Executive summary

In Q2 2024, the venture ecosystem showed modest signs of improvement, but not a drastic break, from Q1.

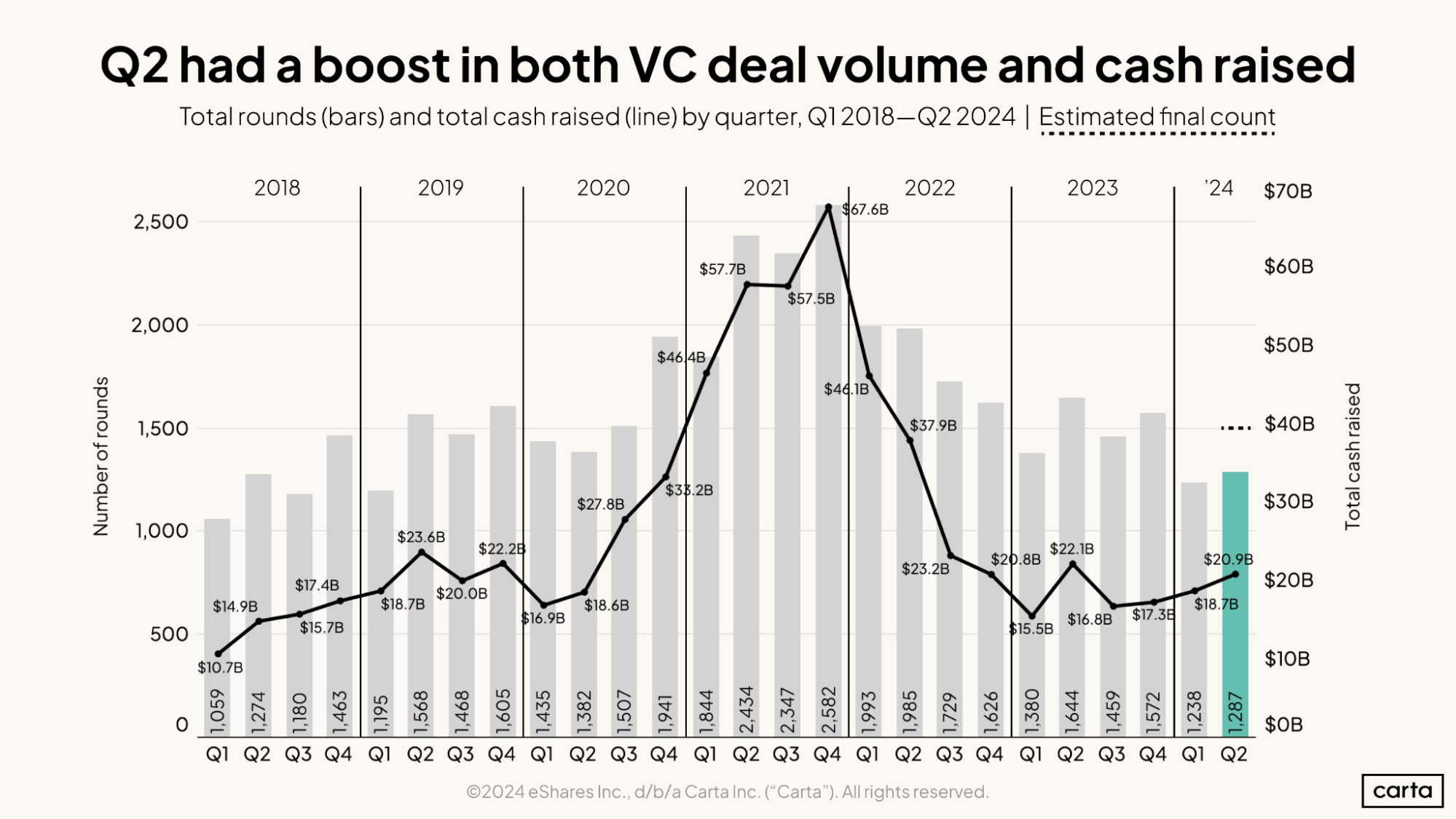

Based on current data, companies on Carta completed 1,287 new funding rounds in the second quarter of 2024, up 4% from Q1 2024. VCs invested a total of $20.9 billion in Q2, up 12% from Q1. Both of these figures will increase as more Q2 data is reported.

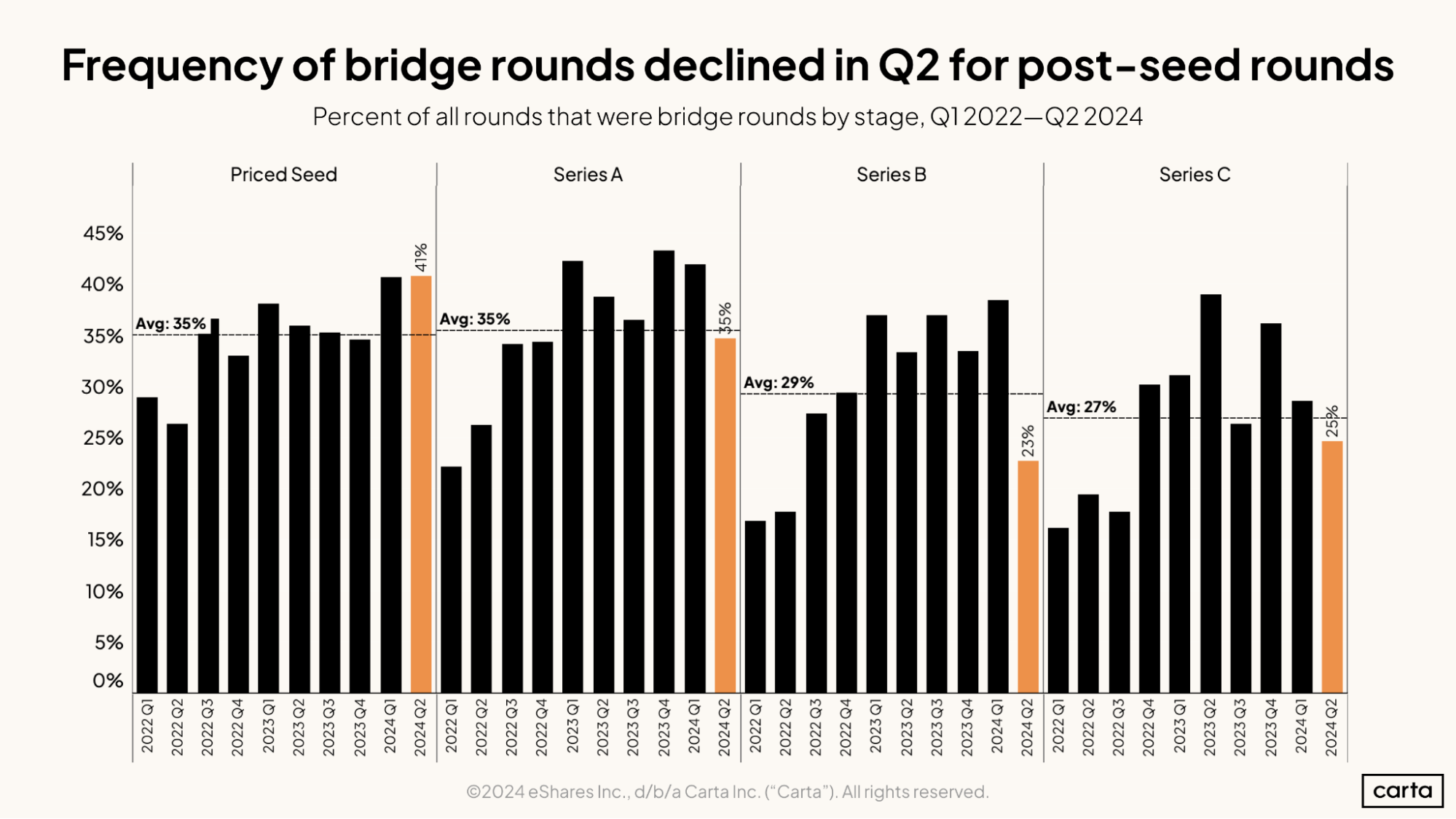

While Q1 experienced a record-high frequency of bridge rounds, there were fewer bridge rounds in Q2 at the Series A, B, and C stages. At the seed stage, the rate of bridge financings remained flat from Q1 at 41%.

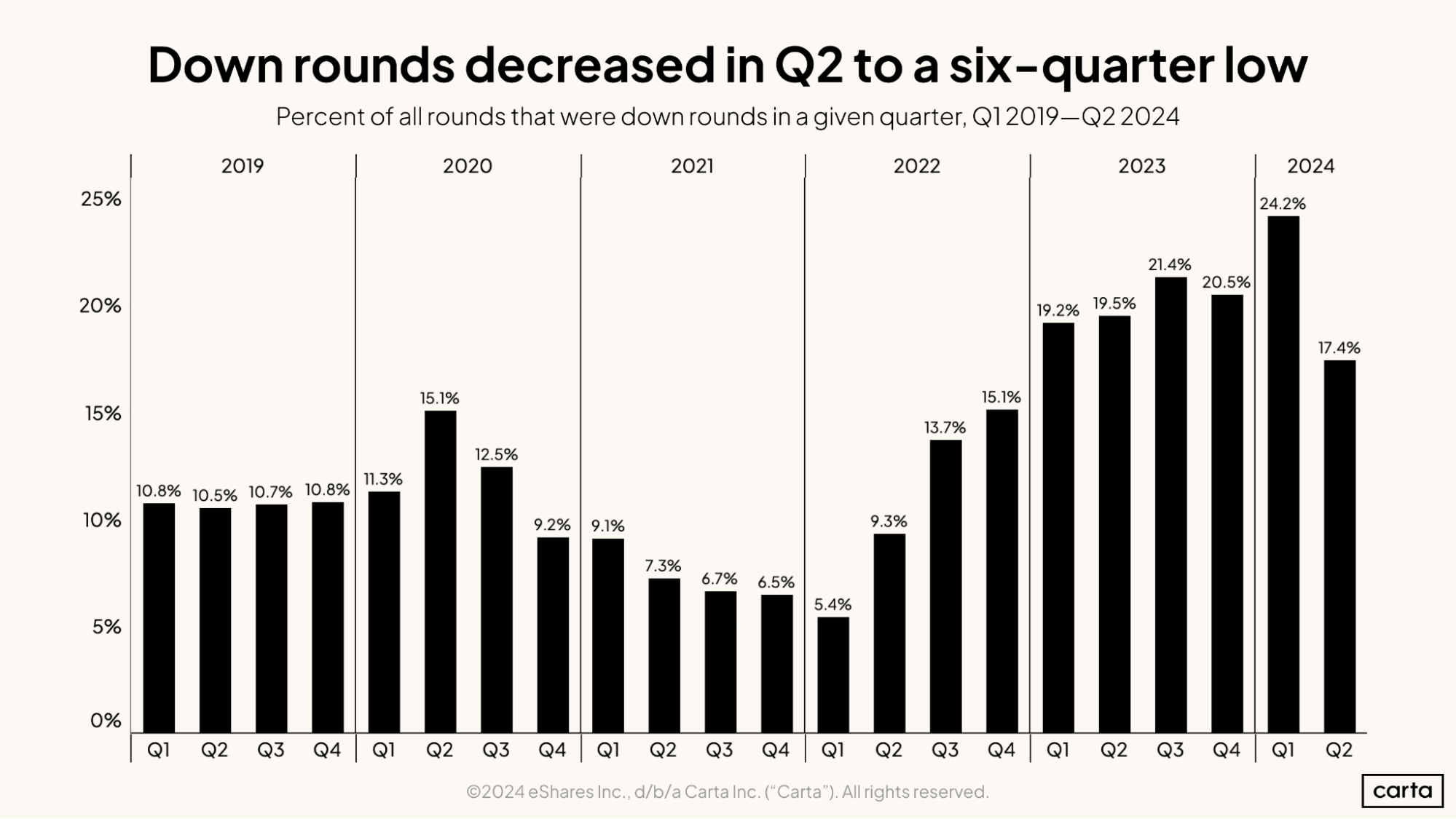

Median pre-money valuations rose at all stages in Q2 except for Series A, where they held steady. The rate of down rounds across stages fell from 24.2% to 17.4%. These findings indicate that founders were in better positions to negotiate higher valuations for their companies this quarter.

The year got off to a slow start in Q1, but Q2’s positive movement along multiple metrics could mean that better days are coming for U.S.-based startups.

Download additional industry-specific dataQ2 highlights

Positive signs in venture activity: The number of rounds and total cash raised by startups both increased this quarter. Primary round valuations rose at all stages except for Series A, where they held steady.

More founder-friendly environment: The rate of down rounds fell to a six-quarter low, and it is less common for deals to include structured terms that favor investors. Bridge rounds also fell for Series A through C.

