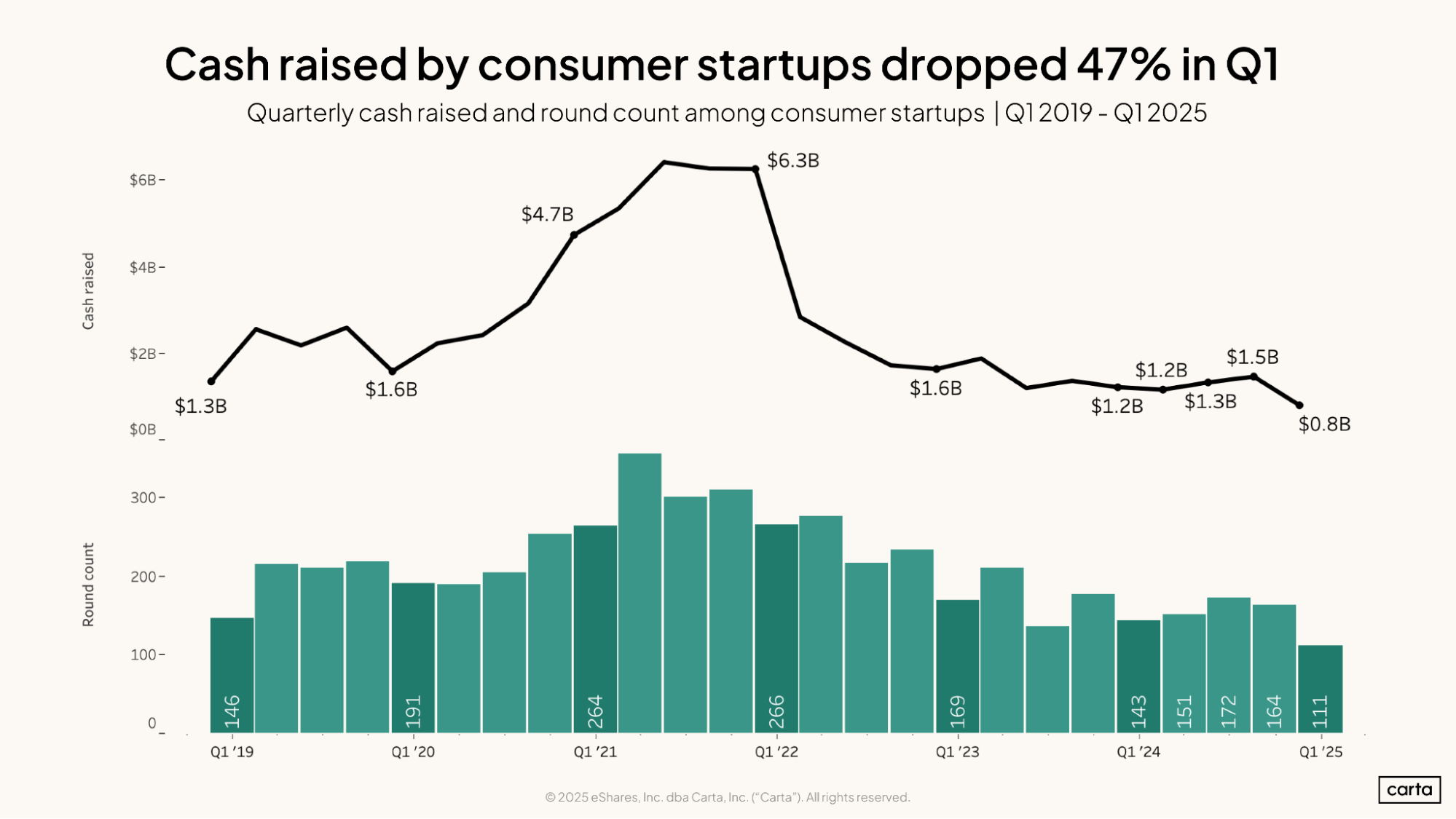

In the consumer sector, the first quarter of 2025 was the slowest stretch for venture fundraising in recent memory.

Consumer startups on Carta combined to raise just shy of $800 million across 111 funding rounds across all stages between the start of January and the end of March. Both of those were the lowest quarterly totals in their respective categories dating back to at least the start of 2019.

And Q2 did not begin with cause for optimism. On April 2, the U.S. announced plans to implement wide-reaching new tariffs on most of its key trading partners, creating major question marks in an industry where many companies have built business models that are reliant on a system of relatively low-friction international trade.

“Consumer startups, especially those with physical goods or cross-border supply chains, are acutely exposed to tariff-related uncertainty,” says Rachel Springate, a founding general partner at Muse Capital, an early-stage firm that primarily backs consumer-tech startups.

For the time being, though, Springate says that most of the companies in her firm’s orbit are insulated from any serious tariff-related impact. They’re not feeling concrete effects; instead, they’re adjusting their plans to reduce future tariff-related risks.

