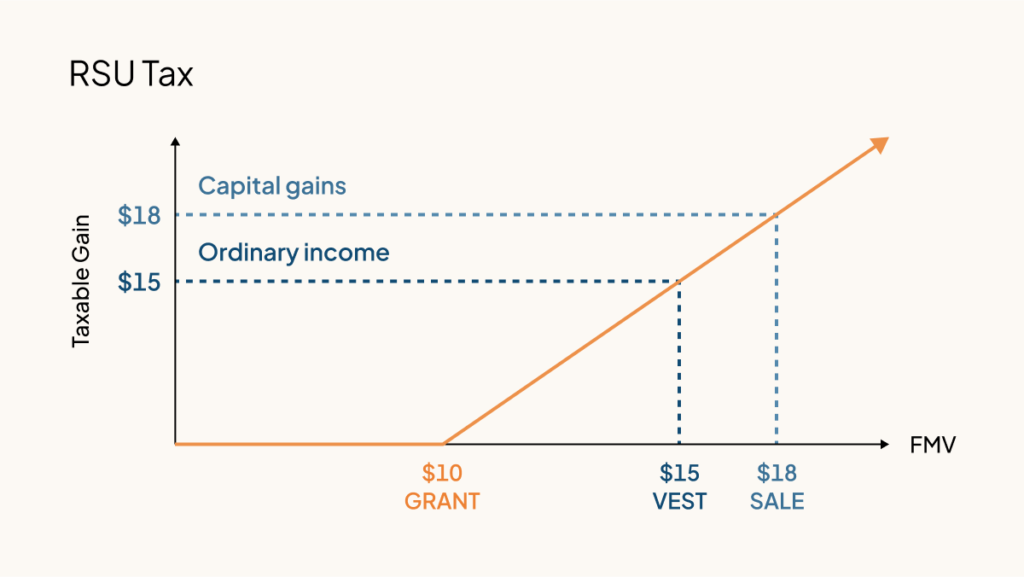

The main thing to know about RSUs and taxes is that you pay ordinary income tax when your shares settle. Some companies choose to settle RSUs (i.e., deliver the shares to the holder) at the time of each vesting event, but other companies may separate the two events.

In the example above, RSUs were granted when the FMV was $10 per share. Since you don’t receive any shares when the RSU is granted, you’re not responsible for paying taxes. The taxable amount is $0 on the grant date.

Instead, you’ll pay ordinary income tax on the full FMV when RSUs settle at the FMV of $15. Later, if you decide to sell your shares at $18 FMV, you’ll owe capital gains tax on the difference between the FMV at vesting and the $18 FMV at the time of sale.

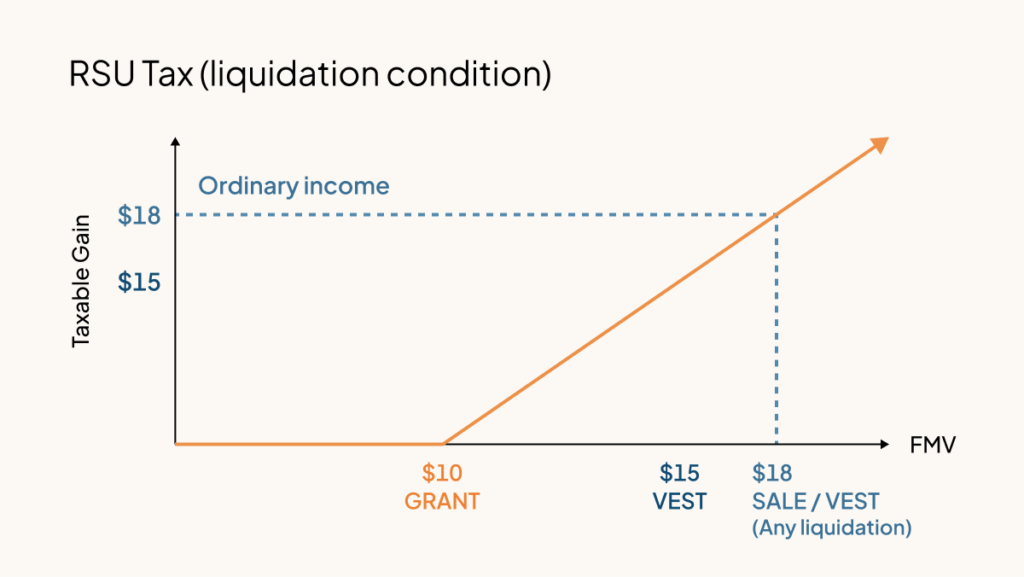

RSU tax: liquidation scenario

Remember that RSUs often have multiple vesting conditions; in the example above, we assumed the RSUs only had time-based vesting (single-trigger RSUs). Here’s how an additional liquidation condition affects RSU taxes:

The example above assumes you decided to sell your RSUs right when they fully vest. Since there’s a double-trigger vesting schedule, you’ll only be taxed when both the time-based vesting and liquidation requirements are satisfied and the shares are considered fully vested. When that happens, you’ll pay ordinary income tax on the entire value of the RSU ($18 per share) at the time you sell.

Restricted stock units and restricted stock awards can be confusing for employees and founders. The complexity increases for founders when restricted stock distribution starts impacting your company’s cap table and ownership structure. To learn more about how Carta can help, schedule a demo of our platform with one of our equity experts.

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. ©2026 Carta. All rights reserved. Reproduction prohibited.