The startup fundraising environment is less friendly today than it was two years ago. There are plenty of ways to prove it.

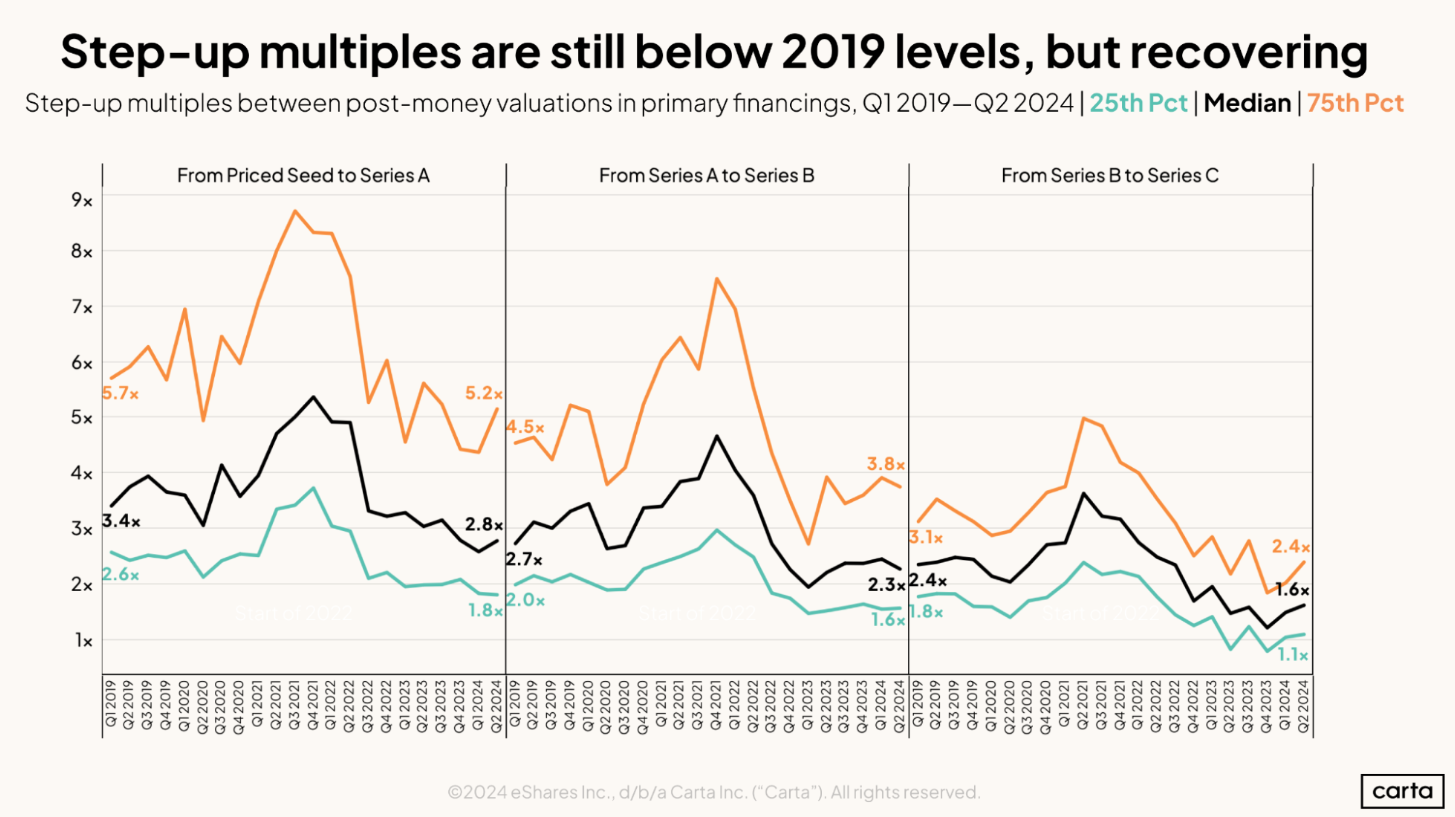

Take the rate at which startup valuations are growing. In Q2 2024, the median startup raising a Series A round achieved a 2.8x valuation increase over its seed valuation. Back in Q2 2022, that median valuation step-up multiple at Series A was much higher, at 4.9x.