“The early-stage companies we back typically aren’t importing at large volumes yet, so the financial impact today is limited,” Springate says. “What we are seeing is founders proactively adjusting for longer-term volatility: diversifying suppliers, considering North American manufacturing earlier, and baking pricing elasticity into their models.”

A consumer recalibration

As consumer startups and investors adjust to a new tariff environment, they’re also adapting to changes in consumer buying behavior.

Each year, a larger percentage of all retail spending happens online, and consumers lead more of their lives online. Apps like TikTok and Instagram have emerged as key drivers of buying decisions. Springate believes that consumers today are more likely than ever to find recommendations from online influencers, niche communities, or other sources they find more authentic.

At WealthMore, a consumer finance startup providing wealth advisory services, founder and CEO Mical Jeanlys-White said her team has found surprising success on YouTube, where they publish podcasts and other consumer-focused videos.

“The way consumers buy has changed dramatically,” Jeanlys-White says. “It’s important not to just look at your particular industry for inspiration, but look holistically around. How are buying patterns changing? Where are people going for validation about a product?”

Of course, technology is driving change in the consumer space in other ways, too. Consumer tech startups today are seeking ways to incorporate AI into the next killer product, and other types of consumer startups are experimenting with ways that AI might streamline their own operations.

As an investor in the field, Springate says that the recent slowdown in deal activity was apparent. She also doesn’t expect it to continue.

“Investors are being more selective and focusing on unit economics, not just brand,” Springate says. “I suspect Q1 was quiet not from a lack of conviction, but from a pause to reassess go-to-market strategies in this new macro landscape.”

Q1 highlights

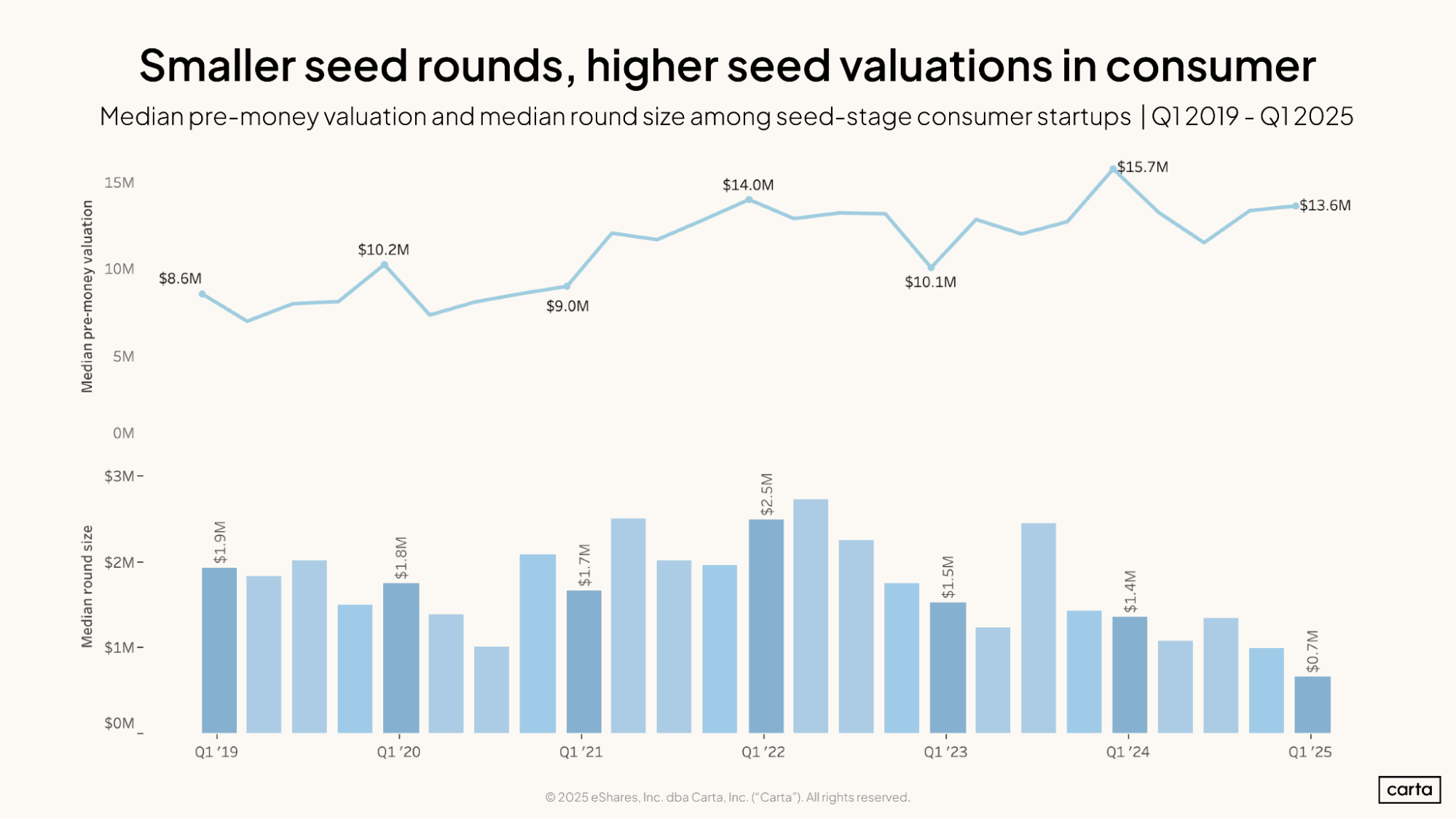

A slowdown at seed: The median seed round raised by consumer startups on Carta in Q1 fell to around $700,000, its lowest point in at least the past six years. The median consumer seed valuation, meanwhile, was $13.6 million in Q1, down 13% year over year.

