As broader investment activity across the venture capital industry has increased over the past decade, the use of special purpose vehicles (SPVs) among institutional investors has expanded, too. The number of new SPVs exploded during the venture capital boom of 2021, rising 235% year over year. SPV formations have slowed down since then, but the long-term trend is clear. Compared to three years ago, the annual count of new SPVs formed on Carta is up 31%. Compared to five years ago, it’s up 116%.

Despite that growth, this segment of the private market can remain opaque. We aim to change that. How large do SPVs tend to be? How many investors do they have? What sort of fees do they charge?

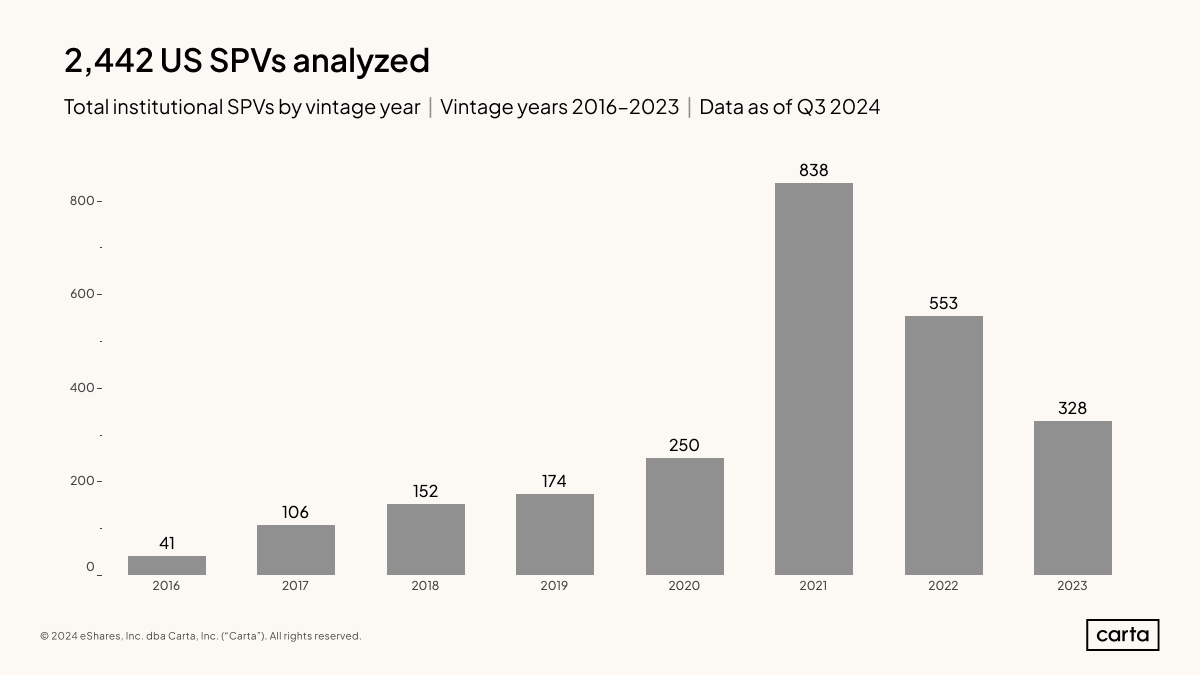

This report offers our broadest and clearest look to date at the state of the SPV landscape. It relies on aggregated and anonymized data from 2,442 SPVs formed in the U.S. between the years 2016 and 2023. Each of these vehicles was either formed or managed (or both) with Carta Fund Administration, an all-in-one platform where investors can form, close, and manage their SPVs. Investors can use turnkey templates or customize their own SPV solutions while streamlining their LP communications and receiving ongoing support throughout an SPV’s lifespan.

In some ways, SPVs are similar to traditional venture capital funds: Both are mechanisms for investors to raise capital from limited partners and invest in startups. But SPVs are also quite different. SPVs typically invest in a single asset, compared to the large portfolios of traditional funds. SPVs serve bespoke purposes, are typically smaller than traditional VC funds, and often draw capital from a smaller group of LPs.

SPVs also present a different set of variables to consider for these LPs. SPVs tend to operate on shorter timelines than other private funds, meaning a successful investment can produce returns more quickly. Management fees are less common in SPVs than traditional funds. However, making one investment instead of many means that SPVs don’t provide the same diversification of risk that other fund varieties can offer.

Highlights

SPVs have boomed in the 2020s: Investors formed and managed a combined 1,719 SPVs on Carta between 2021 and 2023, up 198% compared to the previous three-year period.

SPVs are getting bigger: In 2016, the median SPV on Carta managed $1.18 million in assets. By 2023, that number had climbed to $2.17 million.

Management fees are growing more common: Back in the surging venture market of 2021, just 41% of SPVs with more than $10 million in AUM charged a management fee. In 2023, 67% of similarly sized funds charged a fee.

SPV structure

By far the busiest year in recent history for new SPV formation was 2021. Investors raised 838 new vehicles in the U.S. that year, nearly 600 more than the year prior. Since then, however, SPV formation has slowed. The number of new vehicles declined by 34% in 2022, then another 41% in 2023.