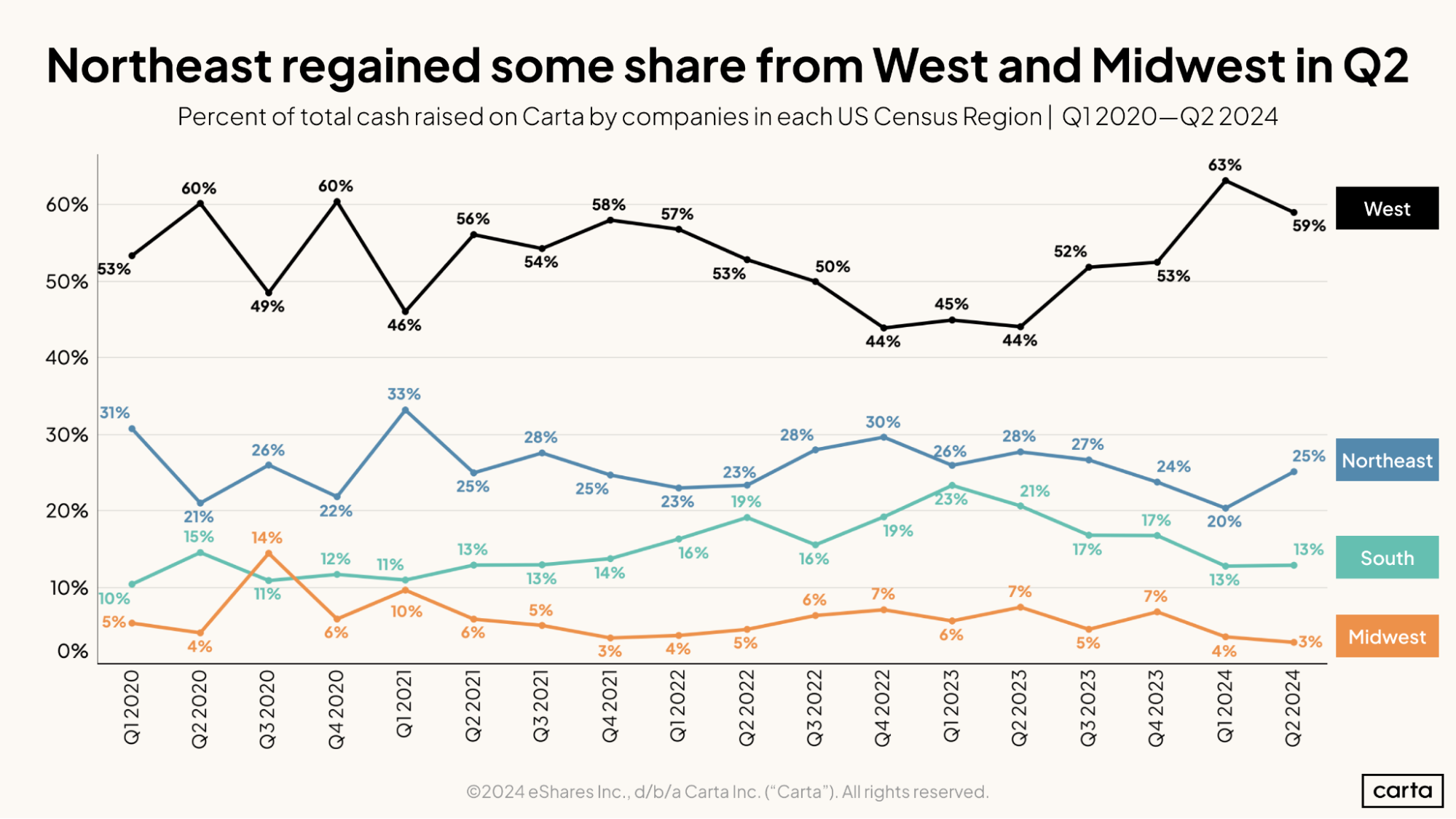

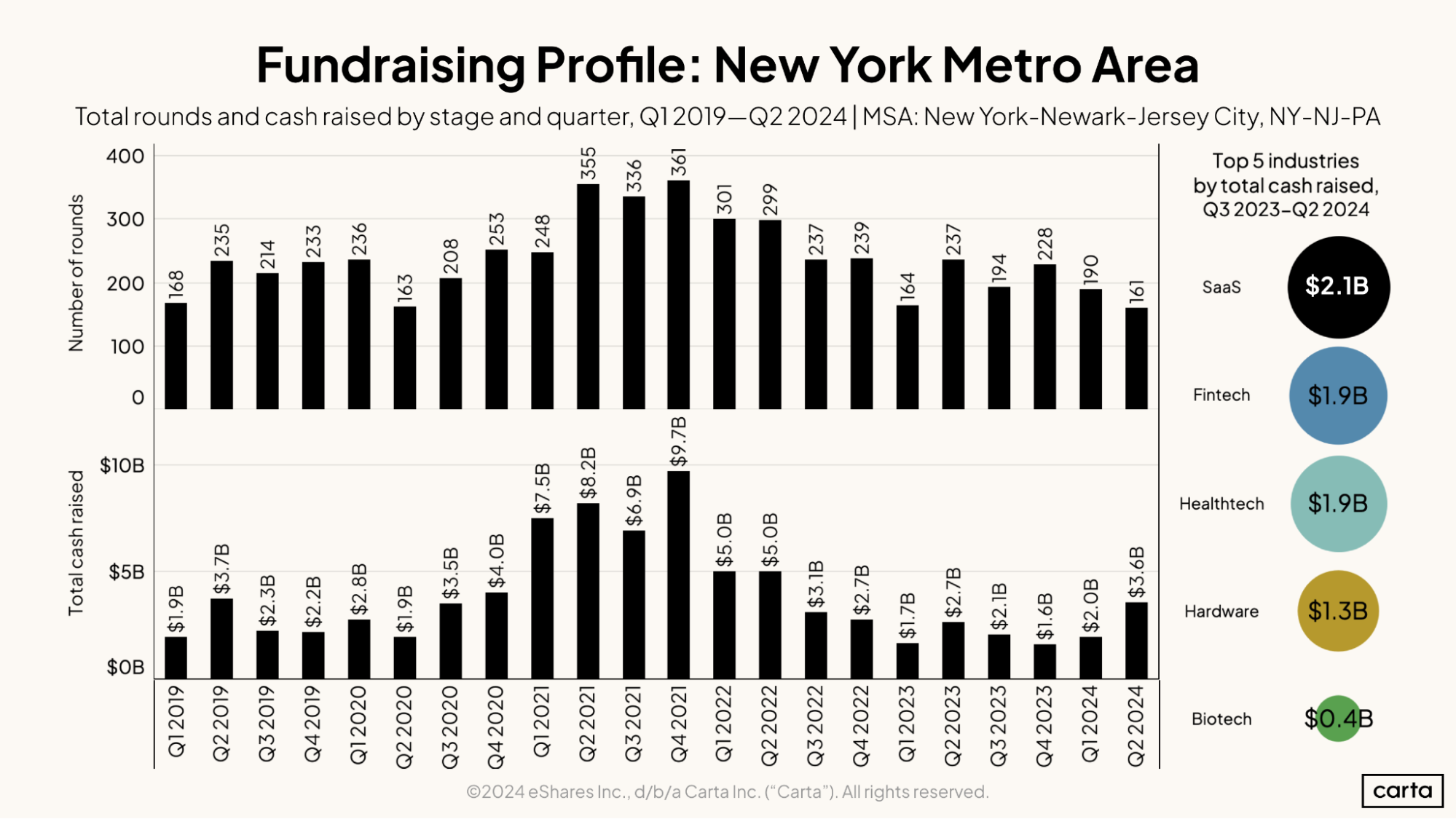

Northeastern recovery: Startups based in the Northeast increased their share of VC cash to 25%, at the expense of the West and Midwest census regions. The New York Metro Area brought in $3.6 billion this quarter, a notable increase from Q1.

Note: If you’re looking for more industry-specific data, download the addendum to this report for an extended dataset.

Key trends

The current data from Q2 2024 shows a boost in both deal count and total cash raised compared to Q1 2024. Q2’s deal count of 1,287 rounds totaling $20.9 billion is already a marked improvement over Q1. Both figures will increase further as some companies have a lag in reporting their data.

Q2 had the highest amount of VC cash invested in any quarter over the past year—and perhaps even longer, as data from Q2 financings continues to finalize in the coming weeks. The increase in deal volume relative to last quarter may indicate that Q1 was the trough and that market activity will stabilize or go up from here.

Q1 2024 represented a five-year high in the prevalence of down rounds, but Q2 reversed that trend. This quarter, the rate of down rounds fell from 24.2% to 17.4%. The falling trend is likely to continue. The downturn in VC fundraising is now more than two years old, which means that going forward, companies that are fundraising are more likely to have raised their most recent round in 2022 or after—in other words, after the period of inflated valuations that occurred in 2020-2021.

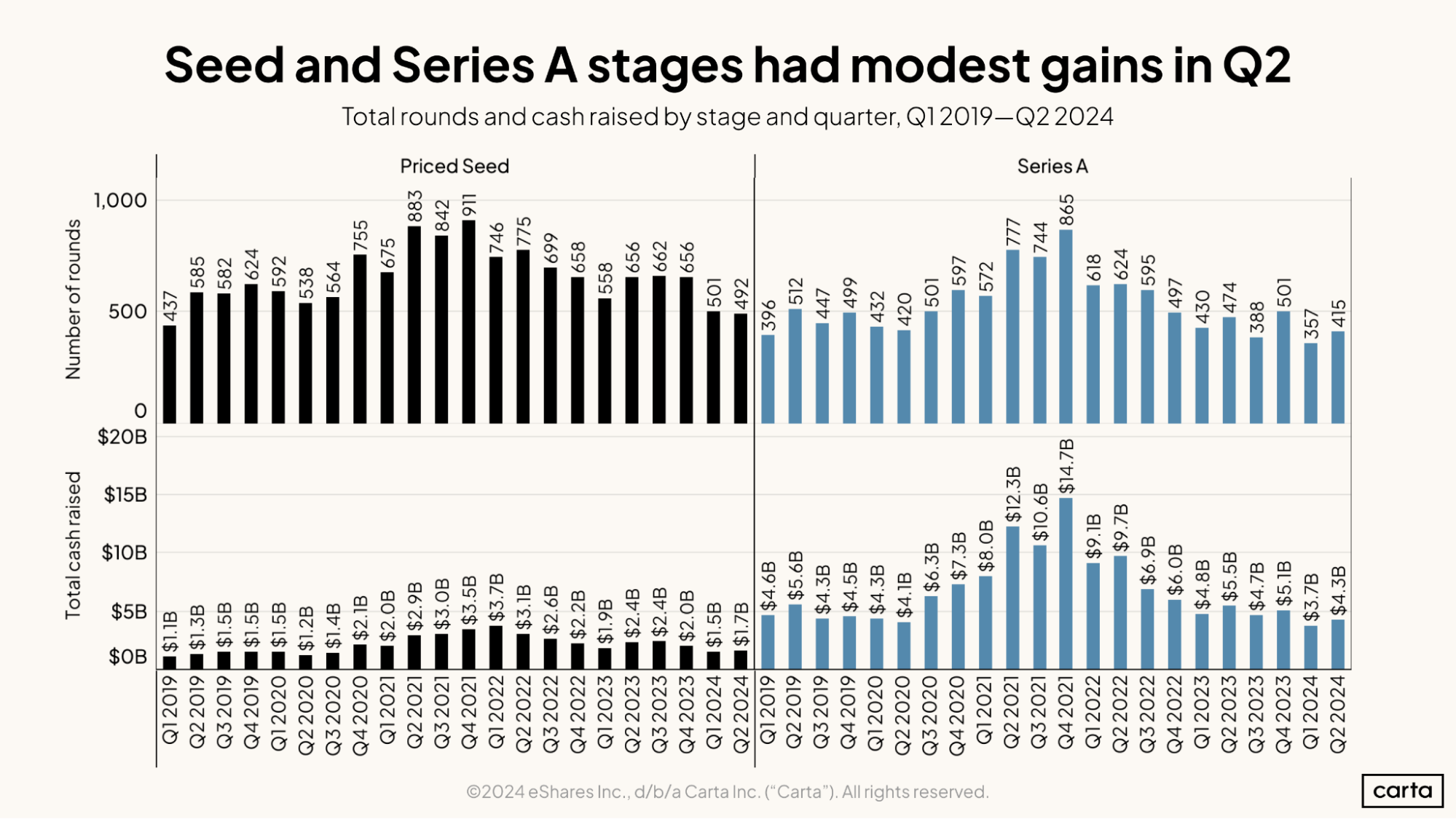

Seed deal count in Q2 is about even with Q1’s total, but Q2 will likely post a slight gain over Q1 after accounting for data lags. At the Series A stage, the data already shows that Q2 fared better than the previous quarter. The rebound in Q2 may represent a turning point from Q1, which had represented the lowest quarterly deal counts for both seed and Series A since early 2019.

Total cash raised for both stages increased modestly in Q2. At the Series A stage, Q1’s total cash raised was the lowest value recorded in the past five years. This quarter’s 16% increase still ranks Q2 among the lowest-earning quarters for Series A, but may signal the beginning of an upward trend.

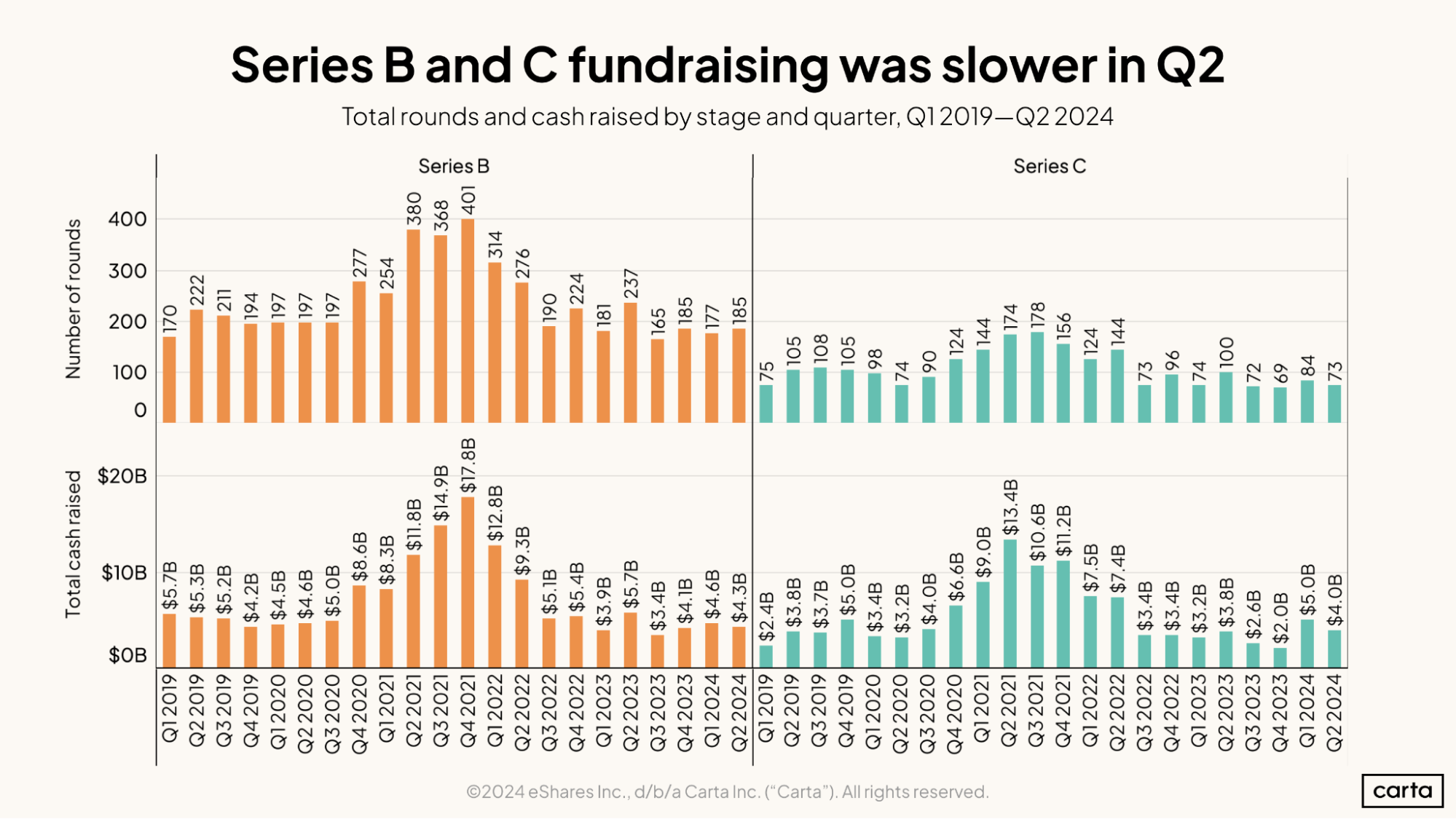

Companies in the middle stages of fundraising experienced a slower quarter. Although the number of Series B deals picked up slightly in Q2, total cash raised declined. For Series C companies, both deal count and cash raised declined this quarter, after previously gaining momentum in Q1.