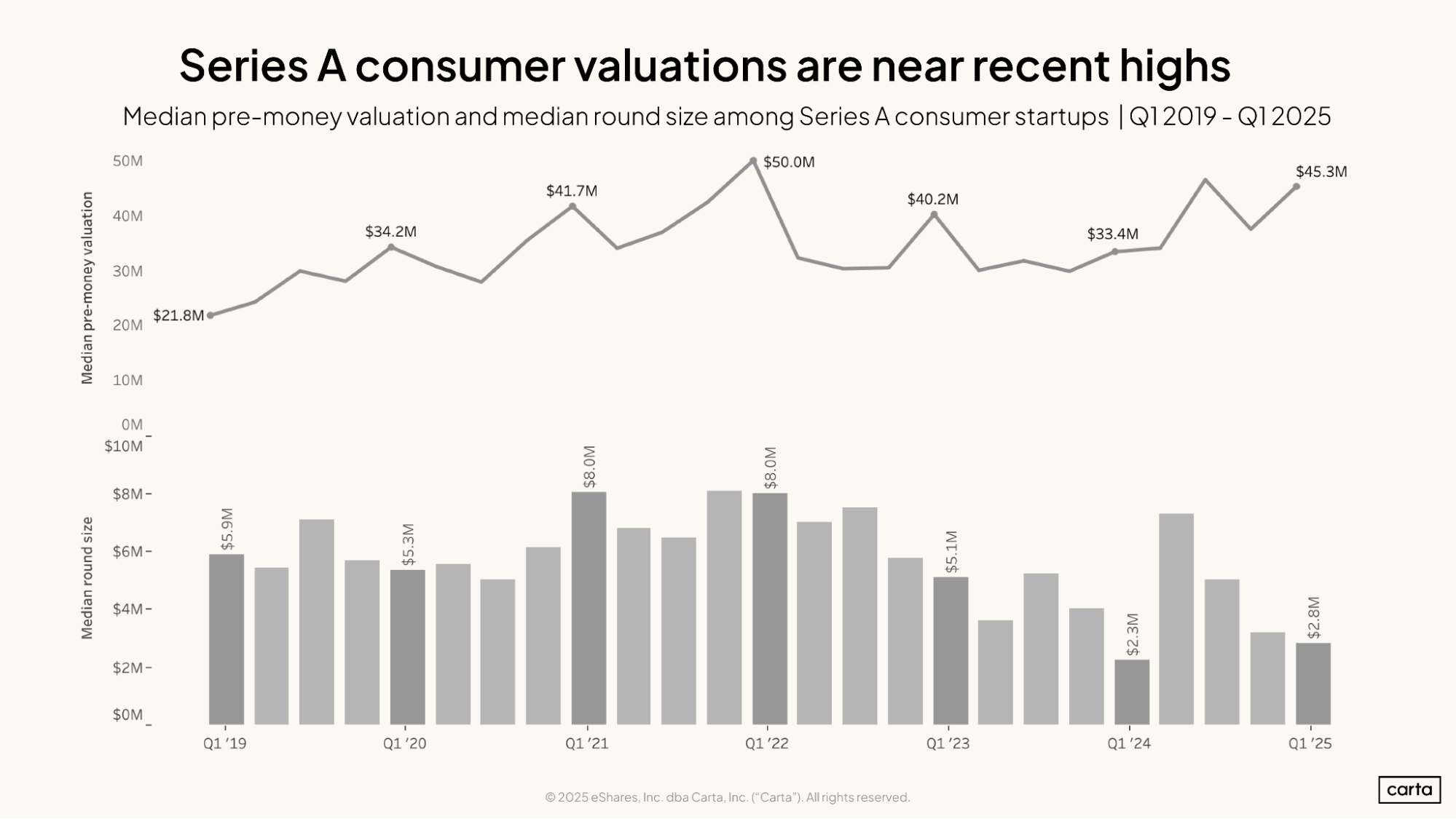

A spike at Series A: The consumer fundraising market was stronger at Series A. There, the median valuation rose to $45.3 million in Q1, up 36% year over year.

