There has been tremendous upheaval in the venture capital markets since interest rates began to rise in early 2022.

Fundraising has slowed. Liquidity has become scarce—due not only to a dearth of IPOs but lackluster M&A as well.

Against that backdrop, fund managers have found themselves in a heightened competition for limited partner dollars across many asset classes.

So how can fund managers make the case that they deserve a greater allotment of LP cash? Better data, especially for small funds, might help.

We’re excited to introduce the first VC Fund Performance report from Carta, based on aggregated and anonymized metrics from 1,803 venture funds currently using Carta Fund Administration.

Carta serves more than 3,000 venture firms across many categories, so we’ve narrowed this analysis in a few ways to make it more impactful. Only U.S. funds are included, and all included funds are direct venture investors (as opposed to funds of funds). Funds must have been in vintage years 2017 through 2022. More detail on our methodology can be found at the end of this report.

Each vintage year includes at least 120 underlying funds (and far more in most vintages). As such, we believe this analysis represents a dramatic expansion of the public data available for small VC fund performance.

Note that this report includes data from funds over $100 million, a traditional delineation point between emerging and established managers.

Highlights

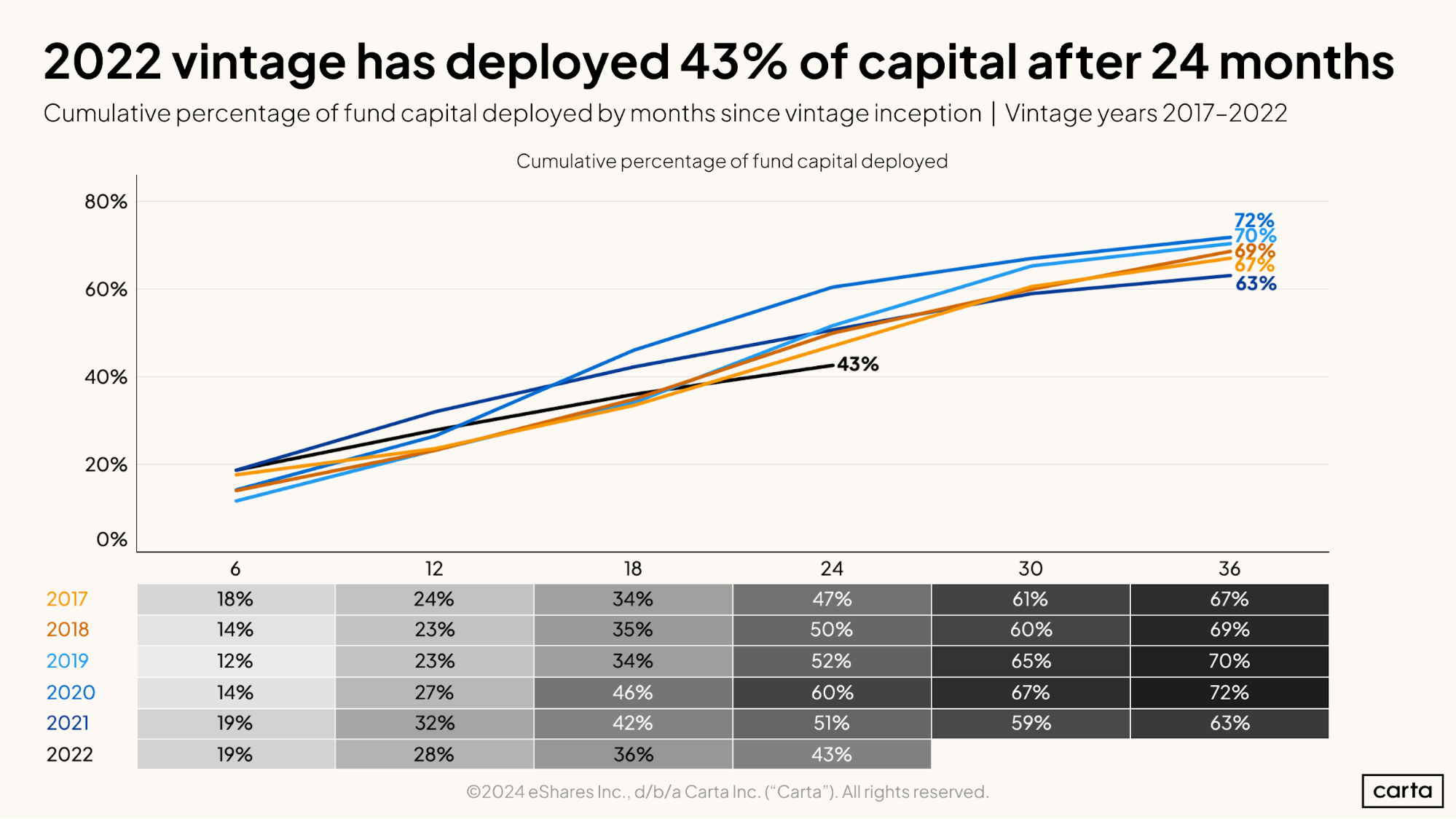

Slow capital deployment: Funds in the 2022 vintage have deployed about 43% of their committed capital at the 24 month mark, the lowest share of any analyzed vintage. Prior vintages ranged from 47%-60% after 24 months.

Graduation rates declining: 30.6% of companies that raised a seed round in Q1 2018 made it to Series A within two years. Only 15.4% of Q1 2022 seed startups did so in the same timeframe.

Distributions back to LPs remain elusive: Less than 10% of 2021 funds have had any DPI after 3 years.