Valuation growth has slowed at later stages, too. At Series C, the median step-up multiple was 1.6x during Q2 2024, down from 2.5x two years ago.

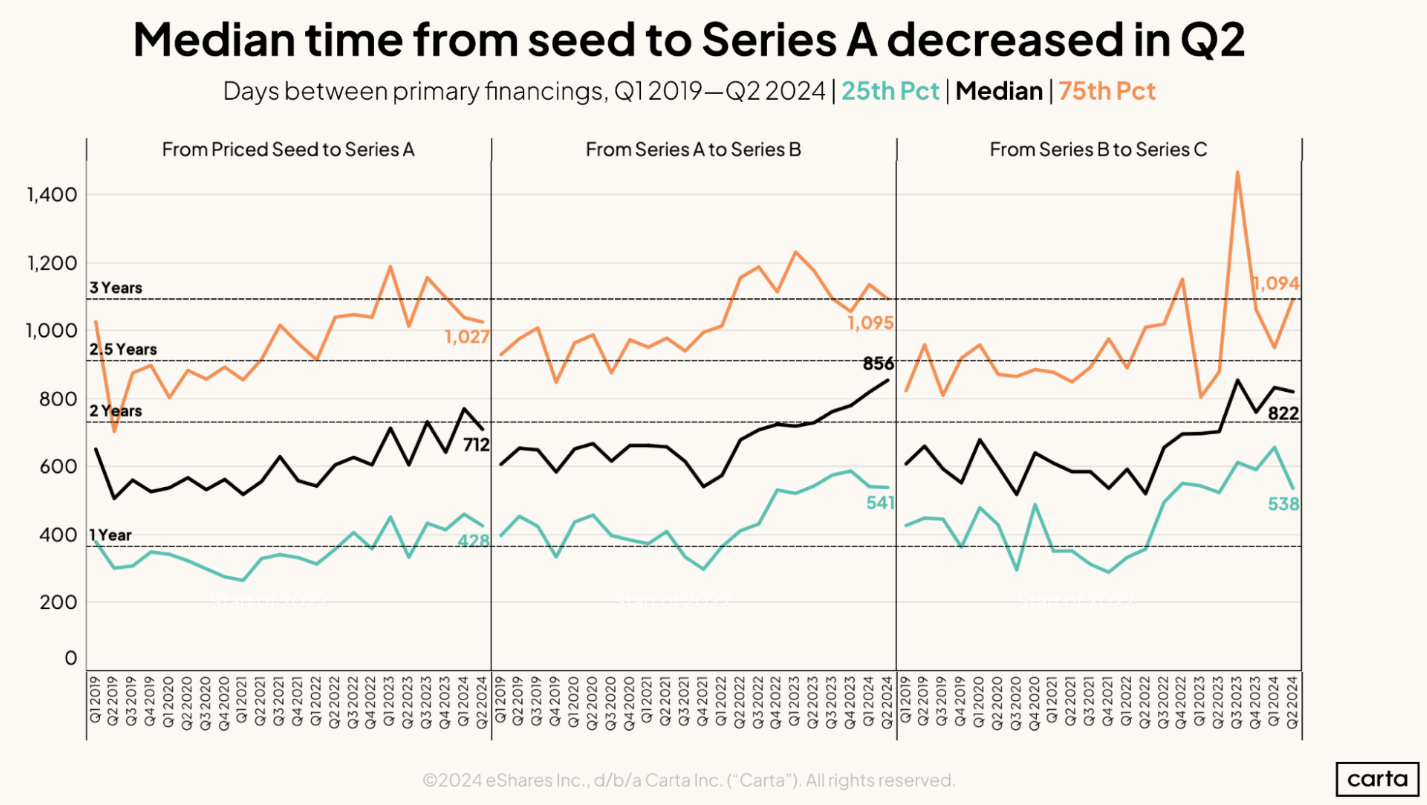

For another example of how the landscape has grown rockier, look at the typical time in between venture rounds. Two years ago, the median Series A round took place 607 days (about 20 months) after the company’s seed round. By Q2 2024, that gap was up to 712 days. Later stages have required even more patience: The median interval between a Series B round and a Series C increased from 681 days to 856 days over that same span.