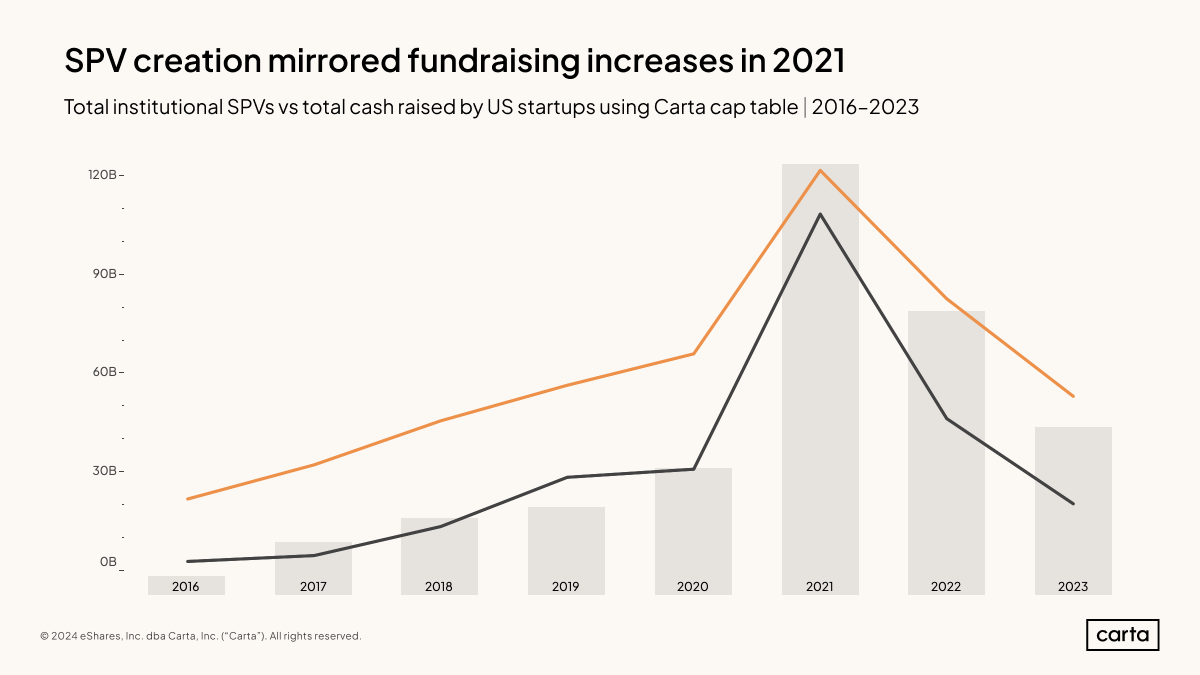

This recent history of SPV formation tracks closely with other recent trends in venture capital, such as annual totals for capital raised by startups through primary rounds, as you can see here. When investors are putting more capital to work, they also tend to utilize more SPVs for alternative deal structures.

We can also see here that, while the rates of both new SPV formation and new investment in primary rounds have slowed compared to 2021, they remain higher than they were in the late 2010s. On this eight-year timeline, the overall trend lines for both these forms of venture capital activity are still pointing up.

Market factors aren’t the only reason for the recent uptick in SPV count, however: Some of the increase can likely be attributed to a concurrent increase in the size of Carta’s overall customer base and dataset.

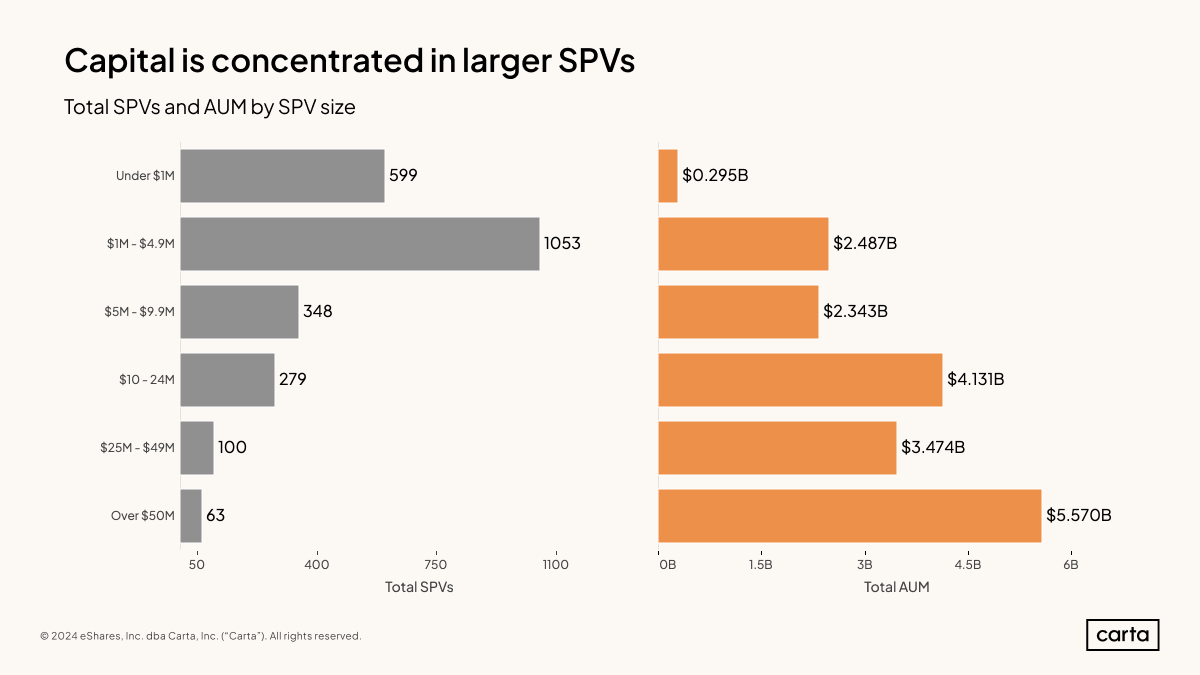

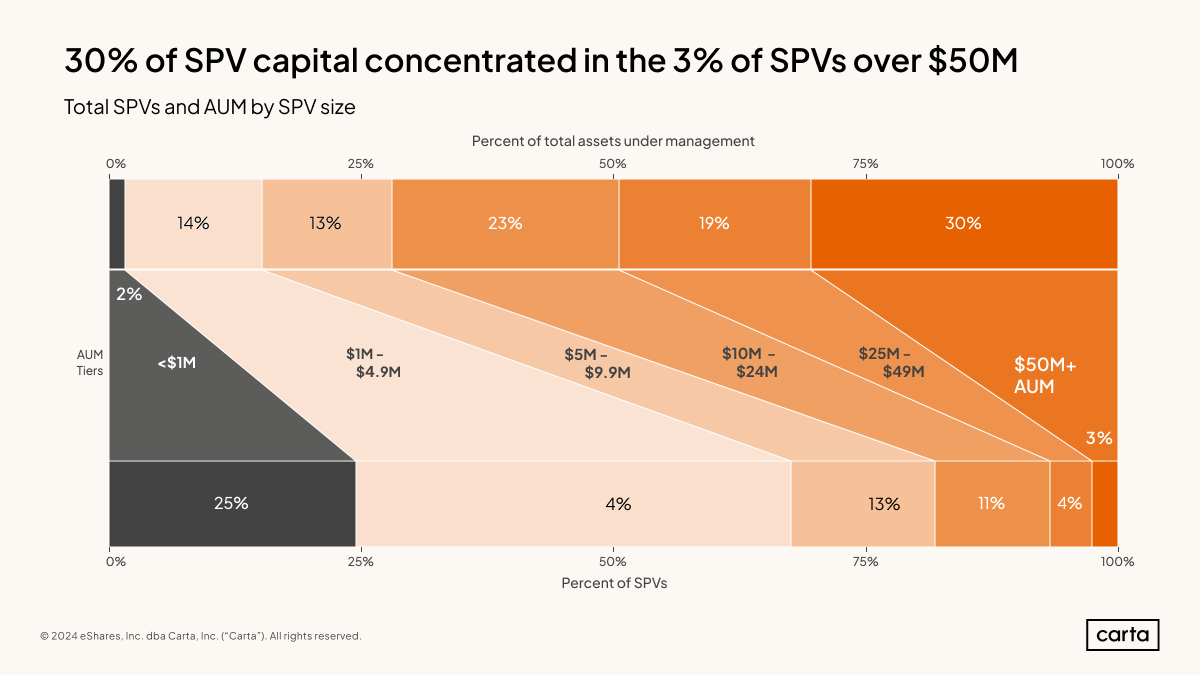

Most SPVs are small: More than two-thirds of all SPVs raised on Carta between 2016 and 2023 had less than $5 million in assets under management. Many of these smaller SPVs are used to invest in early-stage companies. This segment includes most of the SPVs that are deployed by solo GPs who are seeking to establish a track record before raising their first institutional fund.

