The median size of Series A rounds fell for the fourth straight quarter, but seed deals have not experienced a similar dip, signaling a divergence in how VC investors are thinking about these two early stages amid a broader VC slowdown.

Let’s take a closer look at the discrepancy:

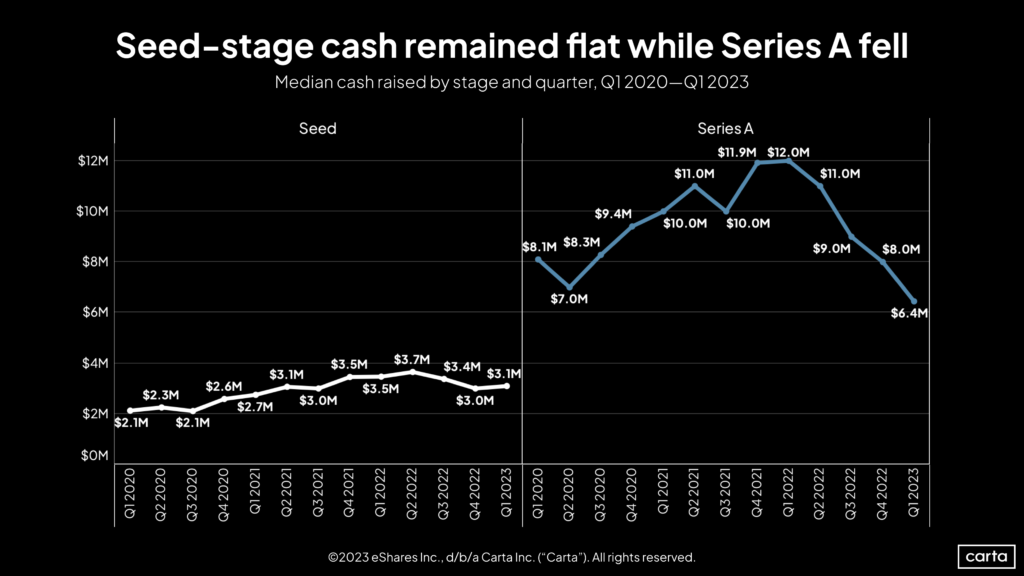

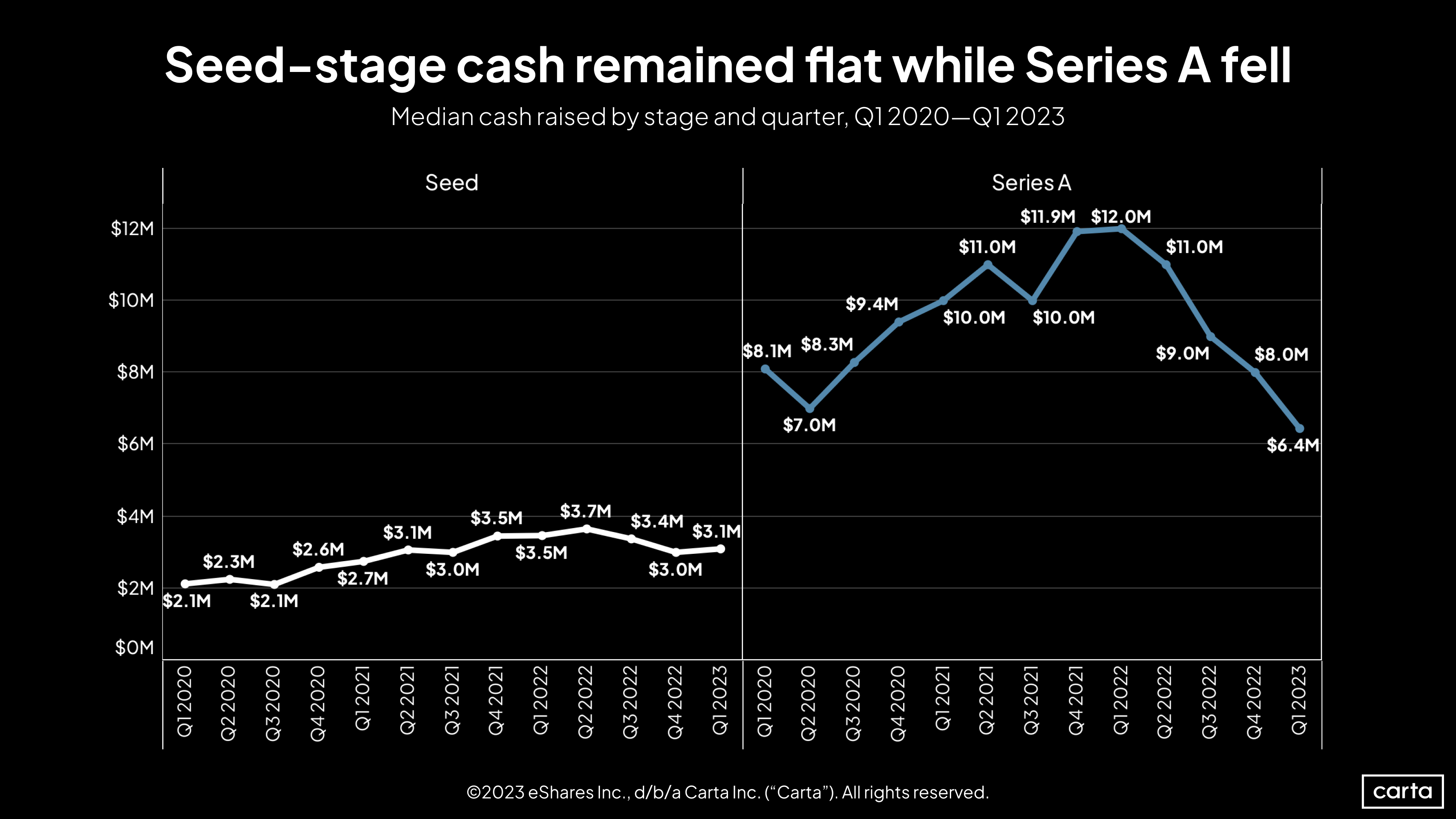

Cash raised: In Q1, median cash raised for a Series A round on Carta dropped 20% to $6.4 million, down from $8 million the previous quarter. Meanwhile, the median cash raised for a seed round on Carta saw a 3% bump to $3.1 million, up from $3 million in Q4 2022.

Declines from 2022 peaks: The Q1 median cash raised for a Series A round was down 47% from the highs reached in Q1 2022, when it peaked at $12 million. In contrast, the Q1 median cash raised for a seed round was down only 11% off the peak of $3.7 million reached in Q2 2022.

Capital invested still way down:In Q1, the capital invested in seed deals totaled roughly $1.3 billion, down 63% from some $3.5 billion in the same period a year earlier. Capital invested in Series A deals took a similar dive, dropping 62% from $8.2 billion in Q1 2022 to $3.4 billion this past quarter.

The drop in Series A deal size is part of a broader slump in the venture ecosystem. Capital invested for late-stage VC deals has cratered since the Federal Reserve began raising interest rates in early 2022: The median cash raised for a Series D deal dropped 67% YoY in Q1 and Series E+ dropped 77% during the same timeframe, according to Carta data. The pullback has had a cascading effect, with Series C, then Series B, and finally Series A feeling the impact of a cautious investing environment characterized by longer due diligence cycles and less capital invested.

Nate Leung, a partner at Sapphire Partners who specializes in early-stage venture fund investments, witnessed the recent Series A dip across the board as a limited partner. He attributes part of the decline to VC firms slowing their deal pace and looking for Series A companies with higher ARR (annual recurring revenue), a closely watched metric that helps determine valuations for startups.

“The bar for Series A deals has gone back to pre-Covid norms,” Leung says. “Now startups need at least $1 million in ARR.”

