In the big picture, the venture capital industry is experiencing a slowdown. But investors agree that plenty of promising startups are still out there—startups showing the potential to transform industries and, eventually, produce enormous returns.

Amid VCs, the battle to back this crop of intriguing young companies is heating up.

Sach Chitnis is co-founder and partner at Jump Capital, an early-stage firm that’s been investing in tech startups for more than a decade. He says that, in the present climate, most investors agree on what makes an attractive startup target—things like early revenue streams, a focus on efficiency, and a clear strategy for solving real-world problems, rather than other metrics like rapid growth and customer acquisition.

And in many cases, investors are willing to pay a premium to add these attractive companies to their portfolio.

“The good deals are very obvious right now. Every good deal that we’ve seen has had at least four or five term sheets,” Chitnis says. “You’re seeing some deals priced at 2021 levels in terms of valuation.”

An early-stage shift

When investors find themselves paying sky-high valuations and battling for access to deals, it’s natural that they will look for some way to invest more efficiently. In the hunt for value, Jump Capital has shifted its attention earlier in the venture lifecycle. And Chitnis expects many of the firm’s competitors to follow suit.

For much of its history, Jump has focused on Series A and Series B investments. Lately, the firm has shifted that window to Series A and seed. For Chitnis, the logic is clear: When the attractive deals are obvious, investors are more confident in identifying winners at early stages. And as investors put capital to work at earlier stages and lower valuations, the potential grows for immense returns.

“Everybody is going to shift earlier,” Chitnis says. “Everybody seeking out those opportunities to deploy capital at lower-valuation entry points.”

Late-stage funding dries up

A shift in investor preference toward earlier stages will have knock-on effects for the rest of the startup ecosystem. In fact, it already has.

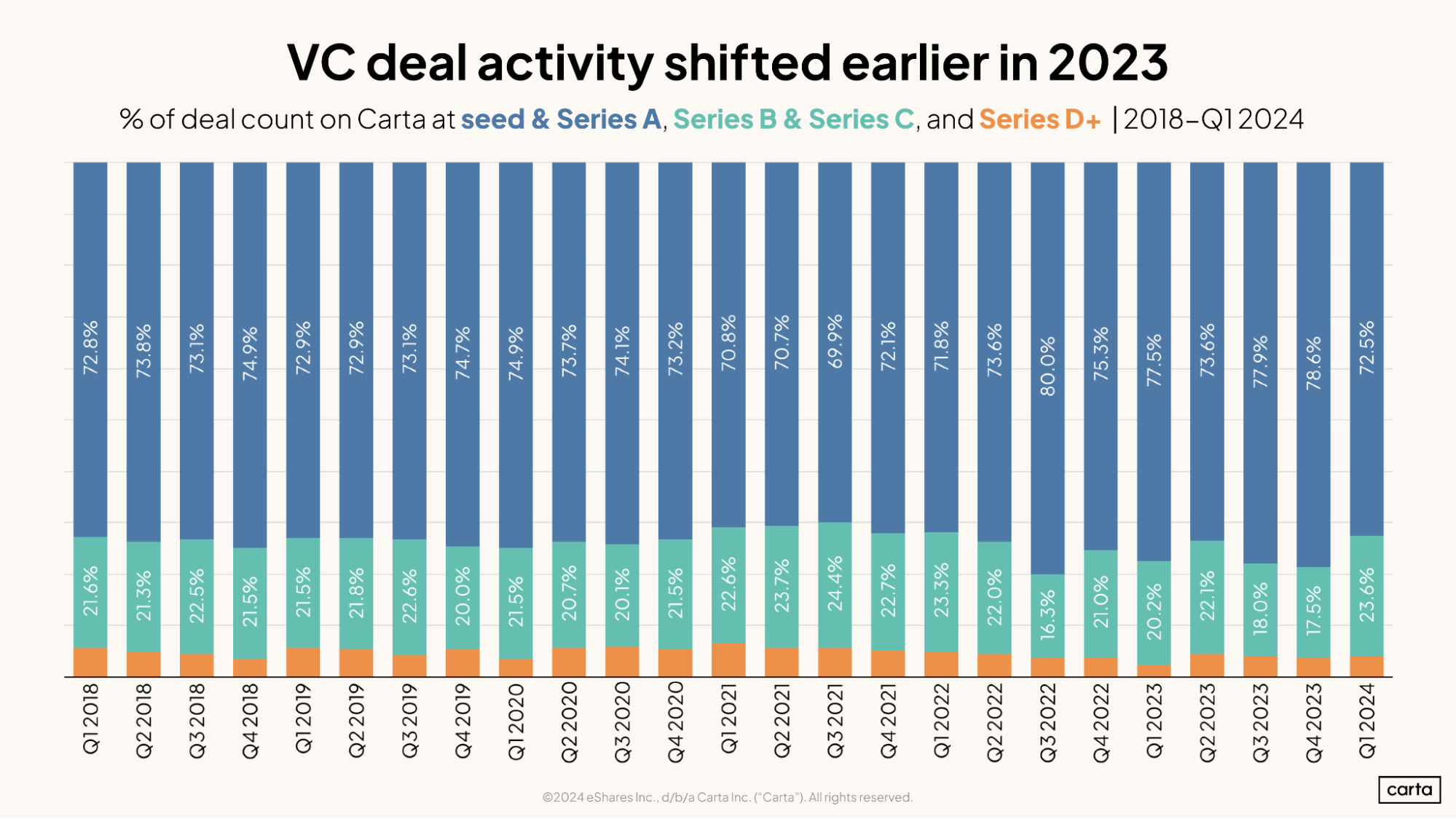

From the start of 2018 through the midway point of 2022, seed and Series A deals combined to account for less than 75% of all venture fundings on Carta in every quarter. Then, as the market began to turn, early-stage deals became more prevalent. Starting in Q3 2022, seed and Series A deals surpassed 75% of all fundings in five of the next six quarters.

Seed and Series A deals made up a slightly smaller percentage of all activity in Q1 2024. Overall, however, venture activity has shifted earlier in the past two years. As investors pivot to younger startups, companies at later stages are finding fewer potential backers for new primary rounds of their own.

“Series B, C, D, E, F—all those letters are non-existent, or there’s an extraordinarily high bar,” Chitnis says.

Venture funds that invest at middle and late stages typically raise larger funds and write larger checks than funds that focus on seed deals. As these bigger funds move earlier in the venture cycle, they bring that increased scale with them. In many cases, this is driving up round sizes—and making it more difficult for smaller funds to access premium deals.

“A lot of Series B, C, D, E, and F investors are moving a click earlier, and they have substantial funds. Their anchor point on entry point and their anchor point on check size is higher,” Chitnis says. “So you’re seeing Series As raising $20 million, when they typically would be raising $10 million or $15 million. And you’re seeing Series As with $2 million or $3 million in ARR, when in prior years, that’s probably closer to $1 million.”

Get the latest data

Sign up for the Carta Data Minute newsletter to receive the latest data on VC financings, valuations, compensation, and more:

DISCLOSURE: This communication is on behalf of eShares Inc., d/b/a Carta Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. ©2024 eShares, Inc. dba Carta, Inc. ("Carta"). All rights reserved. Reproduction prohibited.