From an asset perspective, however, these small SPVs represent a relative drop in the bucket: SPVs smaller than $5 million hold just 15% of all assets raised over this span.

At the other end of the spectrum are SPVs that manage $50 million or more in assets. Just 2.6% of all SPVs on Carta meet this classification. Yet these supersized vehicles account for more than 30% of all capital raised—twice as much capital as is managed by all sub-$5 million SPVs combined.

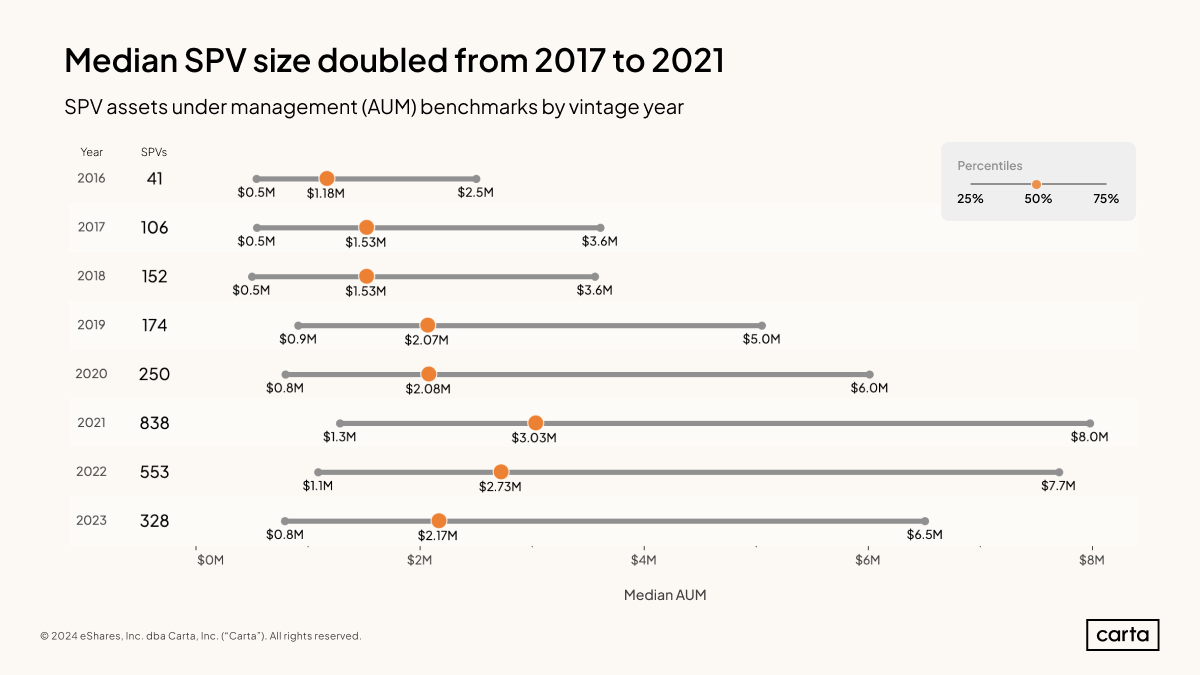

As SPVs have grown more common in the venture ecosystem, they’ve also gotten bigger.

In 2017, for instance, a 25th percentile SPV had about $500,000 in assets under management. A median SPV that year claimed $1.5 million in AUM, and a 75th percentile vehicle managed $3.6 million.

By 2023, the 25th percentile for SPV size had climbed to $800,000, the median to $2.2 million, and the 75th percentile to $6.5 million. Over that span, the 25th percentile figure increased by 60%, the median increased by 47%, and the 75th percentile by 81%.

As the total number of SPVs being raised has increased, the number of vehicles that fall outside the bounds of this middle 50th percentile increases, too. In 2021, for instance, investors raised 838 SPVs, and the 75th percentile for AUM was $8 million. This means there were over 200 SPVs that raised more than $8 million each.

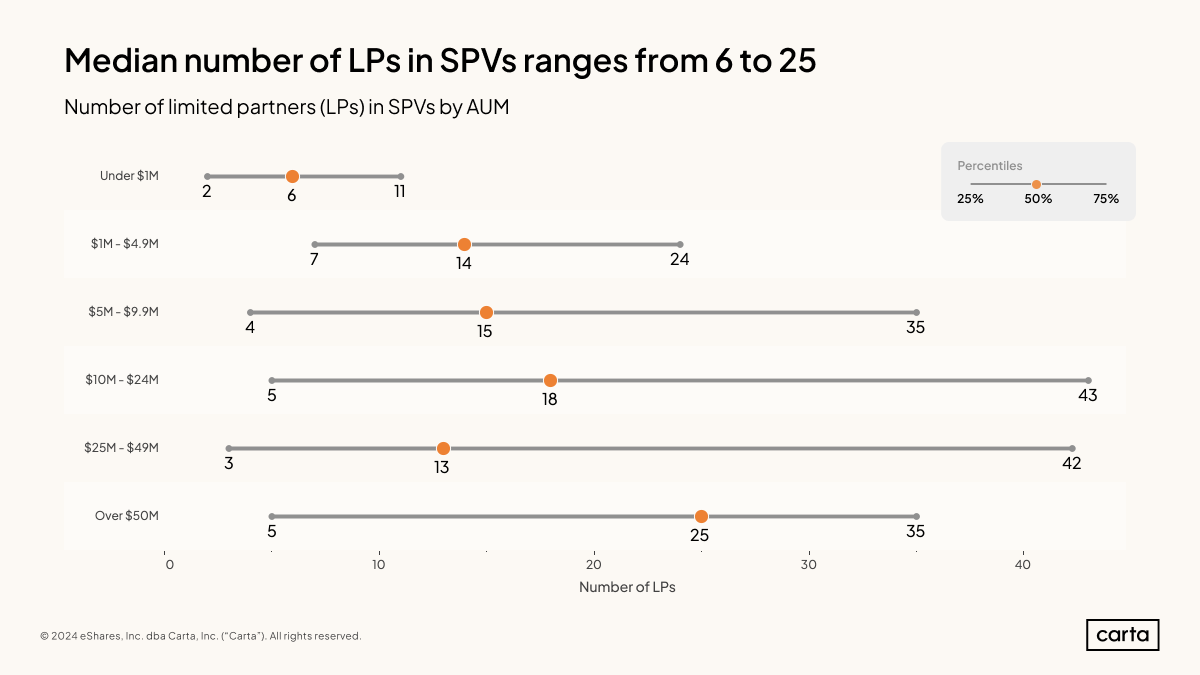

There is no standard number—or even range of numbers—for how many LPs contribute capital to an SPV. It depends more on factors such as deal structure, investment size, and profile of the asset.