Fund details & deployment

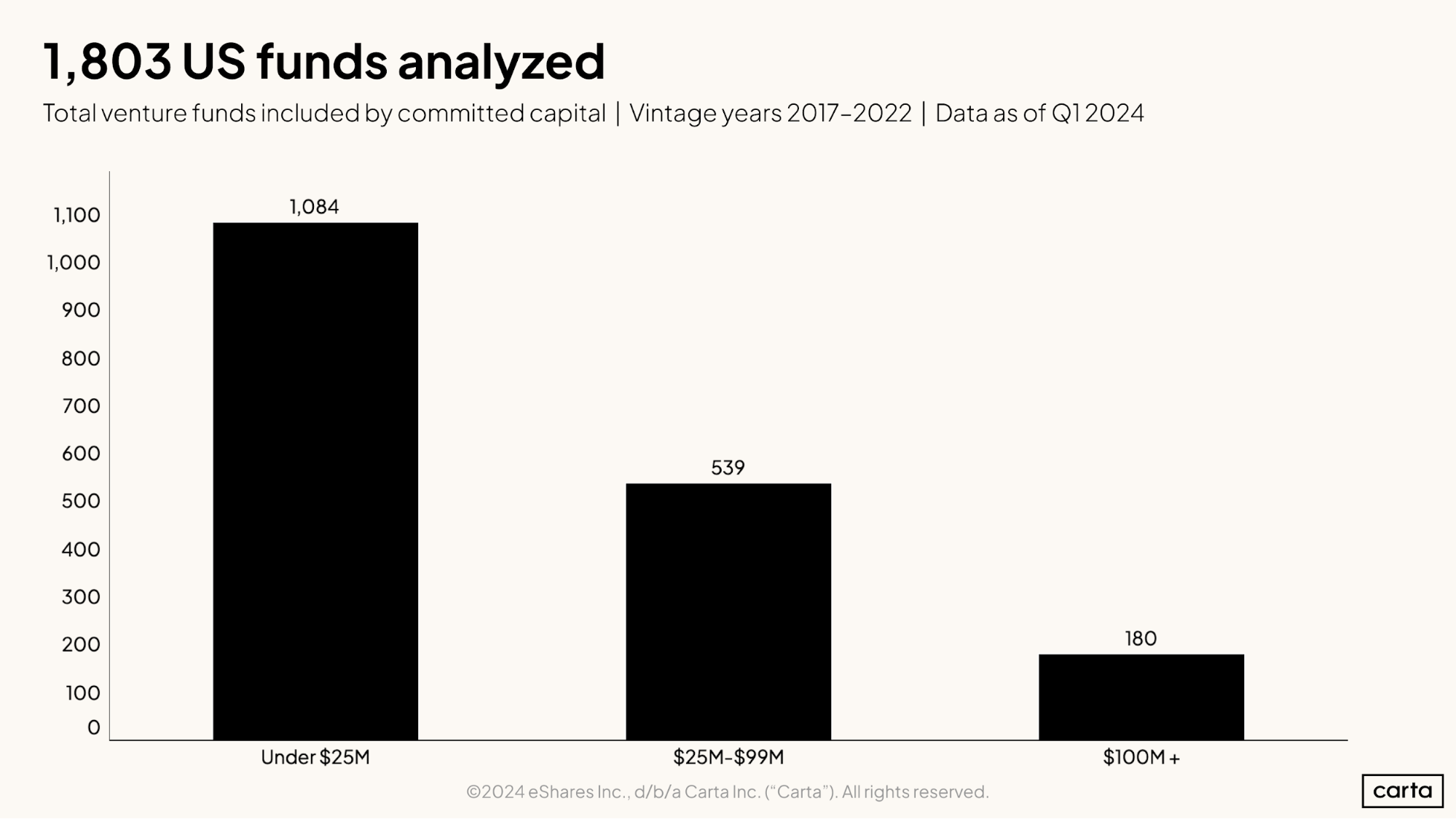

This report is based on data from 1,803 venture funds, ranging in vintage year from 2017 to 2022. A majority of these funds—about 60%—received less than $25 million in capital commitments. Another 30% of funds are between $25 million and $100 million in size, while 10% are $100 million or larger.

This distribution of funds by size makes intuitive sense. Emerging managers may start by raising a small fund, while far fewer have the sort of track record, industry connections, and firm infrastructure required to raise a fund of $100 million or more.

