Building a buzzy, successful, well-funded startup typically requires rapid growth. That’s why many founders have traditionally viewed a down round as something close to a disaster: If investors think your company is worth less today than it was during your previous funding round, it means that the preferred pathway of fast, steady growth has been disrupted.

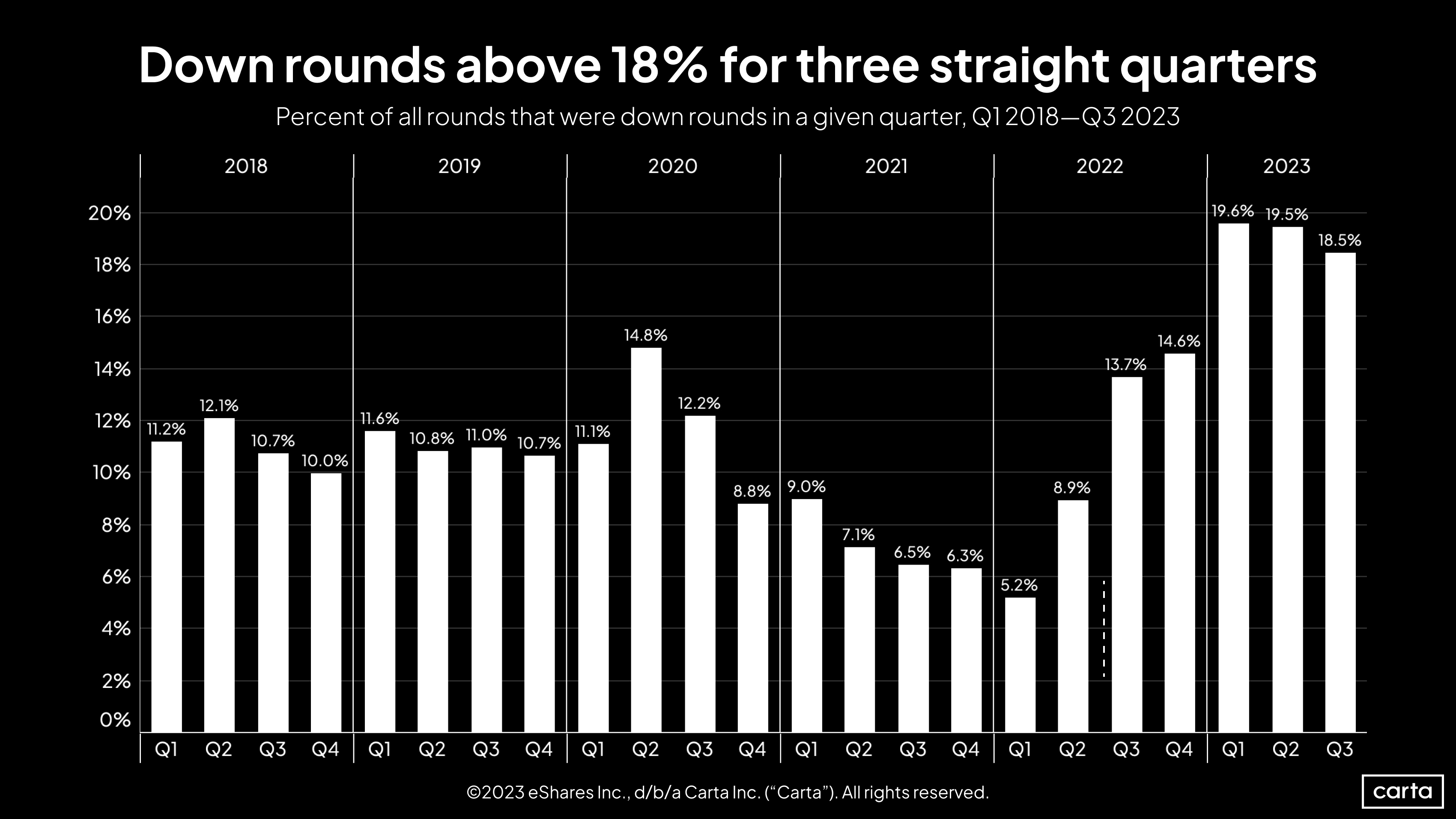

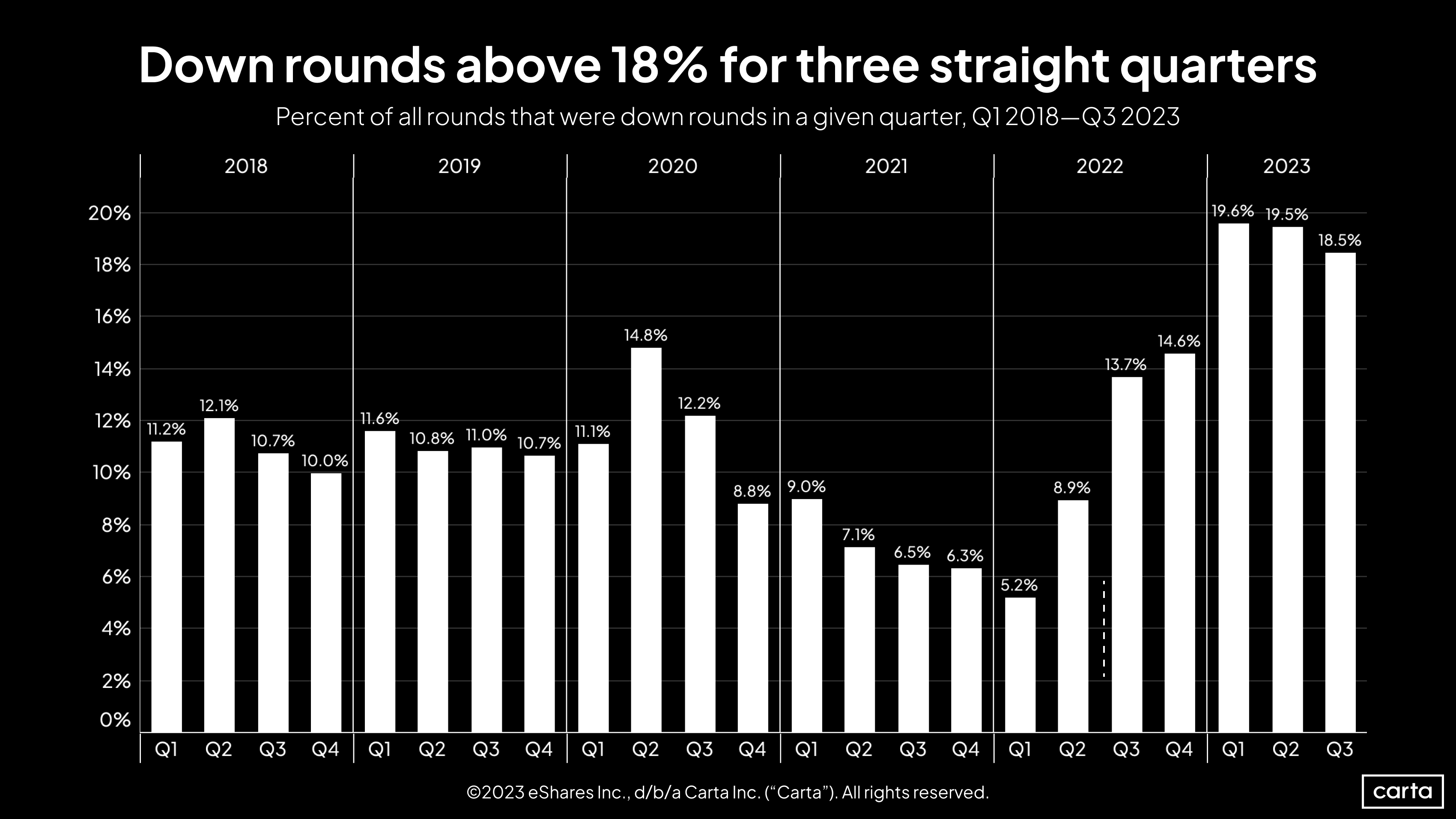

Lately, those disruptions have been stacking up. Down rounds have proliferated over the past several quarters. As recently as Q1 2022, just 5.2% of new fundings on Carta were down rounds. In Q3 2023, that figure was 18.5%, continuing a nine-month stretch in which nearly one out of every five rounds raised by startups resulted in a decreased valuation.

But investors like Julia Gudish Krieger, managing partner at early-stage firm Pari Passu Venture Partners, are not particularly concerned. The reason: Down rounds don’t happen in a vacuum. By definition, they are a comparison across time: How does a valuation today compare to a valuation from one or two years ago? And it’s clear to Krieger that the market has changed.

During most of the 2010s and early 2020s, the venture market was in an extended period of steady expansion that culminated in the record-breaking year of 2021. During that decade-plus, raising a down round had a different context than it does today, when the market is in the midst of a downturn. If the context for fundraising has changed, valuations can be expected to shift accordingly.

Krieger thinks most VCs understand the difference.

“One company that we’re investing in now is technically doing a down round, but it’s just because they raised at the height of these incredible valuations,” says Krieger, whose firm invests at the intersection of retail and tech. “It can be a real ego hit. But my advice is, just do a down round, as long as you’re showing that there are real fundamentals to the business. People know what’s going on. And if investors are spooked by the optics of a down round, then I think they’re out of touch with what’s happening in the venture world in general.”

Venture’s valuation reset

Over the past year and a half, startup valuations have declined at every stage of the venture lifecycle. Later stages have been harder hit. The median seed valuation on Carta got 5% smaller between Q1 2022 and Q3 2023, while the median Series D valuation fell by 50%.