For example, take the group of SPVs with between $25 million and $49 million in assets under management, which we saw above comprises 100 vehicles. At the 25th percentile, SPVs in this size interval have just three LPs. At the 75th percentile, they have 42 LPs. That’s more of a gulf than a gap—and it still only covers the middle 50 percent of all SPVs raised. Some SPVs have a single LP, and some have dozens and dozens.

The LPs in SPVs can come in many different forms, ranging from individual and institutional investors through sovereign wealth funds and endowments.

SPV fees

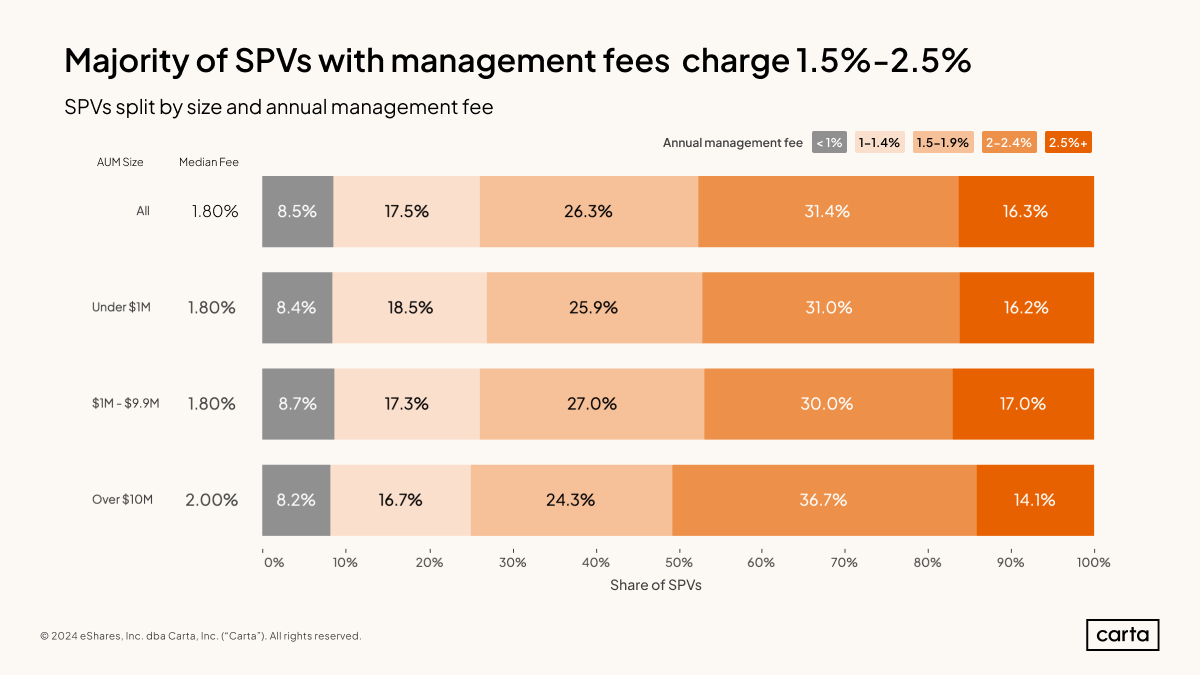

Only about 44% of all SPVs on Carta charge any management fees at all. Among those that do, the management fee typically doesn’t vary too much depending on the size of the SPV. Across all sizes of SPVs, about 75% of all vehicles charge a management fee higher than 1.5%.

There are some differences: The median fee is 1.8% for SPVs smaller than $10 million, compared to 2% for SPVs larger than $10 million. In general, larger SPVs are more likely to charge a larger fee. Of those SPVs larger than $10 million that do apply a management fee, about 50.8% charge a fee of 2% or higher. Among SPVs smaller than $1 million, the rate of SPVs that charge a fee over 2% is slightly lower, at 47.7%.

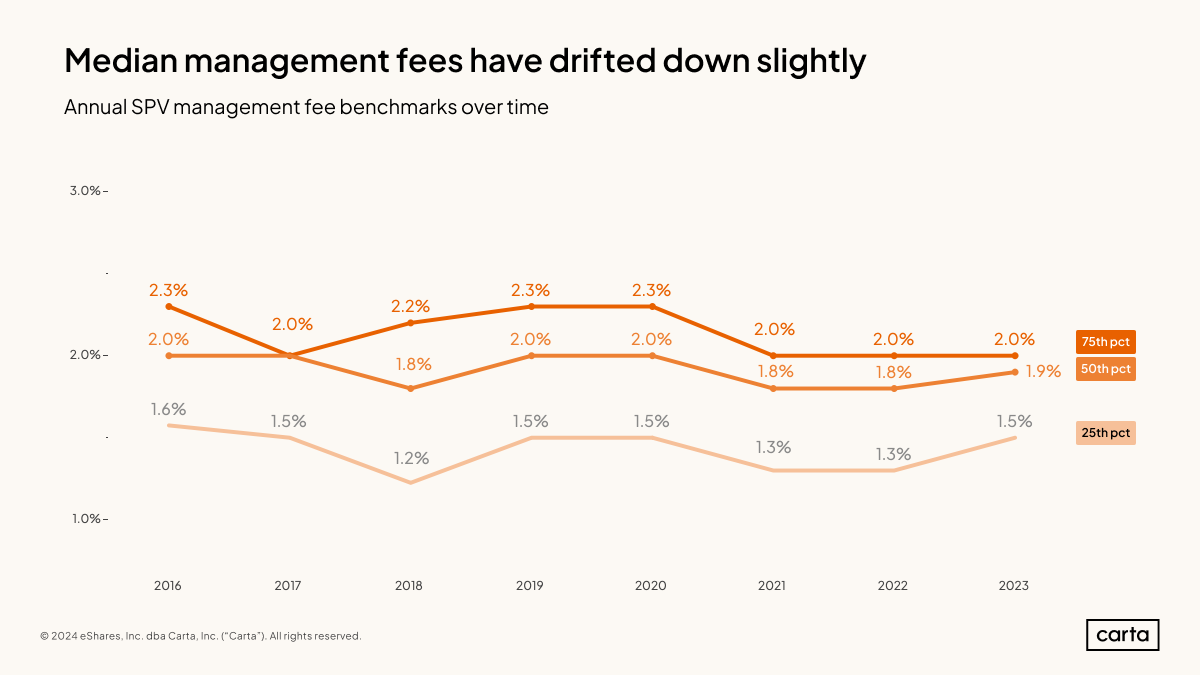

The typical management fees that SPV investors charge their LPs haven’t changed very much over the past eight years. But the needle has moved slightly to favor LPs: The median SPV charged a 1.9% management fee in 2023, down from 2% back in 2016 (and as recently as 2020).

