Executive summary

As we enter the second half of the 2020s, venture investors are being increasingly selective about which companies they choose to back. The bar that a startup must clear in order to successfully raise VC funding may be as high as it’s ever been.

But for the startups that are able to clear this lofty bar, there’s no shortage of investor interest. This competition among VCs for high-end deals is one factor that’s driving up pre-money valuations across the breadth of the venture landscape, even as deal counts dwindle.

The median pre-money valuation in new seed rounds on Carta was $16 million in Q1 2025, about 18% higher than it was a year earlier. The number of seed rounds that took place, however, plunged over that same span, declining by 28%.

At Series A, the median pre-money valuation reached $48 million in Q1, up 9% from the year before. At the same time, the number of closed Series A rounds fell by 10%.

These trends are unfolding at almost every phase of the venture fundraising lifecycle. At each stage from seed through Series C, median valuations are higher than they were a year ago. And yet fewer deals are taking place.

Q1 highlights

Lower dilution at every stage: Median dilution in new funding rounds has declined over the past year at every stage from seed through Series D. The median Series A round in Q1, for instance, involved 17.9% dilution, down from 20.9% just a year earlier.

Fewer deals, fewer dollars at seed: Startups on Carta combined to raise just 401 new seed rounds in Q1, down 28% year over year. And those seed rounds combined to bring in just $1.2 billion, a 37% year-over-year reduction.

Longer waits at Series B: The median company that raised a Series B round in Q1 2025 had waited 2.8 years since their Series A, the longest median interval on record. With fewer rounds taking place, companies must make the most of their existing runway.