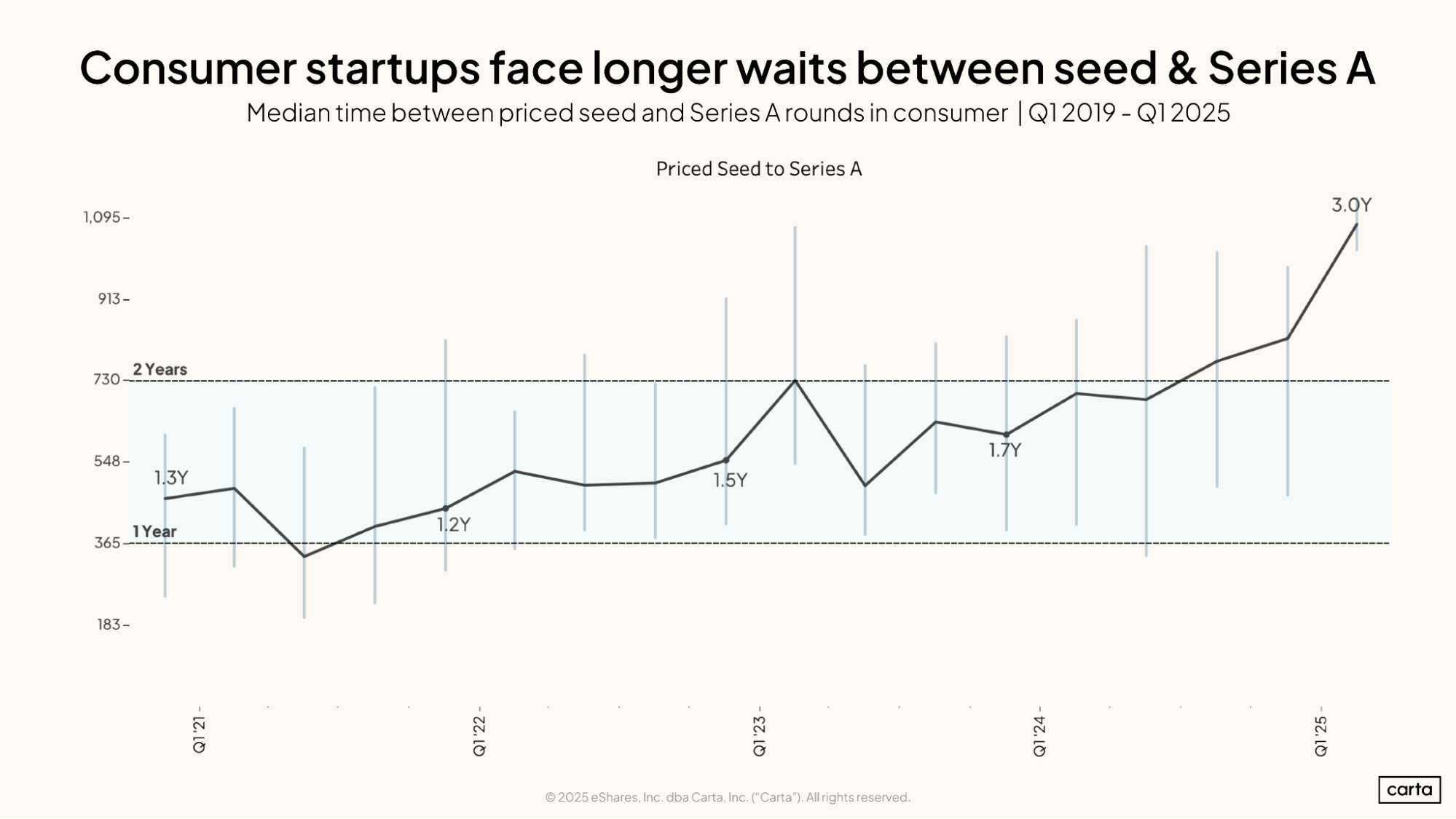

Patience is a virtue: The typical early-stage consumer startup is waiting longer than ever between its seed round and a Series A. For companies that successfully raised a Series A in Q1, the median interval between seed and Series A was three full years, up from 1.7 years in Q1 2024.

Data & analysis

Consumer startups on Carta raised 47% less cash in Q1 2025 and closed 32% fewer rounds than they did in the previous quarter. Prior to these significant declines, venture investment in the consumer space was moving in a positive direction. On a quarterly basis, both deal count and total cash raised both generally trended up over the course of 2024.

The industry appeared to have settled into a new equilibrium from the start of 2023 onward, with quarterly investment in the space landing between $1.2 billion and $1.9 billion in eight consecutive quarters. Those numbers were already well below the typical consumer fundraising figures seen from 2019 through 2022. In Q1, they sank even lower.

