The past year has been a complicated time for startup fundraising. For seed founders, 2023 was a mixed bag—valuations were 40% higher than they were three years prior, but deal count was down 30%, according to Carta data. In Q1 of this year, valuations climbed slightly, while deal count dropped even more at the seed stage.

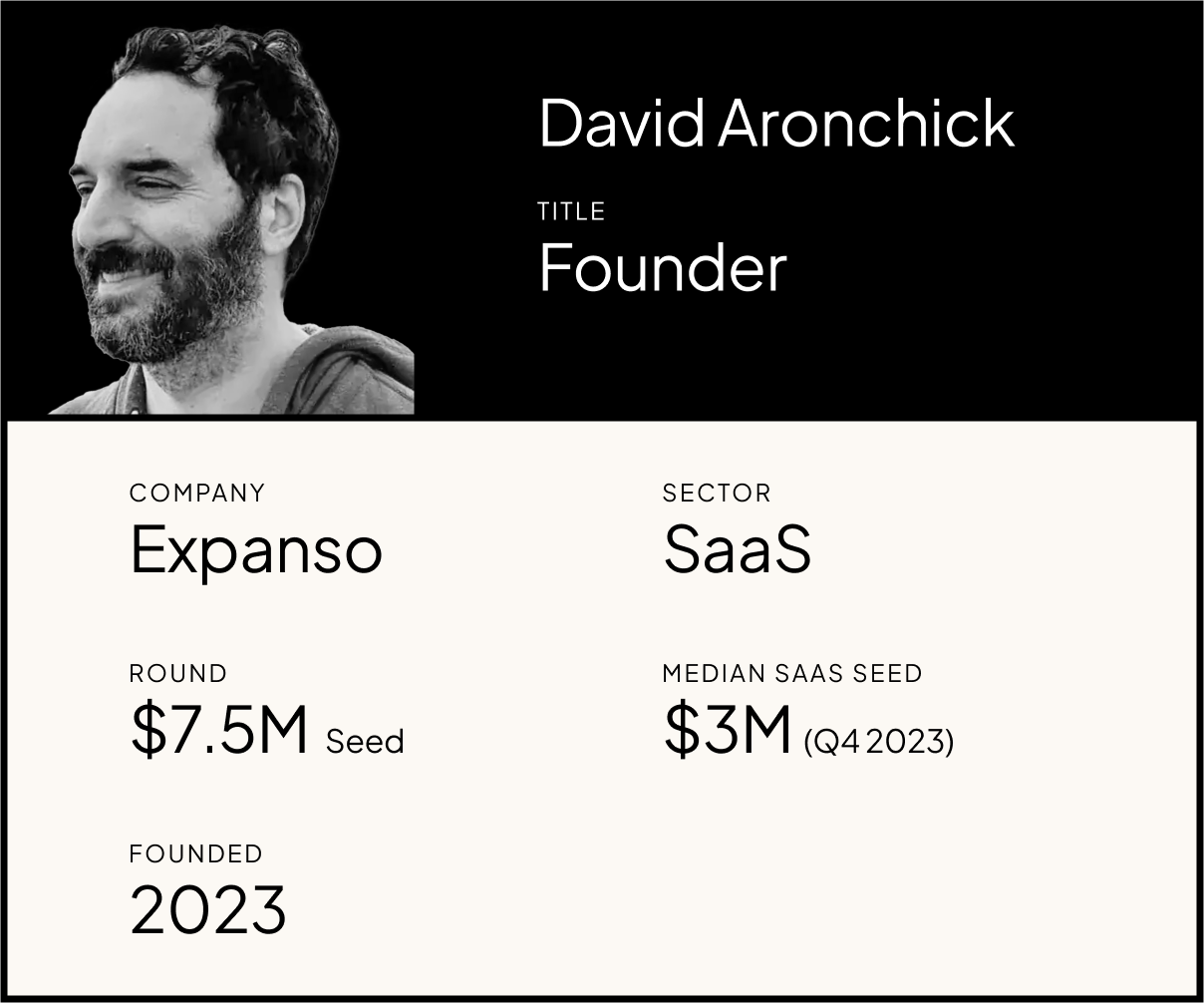

Amid this tricky landscape, Expanso, which helps enterprise companies manage their global data needs, announced in November a $7.5M seed round led by General Catalyst and Hetz Ventures, along with Array Ventures. The company builds on founder David Aronchick’s work on open-source software Bacalhau, built to reduce costs, and improve efficiency of processing large-scale datasets in distributed environments.

Before Expanso, David was head of Open Source Machine Learning at Microsoft, and product manager for Cloud AI and co-founder of Kubeflow at Google.

We sat down with David to talk about raising amid complex market conditions, and his advice to fellow founders tackling a fundraise.

Highlights

The importance of running an efficient fundraising process

The “pre-process” and how to lay the groundwork before you officially raise

Pitch deck essentials

The goldilocks round—how to raise as little as possible, but as much as you need.

CARTA: Tell us about the decision to raise this round.

DAVID ARONCHICK: As we built out our open-source software project Bacalhau, we knew that a large part of it was going to be an enterprise play; there are only a certain number of institutions that have these issues at the global level we were solving.

So once you start getting into that enterprise motion, instead of a bottoms-up motion, you end up having a conversation about how to fund it.

Ultimately we just felt like the only way to do this right was to spin this out properly as its own company. And that meant really leaning into the engineering, sales, and solutions engineering motion that we’d need.

And so, we realized that the way to do this was to form Bacalhau into its own company, and to take funding.