Key trends

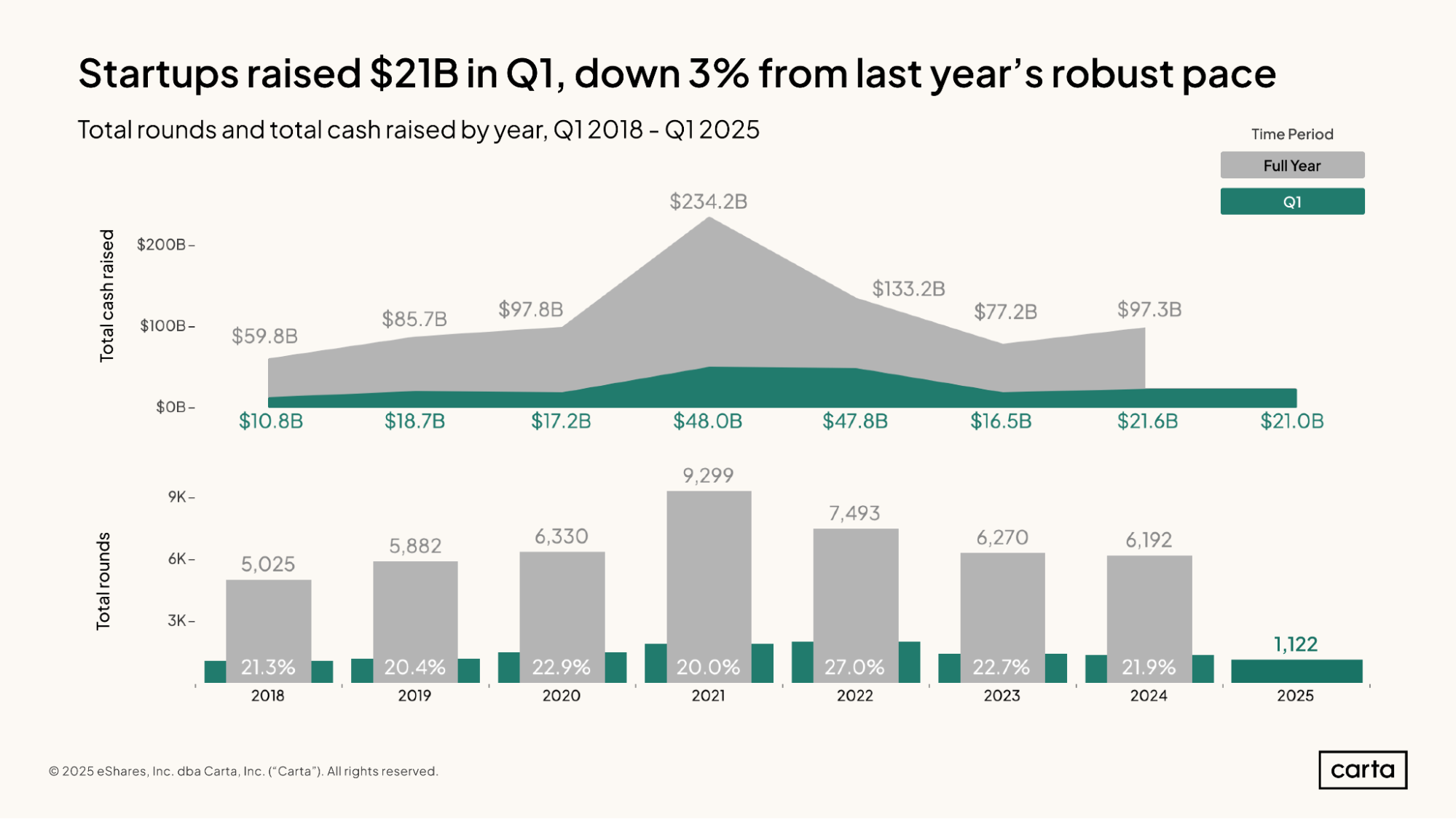

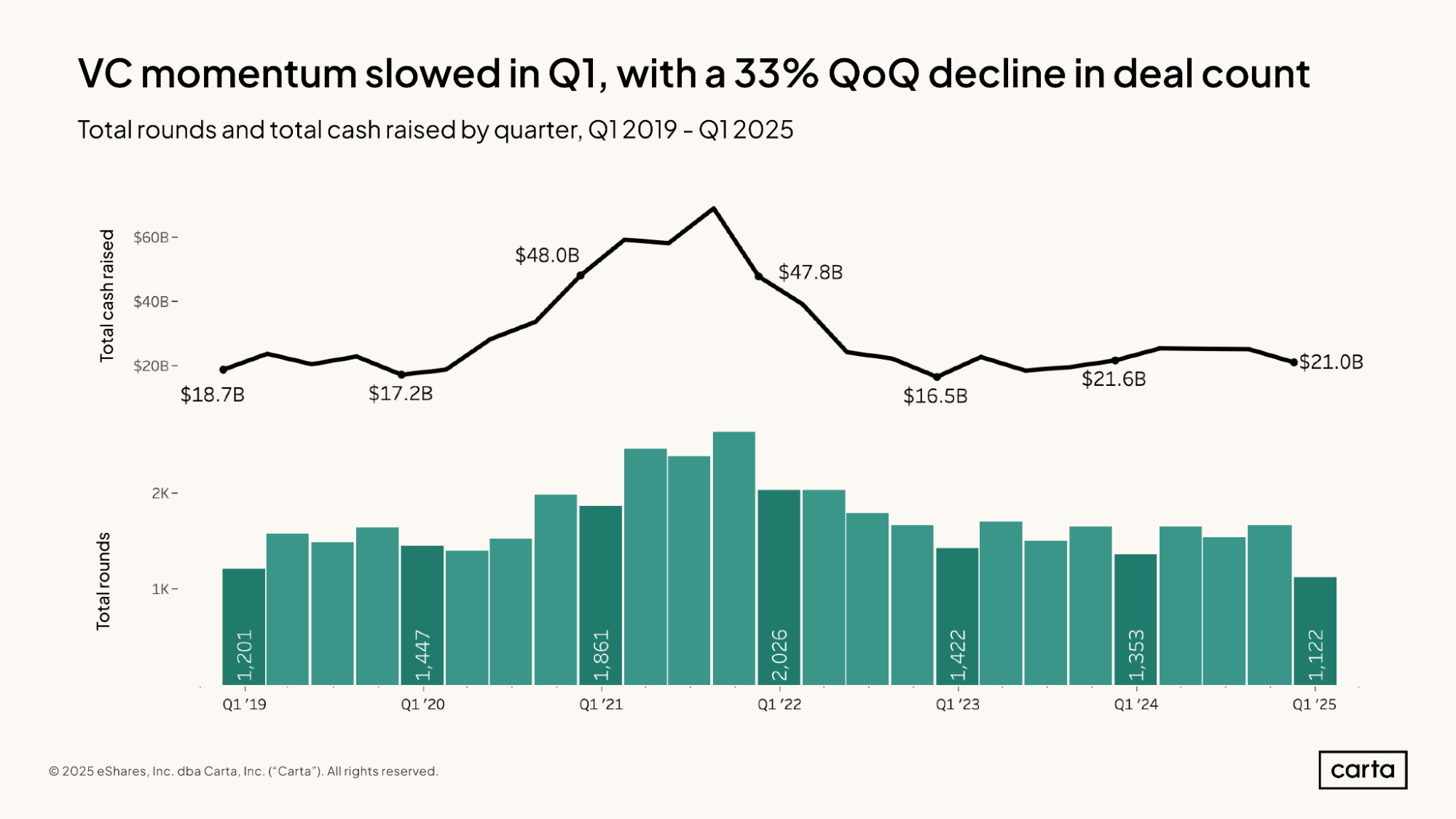

After nearing the $100 billion mark in 2024, the startup fundraising market got off to another healthy start in 2025, with $21 billion in capital raised across Q1. That’s in line with the $21.6 billion sum that startups on Carta combined to raise one year ago, in Q1 2024.

Despite these relatively high dollar amounts, the rate of new investments began to slow in Q1. Startups completed just 1,122 new funding rounds between the start of January and the end of March, the lowest Q1 total since 2018.

This quiet Q1 came after the venture market ended 2024 on an upward trend. In Q4, companies on Carta had combined to close 1,663 new rounds, which was the highest total in the past six quarters. Compared to this strong prior quarter, deal activity in Q1 2025 was down 33%, while capital invested was down 16%.