In 2023, the 75th percentile for management fees was 2%, and the 25th percentile was 1.5%. That’s the smallest difference between those two figures since 2017. This tightening of the gap may indicate that management fees charged by SPVs are growing more standardized.

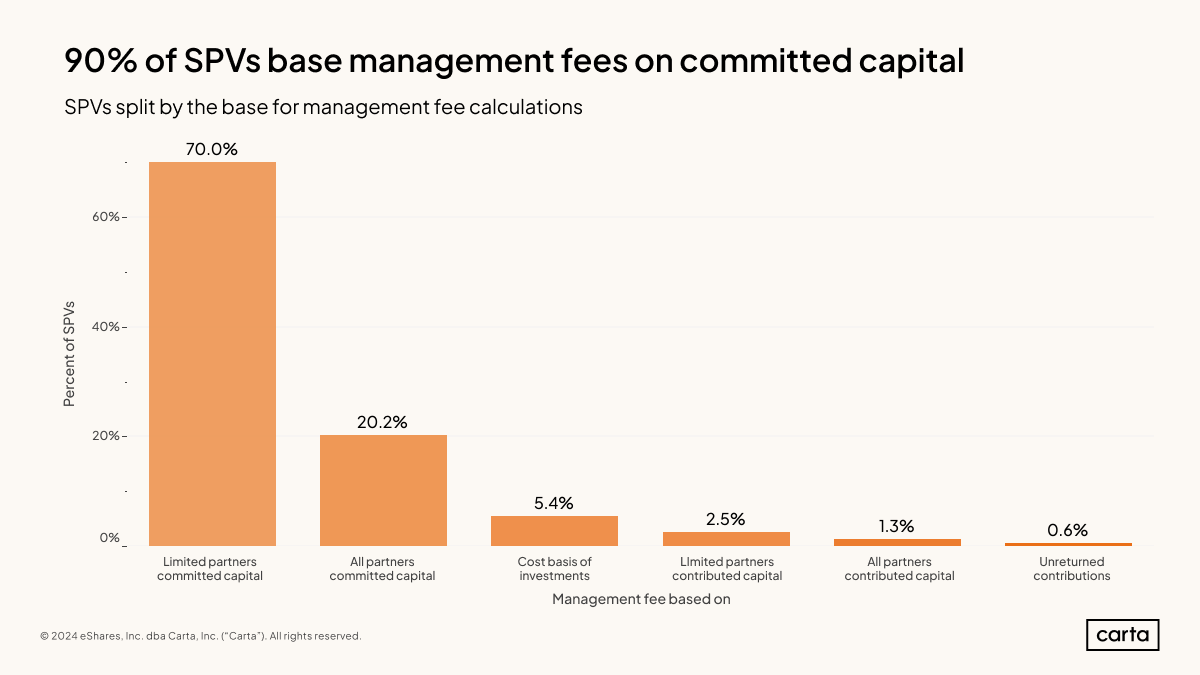

Nearly 90% of all SPVs use a fund’s committed capital as the baseline for calculating management fees. Within this clear majority, however, there are two different approaches: About 70% of all SPVs base their management fees only on the capital committed by outside LPs, while about 20% base their fees on the capital committed by both LPs and GPs.

The latter approach is generally more friendly to the GP. Management fees are typically calculated as a percentage of total capital. So if the GP includes their own contributions, then the pool of total capital grows larger, and the size of the fee grows, too.

In most cases, however, this difference is negligible. As shown below in more detail, the median GP commitment is typically somewhere between 0.3% and 1.2% of the overall SPV size.

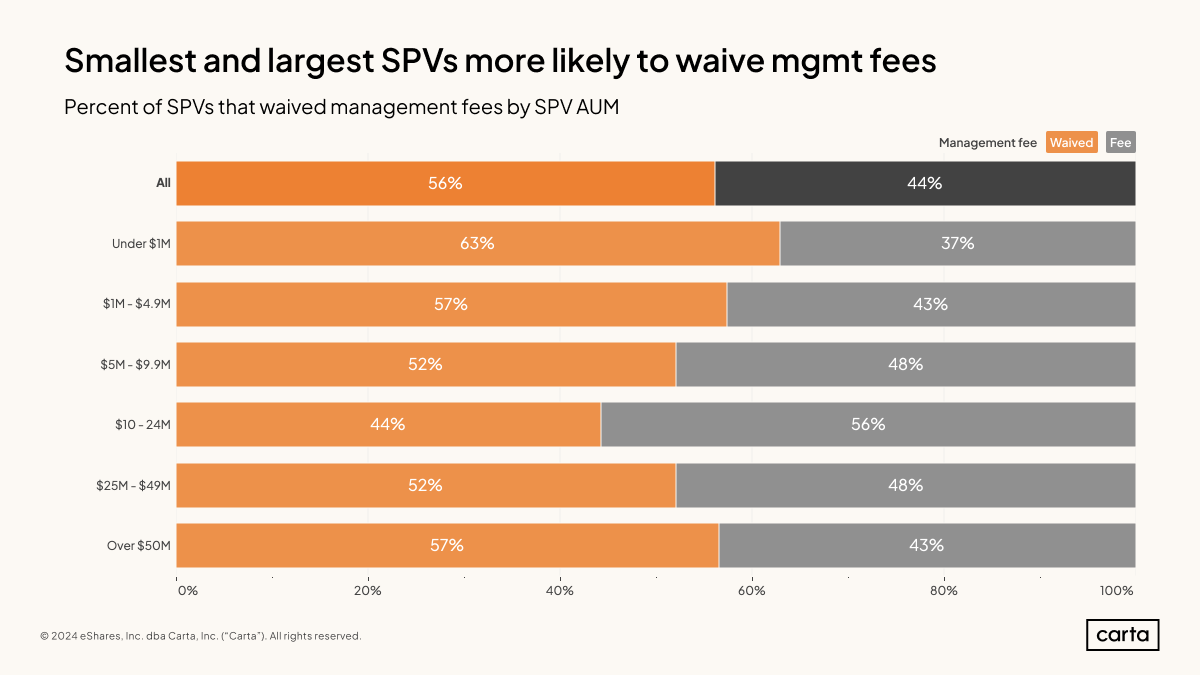

Most SPVs, however, don’t charge any management fees at all. For every size interval except for the $10 million to $24 million range, the most common approach is for SPV managers to waive their management fees, removing one more potential obstacle that might prevent LPs from writing a check.