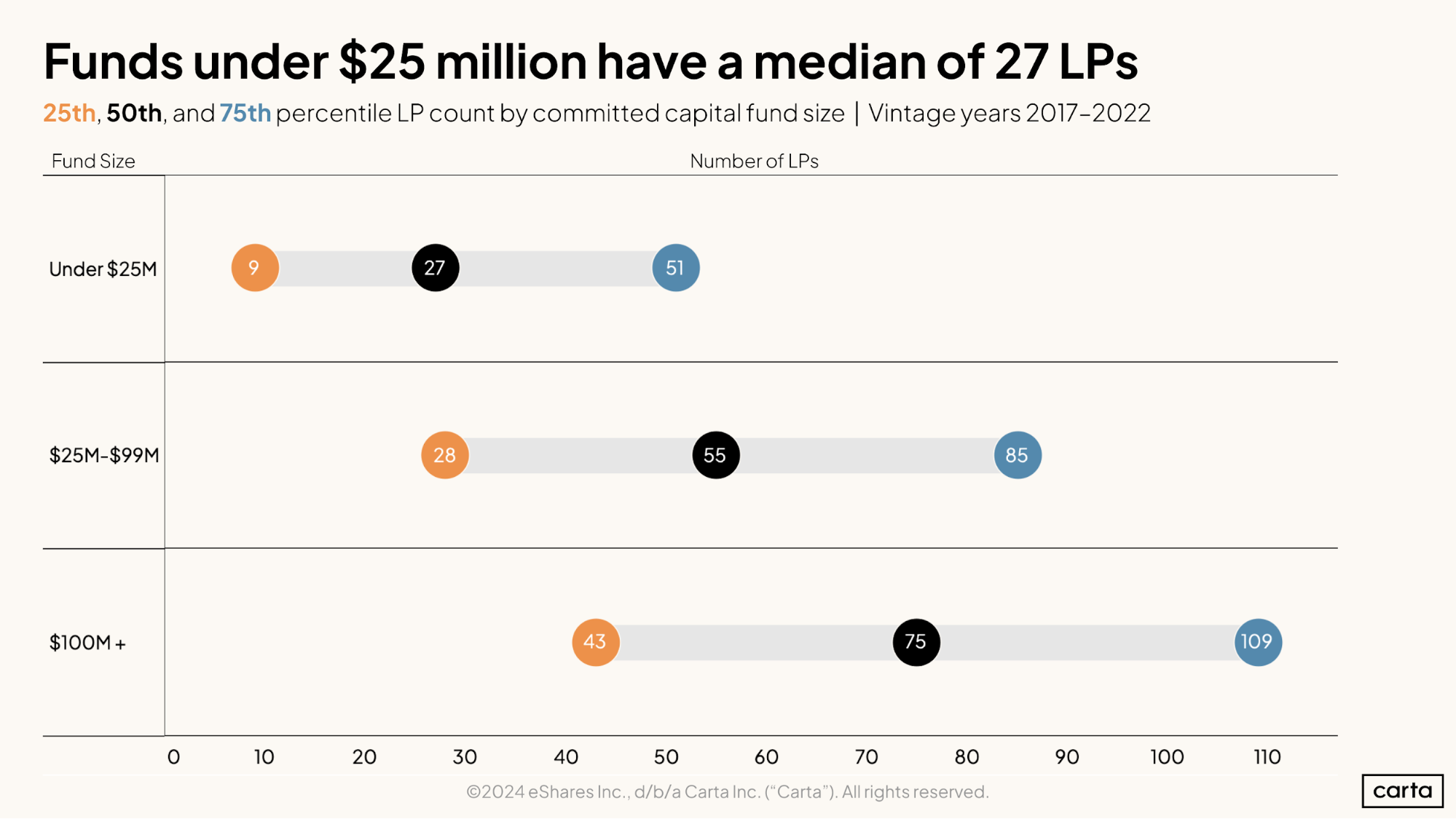

The larger the venture fund, the more LPs it tends to have. But there’s considerable variation in the size of the LP base of different funds, even funds that are roughly the same size.

Among the smallest category of funds—those with less than $25 million in commitments—the median fund closed between 2017 and 2022 had 27 LPs. A fund at the 25th percentile would have 9 LPs, and one at the 75th percentile would have 51.

Funds with $100 million or more in commitments typically have far more LPs, but the gap between the 25th percentile (43 LPs) and the 75th percentile (109 LPs) is similarly wide. For a venture firm, managing more than a hundred different LP relationships can be a much larger lift than managing a few dozen.

The velocity with which capital deploys has steadily decreased after peaking with the 2020 fund vintage. Cumulative capital deployment percentage after 24 months (total dollars deployed / dollars raised at point t) dropped from 60% for the 2020 fund vintage to 43% for the 2022 fund vintage. This points to a larger trend in private capital markets - investors are slowing down the pace of investments as the market reset continues.

Download the full report

To see our analysis of fund performance metrics—such as IRR, TVPI, and DPI by fund vintage year—download the full Q1 2024 Fund Performance report:

Methodology

Carta helps over 3,000 venture firms administer more than $150 billion in capital. We're setting a new standard in fund administration by sharing insights from our unmatched dataset about the private markets and venture ecosystem to help investors and limited partners make informed decisions and understand market conditions.

Overview