Year over year, both of the middle stages have declined in deal volume. Q2 2024 saw 22% fewer Series B deals and 27% fewer Series C deals than Q2 2023.

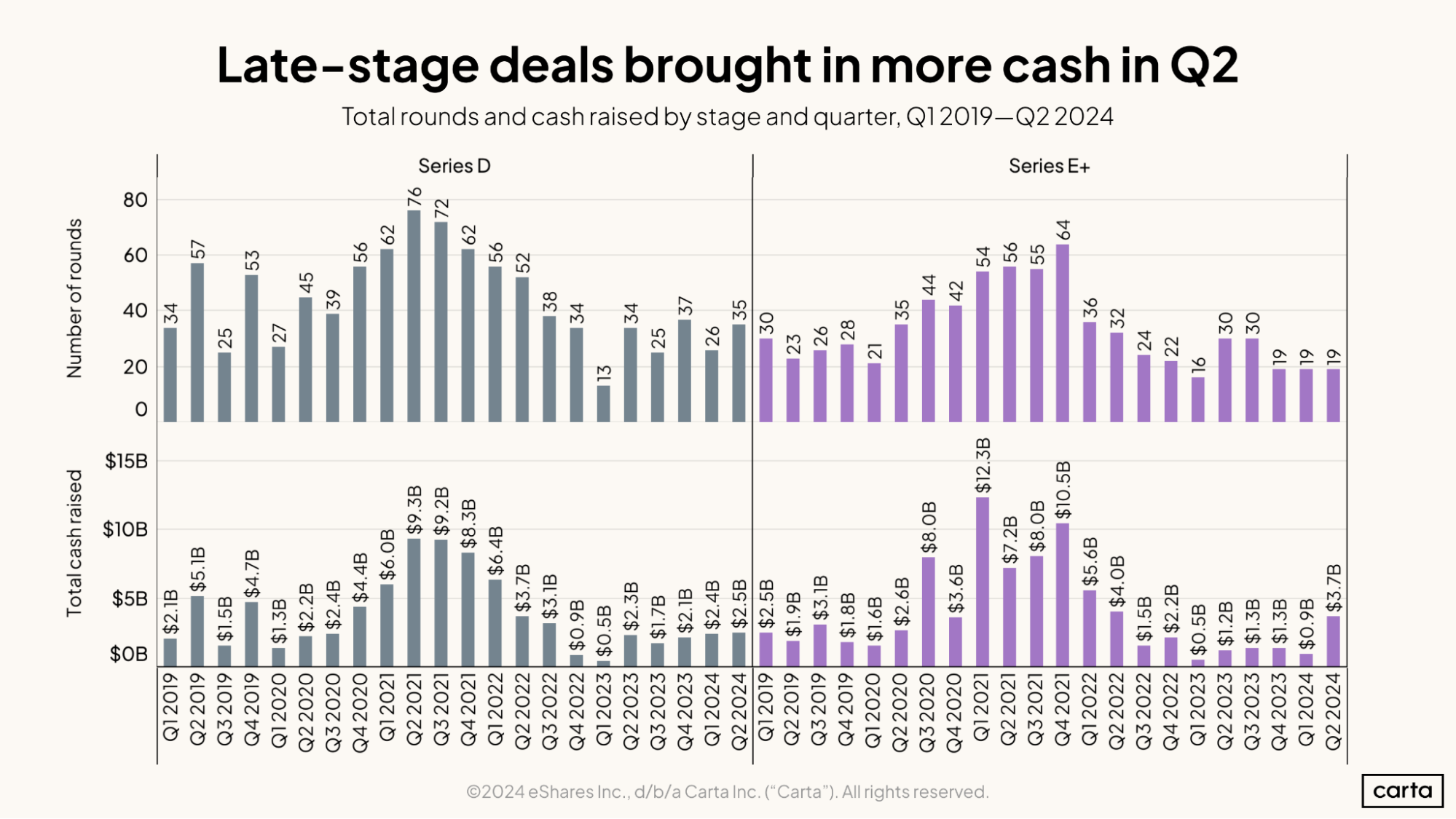

The volume of Series D deals recovered in Q2 after several quarters of volatility. There were 35 Series D deals on Carta this quarter, approaching Q4 2023’s count of 37. Deals at the Series E stage and beyond are rare and have remained flat at 19 deals for the past three quarters.

Series D deals raised a total of $2.5 billion in Q2, slightly up from $2.4 billion last quarter. Given the larger increase in volume, Series D deals raised smaller amounts of cash on average in Q2. On the other hand, the total cash raised at Series E+ surged over 300% in Q2. Considering the flat deal count, this means that rounds were larger on average.

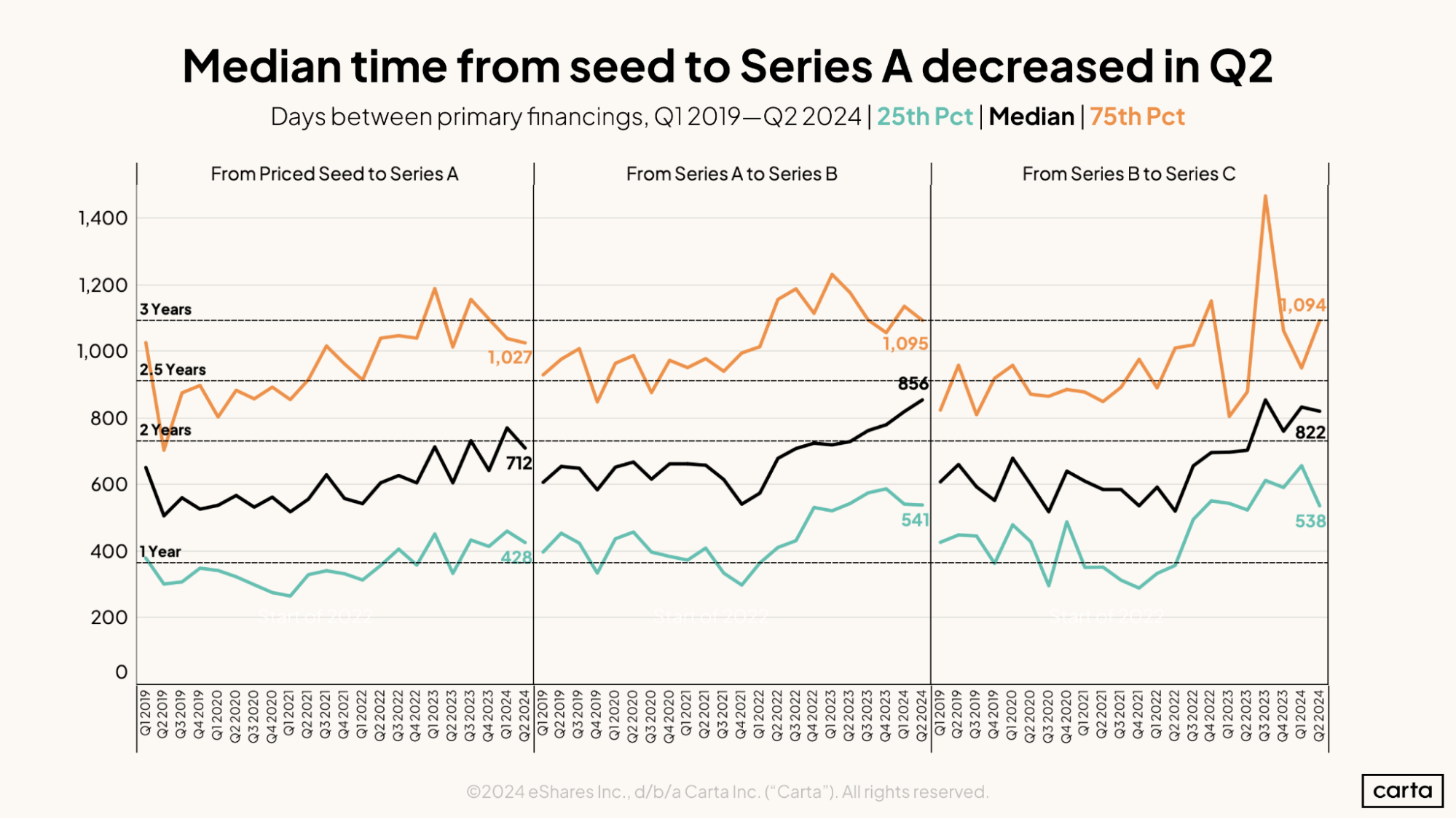

Startups that raised a primary Series A round in Q2 had waited a median of 712 days, or just under two years, since their seed financing. Although this is down from Q1’s peak of 772 days, it still reflects the broader trend of longer intervals between primary rounds.

Companies that raised a Series B round in Q2 waited a record median length of 856 days, approaching 2.5 years. The time between Series B and Series C slightly decreased this quarter to 822 days, but is also near record highs.

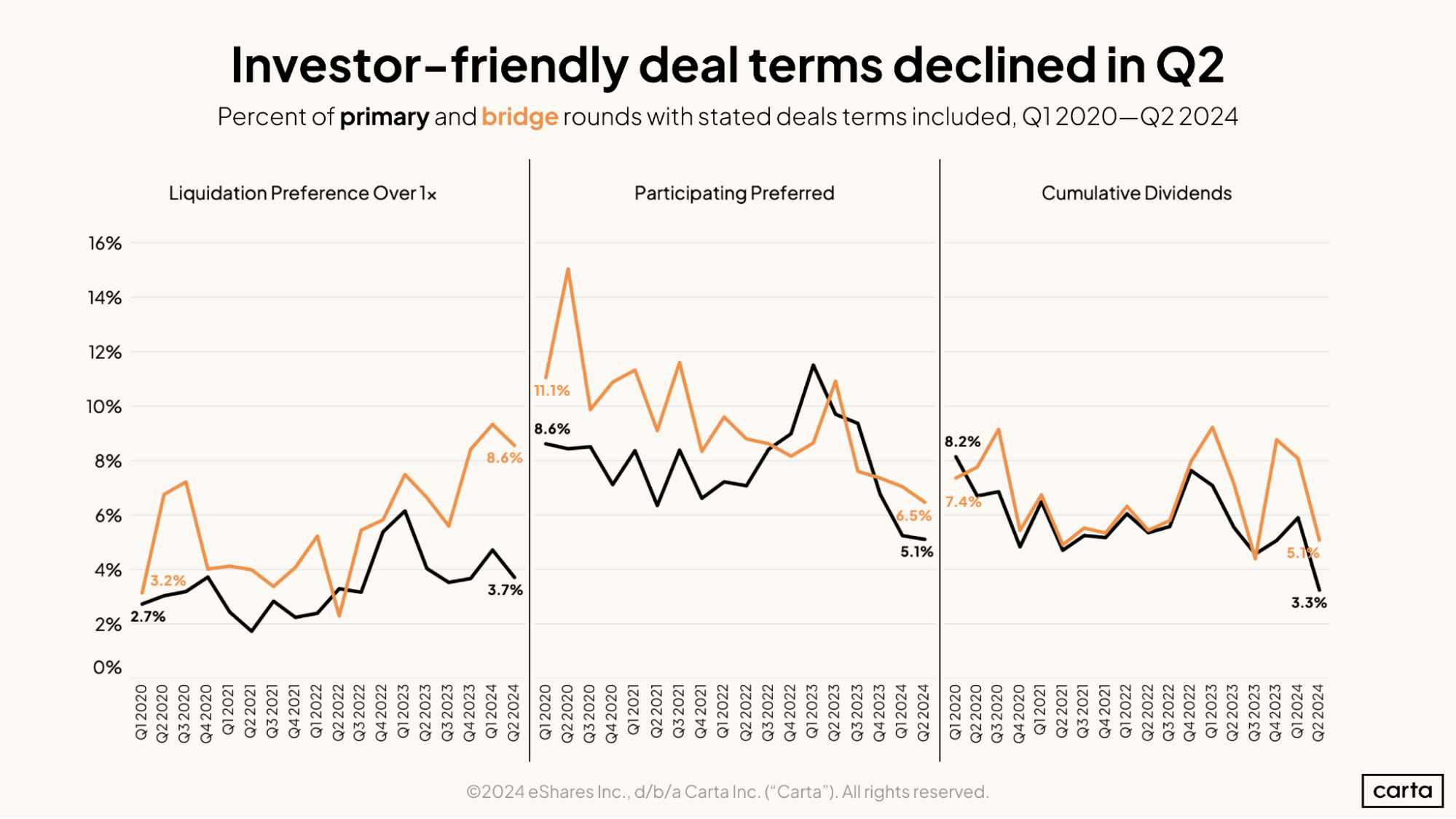

Fewer VC deals included investor-friendly terms in Q2. Participating preferred stock and cumulative dividends have both become less common in primary rounds since 2020, reaching new lows this quarter. During an interim period in 2021 and 2022 these deal terms became more common, but since 2023 the trend away from structured deal terms continued.