Management fees are least common among SPVs with less than $1 million under management: Just 37% of vehicles of this size charge any management fee at all. As the SPV grows larger, management fees grow more common—up to a point. Once SPVs get larger than $25 million, management fees once again start to grow less common, looking more like small SPVs than mid-sized vehicles.

Why are management fees less common among the smallest SPVs? In some cases, the managers of these vehicles might lack the leverage or caché to ask their LPs to pay a management fee. In others, the management fee might be so negligible—perhaps a few thousand dollars—that it isn’t worth the GP’s while. Smaller SPVs are also more likely to invest at earlier stages, which comes with more risk. If the SPV is investing in a more mature startup with a likelier chance of a solid return, LPs may be more willing to pay a fee.

And what about the largest SPVs? Many of these vehicles are follow-ons raised by a VC firm for a specific deal, often to increase their stake in an existing portfolio company. The LPs in these large SPVs often are also LPs in the firm’s other funds. Since these LPs are already paying management fees on these other funds, GPs may be more likely to waive fees on follow-on SPVs.

Compared to these biggest vehicles, SPVs in the middle size intervals are more likely to be raised by managers to pursue new investments, rather than to support existing portfolio companies. Sometimes, they’re the only way for investors to get access to a buzzy, later-stage asset. Oftentimes, the managers of these mid-sized vehicles specialize in SPVs, while managers of jumbo SPVs might make the majority of their investments through VC funds. If an investor’s main business is SPVs, they’re more likely to charge fees.

Between 2021 and 2023, the number of new SPVs raised declined significantly. Over the same span, the percentage of SPVs charging annual management fees increased significantly. To some degree, at least, this dynamic is likely due to simple supply and demand: As the number of VC deal opportunities on the market has declined, some SPV managers have felt more empowered to charge fees on the new SPVs still being raised.

The number of new venture funds closing has also dropped in recent years. Given the relative paucity of options for investing in traditional VC funds, some investors have been more eager to invest in SPVs and more willing to pay a fee for the privilege.

The rate of SPVs with more than $10 million in AUM rocketed from 41% in 2021 to 67% in 2023. For SPVs with between $1 million and $10 million in assets, the rate of vehicles charging management fees increased from 38% to 57% over that same span. For SPVs of these sizes, charging management fees has gone from unusual to the new norm.

