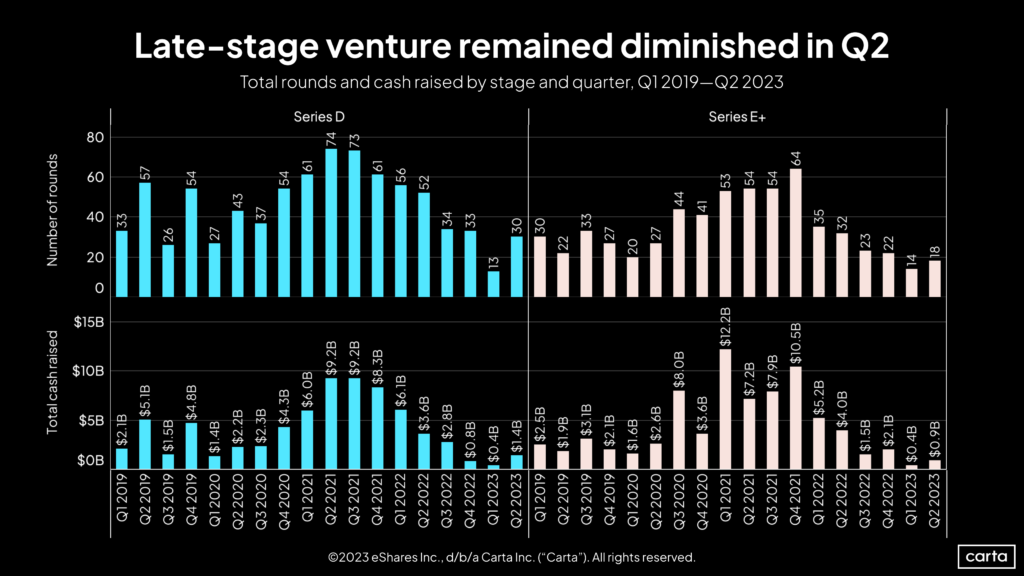

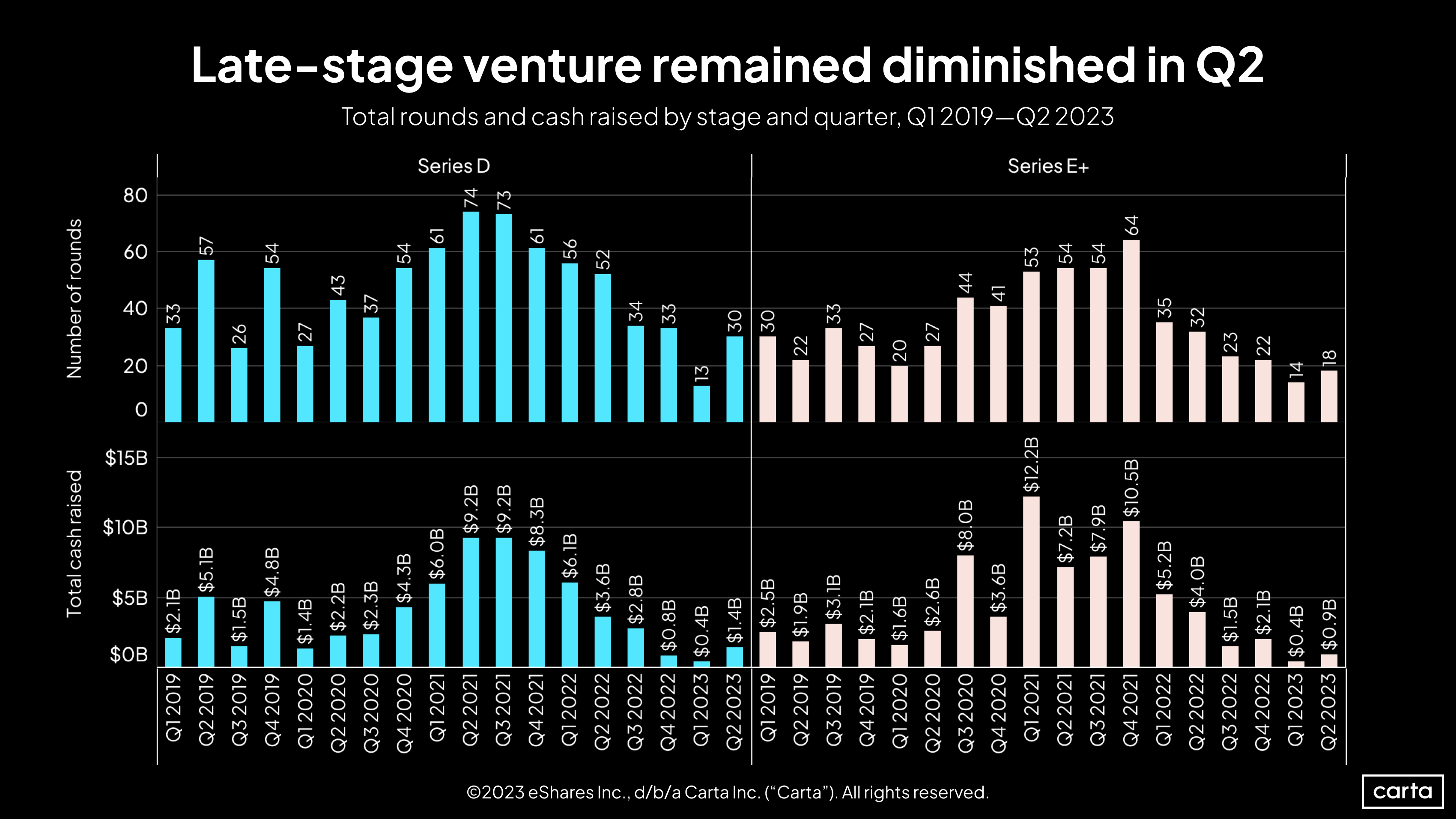

In terms of cash raised and deal count, late-stage venture capital activity was back on the upswing in Q2. Series D startups on Carta raised $1.4 billion in new capital, up some 250% from Q1. The number of Series D deals jumped from 13 to 30.

But even with those gains, the Series D market is still very far from the highs it hit in 2021. Even with Q2’s results, total cash raised in Series D rounds was down 61% year-over year—signaling just how dramatic the market decline was over the previous few quarters.

Similar trends are playing out at later stages. Startups at Series E and beyond pulled in $900 million on Carta in Q2, more than doubling the previous quarter. But that still represented an 78% year-over-year decline and was the second-lowest quarter for cash raised since the start of 2019.

A few factors have likely led to Q2’s late-stage bump. Certain macroeconomic headwinds have abated, with inflation trending down. Additionally, VC firms that closed funds during 2021’s record-setting fundraising period are in the thick of the typical deployment period (18 to 36 months), incentivizing them to put capital to work or return it to LPs.

But there are significant headwinds still hampering the late-stage environment. The IPO market remains muted and M&A has slowed, limiting exit opportunities for late-stage investors and by extension hurting late-stage dealmaking. Also, crossover investors that propped up the market during the height of the VC frenzy have largely retreated. Some investors are even participating in secondary sales of their stakes in portfolio companies to appease LPs that want liquidity.

Meanwhile, the average size of Series A, B, and C rounds ticked up in Q2, signaling that VCs with multi-stage fund strategies may be more focused on the early-stage market than making late-stage bets. Early-stage startups are less impacted by the same macroeconomic headwinds impacting public tech companies and by extension the late-stage market, in part because these startups are typically at least five years away from reaching an exit.

Get weekly insights in your inbox

The Data Minute is Carta’s weekly newsletter for data insights into trends in venture capital. Sign up here:

DISCLOSURE: This communication is on behalf of eShares Inc., d/b/a Carta Inc. (“Carta”). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. ©2023 eShares Inc., d/b/a Carta Inc. (“Carta”). All rights reserved. Reproduction prohibited.