This study uses an aggregated and anonymized sample of Carta fund customer data. Funds that have contractually requested that we not use their data in anonymized and aggregated studies are not included in this analysis.

We use data through the end of Q1 2024. Historical data may change in future studies because there is typically an administrative lag between the time an event took place and when it is recorded in Carta. In addition, new funds signing up for Carta’s services will increase historical data available for the report.

Fund details

This report only includes funds domiciled in the United States. All funds must have reliable performance data dating back to fund inception and/or when they joined the Carta platform. Included funds are direct investors into startups and do not pursue fund of funds or other strategies. Only funds in vintage years between 2017 and 2022 were included.

We define vintage year as the year in which the first cost basis (either conversion or new investment) for a fund occurred.

Values marked “n/a” for specific vintage years in IRR and TVPI due to insufficient performance sample size in earlier time periods.

Financings

Financings include equity deals raised in USD by U.S.-based corporations. The financing “series” (e.g. Series A) is taken from the share class name in their applicable certificate or articles of incorporation. Financing rounds that don’t follow this standard are not included in any data shown by series but are included in data not shown by series. Primary rounds are defined as the first equity round within a series. Bridge rounds are defined as any round raised after the first round in a given series.

DISCLOSURE: This communication is on behalf of eShares Inc., d/b/a Carta Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. ©2024 eShares Inc., d/b/a Carta Inc. ("Carta"). All rights reserved. Reproduction prohibited.