These persistent declines have an impact beyond an increase in down rounds. They’re also causing VCs to rethink valuations in other ways.

VCs typically report back to their limited partners at least once per quarter on the current state of their portfolio investments. Drew Glover, a general partner at fintech firm Fiat Ventures, says that he’s seeing and hearing of more VCs choosing to mark down the value of some of their investments in their reports—that is, to lower a company’s valuation for internal accounting purposes, even if that lower valuation hasn’t been reflected in a primary funding round.

Just because a company isn’t raising new capital doesn’t make it immune from new market realities. Promptly accounting for those new realities can be beneficial in multiple ways. Markdowns can give LPs a more accurate picture of the true state of the portfolio, and that transparency can help improve LP-GP relationships. They can also help VCs decide where best to focus their time and attention. In most cases, a firm’s internal valuation policy will help decide how and when markdowns occur.

“For a really smart, thoughtful VC, it’s not going to take the company actually doing a down round to mark down a couple investments in their fund,” Glover says. “We all know that the majority of VCs are power-law investors. They’re investing for multibillion-dollar exits. And it just so happens that the probability of all those companies succeeding is very low. So being proactive about markdowns is very helpful.”

At some point, the market for startup valuations of all kinds will find some sort of stability. For now, founders are still feeling the side effects of a downturn.

“I think valuations are still being reset from prior bubbles,” Krieger says. “In my perspective, great companies will always get funded—it just might be at a different valuation.”

Get the latest data

For weekly insights into Carta's unparalleled data on the private markets, sign up for Carta’s Data Minute weekly newsletter:

DISCLOSURE: This communication is on behalf of eShares Inc., d/b/a Carta Inc. (“Carta”). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. ©2023 eShares Inc., d/b/a Carta Inc. (“Carta”). All rights reserved. Reproduction prohibited.