Trend lines for liquidation preference multipliers over 1x tell a different story. Their frequency has increased from 2.7% in Q1 2020 to 3.7% this quarter, though this is still down from a peak of 6.0% in Q1 2023. Overall, the decline in all three of the mentioned deal terms in Q2 indicates a move toward a more founder-friendly fundraising environment.

Fundraising & valuations

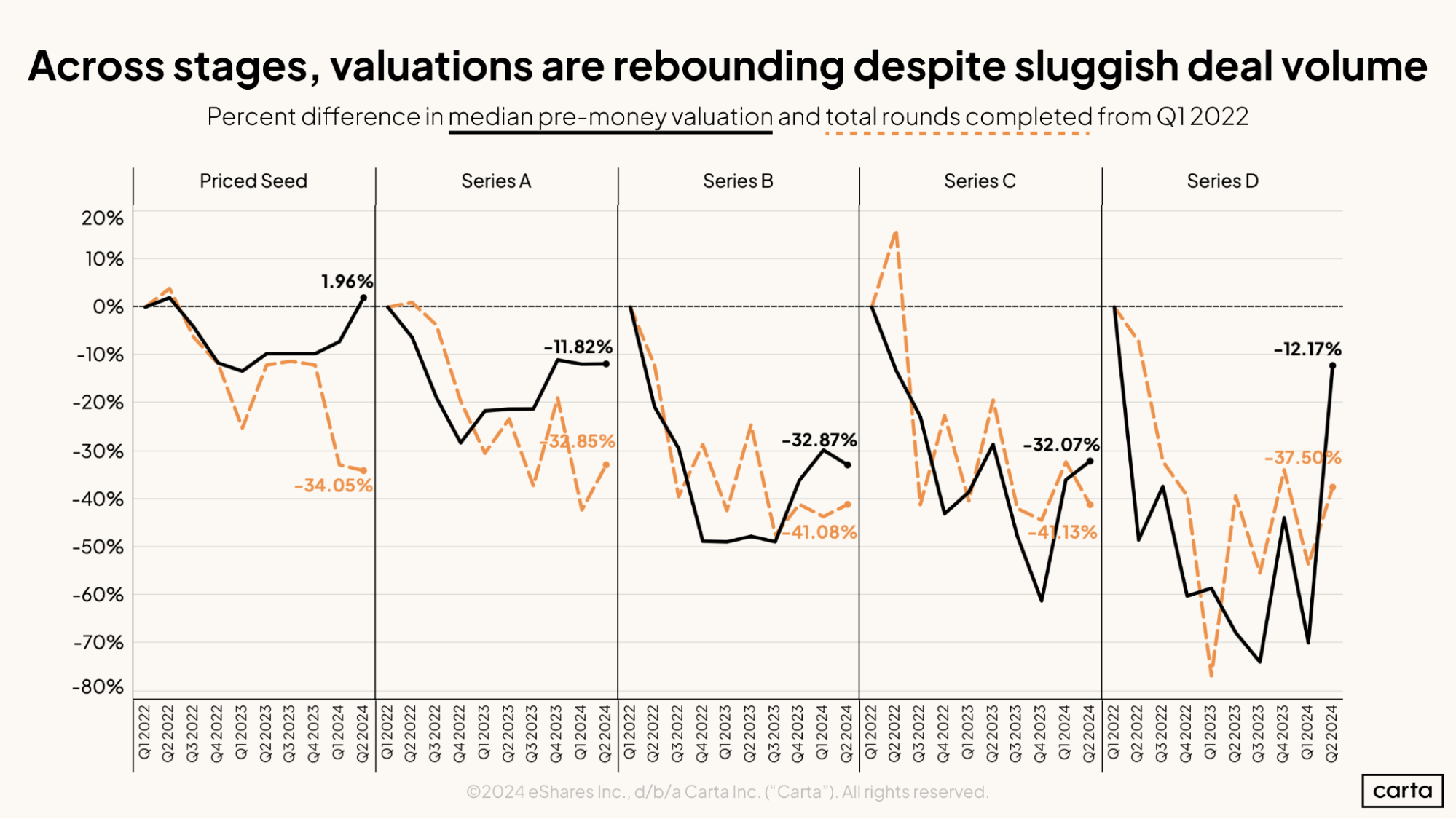

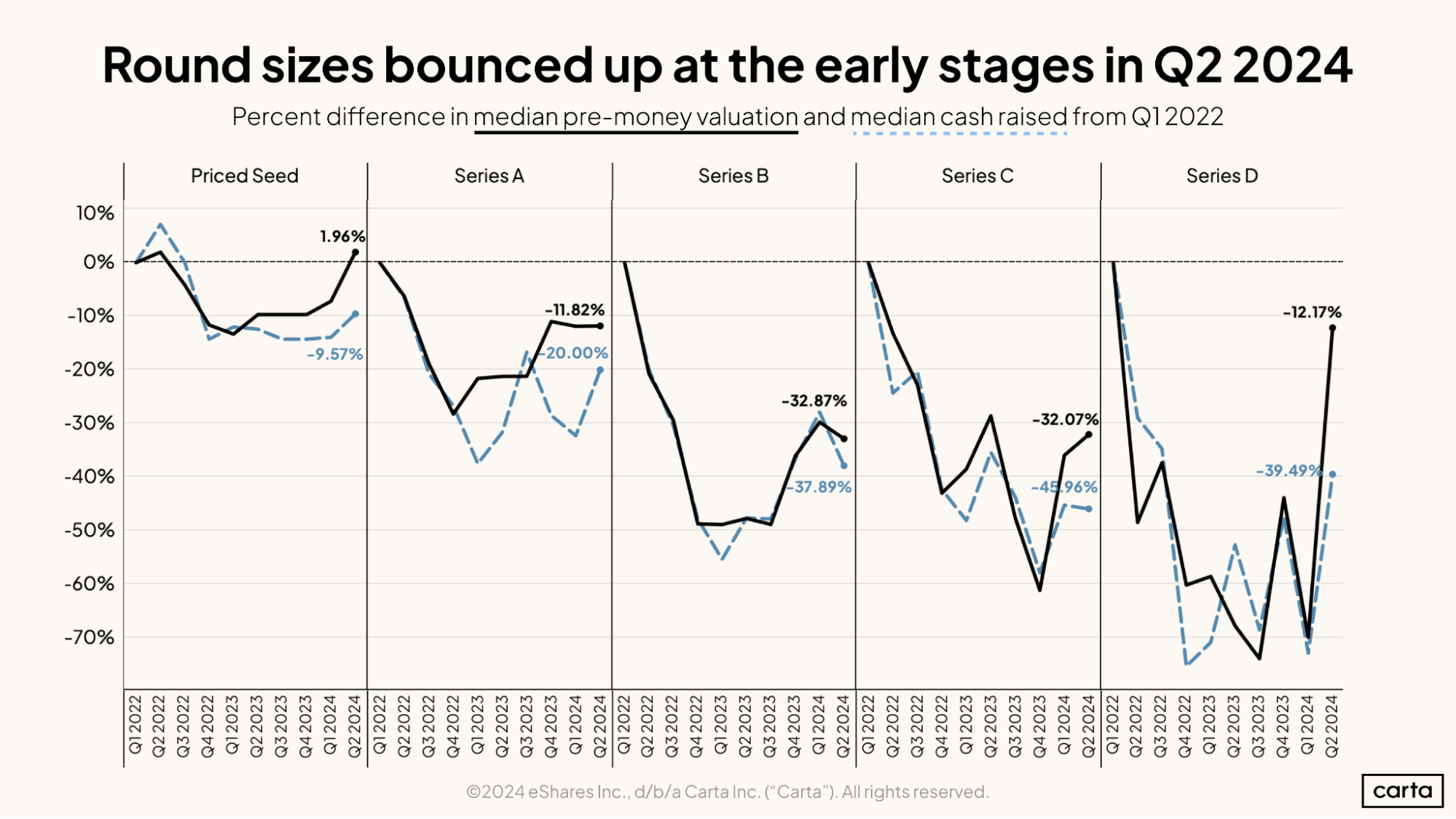

Since Q1 2022, median pre-money valuations have fallen less dramatically than total deal volume, especially at the seed and Series A stages. In Q2 2024, seed valuations finally surpassed Q1 2022 levels, rising by 1.96%. At post-seed stages, valuations are mostly moving upwards as well, though they have yet to reach Q1 2022 levels.

Deal volume at the seed stage has fallen 34.05% since Q1 2022. Considering the increase in median valuations, this suggests that seed investors are completing fewer but larger rounds. Deal count declines since 2022 have more closely tracked valuation declines at the Series C and D stages.

Across stages, percent changes in median valuation and median round size have tended to move together. As with deal volume, round sizes have not been as resilient as valuations. The median cash raised at the seed stages is still down 9.57% from Q1 2022 to Q2 2024, even though seed valuations are now up 1.96% over the same time period.

From seed to Series C, later stages have had larger decreases in both median valuation and median cash raised. As of Q2, however, Series D has defied this trend. The decline in both metrics is less severe for Series D than for Series C deals. Series D valuations are only 12.17% down from their Q1 2022 levels, while Series C valuations are down 32.07%.

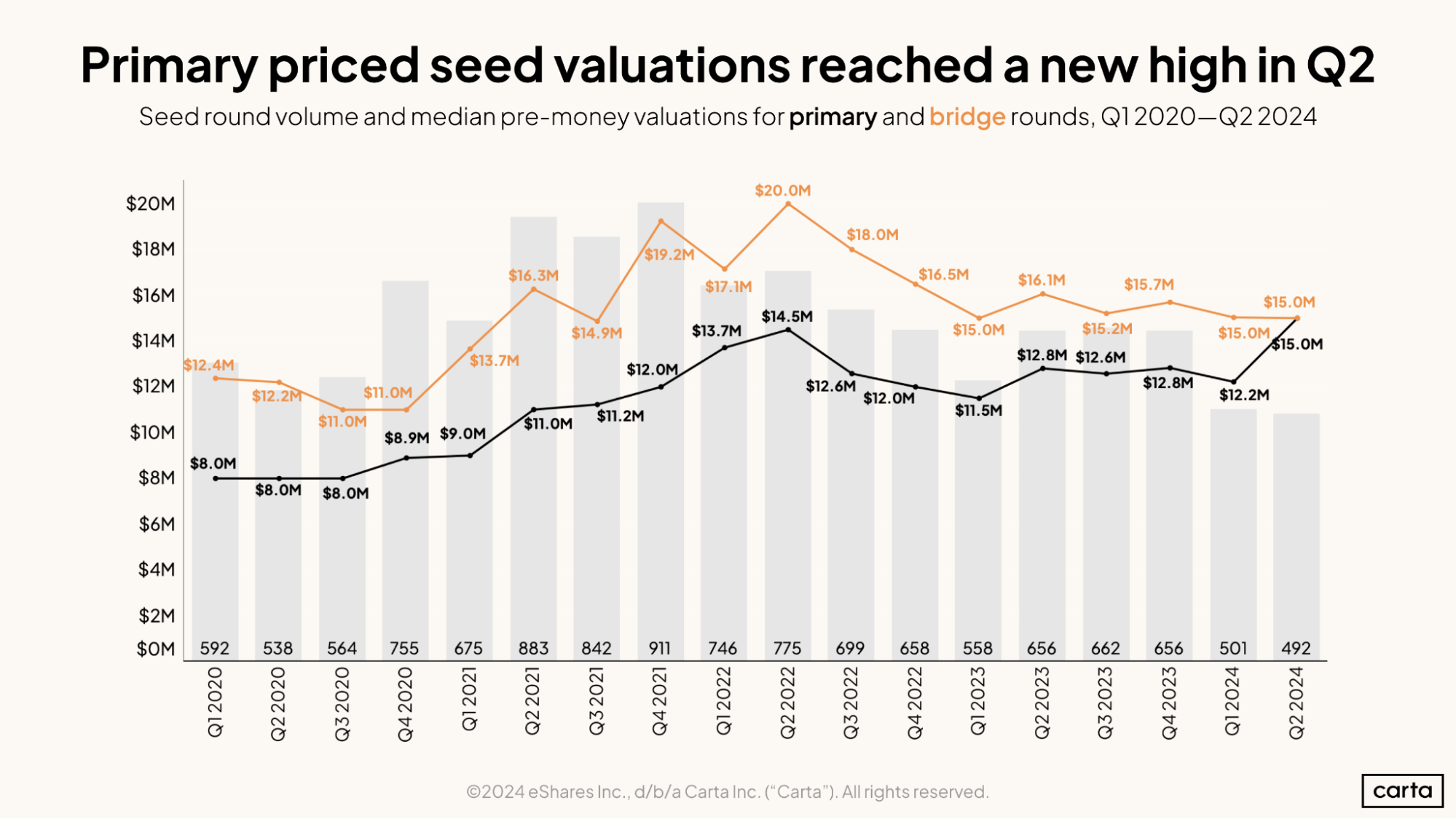

The median valuation for primary seed rounds reached a new high of $15.0M in Q2, up from $8.0M just a few years ago in Q1 2020. The volume of seed rounds has decreased slightly over the same time period.

Bridge valuations for seed rounds have historically been higher than primary valuations, but the two converged at $15.0 million in Q2. Over the past two years, while primary seed valuations have increased, bridge seed valuations have decreased from a high of $20.0 million in Q2 2022.