Two years ago, the median company raising a Series C round had waited 522 days (about 17 months) since its Series B and achieved a valuation step-up multiple of 2.5x. In Q2 2024, the median company had to wait 822 days to raise its Series C—nearly 10 months longer—and achieved a valuation step-up of just 1.6x.

By several metrics, the startup market has begun to pick back up from last year’s low points. But these inklings of a recovery don’t change the fact that many founders have had to adapt to new fundraising timelines and valuation expectations.

The impact of larger seed rounds

Tim Eades has had a front-row view to how the fundraising market has shifted. He also has plenty of past experience to serve as context. A serial entrepreneur and longtime venture investor, Eades is currently the CEO of Anetac, an identity and security startup that emerged from stealth earlier this year with $16 million in funding spread across a seed round and a Series A.

This is a substantial nest egg for such a young startup—more substantial than similar startups might expect in years past. The median size of seed rounds logged on Carta in Q2 was $3.2 million, higher than it’s been in any quarter other than during the bull market’s peak of late 2021 and early 2022.

As Eades scans the landscape, he sees the making of a potential paradigm shift. For some startups, smaller step-up multiples and more time between rounds might not be a problem. In certain cases, a company that starts off with a larger seed check—and which is able to use AI to accelerate its early growth—might no longer be beholden to traditional venture timelines.

“Now, your seed rounds are so big, and you don’t need as much money to build the company, that I think you’re going to see that some of these companies that are raising money during the AI age will make their money go a lot further,” Eades says. “Because you can just do more with so much less engineering and with so much less understanding of your market.”

ZEDEDA’s fundraising journey

Said Ouissal is another founder with firsthand experience navigating the recent ebbs and flows of the venture market. He’s the CEO and founder of ZEDEDA, an edge computing startup that helps other companies manage and orchestrate their edge infrastructure.

ZEDEDA was founded in 2016 and went on to close its seed and Series A rounds in a largely friendly fundraising environment. When the company returned to market for its Series B, however, it was March 2020—the same month that the onset of the Covid-19 pandemic sparked chaos in global financial markets.

“It was not a great time to raise money,” says Ouissal, who ultimately guided ZEDEDA to a $26 million close on the Series B round in 2022, plus a second close later that year with additional capital from some of the company’s customers. “We saw that you have to be realistic in expectations and not go in expecting a certain outcome.”

Only a year later, the market had shifted again—at least for a company with metrics like ZEDEDA. After growing its annual recurring revenue by 250% year over year, Ouissal began to receive calls from investors who were eager for a seat on the company’s journey up and to the right.

“We started seeing a lot of inbounds last year from investors saying, ‘Hey, are you guys looking to raise?’ And at that point, we were not looking to raise,” Ouissal says. “It had only been six or nine months since that additional close, and we were in the midst of building and developing a pipeline and all that great stuff.”

But before long, Ouissal and his colleagues were won over by the prospect of raising new capital and partnering with intriguing new investors, such as Smith Point Capital, the firm founded by former Salesforce co-CEO Keith Block. This February, ZEDEDA announced $72 million in new Series C funding.

By raising such a large sum of capital so quickly after its previous round, ZEDEDA bucked some recent market trends. But to his fellow founder, that’s not necessarily a surprise. While many VCs are being cautious about deployments in the big picture, they’re still willing to battle for the right to invest in a certain segment of companies.

“What I’m seeing in the market right now is, when investors believe they have a real winner, they’re just piling in,” Eades says.

Raising the bar

With Anetac, Eades raised his seed and Series A rounds in relatively quick succession. But he noticed a key difference in how investors approached the two fundraising events.

“When we raised our seed round, I was still mostly leveraging relationships,” Eades says. Even if the company didn’t have an ironclad proof of concept, some LPs were willing to commit capital based on their belief in Eades and the team. “But when you come to your Series A, you really have to know the business. When you go from seed to Series A, there are a lot of expectations on you.”

In the pre-2022 market, a Series A startup could still be filling in some of the blanks on how the business would mature and eventually reach profitability. In the current market, that’s not the case: By the time a Series A rolls around, Eades says the time for experimentation is largely over.

“When you’ve done a larger seed round, they expect you to come into your Series A and know your market, know your customers, have customer revenue, understand your flywheel, understand your pricing level, all of that stuff,” Eades says. “Requirements have definitely gone up.”