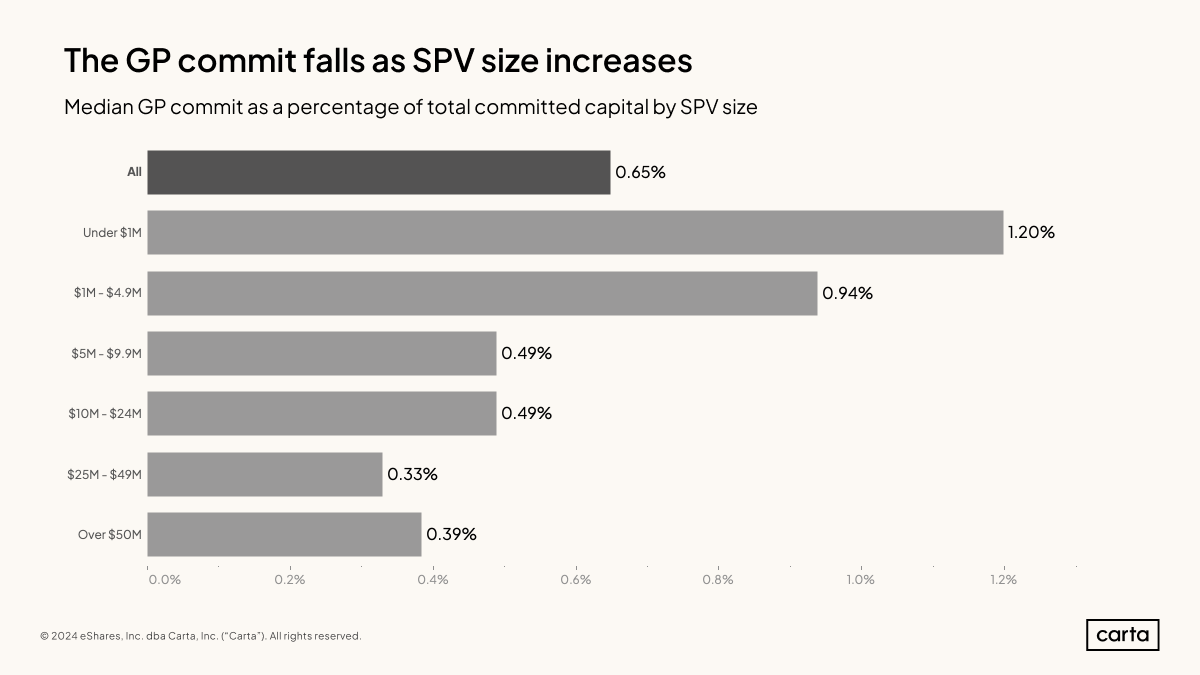

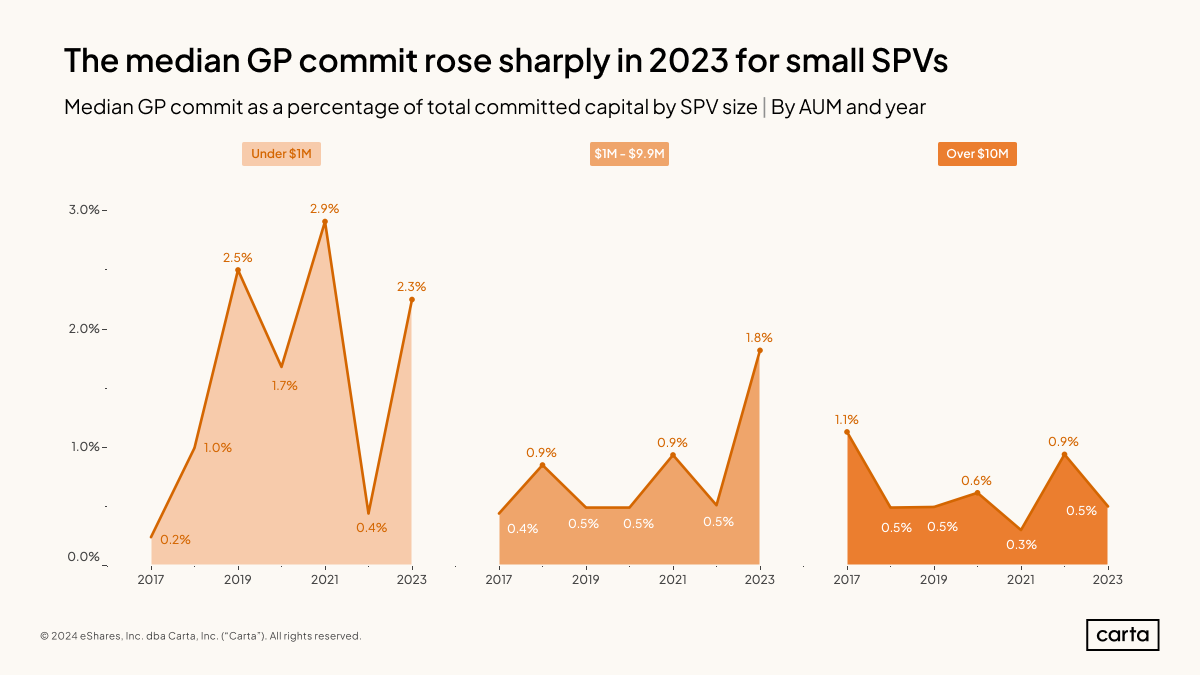

Among GPs that contribute some capital to their SPVs, the relative size of that contribution can vary significantly depending on the size of SPV.

For vehicles smaller than $1 million, the median commitment from the GP is 1.2% of the overall fund size. For SPVs larger than $50 million, meanwhile, the median GP commit comprises 0.39% of the total fund. In general, the larger the SPV, the smaller the portion of its overall capital that will come from the GP.

From 2017 through 2022, the median GP commit for SPVs between $1 million and $9.9 million hovered between 0.4% and 0.9% each year. In 2023, however, it rose to 1.8%—more than twice as high as in any other year on record.

Among SPVs with less than $1 million under management, the median percentage of all capital that was contributed by the GP has fluctuated by multiple percentage points in recent years. This can be explained in part by the relative size of these funds: For an SPV with $500,000 under management, the difference between a 2.3% commitment from the GP and a 0.4% commitment is less than $10,000. At such a small vehicle size, small variations in dollar amounts can have an outsized impact.

SPV investment metrics

Below we dig into a few major performance metrics for institutional SPVs.

If you’d like to join the waitlist for an expanded SPV performance report to be released in Q1 2025, you can do so here.

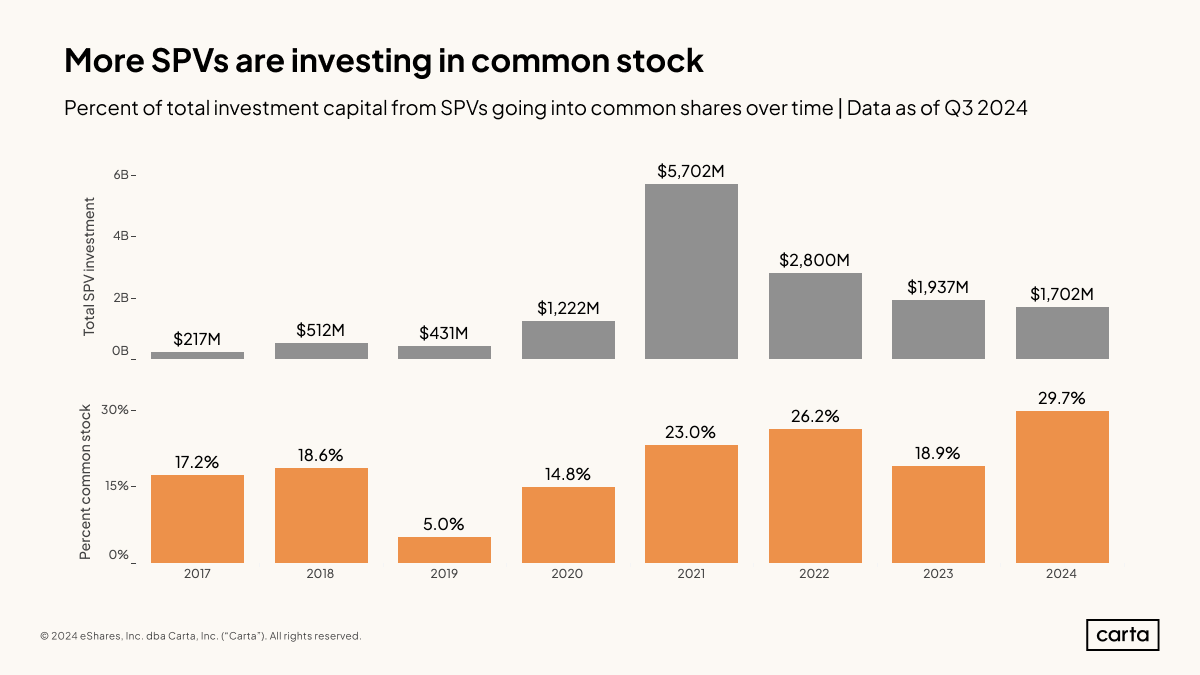

In general, SPVs have become more likely over the past several years to acquire common shares in the companies they back, as opposed to preferred shares or convertible notes. This could indicate an increase in SPVs being used for secondary transactions.

There have been some exceptions to this larger trend, including 2023, when the percentage of all SPV investment that went into common stock declined significantly. But so far in 2024, common stock comprised nearly 30% of all SPV investment, which would be the highest annual rate on record.

The recent declines in overall investment from SPVs, however, means that total SPV spending on common stock has declined, too, even with the percentage of all capital that goes toward common stock on the rise. In 2021, SPVs on Carta deployed about $1.31 billion in purchases of common stock, compared to $505.5 million in 2023.