But this isn’t entirely unexpected. As a general rule, venture activity tends to accelerate as the year goes on. In four of the past six years, Q1 has had the lowest quarterly deal count of any quarter, and Q4 has had the highest. From 2019 through 2024, the average Q4 saw 20% more deal activity than the average Q1.

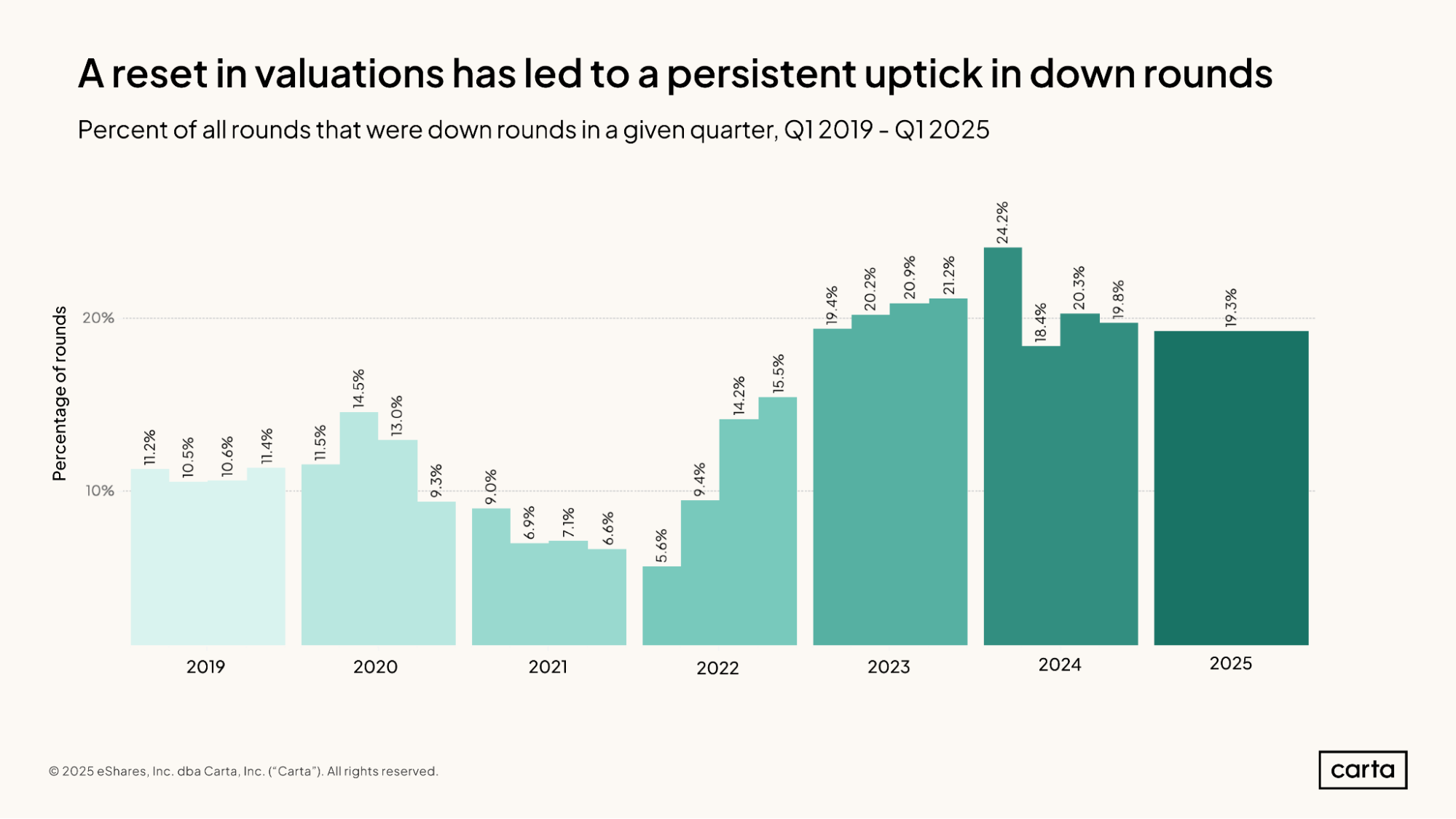

Just over 19% of all new rounds closed on Carta in Q1 2025 were down rounds, with the company receiving a lower valuation than in their previous funding round.

This is in line with the typical frequency of down rounds since the start of 2023. But it’s much higher than the typical down-round rate from 2019 through 2022. This increase in the frequency of down rounds aligns neatly with the broad-based downturn in venture-backed valuations that began in mid-2022. As companies who last raised cash in the record-breaking boom of 2021 and early 2022 return to the market, many have been forced to accept lower valuations.

Full report available: Start reading now for free

Our complete State of Private Markets Q1 2025 report includes more than 20 additional charts and analysis on fundraising and valuation at all stages, deal terms, dilution, geographical trends, and more.

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. © 2026 Carta. All rights reserved. Reproduction prohibited.