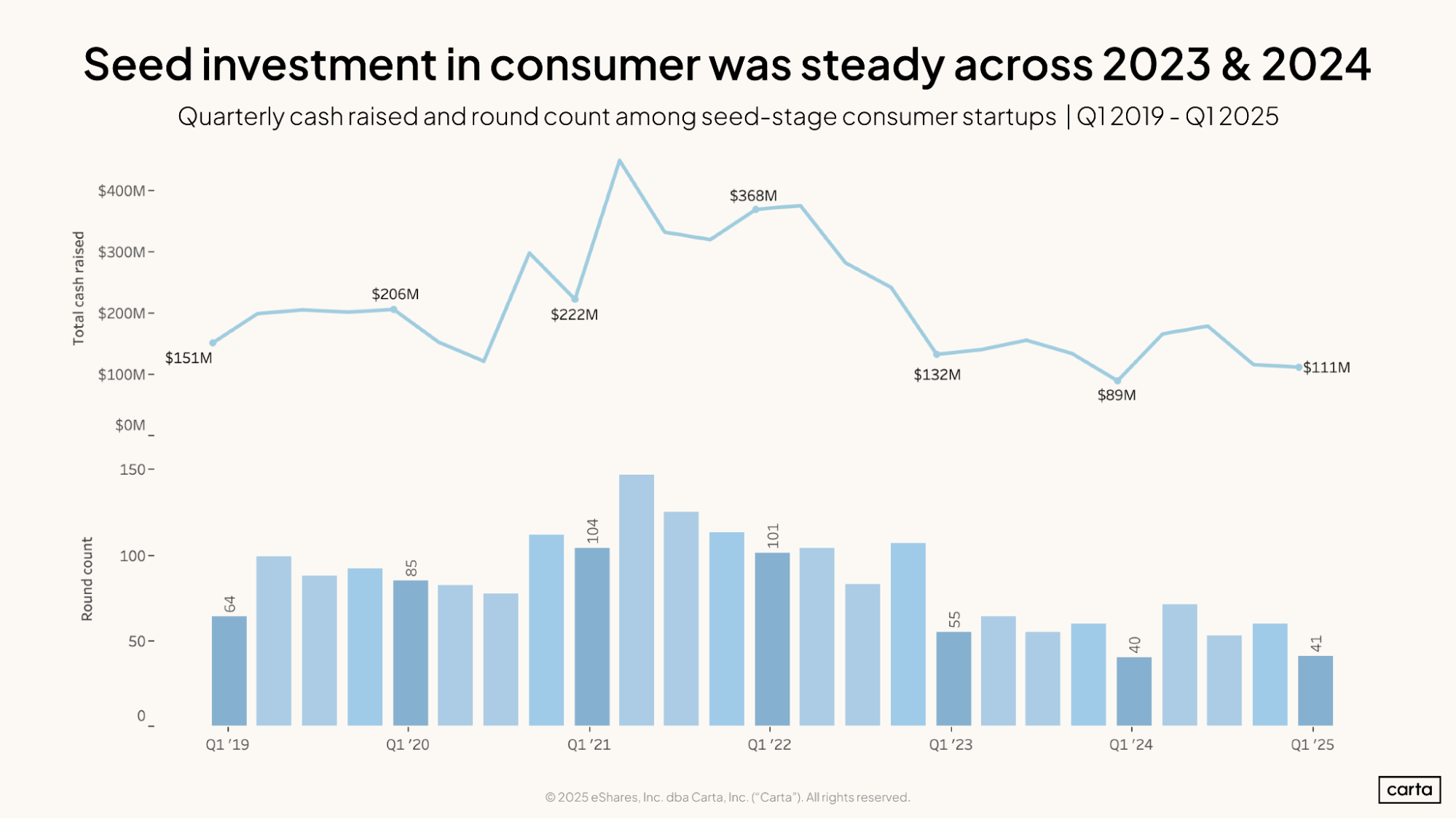

At the seed stage, consumer startups on Carta raised $111 million in Q1 across 41 transactions, equating to an average check size of about $2.7 million. In terms of dollars, investment at the seed stage held firm in Q1: Cash raised at seed was down just 4% quarter over quarter, compared to the above 47% dropoff across all stages.

In terms of deal count, however, Q1 was one of the slowest quarters for seed-stage consumer activity of the past several years, continuing a general trend. Jeanlys-White attributes this decline in deal counts since the start of 2023 to a change in the criteria that investors are looking for before they’re willing to write a check.

“A lot of investors are focusing on profitability, and how quickly a company can get profitable,” Jeanlys-White says. “A few years ago at pre-seed and seed, we weren’t hearing that.”