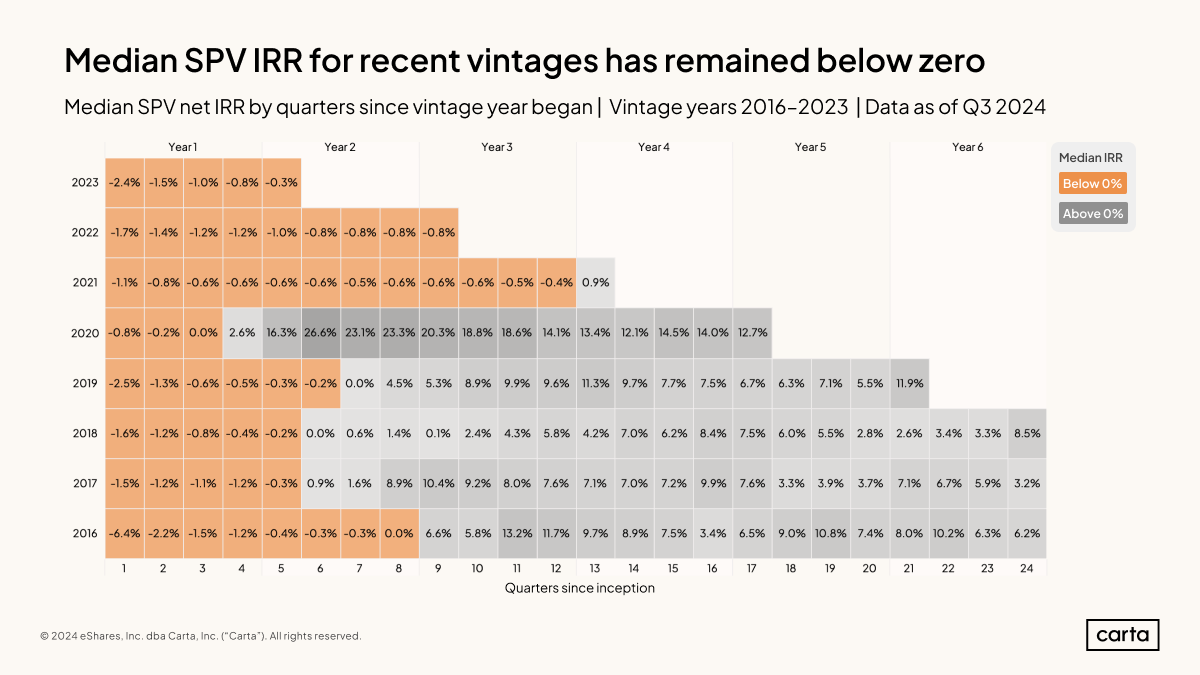

Internal rate of return (IRR) measures the annualized return on investment that an SPV has produced. It’s one of the main ways that investors track an SPV’s performance before the SPV has realized any liquid returns.

IRR typically remains below zero for the first several quarters after an SPV’s inception. The 2021 and 2022 vintages, however, have taken longer to break into the black. The median IRR for SPVs formed in 2021 didn’t turn positive for 12 quarters. At that same juncture, the median IRR for SPVs from 2018 had already been above zero for two full years.

It’s to be expected that more recent vintages will have lower IRRs, since these vehicles have had less time to work with their investments and create value. But this comparison across time shows that something has shifted. The fact that recent vintages have lower IRRs than earlier vintages at the same point in time is likely due in no small part to market conditions: Venture valuations began to decline during 2022, meaning SPVs raised in 2021 and later missed out on investing in the recent venture boom.

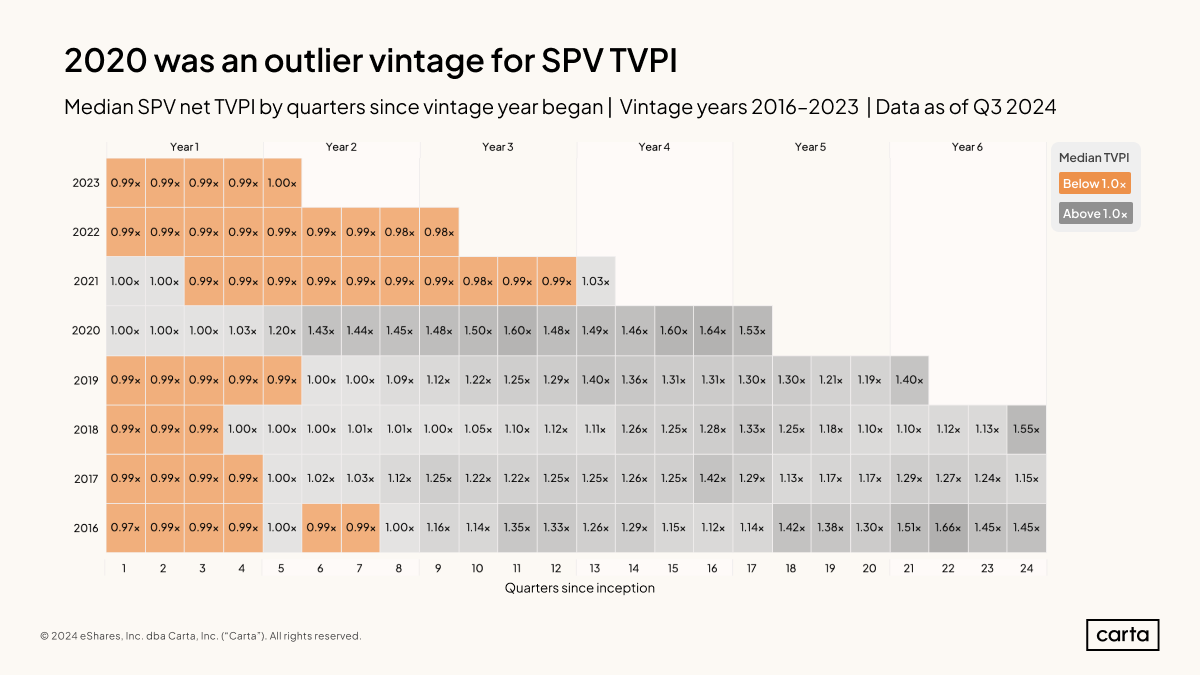

TVPI is another key metric used to measure the performance of active SPVs. It’s expressed as a multiple: A TVPI of 1x means that the current value of the investment is the same as the value of the initial investment. A TVPI of 1.5x means the value of the investment has increased one-and-a-half times over.

For the 2016 through 2019 vintages, it was typical for the median TVPI among SPVs to be below 1x for the first year or so since inception, then rise above 1x after that. In the past four years, however, this has changed. The 2020 vintage posted a median TVPI at or above 1x immediately, with no quarters of negative performance. For the 2021, 2022, and 2023 vintages, it’s been the opposite: Their negative performance has persisted for far longer than was previously typical.

Methodology

SPV Structure

All 2,442 SPVs in this report are US-domiciled, direct-investment, and institutional in nature. If an SPV has left Carta, data from that SPV is filtered out from that date onward.

SPV Performance

Net IRR and net TVPI are both net of fees and carry. Vintage date is defined as the date of first capital call.

Join the waitlist for the expanded SPV report

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. © 2026 Carta. All rights reserved. Reproduction prohibited.