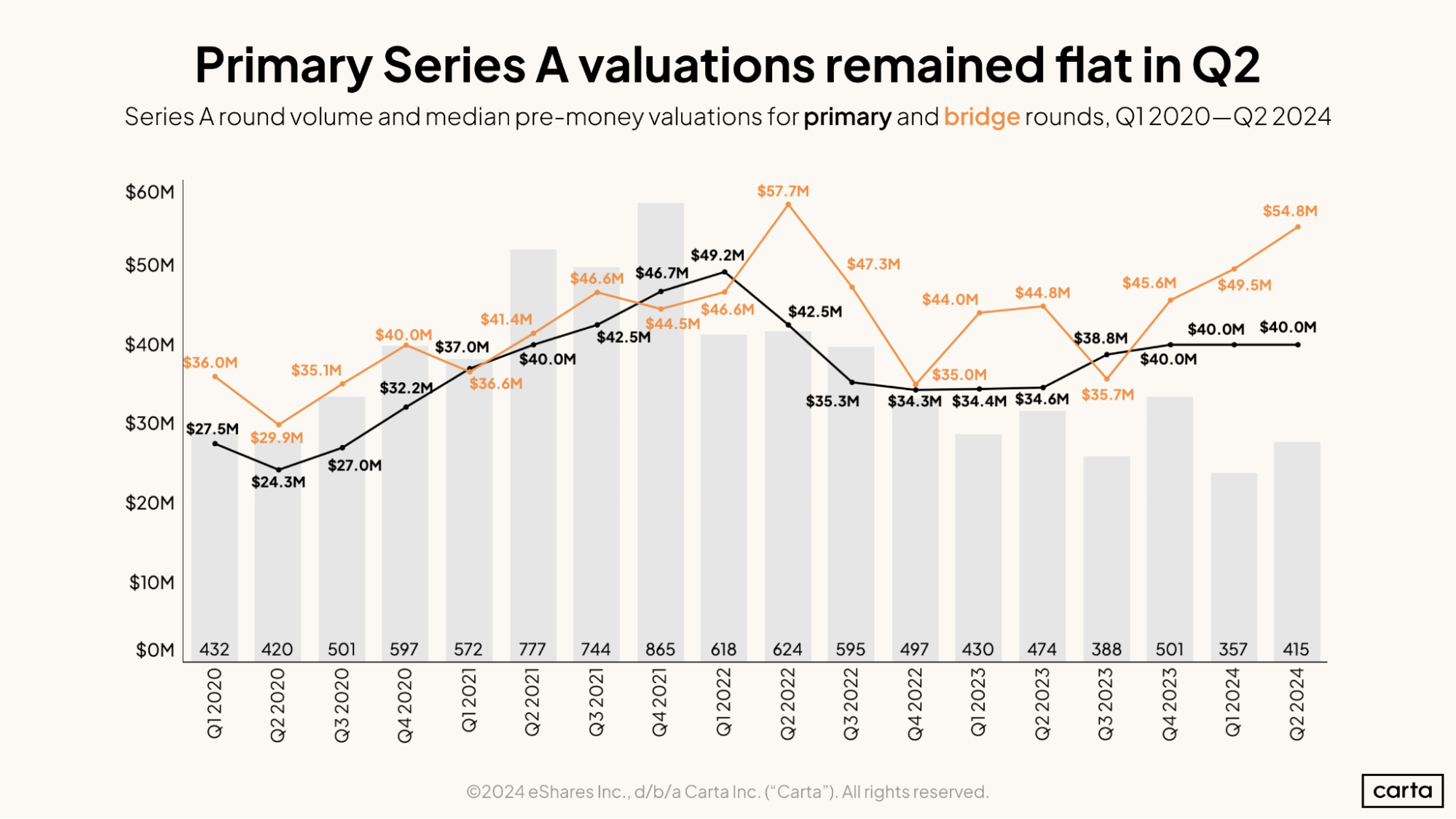

At Series A, median primary valuations have held steady at $40.0 million for the past three quarters. The median Series A bridge valuation, however, has continued to climb. It reached $54.8 million in Q2, a year-on-year increase of 22%. The number of Series A investments increased in Q2, but still sits at its third-lowest value since Q1 2020.

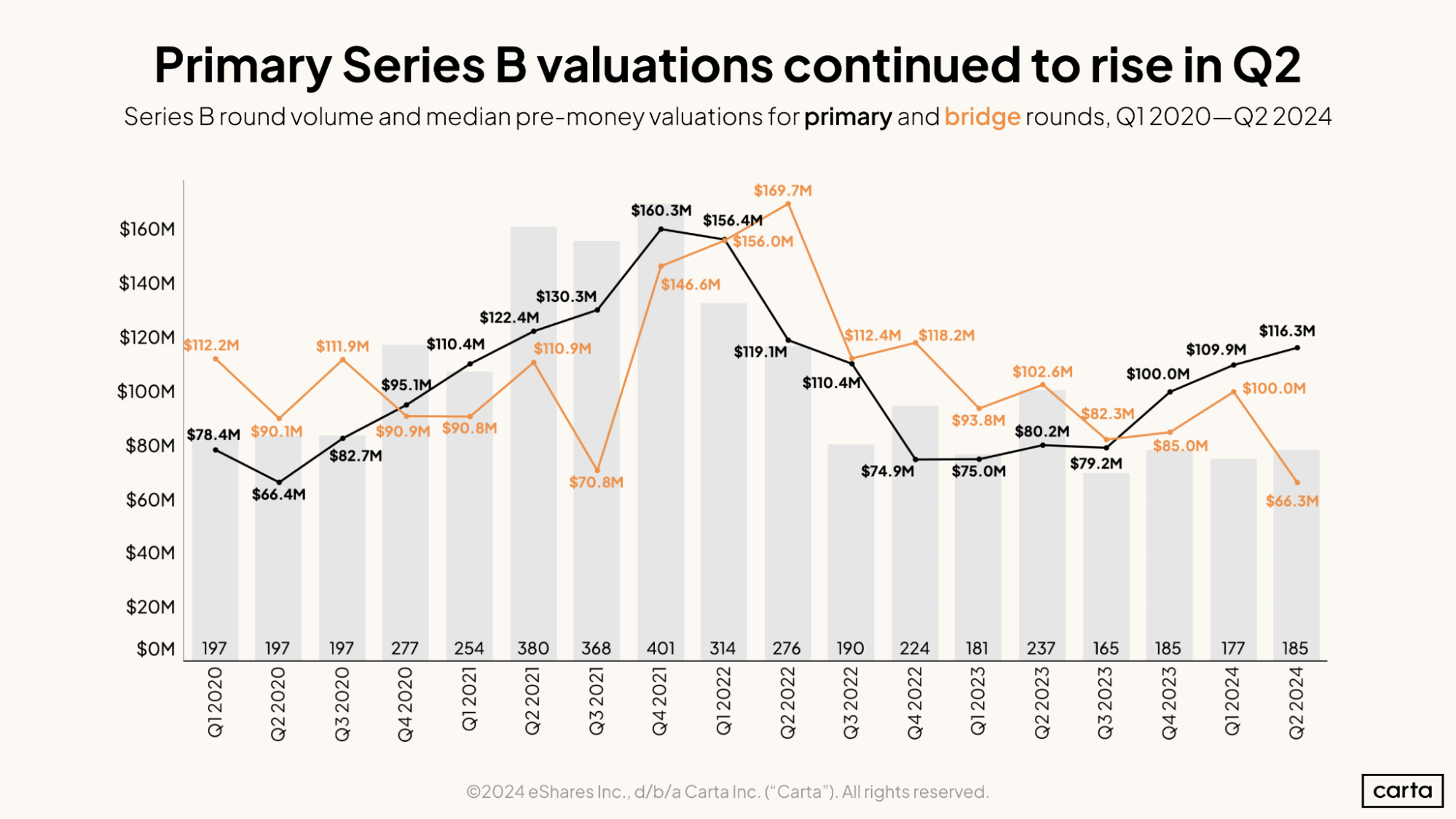

Primary Series B valuations rose for the third consecutive quarter, reaching a median of $116.3 million. For bridge rounds, however, median Series B valuations dropped 34% from Q1 to Q2. The median bridge Series B valuation of $66.3 million is the lowest value so far in this decade. Series B deal volume recovered to Q4 2023 levels after dipping slightly in Q1.

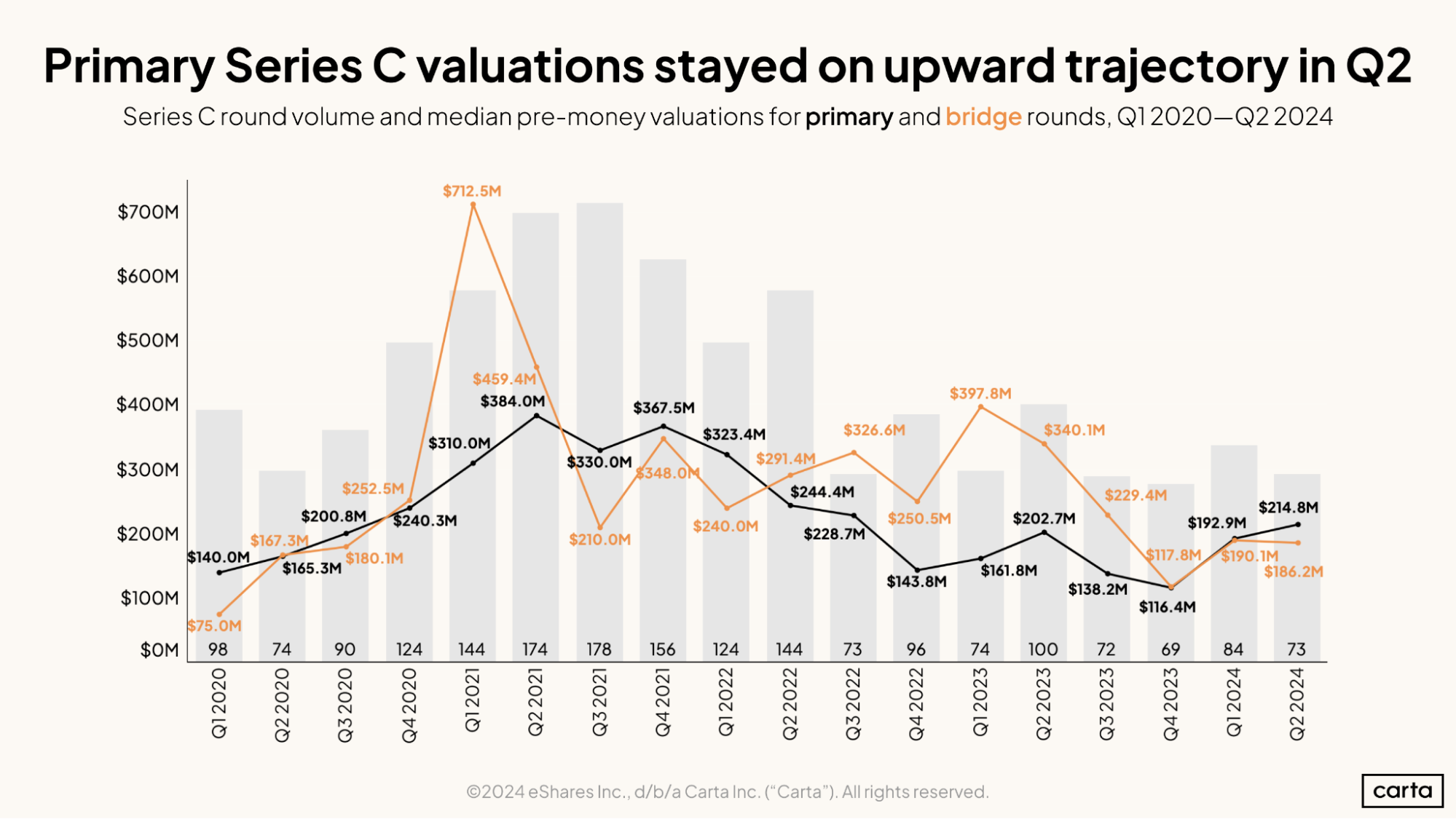

Primary Series C valuations continued on a notable upward trajectory for the second quarter in a row, after previously reaching a low in Q4 2023. The median primary Series C valuation nearly doubled from $116.4 million in Q4 2023 to $214.8 million in Q2. Bridge Series C valuations, however, declined this quarter, as did Series C volume.

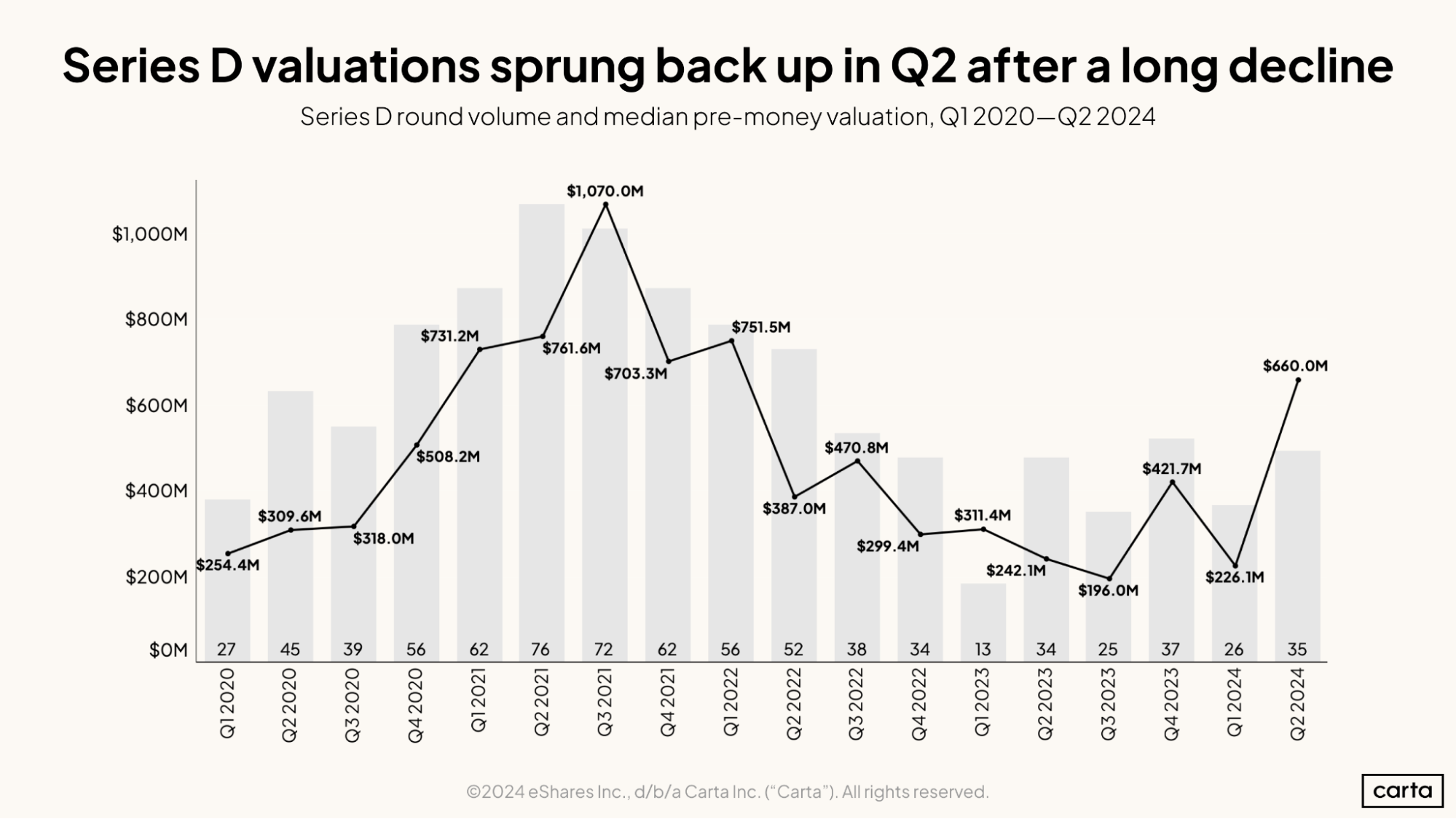

Series D had a strong quarter. The median Series D valuation rebounded by almost 200% since last quarter to $660.0 million, the highest figure of the past nine quarters. Series D deal count also fared well in Q2, increasing by 35%.