Leung says that some VCs have simply opted to execute a SAFE or convertible note instead of going through with a Series A, with only the most sought-after Series A startups drawing elevated valuations. Many VCs have opted to raise a bridge round rather than a traditional Series A deal. In Q1, roughly 40% of investments in Series A companies were bridge rounds.

The turbulence at Series A has caused some VCs to think differently about the seed stage—and it’s changing the character of seed investment.

VCs have traditionally viewed seed deals as a high-risk, high-reward investment strategy. A majority of seed investments fail, but a fund only needs one or two seed companies to succeed to make the fund a success.

Seed investors also focus less on a startup’s revenue and unit economics, and more on providing capital and getting the product to market. Seed-stage startups don’t experience the same volatility in investment size and valuations experienced by late-stage counterparts that are vulnerable to macroeconomic conditions like rising interest rates and geopolitical risks. As a result, seed deals have become a way to hedge against the current private market slowdown.

Leung says upmarket funds raised in 2021 and 2022 that invest at multiple stages have shifted some focus away from Series B and growth deals and increasingly directed that capital toward seed deals. The influx of new capital has made seed deals more competitive than Series A investments, Leung says. That trend won’t subside until investors get more comfortable in a less favorable investing environment.

As Leung says, “Seed remains the safest place to invest.”

Get weekly insights in your inbox

The Data Minute is Carta’s weekly newsletter for data insights into trends in venture capital. Sign up here:

DISCLOSURE: This communication is on behalf of eShares Inc., d/b/a Carta Inc. (“Carta”). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. This post contains links to articles or other information that may be contained on third-party websites. The inclusion of any hyperlink is not and does not imply any endorsement, approval, investigation, or verification by Carta, and Carta does not endorse or accept responsibility for the content, or the use, of such third-party websites. Carta assumes no liability for any inaccuracies, errors or omissions in or from any data or other information provided on such third-party websites.©2023 eShares Inc., d/b/a Carta Inc. (“Carta”). All rights reserved. Reproduction prohibited.