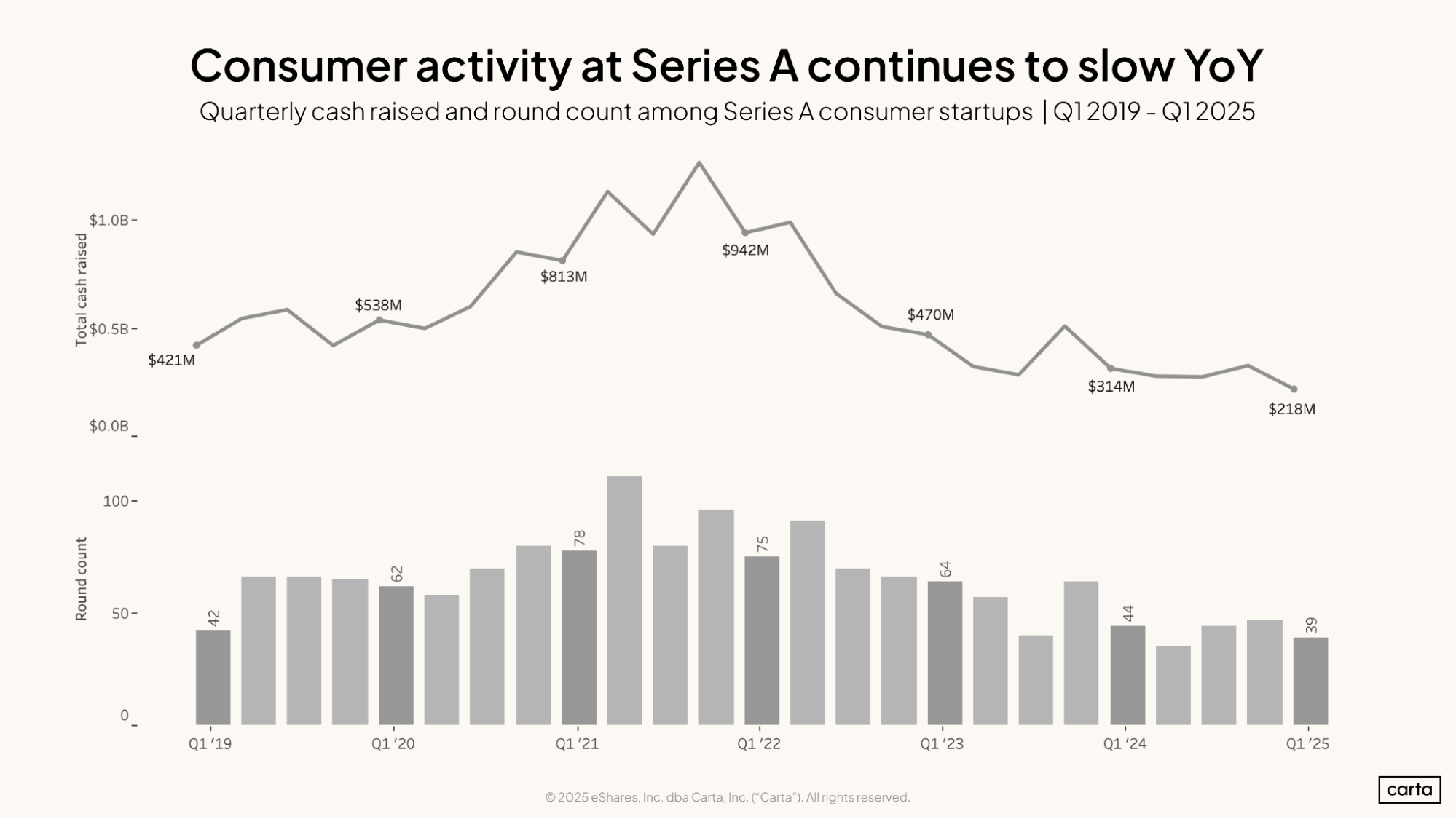

Springate agrees that the baseline of what makes an early-stage consumer company worthy of VC investment has changed. This trend is also apparent at Series A, where companies closed 39 new rounds in Q1. That’s down 11% year over year and 48% compared to two years ago.

“AI has raised the bar: Founders can now do more with leaner teams, so MVP expectations are higher,” Springate says. “Investors want to see traction earlier.”

Quarterly totals for cash raised by Series A consumer startups have been steadily declining for the past four years. Fundraising reached a new lowpoint in Q1 2025, at $218 million, a 31% year-over-year decline.

The size of the median consumer seed round dipped below $1 million in Q1, falling to about $700,000. The median valuation has also fallen compared to a year ago, but in general, valuations at the seed stage have proven much more resilient over the past several years than round sizes.

These statistics may belie an underlying shift in the environment. While valuations have held relatively steady, Jeanlys-White says that valuation multiples have been in decline. This means that startups need to have higher levels of revenue than they used to in order to attain the same valuation.

“The overall sentiment is that people are raising at lower valuation multiples, lower multiples on revenue,” Jeanlys-White says. “The targets have moved. Whereas maybe a year ago, a company that had $2 million in revenue could expect a valuation of 12x or 10x, we’re seeing that now looks closer to 7x or 7.5x.”

After falling off during 2023, median Series A valuations for consumer startups have now been on the rise for more than a year. In Q1, the median valuation reached $45.3 million, the third-highest figure out of the past 25 quarters.

Still, the median Series A valuation in consumer lags a bit behind the median Series A valuation from Q1 across all sectors, which was $48 million. The same is true for the seed stage, where the median valuation across all sectors was $16 million in Q1, compared to $13.6 million in consumer.

Series A consumer round sizes remain far lower than pre-2023 norms. The median Series A round in Q1 2025 totaled $2.8 million, compared to $5.1 million two years ago and $8 million three years ago. Across both seed and Series A, there’s a clear trend of consumer startups raising less capital while retaining roughly similar valuations.