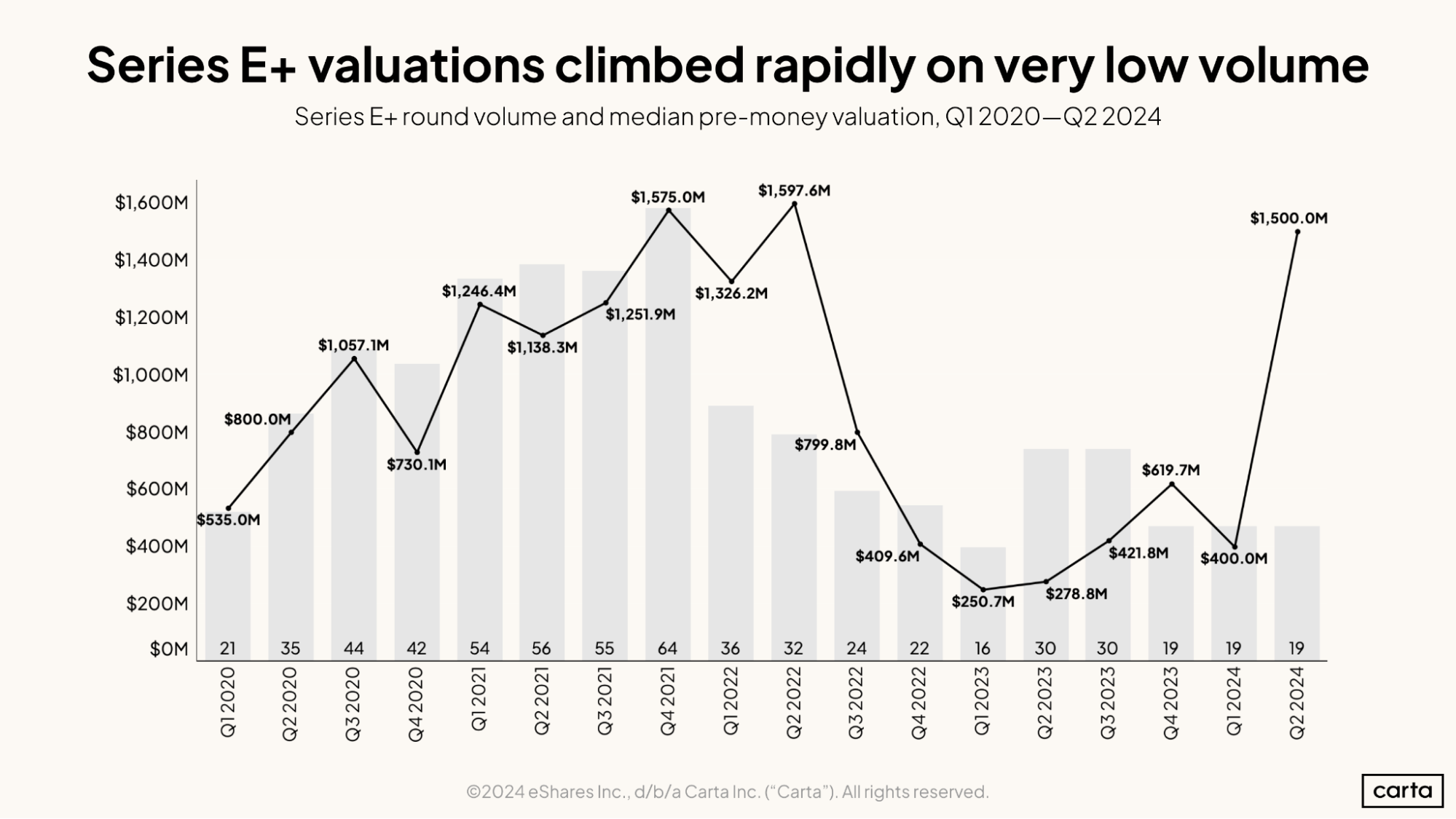

The number of Series E+ deals on Carta has remained steady for the past three quarters at 19, a relatively small sample. As a result,a few mega-deals in Q2 may be driving the surge in median valuation. The median Series E+ valuation was $1.5 billion, a staggering 275% increase from last quarter. Q2’s median valuation was the third highest this decade, nearly tying the Q2 2022 high of $1.6 billion.

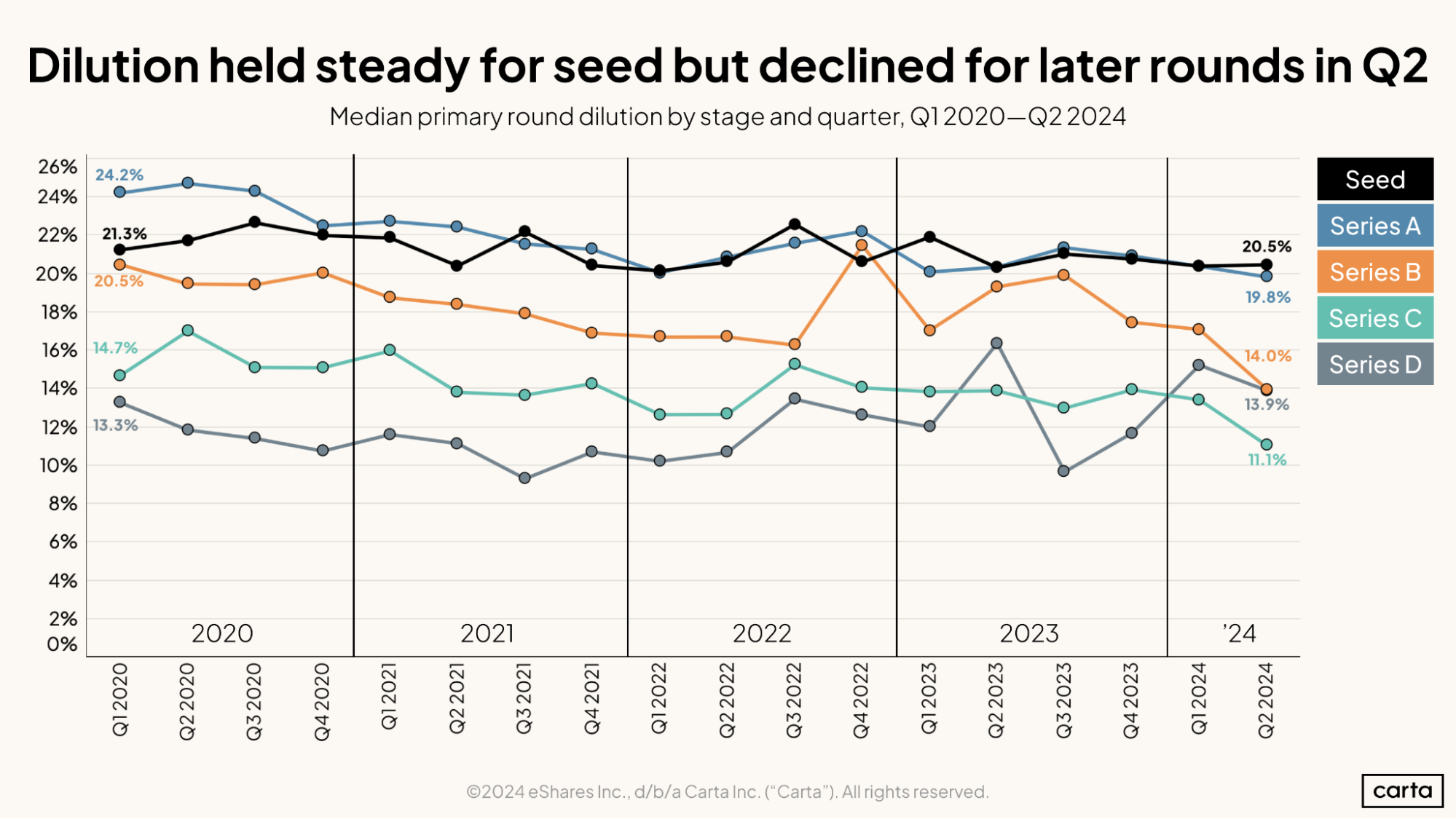

In Q2, median dilution in primary venture rounds remained level at the seed stage but declined for later rounds. The drop was slight for Series A, but relatively larger for the Series B, C, and D stages. For example, at Series B, median dilution fell from 17.1% in Q1 to 14.0% in Q2.

Looking at the bigger picture, founders are holding on to more of their companies for longer than they used to. Compared to 2020, dilution has declined at all stages from seed to Series C, but has slightly increased at Series D. The rise of Series D dilution suggests that these later-stage deals are operating under more investor-friendly conditions.

Following a similar pattern as dilution, the frequency of bridge rounds remained constant at the seed stage but dropped for later funding stages. Series B and C both saw their lowest levels of bridge rounds since 2022. Bridge rounds fell particularly sharply at the Series B stage, from 38% in Q1 to just 23% in Q2.

Bridge rounds have yet to decline at the seed stage. They still comprise 41% of all priced seed rounds, the highest level since the start of 2022. However, Q2 could be a turning point in terms of halting the upward trajectory of bridge rounds since the 2022 downturn.

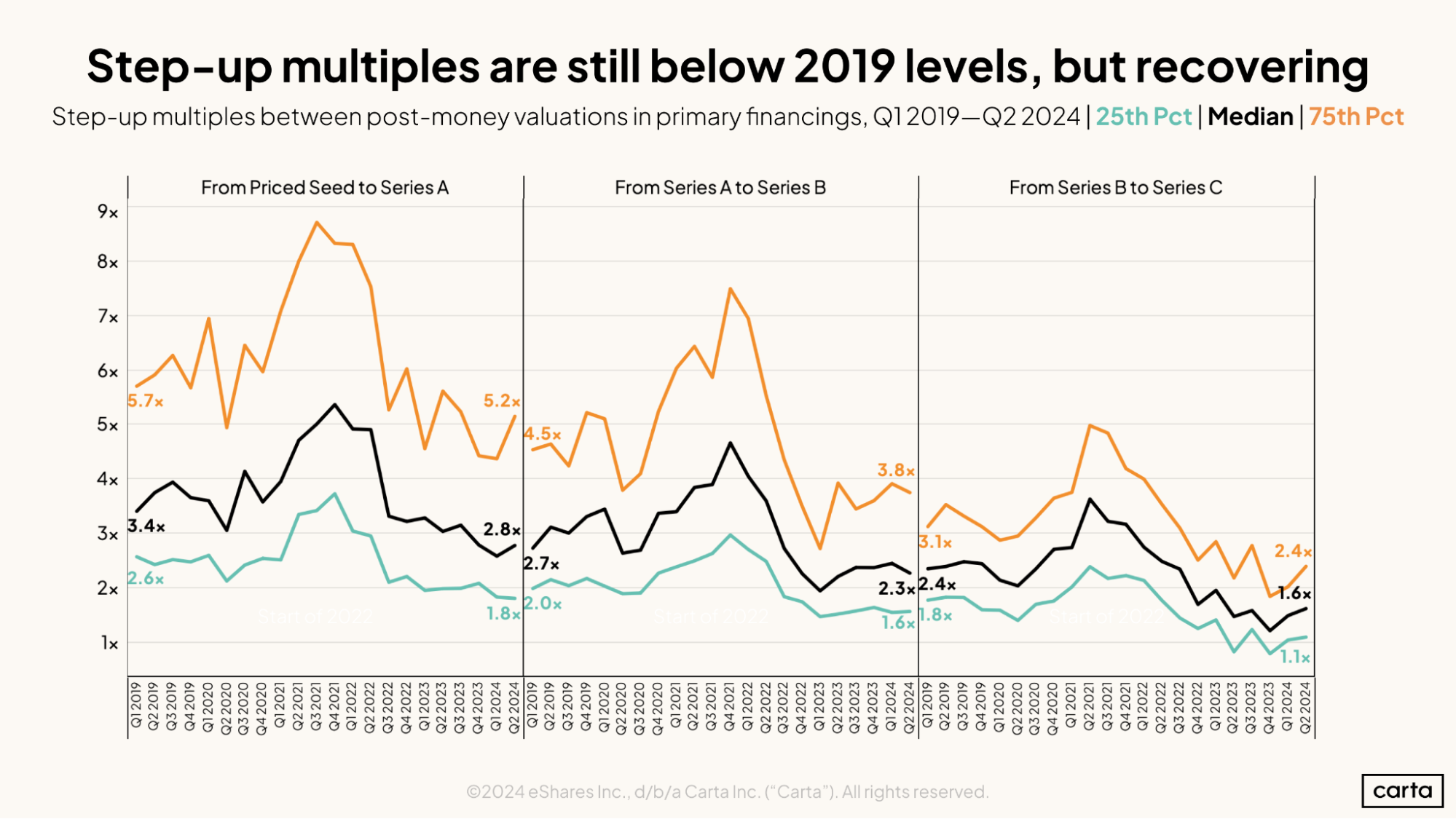

Step-up multiples are calculated by dividing a company’s valuation at one stage by its valuation at the previous stage. The higher the multiple, the more a company’s value rose between the two rounds.