We took probably a bit more funding than we initially expected. We just had so much interest. And more funding was okay for us because we knew that for an enterprise product it was going to be a very long sales cycle, so we really did have to plan for this being a longer road. So we were happy that we raised as much as we did.

I’m curious how you structured your approach to the round, to generate interest and find the right investors.

Fundraising is always very specific to the startup and the investors. I was lucky enough, with my prior experience at Google and at Microsoft, to develop a deep background in these various communities, and I knew a lot of the right players before our fundraise.

When I approached the fundraise, I wanted to start by just getting a sense of the market. It was such a crazy time. Just before we started raising, there was the massive collapse in crypto, where millions of dollars were falling off the table. There was inflation. SVB [Silicon Valley Bank] went bankrupt.

There was a whole bunch of stuff. And we're like, “Geez, when should we do this?”

My philosophy on fundraising is once you start your process, you really have a very finite amount of time to fundraise. Call it 60 to 90 days maximum. Because after a certain amount of time, you're like a dead fish, you just begin to smell. People start to wonder, “Why is this still out there? Why are they still raising? Why aren't they getting back to building?”

So for us, we really wanted to line everyone up before we said go. I wanted to get everyone’s opinion about the people I wanted to raise with before I officially started.

Then we were lucky to be part of a Raise Day where we were able to present and announce that we were officially raising. After that announcement, I sent my notes to everyone who I had sat down with during the pre-process. And we were very lucky and got term sheets very quickly.

Let’s dig into that pre-process. Tell us about what information you wanted to gather. What were these early conversations like?

It's a really subtle thing. You have to be very careful not to start before you start.

In these [pre-fundraise] meetings, just say you're getting advice and you want to know whether or not you should do this. And you’re not just saying that, you really should get that advice. You can’t go out assuming you know everything, or every investor, or what the market looks like. As a founder, you've been spending your time building your company, not thinking about venture funding.

So getting advice is really good. Go in transparent and say, “Look, I don't know whether or not I'm going to raise. I'm trying to get a sense of the market.” Have the conversation and see where they are.

At the end of that conversation, most great investors will say, “When the time comes, absolutely, pitch me." Because they want to see the deal when it comes through.

But you can’t take that as a guarantee that they’ll want to invest. Wanting to see the deal and wanting to write a check are two very different things. It’s not that investors are lying to you or being misleading. But it's a very different conversation when they have to write their deal memo.

So you should calibrate your expectations accordingly. Everyone is preserving optionality for themselves, right? The VCs will want to see your business plan when it's fully formed. You may get some answers right away that it’s not a right fit, and that’s helpful to know too.

But expect early on that most people will say they want to hear more, but there’s a lot between hearing the full pitch and the deal memo.

At a certain point you have to level. Don’t hesitate to be blunt about it. Like, “You’ve seen the deck, what do you think? Are you going to invest?” Because after a certain amount of time, you have to figure out how to save your time and be efficient.

Speaking of the deck, what did you include in the pitch deck? Did it evolve as you went through meetings?

That’s a great question, and similarly, it’s very specific for each company. Personally, I'm a believer in the really stripped-down pitch deck, as tight as you could possibly get it, that's your goal. And the reason is mostly because people have a very limited amount of time. And while no template is perfect, the ten slide thing is not the worst idea in the world.

So what does this look like? You start out with your broad problem statement, something that everyone can get behind.

Then you go into your solution and talk about what works and what doesn't to solve this problem. You have a little bit more in detail about what your solution is, but if you're talking more about your solution than one or two slides, you're probably doing too much.

Talk about customers that you've had, talk about the team you've had.

Talk about traction that you've already shown, and talk about how you're going to use your money.

And that's basically it, and each one of those is a slide.

There's lots of feedback that you're going to get along the way, lots of questions that people are going to ask. Do listen to the feedback, but realize that every bit of feedback is subjective, and take only about 10% or 20% of it at most. Otherwise you're just going to be thrashing around constantly trying to please everyone.

You mentioned earlier about wanting to get a feel of the market before your fundraise. Let’s talk about that market. What were term-sheet negotiation dynamics like when it came to valuation?

I'll be honest, I think it's pretty crazy out there. You really don't have a single way to map any sort of predictions. We had ideas about what things would cost, but by and large, we just said, “We'll let the market decide, and that's fine with us.”

There are lots of materials out there that talk about various functions and, you know, "You have this much traction, you have this many downloads, you have X and Y so your valuation should be Z.” But it really is about what the market will bear.

But if you think about it from the VC angle, the partner who's trying to put this valuation together, the first thing that they're going to do is go find comps, see what is out there to compare your company to, and what those companies are valued for, what they’ve raised recently.

And so that's the best thing you could do as well. Go look at what your potential comps are, and do your best to be honest with yourself about how you match up. That's basically as good as you can get. Outside of that, it's really hard to map onto anything specific.

Did you have a goal in mind for how much you wanted to raise?

So you want to raise as little as humanly possible, but no smaller than you need to be able to show the traction required for the next round.

Striking that balance can be a big challenge. You don't want to over-raise. You don't want to under-raise. Picking out exactly what that looks like, again, it's very, very specific to the organization, the business that you're in and so on.

I have always been under the impression that you want to raise enough to get between two to three years of traction. But you want to think about how you can do that and still raise as small a round as humanly possible, because the most expensive money you're going to raise is the first round, and then the most expensive after that is the next one, and so on. And so the less money you can take at the beginning, the better.

However, if you don't raise enough and you have to go out again while you haven't made as much traction, you're effectively dead in the water.

I don't want to freak anyone out, but this is one of the biggest challenges that you can have is getting the exact right raise size. For us, when we were raising, I wanted enough to get us a solid three years of runway, even pre-revenue.