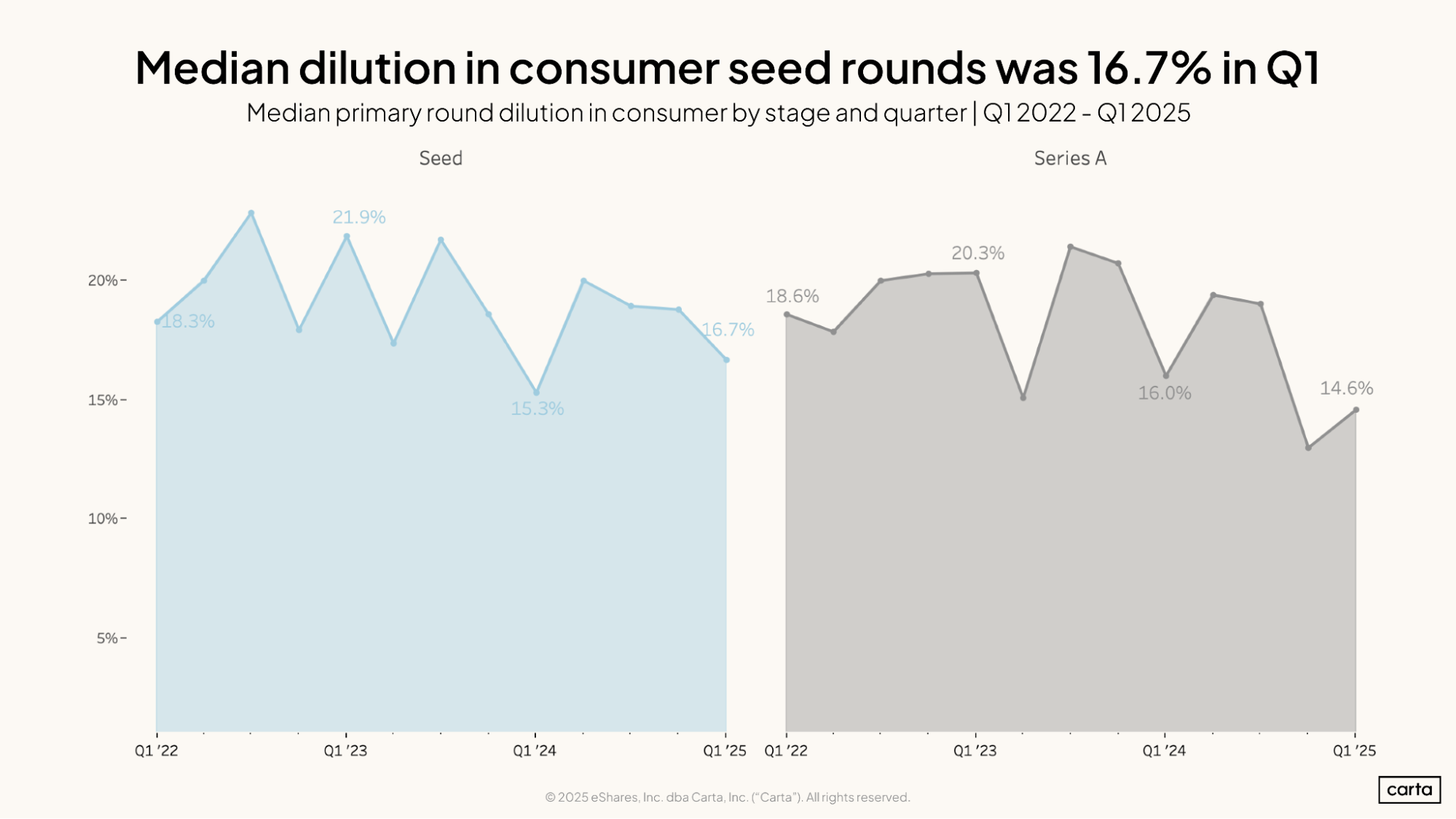

When valuations stay the same and round sizes get smaller, dilution levels decline. In Q1, the median consumer seed round involved 16.7% dilution, while the median dilution at Series A was 14.6%. While there has been some notable variability from one quarter to the next, dilution is generally trending down over the past few years at both stages.

The same trend is true across VC as a whole. In the consumer sector, though, dilution tends to be a little lower than the norm. At seed, median dilution across all sectors was 18.8% in Q1, and at Series A, it was 17.9%.

Over the past year, the expected wait time between raising a seed round and a Series A has skyrocketed for consumer startups. The median reached an even three years in Q1 2025, nearly twice as long as it was in Q1 2024.

This means consumer founders today must be prepared to make their capital last for longer. They can also expect their VC backers to emphasize the need to build with discipline.

“Longer timelines mean founders need to master capital efficiency, storytelling, and re-engagement,” Springate says. “A 36-month seed cycle forces a company to evolve in-market before a growth raise—there’s more time to iterate, but also more pressure to show real traction.”