Since 2019, step-up multiples have declined for companies at the Series A, B, and C stages, despite a spike in 2020 and 2021. In Q2, the median step-up multiple for a company that raised a Series A round was 2.8x, down from 3.4x in Q1 2019. This quarter fared slightly better than Q1 2024, which had the lowest median Series A step-up multiple of the past five years.

Median Series B step-up multiples decreased slightly in Q2, but are still up from their lowest point of 2.0x in Q1 2023. Median Series C step-up multiples increased for another consecutive quarter to 1.6x. This is up from the low point of just 1.2x in Q4 2023, which indicates that startups completing Series C deals then were raising nearly flat rounds.

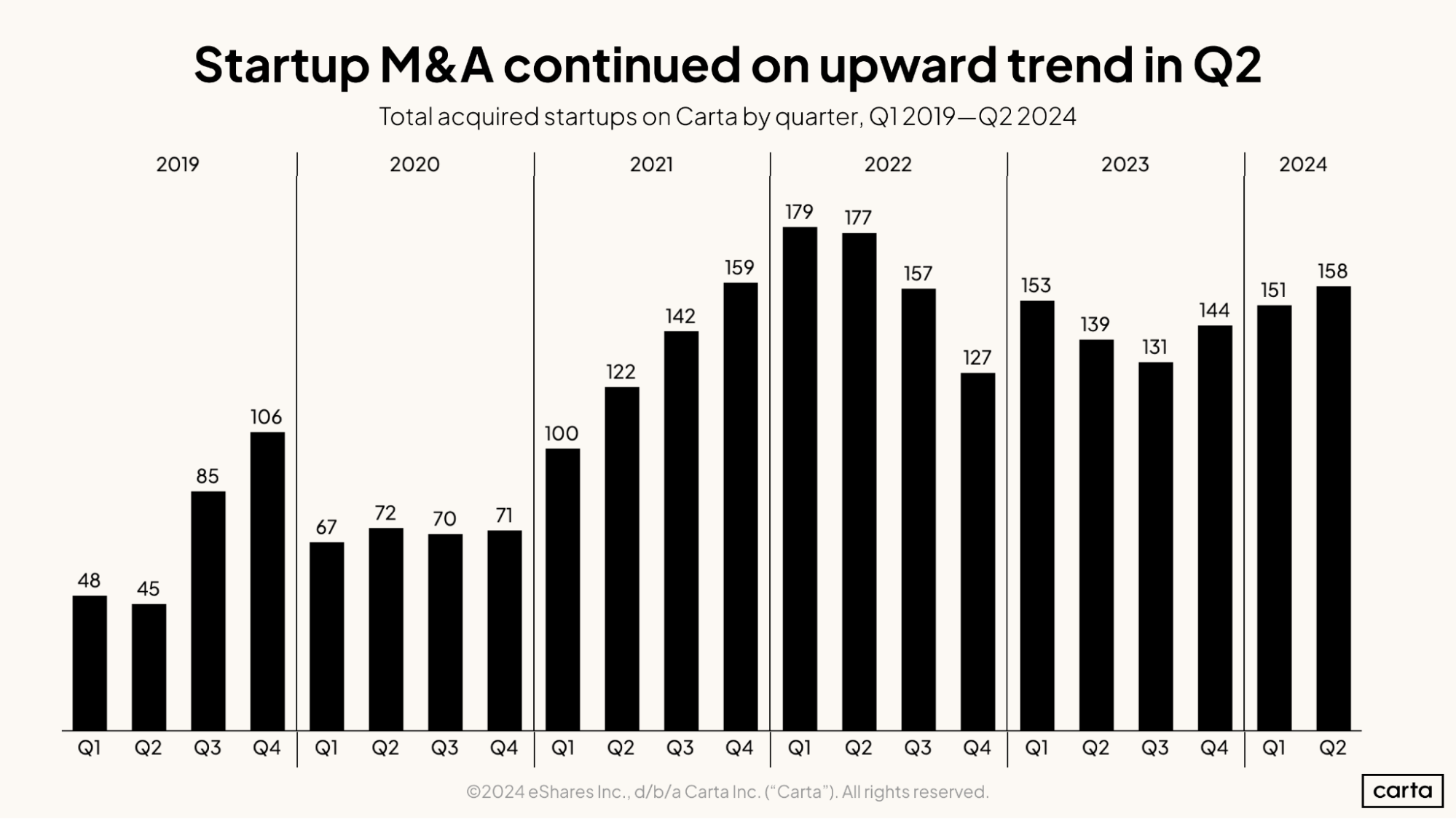

Q2 2024’s count of 158 M&A transactions on Carta represents the highest volume since Q1 2023 as well as the third consecutive quarter of upward movement. Compared to a year ago, M&A activity has increased 14%.

Geographical trends

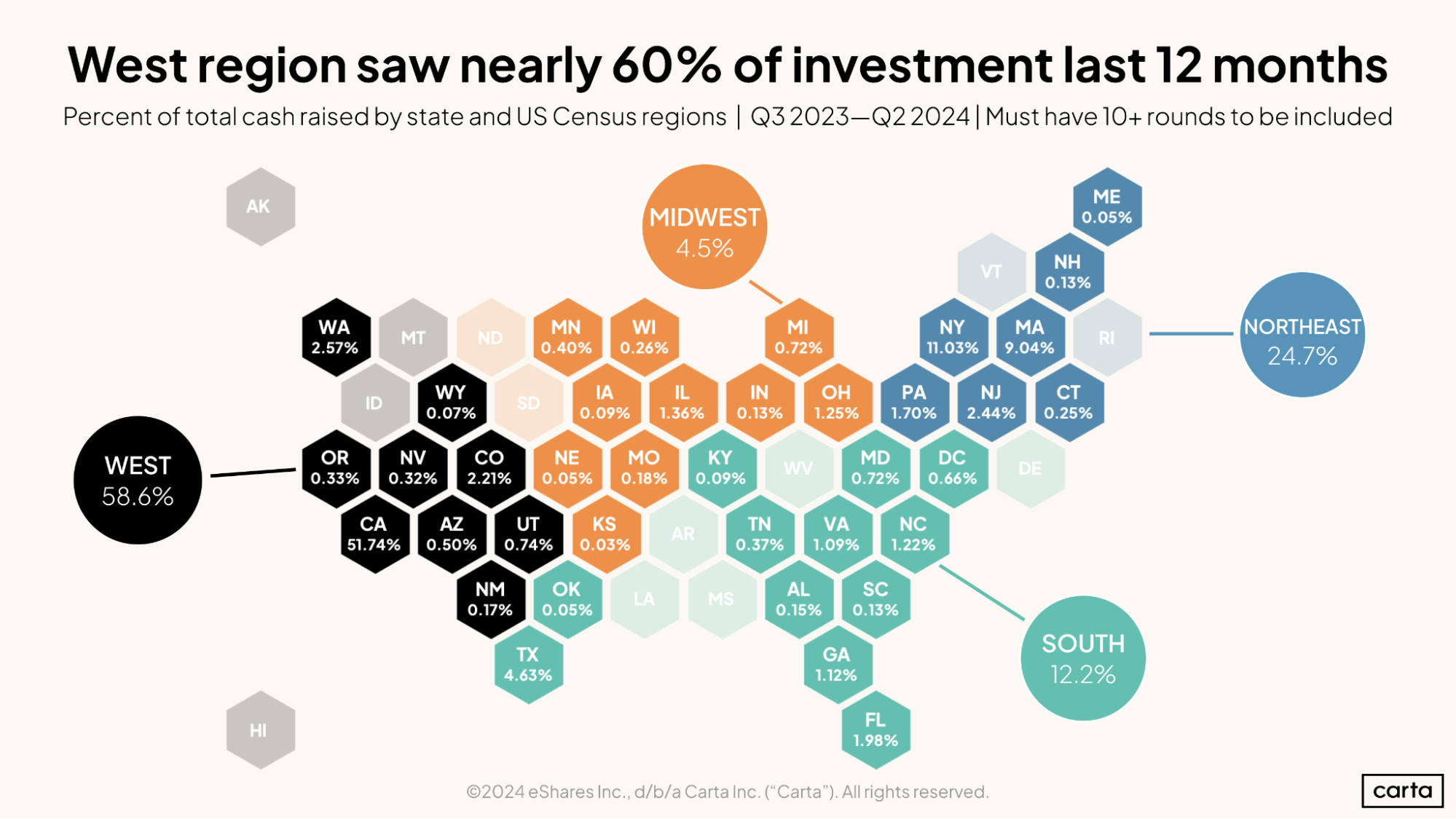

The West has had a strong past 12 months, accounting for nearly 60% of all capital raised by startups on Carta between Q3 2023 and Q2 2024. California alone accounts for an outright majority with 51.74% of VC raised in that time period.

After California, New York took in 11.03% of capital raised, followed by Massachusetts with 9.04% and Texas with 4.63%. No other state attracted more than 3% over the past year.

In Q2, the West lost some of the share of venture capital that it had reclaimed from the other census regions in Q1, though it is still by far the leader of the four regions. Startups based in the West raised 59% of capital invested on Carta total in Q2, as opposed to 63% in Q1.

On the other hand, the Northeast region increased its share from 20% in Q1 to 25% in Q2, reversing its three-quarter-long decline. The South’s proportion of VC raised held steady at 13% from last quarter, while the Midwest fell to just 3%.

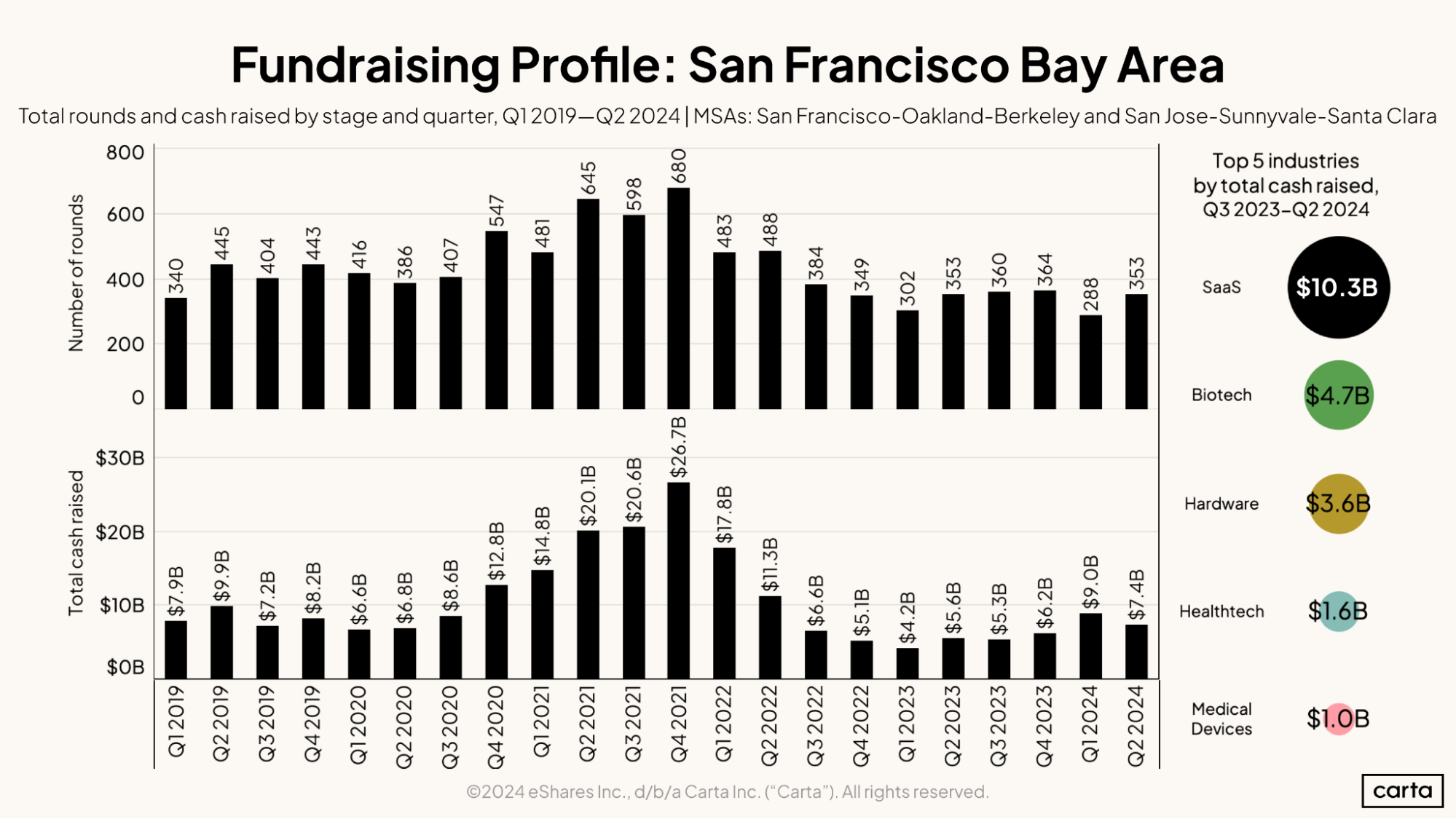

The San Francisco Bay Area brought in a total of $7.4B in venture capital investment across 353 rounds in Q2. While this deal count is higher than last quarter, the amount of cash invested decreased slightly. Both metrics are still well below their Q4 2021 peaks: -48% for deal count and -72% for cash raised.

Looking at top industries, SaaS startups received the most cash in the Bay Area over the past year. Three other health-related industry segments—biotech, healthtech, and medical devices—all made it into the top five out of 13 categories.

The New York Metro Area had a mixed quarter. While it brought in a recent high of $3.6B in VC cash, the number of rounds that took place in Q2 was the lowest in the past five years. In the New York Metro Area, SaaS, fintech, and healthtech received similar levels of funding over the past year and comprise the top three industries.

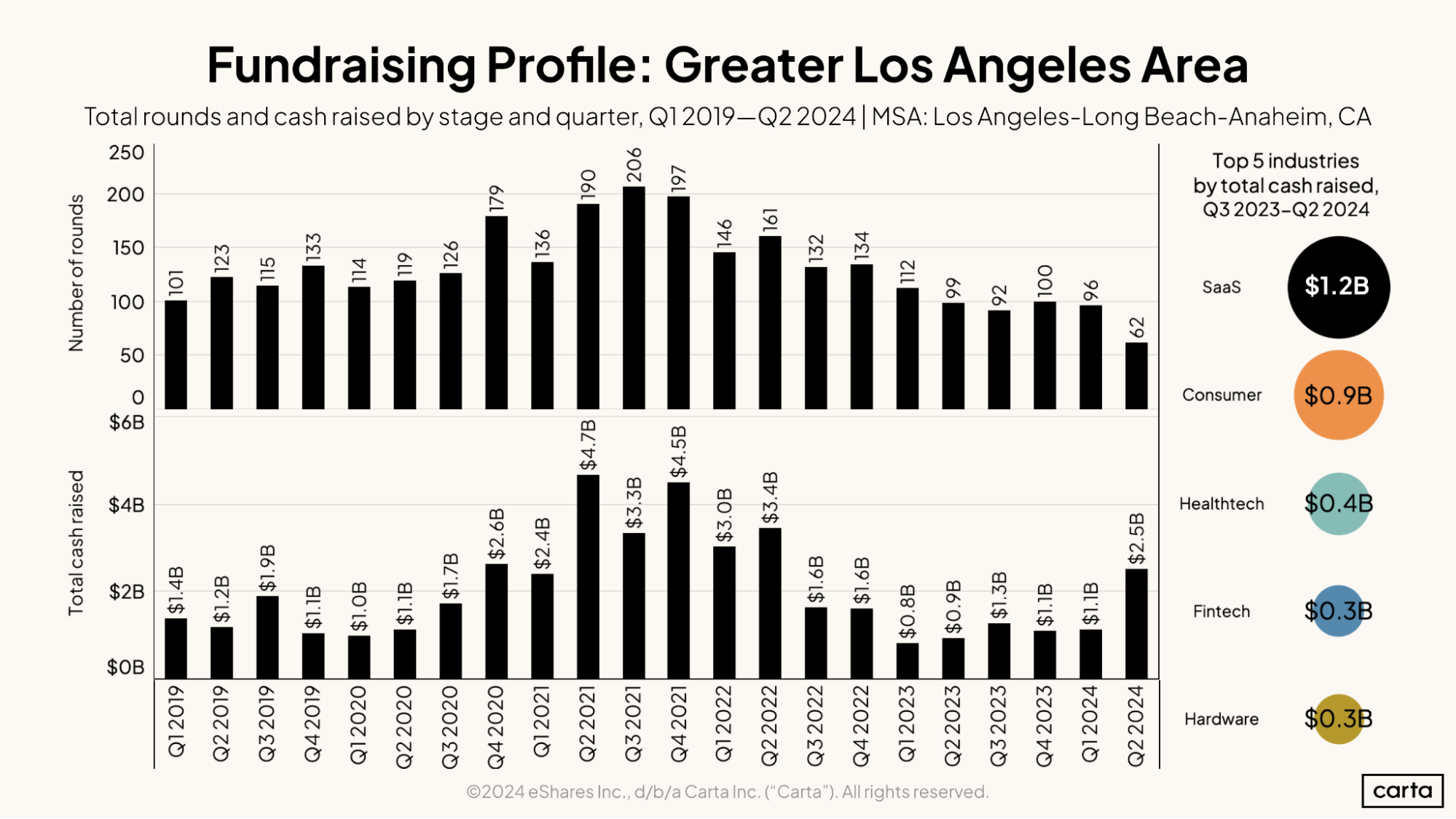

Startups in the Greater Los Angeles Area received a total of $2.5B across 62 deals in Q2. As with New York, Q2’s deal count is a record low for the past five years, but the amount of capital invested is the highest since Q2 2022. Beyond SaaS, Los Angeles is notable for its strong concentration of startups focusing on consumer products and services, which received $0.9B in the past year.

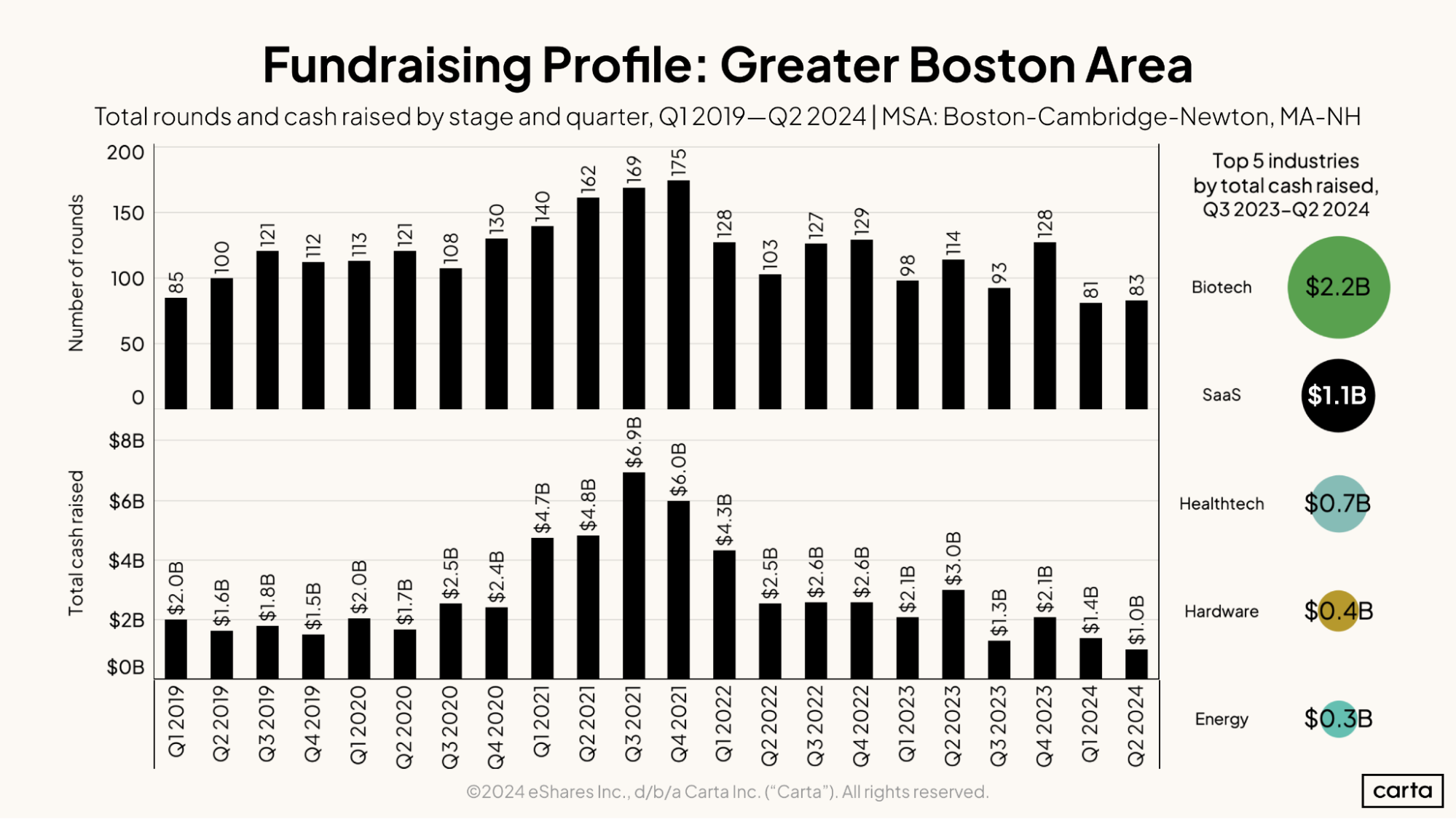

In Q2, the Greater Boston Area brought in $1.0B in venture capital, the lowest recorded by Carta in the past five years. Similarly, Boston’s Q2 deal count of 83 represents the second-lowest over the same time period. These figures suggest that Boston faces a difficult fundraising environment. In terms of industries, biotech is the largest beneficiary of venture capital in the Boston area, receiving $2.2B over the past twelve months. SaaS, healthtech, hardware, and energy also make the top five.

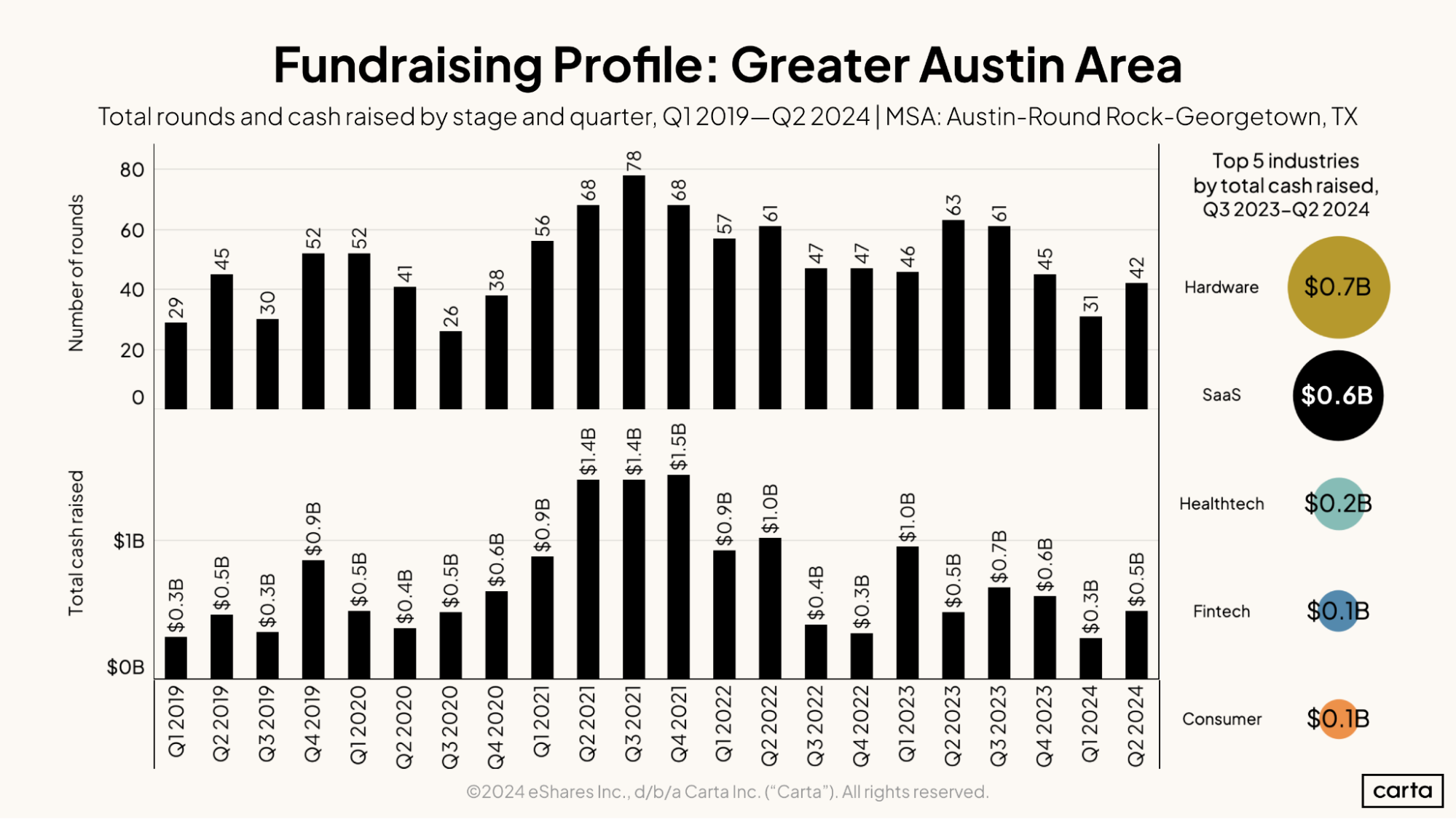

Companies in the Greater Austin Area raised $0.5B in Q2 across 42 deals. Both deal count and total cash raised are up from Q1, but still down from Q4 2023. Greater Austin has a smaller ecosystem than the other metros highlighted in this report, but it is the largest in the South. Hardware is the largest industry in Austin, receiving $0.7B in the past year.

Industry-specific data

Download the addendum to this quarter's report to get industry-specific data on fundraising and valuations:

Methodology

Carta helps more than 45,000 primarily venture-backed companies and 2,400,000 security holders manage over $3.0 trillion in equity. We share insights from this unmatched dataset about the private markets and venture ecosystem to help founders, employees, and investors make informed decisions and understand market conditions.

Overview

This study uses an aggregated and anonymized sample of Carta customer data. Companies that have contractually requested that we not use their data in anonymized and aggregated studies are not included in this analysis.

The data presented in this private markets report represents a snapshot as of July 29, 2024. Historical data may change in future studies because there is typically an administrative lag between the time a transaction took place and when it is recorded in Carta. In addition, new companies signing up for Carta’s services will increase historical data available for the report.

Financings

Financings include equity deals raised in USD by U.S.-based corporations. The financing “series” (e.g. Series A) is taken from the share class name in their applicable certificate or articles of incorporation. Financing rounds that don’t follow this standard are not included in any data shown by series but are included in data not shown by series. Primary rounds are defined as the first equity round within a series. Bridge rounds are defined as any round raised after the first round in a given series.

In some cases, convertible notes are raised and converted at various discounted prices within a series (e.g. Series A-1, Series A-2, Series A-3). In these cases, converted securities are not included in cash raised, and only the post-money valuation of the new money is included.

DISCLOSURE: This communication is on behalf of eShares Inc., d/b/a Carta Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. ©2024 eShares Inc., d/b/a Carta Inc. ("Carta"). All rights reserved. Reproduction prohibited.