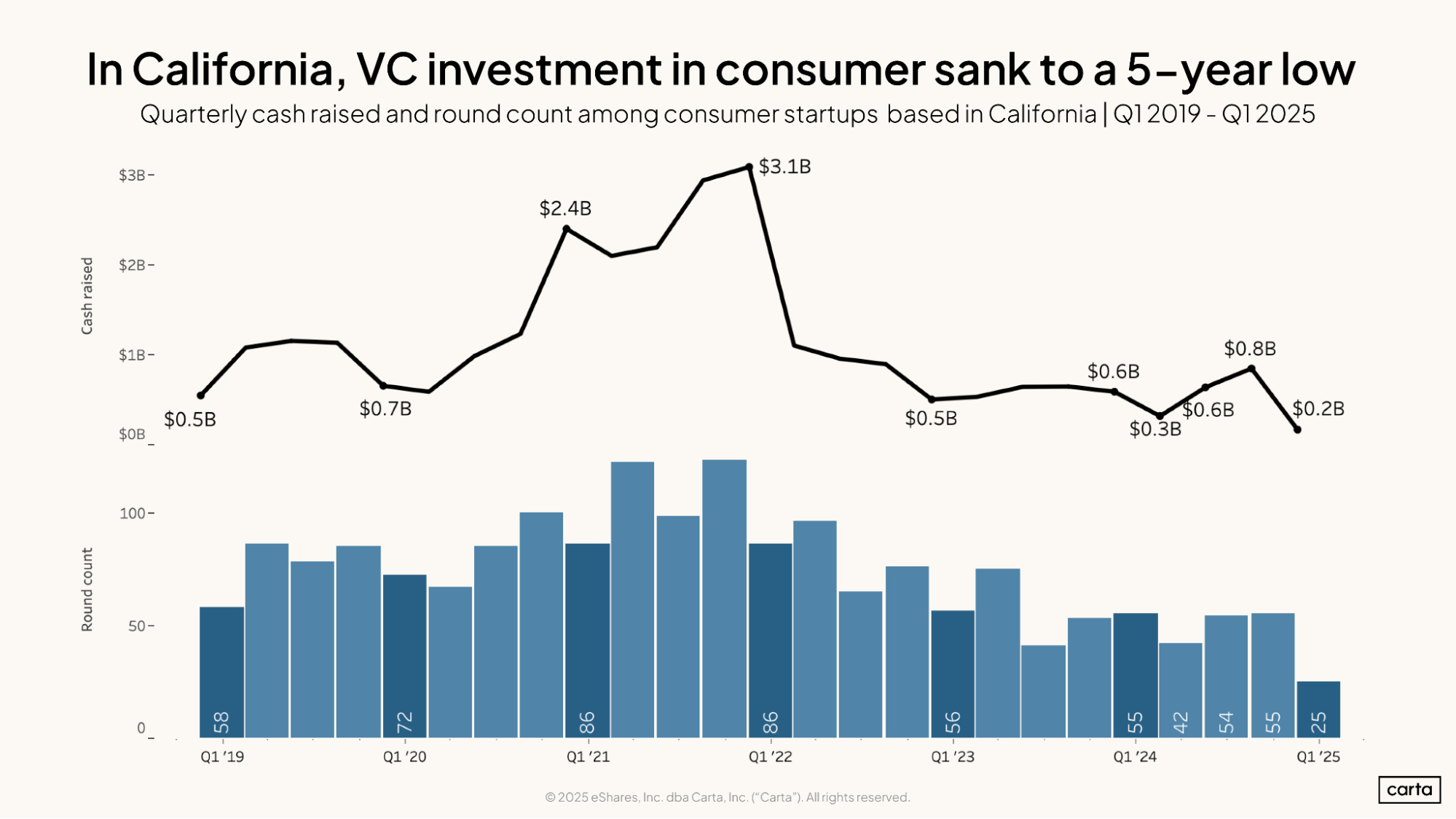

Typically, California is by far the busiest state in the U.S. for consumer fundraising. Over the course of 2024, for instance, consumer startups based there combined to raise about $2.3 billion, roughly 44% of the national total.

In Q1 2025, however, California-based consumer startups on Carta brought in just $168 million (rounded up in the above chart), which was just 21% of all U.S. funding—a significant decline from 2024’s market share. It was the slowest quarter for consumer investment in California since at least the start of 2019.

It was also a very quiet Q1 in terms of deal count. California-based consumer startups on Carta closed 25 transactions between the start of January and the end of March, down 55% both quarter over quarter and year over year.

This data may revert toward historical norms as the rest of 2025 plays out. But Springate believes it may also be a trend to watch, with other consumer markets—particulalry those in the Northeast—showing signs of growth.

“New York City and Boston are benefiting from proximity to media, finance, and healthcare, all increasingly intertwined with consumer behavior,” she says. “Geography is becoming less important than founder-ecosystem fit: who you can access, partner with, and learn from.”

Sign up for the Data Minute newsletter:

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. © 2026 Carta. All rights reserved. Reproduction prohibited.